Written by

Eric

Share this article

.svg)

Subscribe to updates

As a loan officer, I know firsthand the daily headaches of navigating Non-QM lending. You get a solid self-employed borrower, and suddenly you are drowning in a sea of bank statement mortgage guidelines that change drastically from one lender to the next. Spending hours searching through hundreds of pages of PDF matrices just to find the right income calculation is exhausting.

But what if you could just ask an AI? That's where Zeitro's Scenario AI comes into play. You can now verify different lenders' complex guidelines through a simple, natural chat interface, instantly taking your workflow efficiency to the next level.

What is a Bank Statement Loan?

A bank statement loan is a highly popular Non-QM (Non-Qualified Mortgage) product designed specifically for self-employed borrowers, freelancers, gig economy workers, and business owners.

Since these clients lack traditional W-2s or regular pay stubs, standard income verification simply doesn't work for them. Instead of relying on tax returns, which usually show heavy write-offs and lower taxable income, lenders evaluate 12 to 24 months of consistent bank deposits to calculate their true earning capacity.

I've seen countless successful entrepreneurs get denied by traditional banks, only to secure their dream homes through this alternative documentation route. It's an absolute lifesaver for business owners who have strong cash flow but don't fit into the conventional lending box.

What Are Bank Statement Mortgage Guidelines?

Because these are Non-QM products, they are not backed by Fannie Mae or Freddie Mac. As a result, there is a massive lack of standardization across the industry.

Bank statement mortgage guidelines are the specific, internal underwriting rules created by individual lenders. When I review these matrices, I have to look closely at several unique dimensions. This includes maximum Loan-to-Value (LTV) limits, minimum FICO score requirements. Lenders have strict NSF/overdraft limits (e.g., no more than 2-5 per period), as they indicate unstable cash flow.

Furthermore, lenders apply an "expense factor" to business accounts to estimate operating costs. Lenders typically apply a 50% expense factor to business deposits, but may reduce it to 10-40% with a CPA letter specifying expenses (e.g., 10% for solo service businesses, 50% for larger ones). Because every lender writes their own playbook, placing a file correctly relies entirely on knowing these fractured, ever-changing guidelines.

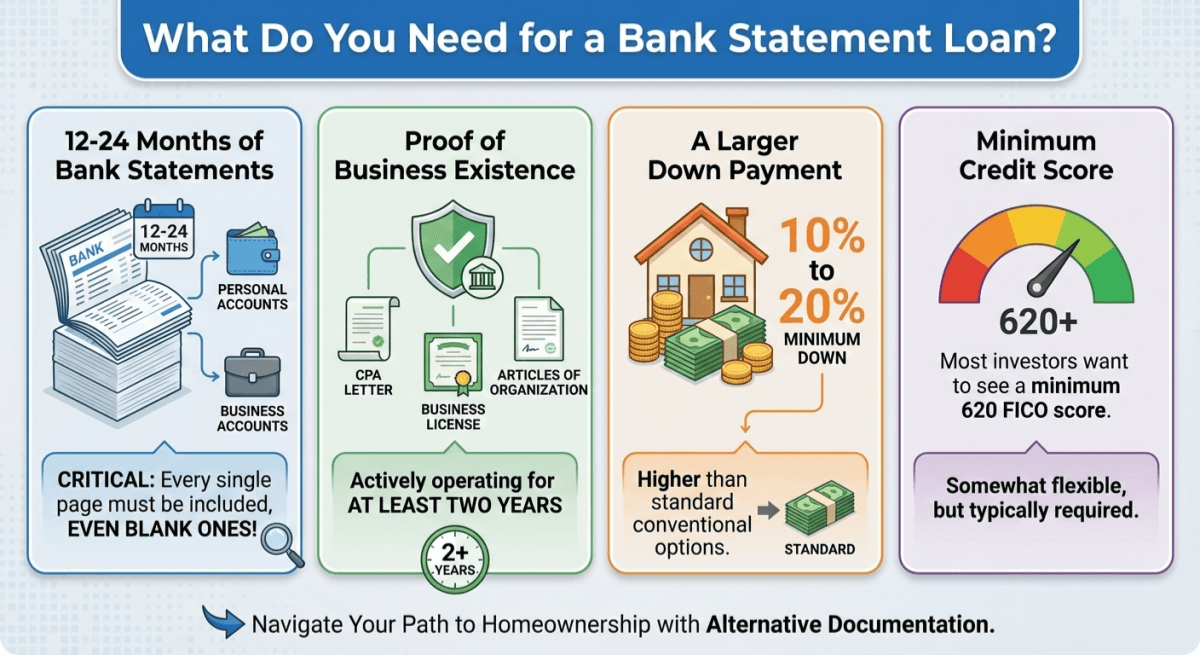

What Do You Need for a Bank Statement Loan?

Gathering the right documentation upfront saves everyone from a massive underwriting headache later. While traditional mortgages focus on tax transcripts, here is what you typically need to collect for a bank statement file:

- 12 to 24 months of bank statements: This can be personal or business accounts. Make sure every single page is included, even the blank ones!

- Proof of business existence: Lenders usually want a CPA letter, business license, or Articles of Organization proving the business has been actively operating for at least two years.

- A larger down payment: These loans typically require a minimum of 10% to 20% down, which is higher than standard conventional options.

- Minimum credit score: While somewhat flexible, most investors want to see a minimum 620 FICO score.

Disclaimer: Please note that exact requirements, especially expense factor calculations, vary significantly from lender to lender.

Why Do You Need to Check Bank Statement Mortgage Guidelines?

Because of the disclaimer I just mentioned above, flying blind is a terrible idea. Here is why I always verify the exact guidelines before submitting my borrower's file:

- Avoid Loan Rejections: Nothing ruins your pipeline faster than a denial that could have been avoided just by reading the fine print on overdraft limits.

- Find the Best LTV and Rates: Matching your client with the lender that views their specific income profile most favorably means securing better terms.

- Stay Updated: Lender matrices update constantly. The program that worked perfectly for your client last month might be suspended today.

- Let's be real: manually flipping through dozens of 200-page PDFs is soul-crushing and prone to human error. You need a smarter approach.

Best Way to Quickly Verify Bank Statement Mortgage Guidelines

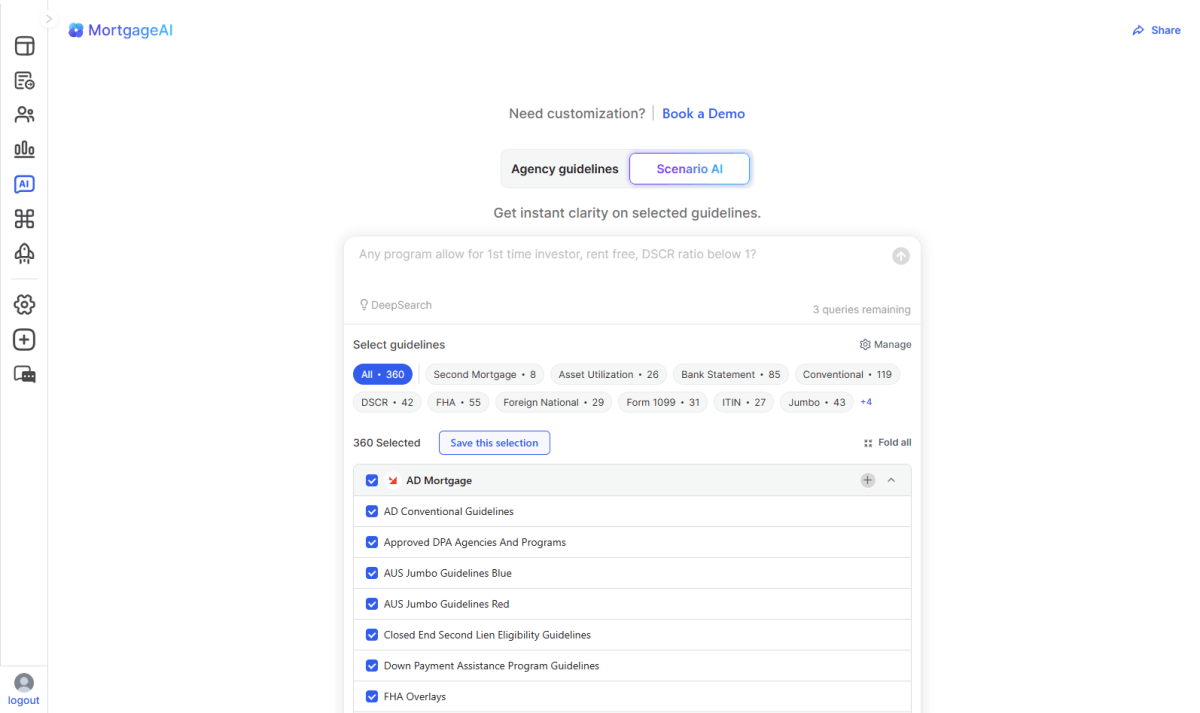

This is where my daily workflow completely transformed. I started using Zeitro's Scenario AI, an AI-Powered Mortgage Guideline Assistant that basically acts like a veteran underwriter sitting right next to you.

It covers over 300 guidelines, including more than 85 specific Bank Statement programs from top-tier lenders like AAA Lending, AD Mortgage, and CMG Financial, and it's constantly updating. Instead of downloading clunky matrices, you just type your borrower's scenario into the chat.

Here are the standout features that make it a game-changer for Loan Officers, Brokers, and Processors:

- High Accuracy with Citations: This is my absolute favorite part. The AI doesn't just guess. It provides specific citations and source links so you can verify the exact guideline yourself.

- Lightning-Fast Responses: It scans vast amounts of data instantly, giving you precise answers in seconds. You no longer have to put clients on hold while you hunt for a rule.

- Custom Data Scope (DeepSearch): You can check a single lender or cross-reference multiple lenders simultaneously to see who offers the most flexible terms.

- Handles All Scenarios: Whether you ask a broad "What is it?" or a highly detailed eligibility question, it understands the context perfectly.

- Explain Feature: If an answer seems confusing, the AI can further break down the details based on your selected data scope.

- Unbeatable Value: You get 3 free queries every single day, and the paid version starts at an incredibly low $8/month. The ROI on time saved is immediate.

FAQs About Bank Statement Mortgage Guidelines

Q1. Do you need 3 or 6 months bank statements for a mortgage?

For traditional conventional or FHA loans, you usually only need 2 months to verify your assets and down payment. However, for a Non-QM Bank Statement Loan, lenders use the deposits to calculate your actual income, so you will need to provide 12 to 24 months of consecutive statements.

Q2. Does FHA require 1 or 2 months bank statements?

Standard FHA guidelines generally require two months of complete bank statements. The underwriter reviews these to ensure your down payment funds are properly seasoned and not coming from an undisclosed loan.

Q3. Can I use both personal and business bank statements?

Yes, but it depends heavily on the lender. Most prefer one or the other. If you submit business statements, the lender will apply an "expense factor" (often ranging from 10% to 50%) to deduct your estimated operating costs from the gross deposits.

Q4. Are interest rates higher on bank statement loans?

Honestly, yes. Because lenders consider these loans slightly higher risk without standard tax documentation, interest rates are typically 1% to 3% higher than conventional mortgages.

Q5. Is a bank statement loan considered a Non-QM loan?

Yes. Because it uses alternative documentation instead of standard W-2s or tax returns to verify your income, it falls outside the Consumer Financial Protection Bureau's (CFPB) standard "Qualified Mortgage" definition.

Final Word

In the mortgage industry, time is literally money. Bank statement loans are an incredible tool to help self-employed borrowers achieve homeownership, but the complex, unstructured guidelines are a massive hurdle. You simply cannot afford to lose deals or delay closings because of a misread PDF matrix or an outdated lender requirement.

That's exactly why I highly recommend adopting technology to do the heavy lifting for you. Take advantage of Zeitro's Scenario AI. With 3 free queries a day and premium plans starting at just $8/month, you can stop searching and start closing. Try typing your next tricky Non-QM scenario into the chat and experience the efficiency firsthand!

People Also Read

- 8 Best Non-QM Mortgage Lenders: Which to Choose?

- Best Mortgage Loan Officer Training: Which to Pick?

- What are Asset Utilization Mortgage Guidelines? How to Verify in Seconds?

- Check ITIN Mortgage Guidelines: How to Verify Eligibility in Seconds?

- DSCR Mortgage Guidelines Explained: What and How to Verify?