Written by

Eric

Share this article

.svg)

Subscribe to updates

If you've been in the mortgage game as long as I have, you know that origination is where the battle is won or lost. We used to drown in paperwork, chasing stips and manually calculating DTIs until our eyes blurred. But heading into 2026, the landscape has shifted entirely. It's no longer just about digitizing paper. It's about leverage.

I've spent years testing different platforms, looking for that "holy grail" that actually saves time rather than just shifting the workload. We need tools that don't just store data but actively help us structure deals. Whether you are a solo broker or part of a massive retail lender, the software you choose today dictates your closing volume tomorrow. In this guide, I'm breaking down the top contenders that are actually worth your time and money this year.

People Also Read:

- [Tips] Where to Buy Mortgage Leads? Warm Leads for LOs

- Detailed Guide: How to Become a Loan Officer with No Experience?

- 6 Best Mortgage CRM for Brokers, Lenders, MLOs in 2026

What is Loan Origination Software?

At its core, Loan Origination Software (LOS) is the operating system for your mortgage business. It isn't simply a digital filing cabinet for 1003 forms. it is the central engine that manages the entire lifecycle of a loan—from the moment a borrower applies (or leads enter your funnel) to the final funding and closing table.

For us Loan Officers, a modern LOS serves as the command center. It handles application processing, underwriting, compliance checks, pricing, and document management. In the past, an LOS was a static database where you entered data and hoped for the best. Today, specifically in 2026, the definition has evolved. The best platforms now integrate Artificial Intelligence to automate income calculations, verify guidelines instantly, and even communicate with borrowers. It bridges the gap between the borrower's experience and the lender's back-office requirements. If your software isn't actively reducing the time you spend on manual data entry or guideline research, it's not a true modern LOS. It's just a database.

6 Top Loan Origination Software to Choose from

Having tested the waters with various systems, I've narrowed down the list to six platforms that stand out for different reasons. Here is my breakdown of the best tools available right now.

#1. Zeitro - Best for Efficiency Improvement

From my perspective, Zeitro has completely redefined what I expect from an origination platform. While many legacy systems feel clunky and outdated, Zeitro operates as a true AI SaaS tool specifically built to tackle the biggest pain point we all face: time. They position themselves as an AI Mortgage Platform, and honestly, the claim holds up. The biggest selling point here is the sheer speed of pre-qualification.

Using their "Scenario AI" and "GuidelineGPT," I've been able to navigate complex borrower scenarios—like Non-QM or tricky self-employed income—in seconds rather than digging through PDF guidelines for hours. The platform claims to deliver 2.5x faster pre-qualifications and save over 7 hours per loan file. In a commission-based industry, that time savings directly translates to closing more deals. It's not just a repository for data. It actively helps you structure the loan with built-in pricing engines and automated conditions. For independent LOs and brokers who don't have a massive support staff, Zeitro acts like a digital underwriter sitting right next to you.

Explore More Features About Zeitro

- GuidelineGPT: Instant answers for FHA, VA, USDA, Fannie, Freddie, and Non-QM eligibility without keyword guesswork.

- Scenario AI: Deep search capabilities to handle complex loan scenarios and edge cases instantly.

- AI Tools: Automated income calculations (85%+ accuracy), document review, and condition collection.

- Borrower Tools: Real-time rate quote tools and affordability calculators that you can embed on your personal site.

- Digital 1003: A seamless POS that allows borrowers to finish applications in under 5 minutes.

Pros and Cons of Zeitro

Pros:

-

- Significantly reduces manual guideline research (saves 7+ hours/loan).

- Generous "Explorer" Free tier makes it accessible for anyone to try.

- High accuracy in AI income calculation (90%+ application completion rates).

- One system covers all loan types (QM, Non-QM, DSCR, Hard Money).

Cons:

-

- As a newer AI-first platform, it may require a mindset shift for LOs used to legacy "data-entry" style software.

- The free plan has daily limits on AI queries (though the paid tiers are very affordable).

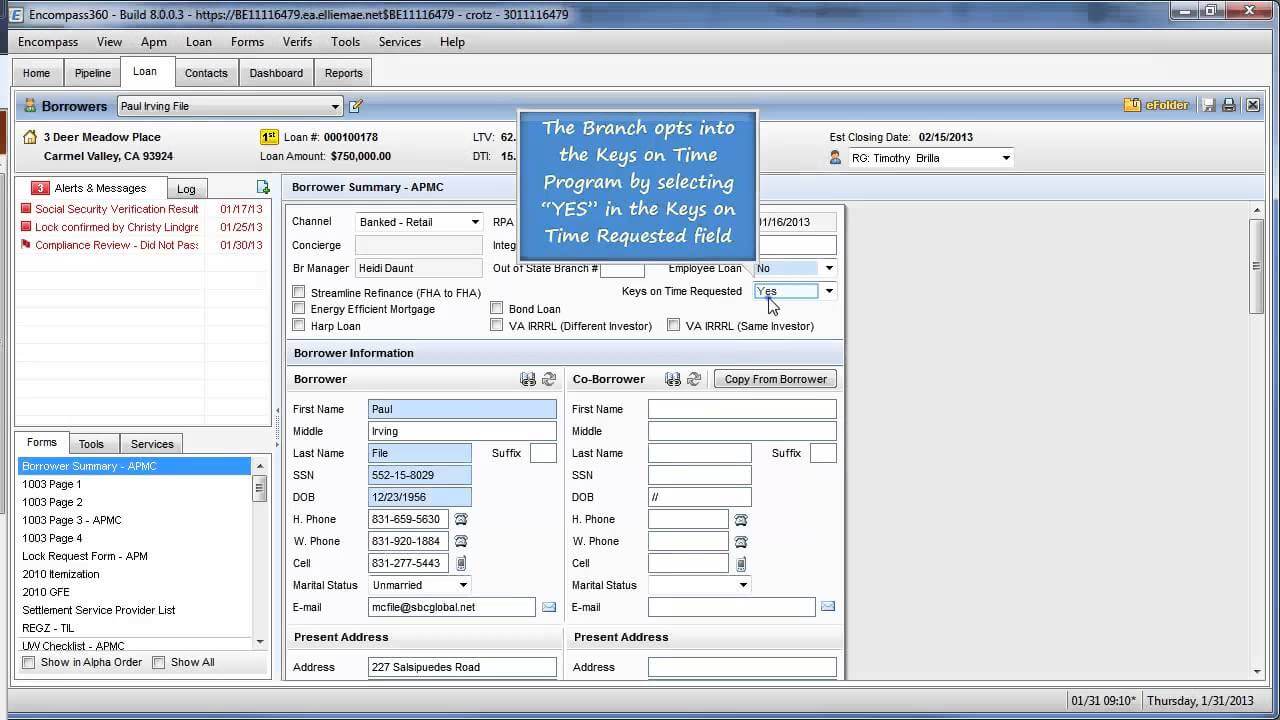

#2. Encompass - Best for Big Lenders and Institutions

If you have worked for a large bank or a major independent mortgage banker, you have almost certainly logged into Encompass by ICE Mortgage Technology. It is the heavyweight champion of the industry in terms of market share and sheer ecosystem size. Encompass is designed to be an end-to-end solution that handles absolutely everything, from lead generation to secondary market delivery.

For large institutions, Encompass is the "safe" choice because it connects with arguably the largest network of lenders, investors, and service providers in the country. Its strength lies in its configurability for compliance and workflow enforcement across massive teams. However, as an individual LO, I sometimes find it to be overkill. It is a beast of a system that requires significant training to master. It ensures that every box is checked for compliance, which protects the lender, but the interface can feel dense. That said, if your goal is to have a system that integrates with literally every other vendor in the mortgage space, Encompass is the standard.

Explore More Features About Encompass

- ICE PPE: A robust product and pricing engine integrated directly into the workflow.

- Encompass eClose: A single source workflow for digital closings, reducing time at the signing table.

- TPO Connect: specifically optimizes how third-party originators receive and manage loans.

- Compliance: Automatic updates to stay compliant with changing state and federal regulations.

Pros and Cons of Encompass

Pros:

-

- Unmatched ecosystem of integrations and partners.

- Extremely robust compliance and secondary marketing features.

- Scalable for massive organizations with hundreds of users.

Cons:

-

- Can be slow and "heavy" to operate compared to web-based competitors.

- Implementation takes a long time and usually requires dedicated admins.

- Pricing is generally opaque and geared towards enterprise contracts.

#3. LendingDox - Best for Underwriting

LendingDox captures my attention because it focuses intensely on the part of the job that gives most Loan Officers headaches: document management and underwriting organization. While it markets itself as an LOS and POS, its superpower is really in how it streamlines the paper trail. It integrates tightly with CRMs like Shape, creating a bridge between sales and processing.

For teams that struggle with "stips" and chasing borrowers for updated bank statements, LendingDox offers a very clean, centralized location to store and track documents. It emphasizes security with SOC 2 compliance, which is critical when you are handling sensitive borrower data. I find it to be particularly strong for the processing and underwriting side of the house. It automates requests and reminders, so you don't have to manually email a client three times to get that missing W2. It's less about the "sales" flash and more about the operational rigor of getting a file cleared to close.

Explore More Features About LendingDox

- Centralized Document Suite: Upload, organize, and manage all loan docs in one secure portal.

- Real-Time Tracking: Automated notifications for new documents or those requiring attention.

- Automated Workflows: Triggers for document requests and reminders to reduce manual follow-up.

- Seamless Integration: bidirectional sync with other LOS platforms and CRMs.

Pros and Cons of LendingDox

Pros:

-

- Very affordable pricing structure (around $30/month per user).

- Excellent for reducing operational friction in document collection.

- No long-term contracts or per-loan fees, which is rare.

Cons:

-

- Feels more like a specialized document engine than a full-suite AI origination platform like Zeitro.

- Heavily reliant on integrations to get the full "all-in-one" experience.

#4. MortgageBot - Best for Banks and Credit Unions

Finastra's MortgageBot is a staple in the banking world. I see this platform used most often by community banks and credit unions that need to bridge the gap between their retail banking operations and their mortgage wing. It is a cloud-native platform, which gives it a leg up over older on-premise solutions, and it supports retail, wholesale, and correspondent lending effectively.

The user experience here is designed to be "all-in-one," covering everything from the point of sale (POS) to closing and servicing. For an LO working in a bank branch, MortgageBot is great because it integrates well with core banking systems. It handles the full gamut of loan types, including construction and home equity, which are often bread-and-butter products for credit unions. It claims to reduce the application process time by 40% compared to manual methods, and while the interface isn't as flashy as some fintech startups, it is reliable and compliant, which bank compliance officers love.

Explore More Features About MortgageBot

- PowerSearch: An integrated pricing and eligibility engine.

- Direct POS Integration: Borrowers can apply online and data flows directly into the LOS.

- Compliance Reporter: Built-in tools to scrutinize files for state and federal defects.

- Multi-Channel Support: Handles retail, wholesale, and correspondent channels in one system.

Pros and Cons of MortgageBot

Pros:

-

- Strong integration with wider banking core systems.

- Cloud-native architecture makes it accessible from anywhere.

- Excellent support for niche bank products like HELOCs and construction loans.

Cons:

-

- The user interface (UI) can feel utilitarian and less modern than newer competitors.I

- nnovation cycles can be slower due to the size of the parent company (Finastra).

#5. TurnKey Lender - Best for Automation

TurnKey Lender is a bit of a different animal. It isn't just for mortgages. it's a global digital lending automation platform that covers everything from BNPL (Buy Now Pay Later) to commercial lending and mortgages. Because of this broad focus, their decision engine is incredibly powerful. They utilize proprietary AI to automate credit decisions, often claiming to process applications in under one second.

For a mortgage lender looking to diversify or one that focuses on high-volume, standardized loans, TurnKey offers incredible efficiency. The system is designed to be "end-to-end" with very little human intervention required for straightforward files. I find it fascinating for its "Decision Rules," which you can configure extensively. If you are running a lending operation that wants to scale into different types of finance—like bridging loans or SME lending—alongside mortgages, this is the top pick. However, for a pure residential mortgage broker, the breadth of features might feel overwhelming.

Explore More Features About TurnKey Lender

- AI Credit Decisioning: Machine learning for instant, accurate risk assessment.

- Configurable Application Flow: Drag-and-drop customization for the borrower journey.

- Debt Collection Module: Built-in tools for servicing and collections (rare in standard mortgage LOS).

- Global Compliance: tailored for multiple jurisdictions and lending types.

Pros and Cons of TurnKey Lender

Pros:

-

- Incredible automation speed for credit decisions.

- Versatile: handles consumer, commercial, and mortgage loans in one spot.

- Modern, white-label ready interface for borrowers.

Cons:

-

- Can be "overkill" for a standard independent mortgage broker.

- Implementation can be complex due to the sheer number of configuration options.

#6. LendingPad - Best for Real-time Collaboration

LendingPad has gained a massive following among brokers in recent years, and for good reason. It positions itself as the modern, cloud-native alternative to the older giants. The best way I describe LendingPad to other LOs is that it's like the "Google Docs" of loan software. It allows multiple users—processors, LOs, and underwriters—to work in the same file at the same time without locking each other out.

This real-time collaboration is a game-changer for remote teams. The interface is clean, web-based, and very fast. It doesn't require installing heavy software on your laptop, so you can originate a loan from a Chromebook if you want to. It has distinct editions for Brokers, Lenders, and Institutions. For the average broker shop, the "Broker Edition" connects seamlessly with wholesale lenders, allowing you to push files to major wholesalers with a single click. It cuts out a lot of the friction in the broker channel.

Explore More Features About LendingPad

- Multi-User Editing: Real-time updates and file sharing across departments.

- Direct Wholesale Integration: Seamless connection to manage pricing and lock loans with wholesalers.

- Cloud-Based: access from anywhere with an internet connection. no server maintenance.

- Built-in POS: Includes a complementary point-of-sale system for borrowers.

Pros and Cons of LendingPad

Pros:

-

- Extremely fast setup and implementation time.

- Modern, intuitive interface that requires very little training.

- Excellent for brokers due to deep integration with wholesale lenders.

Cons:

-

- Reporting capabilities are sometimes considered less granular than Encompass.

- Customization options are good but less infinite than enterprise-level systems.

How to Choose the Best Loan Origination Software?

Selecting an LOS is a commitment. switching platforms costs time and creates downtime. To get it right for 2026, you need to look beyond the brochureware and evaluate how the software fits your specific workflow.

Identify Your Need

First, define your business model. Are you a Broker who needs speed and wholesale connectivity? Then systems like LendingPad or Zeitro shine. Are you a large Bank needing deep compliance and core integration? MortgageBot or Encompass might be your lane. If you are handling complex, non-standard deals, you need the AI analysis capabilities of a platform like Zeitro. Don't buy an enterprise battleship if you just need a speed boat.

Consider Core Features

Look for features that actually move the needle. In 2026, AI is non-negotiable. You need automated document recognition (OCR) and intelligent guideline search. If the software still requires you to manually type in data from a W2, it is obsolete. Also, look for a built-in Pricing Engine and a smooth Point of Sale (POS). Having these integrated saves you from paying for three different subscriptions.

Evaluate Integration Capabilities

Your LOS cannot live in a vacuum. It needs to talk to your CRM (like Salesforce or Jungo), your credit report vendors, and your AMC (Appraisal Management Company). Check the "marketplace" or API documentation of the LOS. For example, Zeitro and LendingDox emphasize seamless export and integration capabilities (like FNM 3.2/3.4 exports) which ensure you aren't double-entering data into lender portals.

Compare Pricing

Pricing models vary wildly. Some legacy platforms charge high setup fees plus a "per loan file" fee that eats into your margin. Others, like Zeitro, offer a subscription model or even a freemium tier, which is unheard of in the enterprise space. LendingDox is also affordable at ~$30/user. Calculate your total cost of ownership based on your monthly volume. High per-file fees punish you for being successful. flat user fees are generally better for scaling.

FAQs About Best Loan Origination Software

Q1. What is loan origination software used for?

Loan Origination Software (LOS) is used to manage the steps of generating a mortgage or loan. It handles the application (1003), credit checks, eligibility verification, underwriting, document management, and preparation for closing. It is the central database where the loan file "lives."

Q2. What are the benefits of loan origination systems?

The main benefits are efficiency and compliance. A good LOS automates manual tasks (like calculating income), ensures you collect the right documents, prevents you from offering loans that don't meet guidelines (compliance), and speeds up the time from application to funding.

Q3. Which is the best loan origination software for small lenders?

For small lenders or independent brokers, Zeitro and LendingPad are excellent choices. They are cloud-based, require minimal IT setup, offer affordable pricing, and include powerful features like AI processing and wholesale integrations that level the playing field against big banks.

Q4. What is TMO software?

TMO generally stands for Total Mortgage Office or similar terminology referring to software that encompasses the entire front, middle, and back office of a mortgage operation. It implies a system that handles CRM (Customer Relationship Management), LOS (Origination), and sometimes Servicing in one ecosystem.

Conclusion

The mortgage industry is unforgiving to those who refuse to adapt. In 2026, the difference between a struggling LO and a top producer often comes down to the tech stack they utilize. While giants like Encompass serve the big banks well, and LendingPad offers great collaboration for brokers, the industry is clearly moving toward AI-driven efficiency.

That is why I personally lean towards Zeitro. It addresses the actual bottlenecks of our job—guideline research, income calculation, and speed-to-prequal—better than any legacy tool I've seen. It's not just about managing the loan. it's about closing it faster. With features like GuidelineGPT and Scenario AI, Zeitro acts like a force multiplier for your expertise. If you are ready to save 7+ hours per loan file and modernize your workflow, I highly recommend checking out Zeitro's free Explorer plan to see the difference for yourself.