Written by

Eric

Share this article

.svg)

Subscribe to updates

Over my decade in the mortgage industry, I've watched real estate investment loans skyrocket. But here's the reality: every lender's Debt Service Coverage Ratio (DSCR) approval standards are vastly different. Spending hours manually digging through massive PDF matrices to see if a deal pencils out is a major pain point that kills pipeline momentum. Fortunately, mortgage tech has caught up.

Using Zeitro's Scenario AI, loan officers can now use a simple chat interface to quickly verify different lenders' DSCR mortgage guidelines. You can finally ditch the manual document hunting and drastically boost your workflow efficiency. Let's break down what these guidelines look like today.

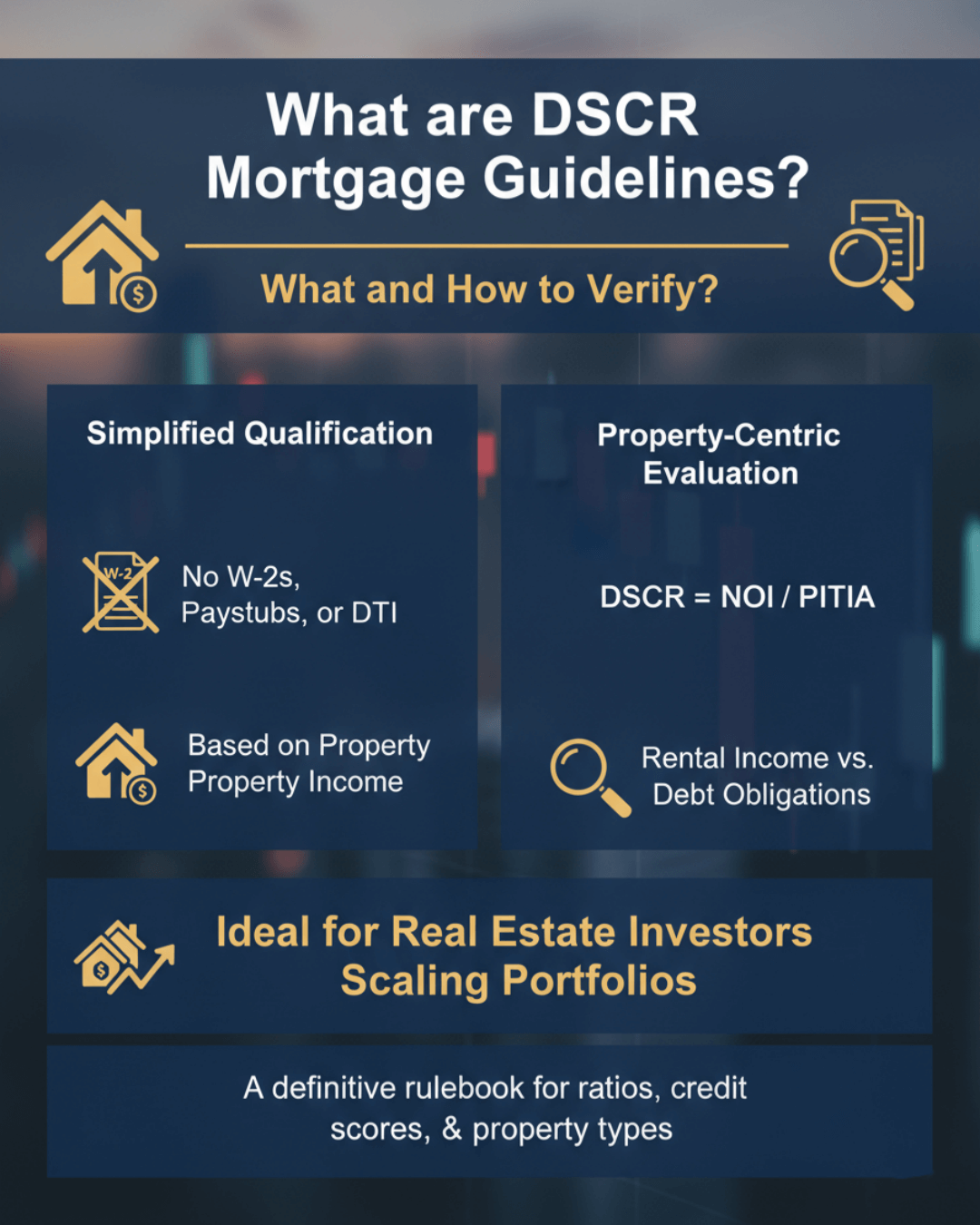

What are DSCR Mortgage Guidelines?

When we talk about DSCR mortgage guidelines, we are looking at a specific subset of Non-QM underwriting rules. Generally, a Debt Service Coverage Ratio loan does not rely on a borrower's personal income for qualification. In most programs, there are no W‑2s, no paystubs, and no DTI ratios to calculate.

Instead, these guidelines dictate how a lender evaluates the property itself. The primary focus is whether the property's rental income can comfortably cover the monthly debt obligations. Lenders calculate this by dividing the Net Operating Income (NOI) by the annual Debt Service (PITIA).

The primary target audience for these products is real estate investors looking to scale their portfolios without the headache of traditional personal income verification. Think of these guidelines as the definitive rulebook detailing exactly what ratios, credit scores, and property types are acceptable to get your client's deal funded.

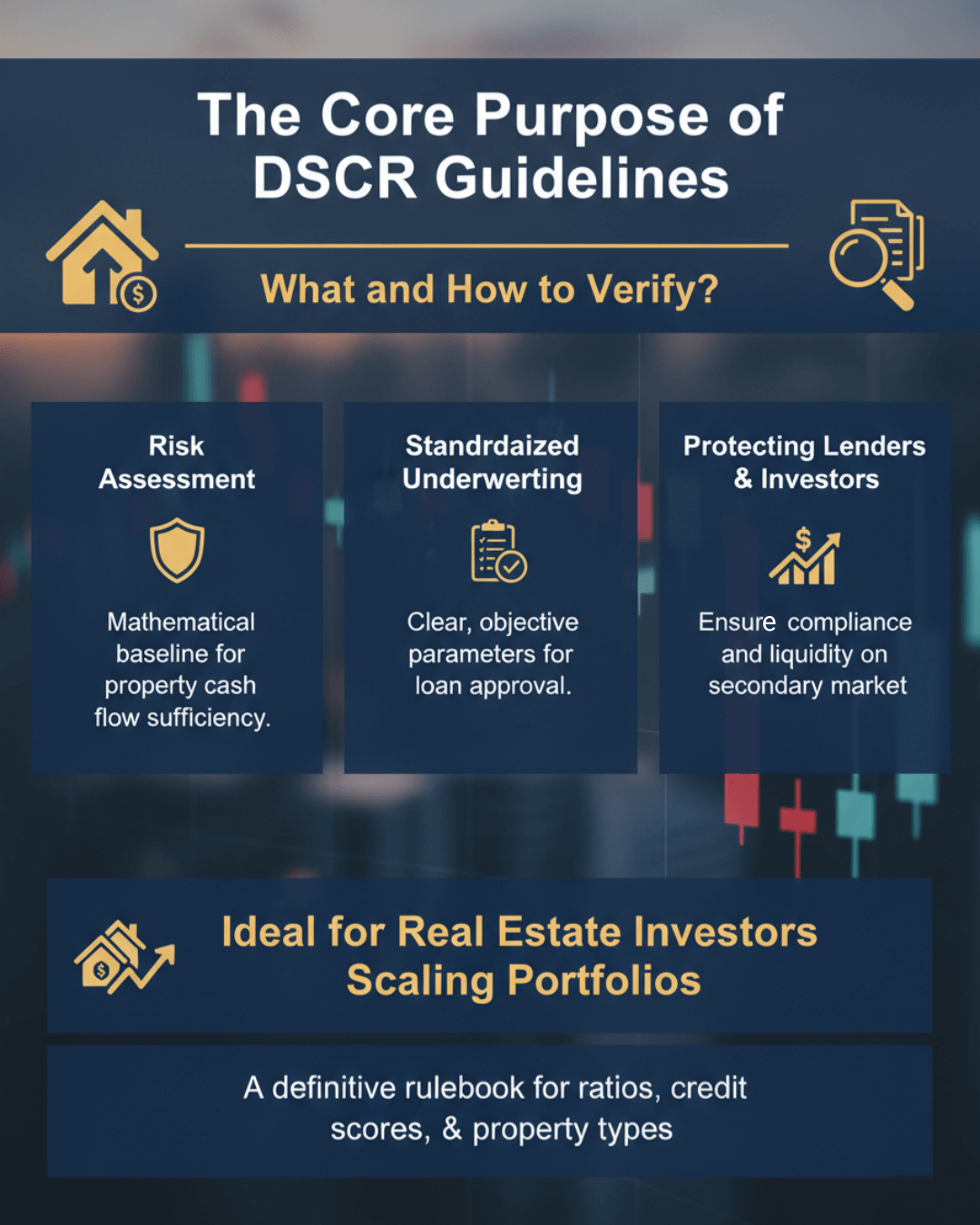

The Core Purpose of DSCR Guidelines

You might wonder why these matrices are so dense. As someone who has structured hundreds of these loans, I can tell you that DSCR guidelines serve a few crucial functions:

- Risk Assessment: They provide a mathematical baseline to help lenders determine if a property's cash flow is truly sufficient to cover the monthly mortgage payment.

- Standardized Underwriting: They give underwriters clear, objective parameters to approve or deny a file, which takes the guesswork out of Non-QM loans.

- Protecting Lenders & Investors: Because these loans are heavily securitized, strict guidelines ensure the originated mortgages maintain compliance and liquidity on the secondary market.

Without these rulebooks, accurately pricing risk in the Non-QM space would be impossible.

DSCR Loan Requirements in 2026

If you are structuring deals right now, you need to know the baseline numbers. Based on current 2026 market data, here is what most DSCR lenders are looking for:

- DSCR Ratio: The sweet spot is typically a 1.20 to 1.25 ratio or higher for stronger pricing. A 1.0 ratio (where rent exactly equals the mortgage payment) is a common floor, and while some lenders allow a 0.75 ratio or even "No Ratio" products, those usually come with significant pricing hits.

- Down Payment/LTV: For purchases, a maximum 80% LTV (20% down) is typical in 2026, with some programs requiring 25% down for better pricing. For cash‑out refinances, lenders commonly cap leverage at 70% to 75% LTV.

- Credit Score (FICO): Minimum qualifying scores typically fall in the 620 to 640 range, depending on the lender. To get your client a more competitive rate, you generally want at least a 680+, with the best terms often reserved for 740+ borrowers

- Reserves: Plan on showing 3 to 6 months of PITIA reserves. If the DSCR falls below 1.0 or it's a short-term rental, underwriters will often demand 6 to 12 months of liquid reserves.

However, this is just the industry average. Specific DSCR loan requirements across major lenders, like AAA Lending or AD Mortgage, vary wildly and update constantly. This is exactly why checking guidelines quickly is vital to your success.

Tip: How to Quickly Check DSCR Mortgage Eligibility?

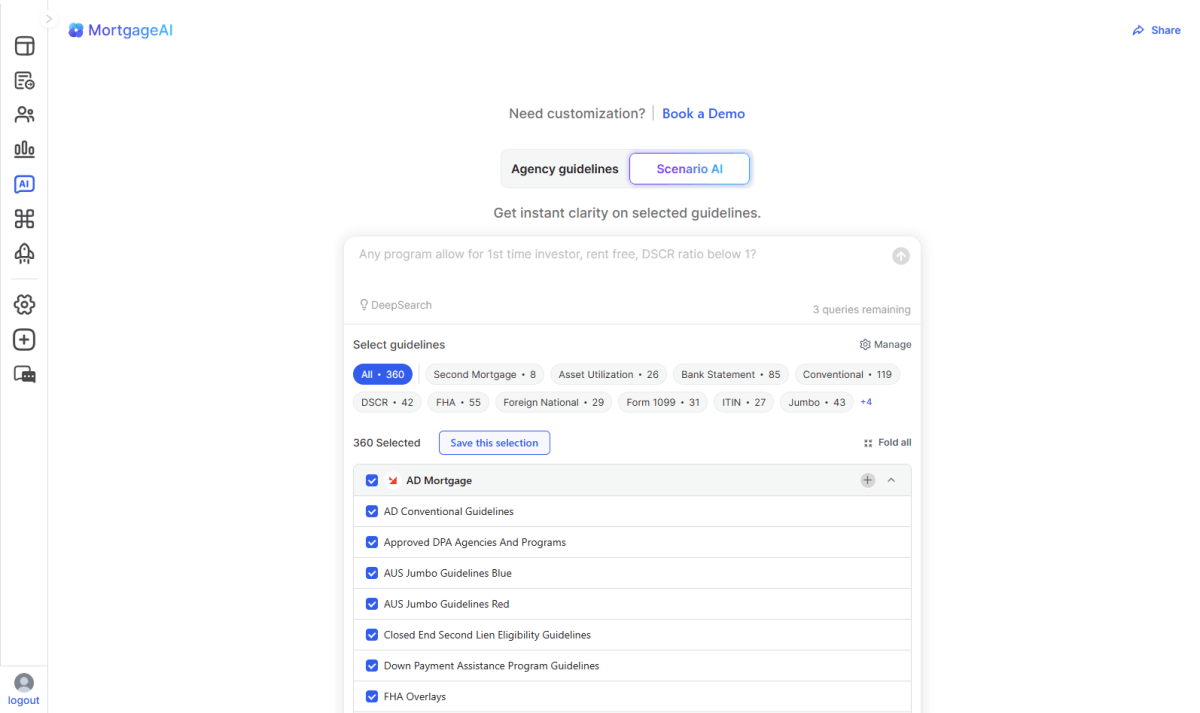

Let's be honest: memorizing the nuances of 20 different lending matrices is impossible. Whenever I have a tricky Non-QM scenario, my go-to move is using Zeitro's Scenario AI. It's an AI-powered mortgage guideline assistant specifically built for our industry, and it absolutely shines when handling Non-QM products.

The platform covers 15 major wholesale lenders (including AmWest, Forward Lending, and HomeXpress) and houses over 300 up-to-date guidelines, including 42 specific DSCR matrices that are continuously refreshed. Instead of CTRL+Fing through massive PDFs, here is how Scenario AI transforms your workflow:

- Instant & Accurate Answers: Ask anything from a vague "what is" question to a highly specific prequalify scenario, and it extracts the exact answer in seconds.

- Verifiable Citations: It doesn't just guess. It provides direct citations back to the source text, ensuring 100% accuracy and reducing underwriting errors.

- Custom DeepSearch: Select a single lender or check multiple lenders simultaneously to compare eligibility on the fly.

- "Explain" Feature: If a specific reserve requirement is confusing, use the explain tool to run a secondary query for instant clarification based on your selected parameters.

- Multi-language & LOS Integration: It supports both English and Chinese input, and integrates seamlessly with your LOS for a frictionless process.

- High ROI & Cost-Effective: Starting at just $8 a month and offering 3 free queries daily, it saves LOs and processors hours of reading time, significantly speeding up closings.

FAQs About DSCR Mortgage Guidelines

Q1. Do all DSCR loans require 20% down?

Not all DSCR loans require exactly 20% down, but 20% to 25% is the typical range for most lenders in 2026. Some niche programs may allow as little as 15% down for borrowers with top‑tier credit (often 740+ FICO) and strong DSCR, but these usually come with noticeably higher rates and tighter terms.

Q2. What is the DSCR 1% rule?

In some investor conversations, people use a shorthand where a "1.0 DSCR" means the property's gross monthly rental income covers 100% of the monthly housing expense. For example, if the rent is 2,000 dollars, the PITIA should not exceed 2,000 dollars.

Q3. What is the downside to a DSCR loan?

While convenient, DSCR loans have a few trade-offs. First, the interest rates are typically 1% to 2% higher than conventional loans. Second, they require larger down payments. Finally, most DSCR loans carry prepayment penalties if you refinance or sell within the first few years, and programs that waive or shorten prepay periods usually charge higher rates or fees.

Q4. Do I have to have an LLC for a DSCR loan?

It isn't strictly required by all lenders, but I highly recommend it. Lenders actually prefer to close these loans in the name of a business entity, like an LLC or Corporation, because it offers better personal asset protection for the real estate investor.

Q5. Do DSCR loans have closing costs?

Yes, they absolutely do. Just like conventional mortgages, you will see standard third-party fees for appraisals and title work. Additionally, DSCR loans often include lender origination points. Expect total closing costs to run anywhere from 2% to 5% of the total loan amount.

Final Word

DSCR loans remain one of the most powerful tools in 2026 for real estate investors looking to scale their portfolios quickly. However, successfully funding these deals means you have to master the intricate and constantly changing guidelines of multiple lenders. Don't let manual document searches slow down your pipeline.

I highly encourage my fellow loan officers and brokers to leverage technology to close loans faster. Stop wasting time flipping through PDFs and register for Zeitro's Scenario AI. With 3 free queries every single day, you can experience firsthand what it's like to get precise, citation-backed answers in a matter of seconds. Embrace AI, increase your client satisfaction, and watch your ROI grow.

People Also Read

- How to Get a DSCR Loan? Step-by-Step for Real Estate Investors

- Mortgage Guidelines: What Are They? How to Verify?

- Foreign National Mortgage Guidelines: Verify Eligibility Fast

- Jumbo Mortgage Guidelines: Check Eligibility Quickly and Accurately

- 8 Best Non-QM Mortgage Lenders: Which to Choose?