Written by

Eric

Share this article

.svg)

Subscribe to updates

Last checked and updated in July, 2026.

Have you ever found the perfect rental property, run the numbers, and known it was a home run, only to get stuck behind a mountain of paperwork at a traditional bank? I've been there. Nothing kills a good deal faster than a loan officer pulling two years of my tax returns and telling me my Debt-to-Income (DTI) ratio is too high for another property.

So what if there were a mortgage where the lender didn't care about your paycheck at all? Where the only question was: does the property itself make money?

That's the whole idea behind a DSCR loan, and for a lot of investors, it's become the quiet workhorse behind scaling a rental portfolio. In this guide, I'll walk through what the term actually means, how the loan works, what it costs, and the questions I get asked most often by investors weighing this option for the first time.

What is a DSCR Loan?

Before we get to the loan, it helps to understand the metric behind it. DSCR stands for Debt Service Coverage Ratio. It's a simple idea borrowed from commercial real estate: does a property generate enough income to cover its own debt payments, without any help from the owner's paycheck?

A DSCR Loan, therefore, is a type of Non-QM loan designed specifically for real estate investors. Unlike a conventional mortgage that relies heavily on your personal W-2 income or tax returns, a DSCR lender focuses almost entirely on the income potential of the property itself.

Worth noting: DSCR as a concept isn't new. Commercial lenders have used it for decades to underwrite apartment buildings, office parks, and shopping centers, usually calculating it off a property's audited financial statements and net operating income. What's newer is applying that same logic to single-family rentals and small multifamily properties, which is largely a product of the Non-QM market rebuilding itself after 2008. Instead of pulling financial statements, residential DSCR lenders typically lean on an appraiser's rent estimate — a difference worth keeping in mind if you've seen the term used in a commercial lending context and assumed it worked the same way.

The Key Difference:

- Traditional Loans: The lender asks, "Can YOU afford to pay this mortgage with your salary?" They look at your DTI, pay stubs, and employment history.

- DSCR Loans: The lender asks, "Can THE PROPERTY pay this mortgage with its rent?" They look at the property's cash flow.

One more thing worth flagging up front: DSCR loans are strictly for investment properties. You can't use one to buy the house you plan to live in — that's a business-purpose loan, not a consumer mortgage, and lenders treat that distinction seriously.

If you're comparing the two side by side, here's the simplest way to think about it: DTI measures you, DSCR measures the asset. A conventional lender adds up your monthly debts and divides by your gross income. A DSCR lender does something similar, but with the property's rent standing in for your paycheck and PITIA standing in for your debts. Same math logic, completely different subject.

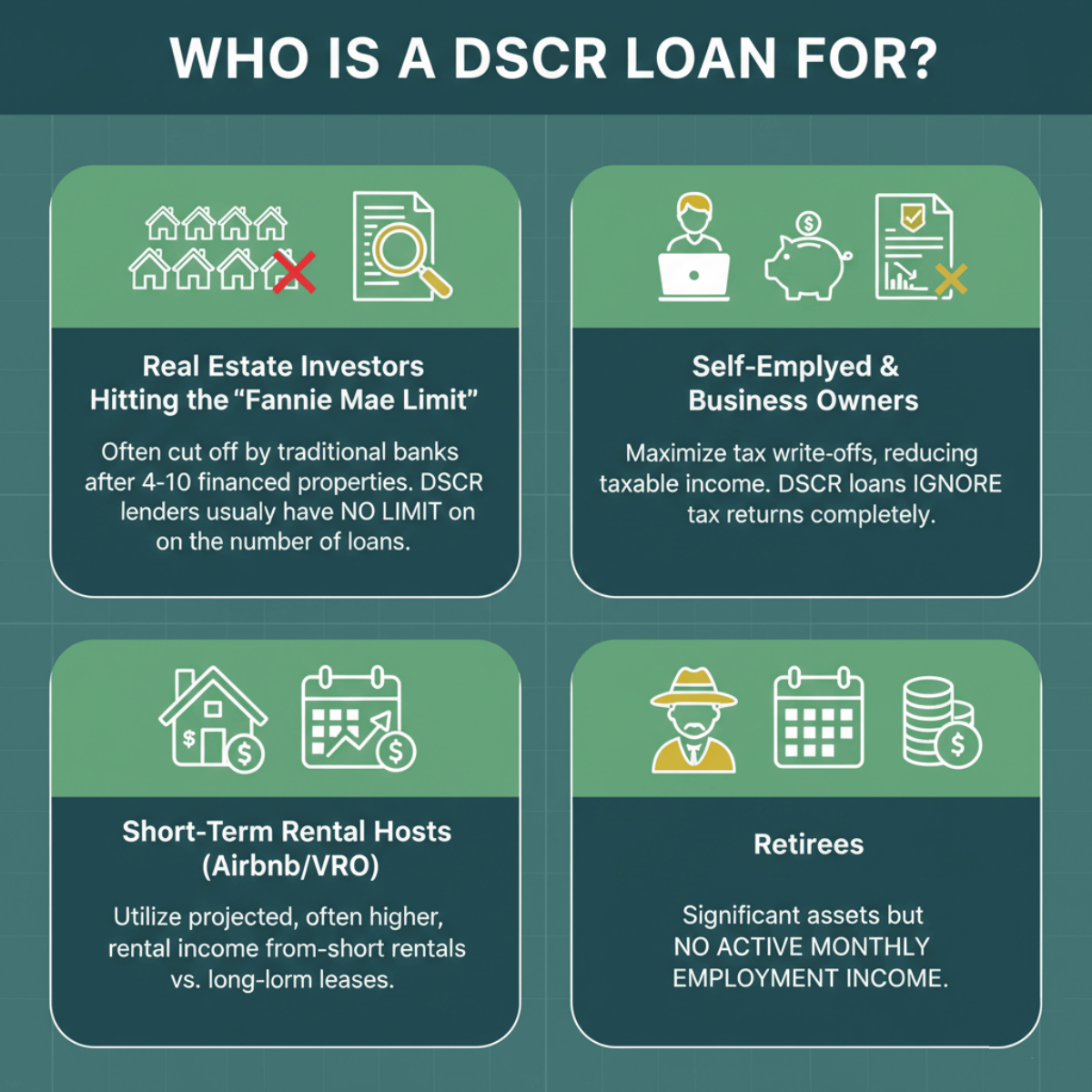

Who is a DSCR Loan for?

This isn't a loan for every buyer, but for a handful of specific situations, it's genuinely one of the better tools available:

- Investors who've hit the "Fannie Mae limit." Fannie Mae caps conventional financing at 10 financed one-to-four-unit properties per borrower, including your primary home, and plenty of individual lenders cap it even lower, often somewhere between four and ten. Once you hit that wall, DSCR lenders generally don't count how many rental loans you already carry.

- Self-employed borrowers and business owners. If you write off aggressively to lower your tax bill, you probably look "poor" on paper even when your actual cash flow is healthy. A DSCR loan skips the tax return conversation entirely.

- Short-term rental hosts. Airbnb and VRBO income can be counted toward your DSCR calculation, and it's often higher than what a long-term lease would show, which can work in your favor.

- Retirees and asset-rich, income-light buyers. If you're sitting on savings or a paid-off portfolio but don't have a monthly paycheck to show a lender, this sidesteps that problem completely.

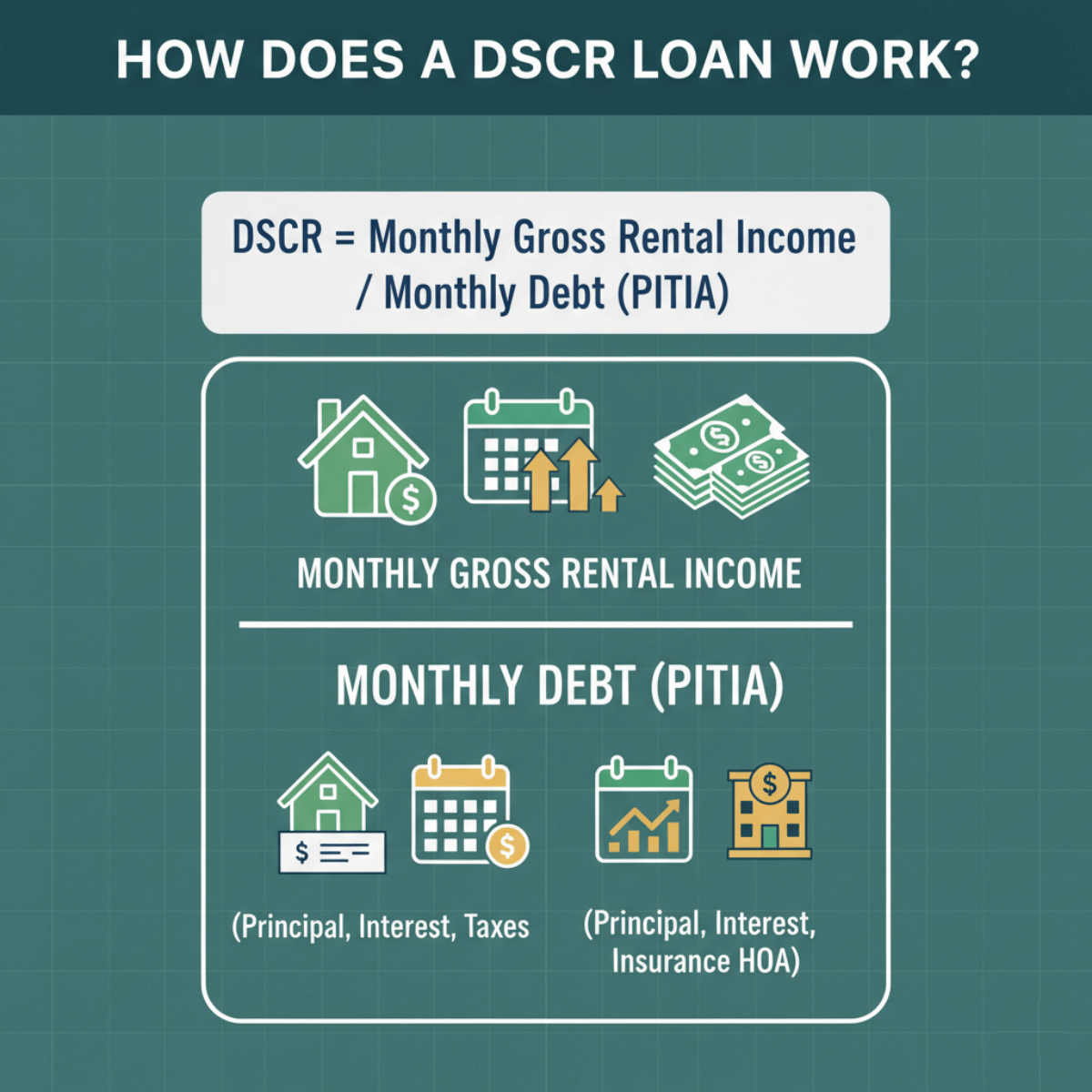

How Does a DSCR Loan Work?

The mechanics of a DSCR loan are surprisingly simple. The lender acts more like a business partner evaluating a project than a bank evaluating a person.

The lender calculates the DSCR Ratio to see if the property is a safe bet. Here is the formula lenders use:

DSCR = Monthly Gross Rental Income / Monthly Debt (PITIA)

- Rental Income: This is determined by a signed lease agreement or, more commonly, by an appraisal report (Form 1007 Rent Schedule) that estimates the fair market rent.

- PITIA: This stands for Principal, Interest, Taxes, Insurance, and HOA fees (if applicable).

Understanding the Score:

- Ratio > 1.0: The property generates more money than it costs. (e.g., A ratio of 1.25 means the property makes 25% more than the mortgage payment). This is the gold standard.

- Ratio = 1.0: The property breaks even.

- Ratio < 1.0: The property is losing money (negative cash flow). Believe it or not, some lenders will still fund these "No-Ratio" deals, but they will require a larger down payment and charge a higher interest rate to offset the risk.

What Loan Terms and Structures Are Available?

This is a piece that gets skipped over a lot, but the structure you pick can change your numbers as much as your rate does. Most DSCR programs offer a 30-year fixed loan as the default, which keeps payments predictable for the life of the loan.

Beyond that standard option, a few structures show up regularly across DSCR lenders:

- 40-year fixed terms, which stretch out the amortization schedule and lower the monthly payment — useful if you're trying to push a tight DSCR ratio above 1.0.

- Interest-only periods, typically the first 10 years, where you pay only interest and none of the principal. This maximizes monthly cash flow (and your DSCR number), though you build no equity through paydown during that stretch.

- Adjustable-rate options, often structured as 5/6, 7/6, or 10/6 ARMs, which usually start with a lower rate than a 30-year fixed in exchange for the rate resetting after the initial period.

None of these are automatically the "right" choice — a 40-year term with an IO period can turn a marginal deal into a qualifying one, but it also means slower equity growth. It's worth running the math both ways before you commit.

Example of DSCR Loan

Let's put this into a real-world scenario so you can see the math in action.

Imagine you want to buy a single-family rental property for $400,000. You plan to put $80,000 down as a down payment.

First, the lender looks at the costs. Let's assume your total monthly payment (Principal, Interest, Taxes, Insurance) comes out to $2,500.

Next, the appraiser assesses the local rental market and determines that this house can rent for $3,000 per month.

Here is the calculation:$3,000 (Rent) ÷ $2,500 (Debt) = 1.20 DSCR

Because 1.20 is greater than 1.0, the property is cash-flow positive. Most lenders would consider this a strong loan application and would likely approve it without asking for a single pay stub from you.

What are Pros and Cons of DSCR Loan?

While DSCR loans offer incredible flexibility, they are not perfect. In the spirit of transparency, here is what you need to weigh before signing the papers.

The Benefits

- No Income Verification: No W-2s, no tax returns, and no employment history checks.

- Scale Faster: Since these loans don't weigh heavily on your personal Debt-to-Income (DTI) ratio, you can keep buying properties as long as you have the down payment.

- LLC Protection: Unlike conventional loans, most DSCR lenders allow (and sometimes prefer) you to close the loan in the name of an LLC, which provides better asset protection.

- Faster Closing: With less paperwork to review, these loans can often close in 2-3 weeks.

The Drawbacks

- Higher Interest Rates: You pay for the convenience. DSCR rates are typically 0.5% to 1.5% higher than a standard conventional mortgage.

- Higher Down Payments: Don't expect 3% or 5% down. Most DSCR lenders require typically 20-25% down (75-80% LTV), up to 80% LTV (20% down) for strong credit (720+), higher if DSCR <1.0 or lower credit.

- Prepayment Penalties: This is a big one. Many DSCR loans come with a "Prepayment Penalty", usually for the first 1-3 years). This means if you sell the house or refinance too quickly, you pay a fee. Please always check this clause!

What are the Requirements of DSCR Loan?

Even though this is a "no-doc" loan, you can't just walk in with zero credentials. Lenders still need to manage their risk. Based on current US lending standards, here is what you generally need to qualify:

- Credit Score: While income doesn't matter, your credit history does. Most lenders require a minimum FICO score, typically 620-680, varying by lender. Some accept 620, others 640-700 for best rates. A score of 700+ will get you significantly better interest rates.

- Down Payment (LTV): The standard requirement is 20% down (80% Loan-to-Value). If your credit score is lower or the DSCR ratio is under 1.0, the lender might ask for 25% or even 30% down.

- Cash Reserves: Lenders want to ensure you can pay the mortgage even if the property sits vacant for a month or two. You typically need to show 3 to 6 months of liquid cash reserves (enough to cover the PITIA payments) in your bank account.

- 1007 Appraisal: You will need to pay for a specific appraisal that includes a "Rent Schedule" to officially determine the market rent.

Is It Hard to Qualify for a DSCR Loan?

Honestly, compared to the grueling process of a conventional mortgage, qualifying for a DSCR loan is significantly easier. You strip away the most stressful variables like your job, your tax write-offs, and your personal debts—and focus entirely on the asset. If the property is a good deal, the loan is usually approved.

However, because these are specialized Non-QM products, you cannot just walk into a big bank like Chase or Wells Fargo to get one. You need to work with specialized lenders who understand this niche. To get the best terms, you should shop around and find the best DSCR lenders who are currently offering the most competitive rates for your specific situation.

In my experience, most denials trace back to one of a few repeat offenders: a DSCR ratio that falls short of the lender's minimum with no compensating factor, a credit score below the program floor, thin cash reserves, or a rent estimate the lender's underwriter simply doesn't buy. Short-term rental income is a frequent sticking point too — if a lender doesn't recognize your platform's income history or the property's condition raises flags at appraisal, the deal can stall even when the borrower looks strong on paper.

Frequently Asked Questions

Does a DSCR loan show up on my personal credit report?

Usually not, if the loan closes under an LLC without a broad personal guarantee — these are treated as business-purpose loans, which sit outside the standard consumer credit-reporting pipeline. Close the loan in your own name, though, and it's likely to appear just like a conventional mortgage would. Either way, expect a hard inquiry on your personal credit during the application itself, even if the loan never shows up as an ongoing account afterward.

Can foreign nationals or UK investors get a DSCR loan?

Yes. DSCR loans have become one of the more common financing paths for international buyers, including UK and Canadian investors, since they don't require U.S. tax returns or a domestic credit history. Expect a higher down payment, typically 25-30%, and plan on working with a lender who specifically handles foreign national programs.

How many DSCR loans can I have?

There's no hard cap the way there is with Fannie Mae's 10-property conventional limit. Most DSCR lenders will keep funding deals as long as your down payment, reserves, and the property's numbers hold up — though individual lenders may set their own internal caps on total exposure.

Can I use a DSCR loan for my primary residence?

No. These are business-purpose loans by definition, reserved for investment properties. If you're buying a home to live in yourself, you'll need a conventional, FHA, or other owner-occupant loan program instead.

Is a DSCR loan a conventional loan?

No — it falls under the Non-QM umbrella, meaning it sits outside Fannie Mae and Freddie Mac's standard underwriting guidelines. That's exactly what gives it the flexibility on income documentation that conventional loans don't offer.

Are DSCR construction loans available?

Not commonly, and not in the way people expect. Most DSCR programs require a property that's already rent-ready or close to it, since the whole underwriting model depends on an appraiser estimating market rent. Ground-up construction typically runs through a short-term bridge or hard money loan first, with a refinance into a DSCR loan once the property is built and leased.

Conclusion

A DSCR loan is a powerful tool in a real estate investor's toolkit. It unlocks the ability to buy properties based on their potential rather than your personal history. For self-employed individuals or investors looking to scale beyond a few properties, it offers a freedom that traditional financing simply cannot match.

However, it's not "free money." You must be comfortable with a slightly higher interest rate and a larger down payment. But if the numbers work and the cash flow is positive, the premium is often a small price to pay for the speed and flexibility to close the deal.

People Also Read

- 8 Best Non-QM Mortgage Lenders in 2026: Which to Choose?

- Breakdown: How Much Does It Cost to Refinance a Mortgage?

- 2026 Guide: How to Get NMLS License? All the Details