Written by

Eric

Share this article

.svg)

Subscribe to updates

I still remember the days when "underwriting" meant sitting at a desk buried under piles of W-2s, bank statements, and tax returns, highlighting guidelines in thick physical binders. If you're a loan officer or a broker in today's market, you know that those days are, thankfully, mostly behind us.

Whether you are an independent broker trying to scale or a lender looking to slash "time-to-close," mortgage underwriting automation has become the engine of our industry. In this guide, I'll break down what this technology actually is, how it's changing the way we work, and which tools are actually worth your time.

What is Mortgage Underwriting Automation?

Mortgage underwriting automation is the use of technology, specifically algorithms and AI, to evaluate a borrower's creditworthiness against specific lending guidelines. While "Manual Underwriting" relies on a human to cross-check every detail of a 1003 application against a handbook, automation does the heavy lifting in seconds.

I like to think of it as a bridge between raw data and a final "yes." In the US, this usually takes the form of an Automated Underwriting System (AUS). It doesn't just calculate numbers. It applies logic to determine if a loan fits the risk profile of an investor. We need this because today's borrowers expect instant answers. If you can't provide a pre-approval in minutes, they'll find a broker who can.

Key Features often include:

- Data Integration: Automatically pulling credit reports, income verification (VOE/VOI), and asset data.

- Rule-Based Engines: Instant matching against Fannie Mae, Freddie Mac, or private investor guidelines.

- Risk Scoring: Analyzing DTI (Debt-to-Income) and LTV (Loan-to-Value) ratios in real-time.

- Conditional Approval Generation: Creating a "needs list" for the borrower immediately.

- Fraud Detection: Identifying inconsistencies in social security numbers or employment history.

- Document Recognition (OCR): "Reading" uploaded PDFs to extract relevant financial data.

Also Read:

- Should Mortgage Lender and Broker Build In-House AI Tools?

- AI Mortgage Underwriting Explained: Will You Be Replaced?

- What Conditions Will Underwriting Ask for? Get to Know

Benefits of Automated Mortgage Underwriting

In my experience, the biggest shift hasn't just been speed. It's the peace of mind. Here is why I believe every modern professional needs to embrace these tools:

- Massive Time Savings: Massive Time Savings: You can save days of processing time per loan file, often 40-60% faster, by removing the manual "stare and compare" work.

- Reduced Human Error: AI doesn't get tired at 4:00 PM on a Friday. It checks DTI with 85%+ accuracy every single time.

- Faster Pre-Qualifications: You can deliver results up to 2.5x faster, which is often the difference between winning a deal and losing it.

- Scalability: You can handle a sudden surge in volume without needing to double your staff.

- Transparency: Modern tools provide clear citations, showing exactly why a borrower was or wasn't eligible.

- Improved Conversion: When borrowers get a 5-minute application experience, they are much more likely to hit "submit."

Limitations of Mortgage Underwriting Automation

I'd be lying if I said technology solved everything. We still need humans in the loop for several reasons:

- Complexity "Edge Cases": If a borrower has five different self-employment income streams and a unique legal situation, a standard AUS might struggle.

- Data Quality Issues: "Garbage in, garbage out." If the initial data entry is wrong, the automation will confidently give you the wrong answer.

- The "Human Touch": Automation can't explain a denial to a disappointed first-time homebuyer with empathy.

- Over-reliance Risk: I've seen junior LOs stop learning the guidelines because they trust the software too much, which can be dangerous during an audit.

- Regulatory Shifts: AI models must be constantly updated to stay compliant with changing fair lending laws.

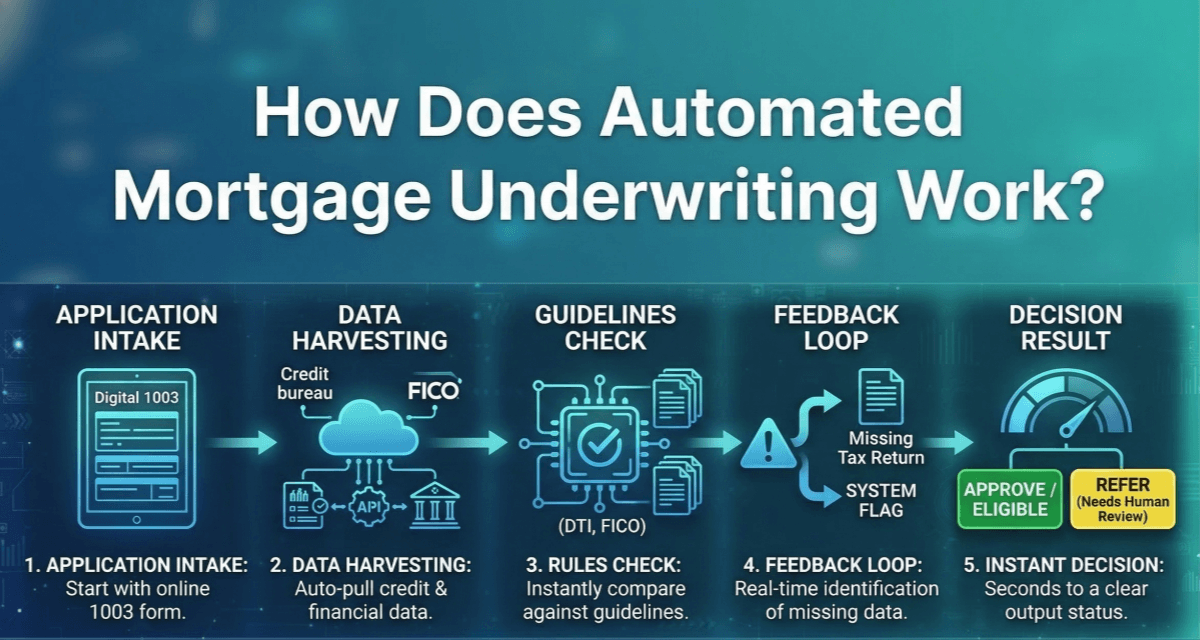

How Does Automated Mortgage Underwriting Work?

The process is more straightforward than it sounds. Once a borrower starts an application, the "Digital 1003" acts as the intake valve.

- Data Harvesting: The system pulls data from credit bureaus and financial institutions via API.

- The "Check" Phase: The engine compares this data against thousands of pages of guidelines (e.g., "Is the DTI under 43%? Is the credit score above 620?").

- The Feedback Loop: If something is missing, like a missing year of tax returns, the system flags it instantly.

- The Decision: Within seconds, the system outputs an "Approve/Eligible" status or a "Refer", which means a human needs to take a closer look.

Tools that Provide Mortgage Underwriting Automation

Fannie Mae's Desktop Underwriter (DU)

Best for: Standard Conventional and High-Balance loans being sold to Fannie Mae.

DU is essentially the "North Star" of the American mortgage industry. Since its launch in the 90s, it has set the standard for what a digital approval looks like.

Features:

- Instant "Approve/Eligible" decisions.

- Direct integration with almost every Loan Origination System (LOS).

- Validated income, asset, and employment data through the Day 1 Certainty® program.

- Extensive support for 2-4 unit properties and manufactured homes.

- Comprehensive "Findings" report that outlines exactly what documentation is required.

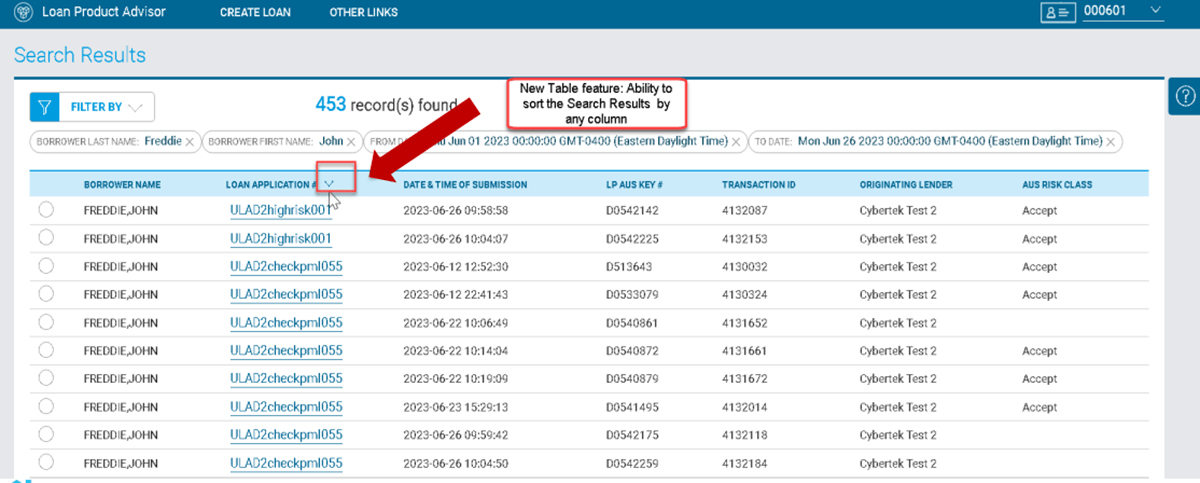

Freddie Mac's Loan Product Advisor (LPA)

Best for: Lenders who want a second opinion or specifically target Freddie Mac's secondary market.

LPA is Freddie Mac's answer to DU. While similar, its risk assessment algorithms can sometimes offer a different result, which is why most brokers I know run both.

Features:

- Streamlined "Asset and Income Modeler" (AIM) to reduce documentation.

- Integrated credit reporting from all three major bureaus.

- Real-time feedback on loan eligibility.

- Specific "ChoiceHome" features for affordable housing initiatives.

- Automated collateral evaluation (ACE) to potentially skip the appraisal.

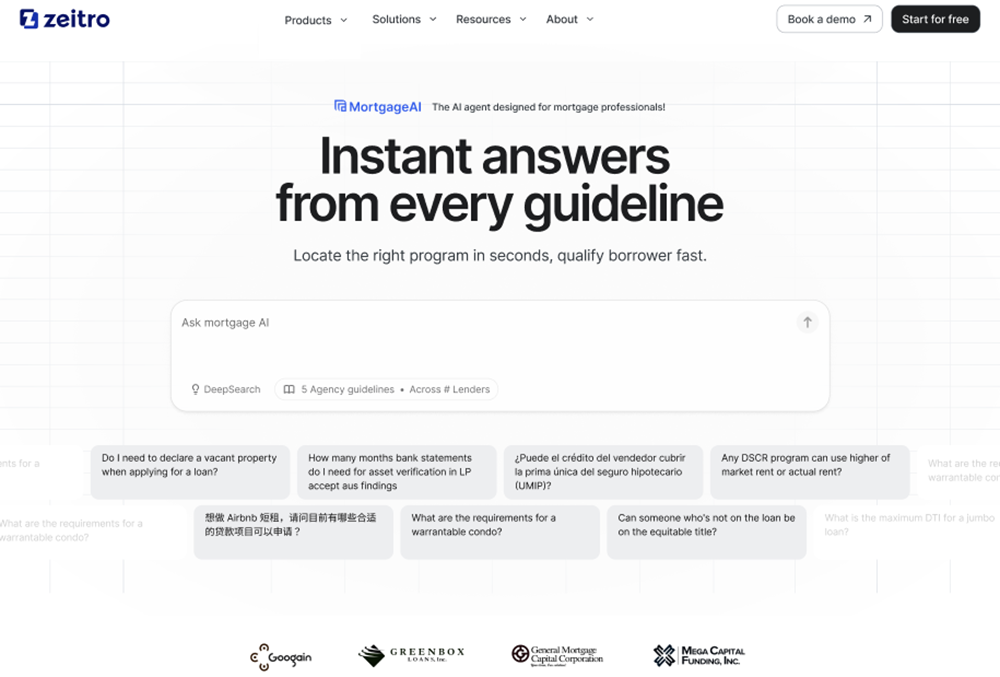

Zeitro's AI Mortgage SaaS

Best for: Modern brokers and LOs who handle complex Non-QM loans and need a "neutral" AI assistant.

I've found Zeitro to be a game-changer because it's not tied to a specific lender. It's an "AI Agent" that feels like having a senior underwriter sitting right next to you, ready to answer questions about 300+ different guidelines instantly.

Features:

- Zeitro Strata AI: A specialized assistant that lets you query complex QM and Non-QM guidelines (DSCR, ITIN, Bank Statement loans) and get answers with citations in seconds.

- Digital 1003 (POS): A borrower-facing portal that achieves 90%+ completion rates and exports data in FNM 3.4 format.

- DeepSearch Technology: It cross-checks over 100 investors to find a "home" for your difficult files.

- AI DTI Calculator: Instantly computes complex ratios using AI-driven tools to ensure pre-qual precision.

- Personalized Microsites: Tools like Bluerate help LOs build their brand and attract organic leads through SEO-optimized pages.

FAQs about Mortgage Underwriting Automation

Q1. Will automation replace human underwriters?

No. It replaces the "busy work." Humans are still needed for final sign-offs, complex problem-solving, and managing the nuances of high-net-worth or atypical borrowers.

Q2. Can I use these tools for Non-QM or DSCR loans?

Standard systems like DU/LPA aren't built for Non-QM loans. That's where tools like Zeitro Strata AI shine. They are specifically designed to handle the "outside-the-box" guidelines that traditional banks won't touch.

Q3. Is my borrower's data safe?

If you choose the right tools, yes. For example, Zeitro is SOC 2 Type II certified, meaning they meet the "gold standard" for enterprise-grade security and data protection.

Q4. How much does this technology cost?

It varies. While GSE systems have transaction fees, modern SaaS tools like Zeitro offer "freemium" models, with professional tiers as low as $8/month, making it accessible even for one-person shops.

Q5. How accurate is the income calculation?

Top-tier AI tools now reach over 85% accuracy in income calculation, significantly reducing the "back-and-forth" during the processing stage.

Final Word

Moving toward automation isn't just about following a trend. It's about survival in a margin-compressed market. By offloading the repetitive guideline research and data entry to AI, we get to spend more time doing what we actually get paid for: building relationships and closing deals.

My Recommendations:

- For Conventional Prowess: Master Fannie Mae's DU. It's the industry's backbone for a reason.

- For Complex & Non-QM Deals: Use Zeitro Strata AI. It's the fastest way to verify eligibility for DSCR, ITIN, or Bank Statement loans without reading 500-page PDFs.

- For Client Intake: Implement Zeitro's Digital 1003. Your borrowers will love the 5-minute mobile experience, and you'll love the auto-generated FNM 3.4 files.

People Also Read

- What is Mortgage Eligibility Checker? Best Tool to Verify Guidelines

- Best Mortgage Underwriter Software: AI & Guideline Verification

- 6 Best Loan Origination Software for LOs/Brokers

- Best CRM for Loan Officers: Which One Suits You Most?

- [ Guide] How to Calculate DTI Ratio for Mortgage?