Written by

Eric

Share this article

.svg)

Subscribe to updates

Last checked and updated in July, 2026

Sitting in a bank branch, watching a traditional loan officer flip through a 100-page stack of personal tax returns, is a frustrating experience. For self-employed individuals or business owners, legal tax write-offs can make personal debt-to-income (DTI) ratios look risky to conservative banks, even with several highly profitable properties already in a portfolio.

For property owners facing these exact hurdles, learning how to get a dscr loan can change an entire investment strategy. These specialized dscr loans bypass the headache of personal income verification entirely. This dscr loan guide acts as a practical pathway to commercial-style financing. It functions as a complete resource to help you get your free guide to dscr loans in one detailed, easy-to-follow layout. Let’s look at how this financing tool empowers a dscr loan for real estate investors who want to scale their portfolios without traditional red tape.

What is a DSCR Loan Program and How Does It Work?

Before gathering documents, it helps to understand the fundamental dscr loan meaning. What exactly is a dscr loan? In plain terms, a dscr loan is a commercial-purpose mortgage designed specifically for rental properties. Unlike a conventional mortgage that relies on personal pay stubs, this loan qualifies you based entirely on the cash flow generated by the target property.

If you are wondering, how does a dscr loan work in practice? The lender analyzes whether the property’s rental income is high enough to cover the proposed monthly mortgage payment, which includes property taxes, home insurance, and any HOA fees. If the rental income meets or exceeds this threshold, you qualify. This answers the common question: how does dscr loan work? It shifts the underwriting focus away from your personal tax returns and onto the physical asset.

Many investors ask about the main benefit of a dscr loan program. The biggest advantage of utilizing a what is a dscr loan program strategy is that it allows you to build a portfolio of rental properties without hitting the strict 10-mortgage limit set by traditional agency lenders. While some might ask, can anyone get a dscr loan? The reality is that while you do not need a W-2 job, you still need to meet credit and down payment benchmarks. So, how hard is it to get a dscr loan? As long as you have the required down payment, solid credit, and a property that cash-flows, the underwriting process is actually much faster and less invasive than a traditional home loan.

How is the Debt Service Coverage Ratio Calculated?

Before you talk to a lender, you need to know your numbers. The formula is straightforward, but accuracy is key.

The Formula: DSCR=Net Operating Income (or Monthly Rent)/Total Debt Service (PITIA)

- Numerator: The lower of the actual rent (if leased) or the appraiser's market rent estimate.

- Denominator: Principal, Interest, Taxes, Insurance, and HOA dues (PITIA).

- Real-World Example:Let's say you are buying a rental home in Texas.

- Monthly Rental Income: $2,500

- Total Monthly Debt (PITIA): $2,000

- DSCR= $2500/$2000=1.25

A ratio of 1.25 means the property generates 25% more cash than it costs to own. This is a green light for most lenders.

Who Qualifies for a DSCR Loan? Typical Lender requirements in 2026

While you don't need income verification, DSCR loans aren't a "free pass." Lenders in 2026 have specific risk appetites. Here is what you need of DSCR loans to aim for to get approved.

Typical DSCR Threshold Lenders Expect

Typical DSCR thresholds start at 1.0 (break-even) for many lenders, but 1.25+ remains the gold standard for optimal rates and terms.

- 1.20 – 1.25+: This is the gold standard. If your ratio is here, you will unlock the best interest rates and lowest down payment options.

- 1.00: This is the "break-even" point. The rent exactly covers the debt. Many lenders accept this, though the rate might be slightly higher.

- Below 1.00: Yes, some lenders offer "no-ratio" or low-DSCR loans where the property loses money monthly (negative cash flow). However, expect to pay a premium in interest rates and put down a larger down payment (often 30-35%) to offset the lender's risk.

Common Credit Score, LTV, and Down-Payment Ranges

Unlike conventional Fannie Mae loans, DSCR requirements vary wildly between lenders. However, based on current 2026 market trends, here are the typical ranges:

- Credit Score: Most lenders require a minimum FICO of 620. However, to get a competitive rate, you really want to be above 700-720.

- Down Payment: Expect to put down 20% to 25%. It is rare to see 15% down payments unless you have stellar credit and a very high DSCR ratio.

- Cash Reserves: Lenders want to see you can weather a storm. You typically need 3 to 6 months of mortgage payments sitting in your bank account (liquid cash) after closing costs.

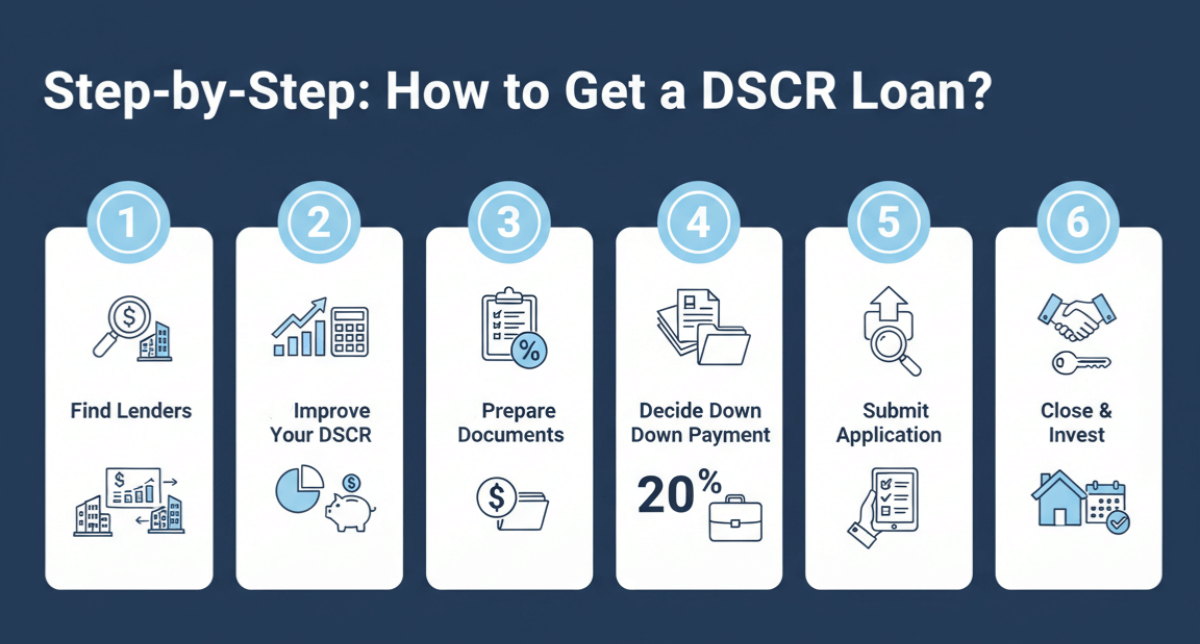

Step-by-Step: How to Get a DSCR Loan?

Ready to move forward? I've broken this down into actionable steps based on my own experience closing these deals.

Step 1. Find experienced DSCR Lenders and Compare Terms

Avoid assuming big retail banks like Chase or Wells Fargo never originate these loans. Some offer DSCR products for investors, though specialized Non-QM lenders often provide more flexibility. Always verify with the specific bank.

Because rates and fees are not standardized like conventional loans, shopping around is critical. One lender might quote you 7.5% while another quotes 8.5% for the same deal.

- What to ask: "Do you underwrite in-house?" and "What is your current turn time for appraisals?"

To save hours of phone calls, I recommend using Bluerate. They connect you with verified loan officers who specialize in DSCR loans. You can check rates online and get a clear picture of what's available in your area without the sales pressure.

Check rates here: Search for NonQM Loan Officers Nearby

Step 2. Calculate and Improve Your DSCR

Don't wait for the appraisal to see if you qualify. Run the math yourself first. If your ratio is tight (e.g., 0.95), try to improve it before applying.

- Expense Reduction: Shop around for cheaper landlord insurance. Lowering your annual premium by $600 reduces your monthly debt by $50, which bumps up your DSCR.

- Tax Protest: If it's a refinance, ensure you aren't overpaying on property taxes.

- Rent Adjustments: If the unit is vacant, check if your projected rent aligns with the "1007 Rent Schedule" (the form appraisers use). If the market supports higher rent, provide comparables to your lender to justify a higher income figure.

Step 3. Prepare Required Documents

The beauty of DSCR loans is the "lite" documentation. You can say goodbye to digging up tax returns from two years ago. Here is the checklist I usually prepare:

- Application (1003 Form): Standard loan application.

- Credit Authorization: To pull your FICO scores.

- Bank Statements: Usually the most recent 2 months. This proves you have the down payment and the required 3-6 months of reserves.

- Property Docs: If it's a purchase, the purchase contract. If it's a refinance, your current mortgage statement and insurance.

- Lease Agreements: If the property is currently rented.

- Entity Docs: If you are closing in an LLC (which I highly recommend), you'll need your Articles of Organization and Operating Agreement.

Step 4. Decide Down Payment & Structure

At this stage, you need to make strategic decisions.

- First, Vesting. Most investors prefer to close DSCR loans in an LLC name for liability protection. Unlike conventional loans, DSCR lenders are very LLC-friendly.

- Second, Down Payment size. Ask your loan officer to run scenarios for 20% down versus 25% down. In my experience, bumping your down payment to 25% often unlocks a "pricing tier" that significantly lowers your interest rate. If you have the extra cash, that interest savings adds up massively over 30 years.

Step 5. Submit Application & What Underwriters Check

Once you submit, the process moves to underwriting. The Underwriter is the gatekeeper. Their main focus will be the Appraisal.

- Valuation: Is the purchase price supported by the market?

- Rent Schedule (Form 1007): This is crucial. The appraiser estimates the market rent. If this number comes in lower than you expected, it kills your DSCR ratio.

- Habitability: The property must be "rent-ready." DSCR loans generally do not work for gut-renovation projects (fix-and-flips) because the property needs to be habitable to theoretically generate income immediately.

Step 6. Approval, Closing, and Post-Closing Checklist

DSCR loans can close fast, often in 2-3 weeks if you are organized. But before you sign the final closing disclosure, check one specific clause: the Prepayment Penalty (PPP).

Most DSCR loans come with a PPP, often structured as "3-2-1" (3% penalty if sold in year 1, 2% in year 2, etc.).

If you plan to hold the property long-term, a PPP is fine and gets you a lower rate. If you plan to sell or refinance in 12 months, negotiate to buy out the penalty. Do not let this surprise you at the closing table.

The Truth About the DSCR Loan Down Payment Requirements

One of the most common questions investors ask is, what is the down payment on a dscr loan? The general guideline is that a dscr loan typical down payment 20% 25% is standard across the industry. Most programs operate under a dscr loan typical down payment 20 25 percent tier because it offsets the lack of personal income verification.

When structuring your investment, you should expect a dscr loan down payment typically 20 25 percent for a purchase. If you want the absolute best interest rate, putting down a dscr loan typical down payment 20% 25% 30% often bumps your loan file into a superior pricing bracket. Let’s break down the specific tiers you will encounter in the market:

- The Standard 20% to 25% Down Option: For a typical dscr loan down payment, putting 20% down (80% LTV) represents the entry point for most prime programs. A dscr loan down payment 20% 25% typical structure keeps your monthly payment lower, making it easier to hit a target ratio of 1.20 or higher.

- The 15% Down Program: Can you get a 15% down dscr loan? Yes, but a 15 down dscr loan is a highly specialized product. Lenders who offer a dscr loan low down payment option at 15% down usually require a credit score of 720+ and a strong historical DSCR of 1.25 or more.

- The 10% Down Program: Finding a 10% down dscr loan is extremely rare in residential lending. A 10 down dscr loan typically requires cross-collateralization, where the lender takes a security interest in another property you own that has significant equity.

- The Zero Down Myth: If you are searching for how to get a dscr loan with no down payment, you need to be careful. There is practically no institutional dscr loan with no down payment option. If a lender offers zero down, they are likely requiring you to pledge other real estate assets as collateral, meaning you are still bringing value to the table, just not in cash.

Ultimately, your minimum down payment for dscr loan programs depends heavily on your credit score and the property type. Single-family homes enjoy the lowest dscr down payment requirements, while multi-family properties (2-4 units) often see their dscr loan minimum down payment rise to 25%. Understanding these dscr loans down payment mechanics helps you plan your cash reserves long before you submit an application.

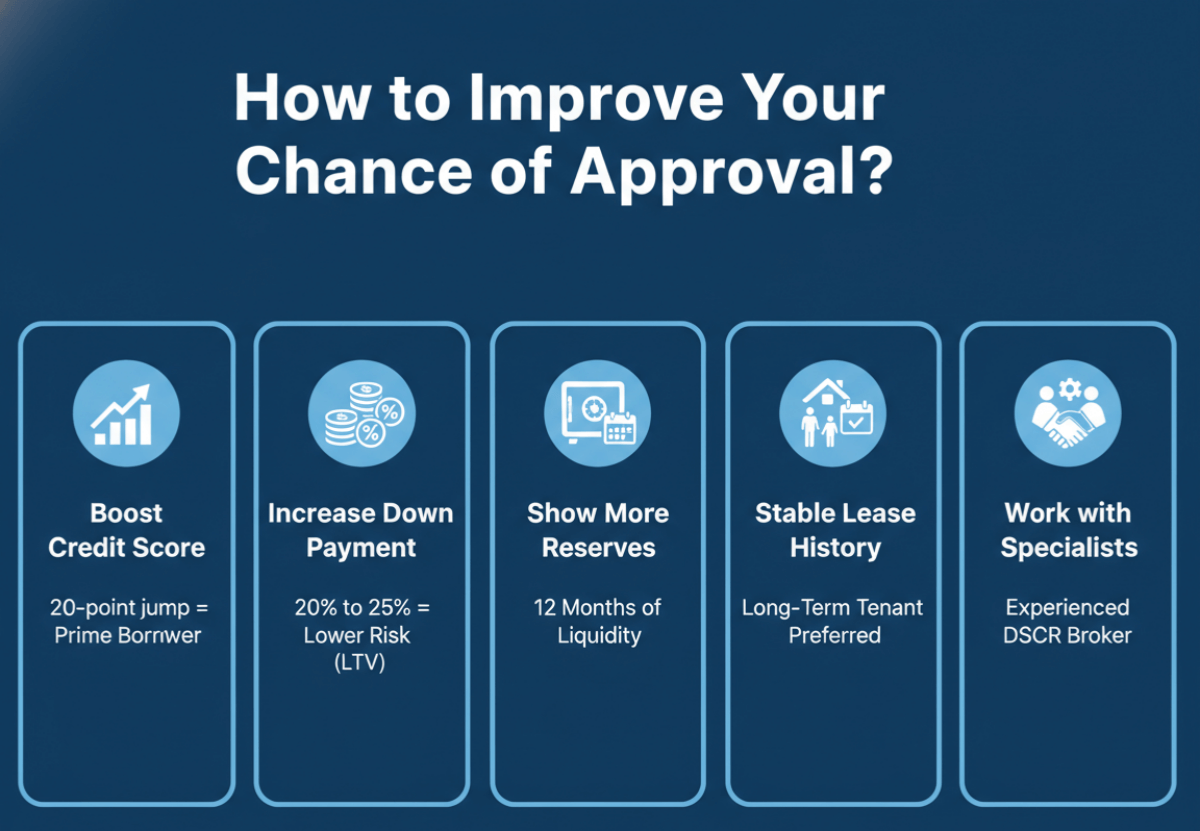

How to Improve Your Chance of Approval?

If you are worried about rejection, focusing on these factors will significantly strengthen your file:

- Boost Credit Score: Even a 20-point jump can move you from a "Standard" to "Prime" borrower tier.

- Increase Down Payment: Moving from 20% to 25% reduces the lender's risk (LTV), making them more lenient on other issues.

- Show More Reserves: Lenders love liquidity. Showing 12 months of reserves instead of 3 makes you look incredibly safe.

- Lease History: If refinancing, showing a stable, long-term tenant is better than a vacant unit.

- Work with Specialists: I cannot stress this enough. A generalist broker who does FHA loans all day might mess up a DSCR file. Use a platform like Bluerate to find professionals who understand investment nuances.

Geographic Nuances: Navigating State-Specific Rules

Real estate is inherently local, and geographic factors play a major role in how your debt ratio is calculated. Let's look at a few key regional differences across the United States:

- DSCR Loan Florida: Florida is incredibly popular for property investment, but soaring homeowners insurance premiums have dramatically increased the PITIA payment (the denominator in your ratio). When writing offers in Florida, always pull early insurance quotes to ensure high premiums do not compress your cash flow.

- DSCR Loan California (Your Helpful Guide): In California's high-priced markets, rental yields often do not cover the high cost of acquisition at 80% LTV. Investors looking for a dscr loan california often have to put down 30% to 35% or utilize "no-ratio" programs where the lender waives the rental calculation entirely in exchange for stellar credit.

- DSCR Loan NC (North Carolina), Ohio, and Missouri: In contrast to California, states like North Carolina, Ohio, and Missouri offer excellent rent-to-price ratios. Securing a dscr loan nc, dscr loan ohio, or dscr loan missouri is generally much simpler because purchase prices are lower, making it easy to hit a healthy 1.25 DSCR with a standard 20% down payment.

FAQs About Getting a DSCR Loan

Q1. Can I get a DSCR loan with no tax returns?

Yes, absolutely. That is the defining feature of this loan. Lenders rely on the appraisal and credit report. I have closed multiple DSCR loans without ever showing a single page of my personal or business tax returns.

Q2. How much down payment do I need for a DSCR loan?

Typically, you need 20% to 25%. While some aggressive lenders might advertise 15% down, those programs are rare in 2026 and usually come with very high interest rates. If your credit is below 660, you might be asked for 30%.

Q3. Are DSCR loans good for short-term rentals?

Yes, but be careful. Short-term rentals (Airbnb/VRBO) earn more but are riskier. Make sure your lender allows AirDNA or short-term rental projections for the income calculation. Some conservative lenders will only use long-term rental comps, which might kill your deal if the long-term rent is low.

Q4. What is a Prepayment Penalty (PPP) period on a DSCR loan?

Because DSCR loans are legally classified as business-purpose transactions, lenders almost always include a prepayment penalty. You will frequently see this referred to as a ppp period dcsr loan or ppp dcsr loan (often using common typos like dcsr loan, dcrs loan, or even dscr lian). This penalty protects the lender's yield. A typical PPP structure is 3-2-1, meaning you owe a 3% penalty if you refinance or sell in year one, 2% in year two, and 1% in year three. If your investment strategy involves flipping or refinancing quickly, you should ask your loan officer to buy down the prepayment penalty to zero in exchange for a slightly higher interest rate.

Conclusion

Getting a DSCR loan is one of the most powerful moves you can make as a real estate investor. It removes the friction of personal income verification and allows you to scale your portfolio based on the quality of your assets, not your W-2.

While the interest rates are slightly higher than conventional mortgages, the speed, flexibility, and ability to close in an LLC make it worth it. If you are ready to see what you qualify for, don't guess. Head over to find DSCR loan lenders to compare rates and connect with loan officers who know exactly how to structure these deals for success.