Written by

Eric

Share this article

.svg)

Subscribe to updates

I remember the sheer panic I used to feel when a potential borrower walked in asking for a $2 million loan on a luxury property. Why? Because I knew I was about to spend the next three hours digging through PDF matrices, trying to figure out which investor would actually take the deal. In the mortgage industry, time is literally money.

That's why finding a way to verify guidelines instantly has been a game-changer for my workflow. Today, tools like Zeitro's Scenario AI have revolutionized how we work. Instead of manual cross-referencing, I can now verify different lender's Jumbo Mortgage Guidelines through a simple chat interface. It turns a chaotic research process into a 10-second conversation, drastically improving efficiency and pre-qualification accuracy.

What is a Jumbo Mortgage?

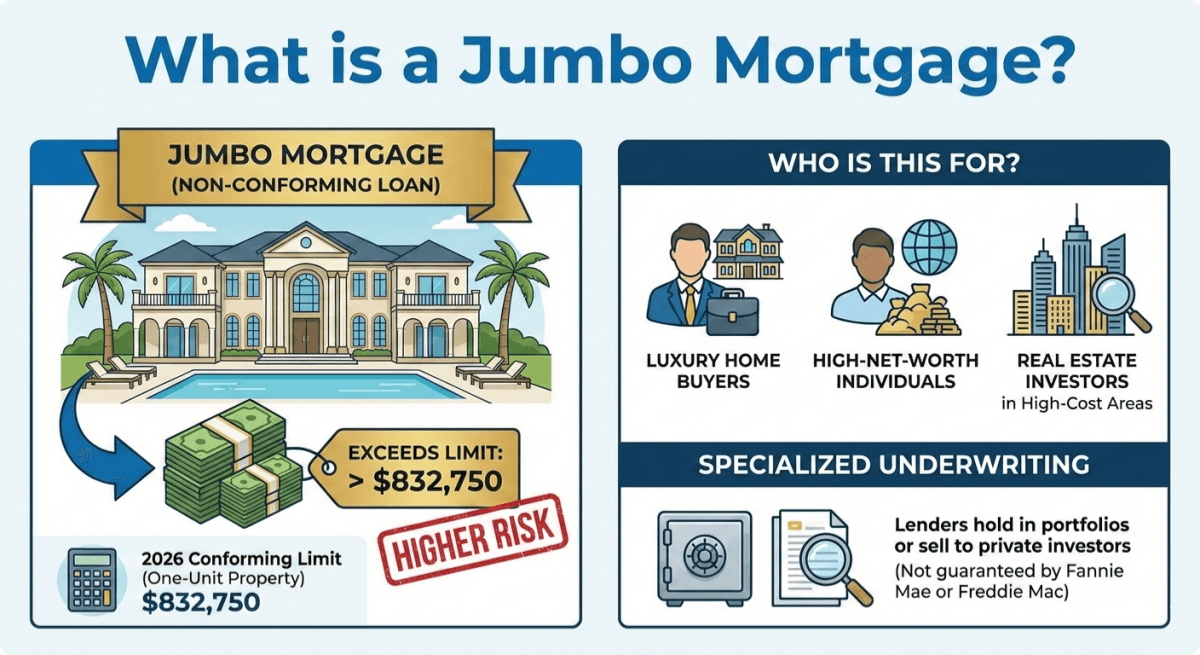

Put simply, a Jumbo Mortgage (or non‑conforming loan) is a home loan that exceeds the dollar limits established by the Federal Housing Finance Agency (FHFA). In 2026, the conforming loan limit for a one‑unit property in most U.S. counties is $832,750. Any loan amount above that threshold becomes a jumbo loan.

Who is this for? In 2026, Jumbo loans are primarily designed for luxury home buyers, high-net-worth individuals, and real estate investors targeting properties in high-cost areas like Los Angeles, New York, or San Francisco. Because these loans often carry higher risk for lenders as they are typically held in portfolios or sold to private investors rather than guaranteed by Fannie Mae or Freddie Mac, they require a specialized approach to underwriting that differs significantly from your standard conventional loan.

What are the Jumbo Mortgage Guidelines?

Unlike conventional loans, where the rulebook is fairly standardized by the GSEs, Jumbo Mortgage Guidelines are the Wild West. They are set entirely by individual lenders, banks, and private investors.

This means the rules vary—a lot. One lender might require 20% down, while another aggressive Non-QM investor might accept 10%. These guidelines dictate key parameters such as minimum credit score, maximum Debt‑to‑Income (DTI) ratio, required post‑closing reserves, and typical property‑type eligibility.

What you need to watch out for:

- Source: Guidelines are proprietary. A "Jumbo" at Wells Fargo looks completely different from a "Jumbo" at AD Mortgage.

- Overlays: Investors often add strict overlays.

- Appraisals: Many require two full appraisals rather than one.

As a Loan Officer, you can't just memorize "Jumbo rules" because they don't exist in a vacuum. You have to know the specific guidelines of the investor you are selling to.

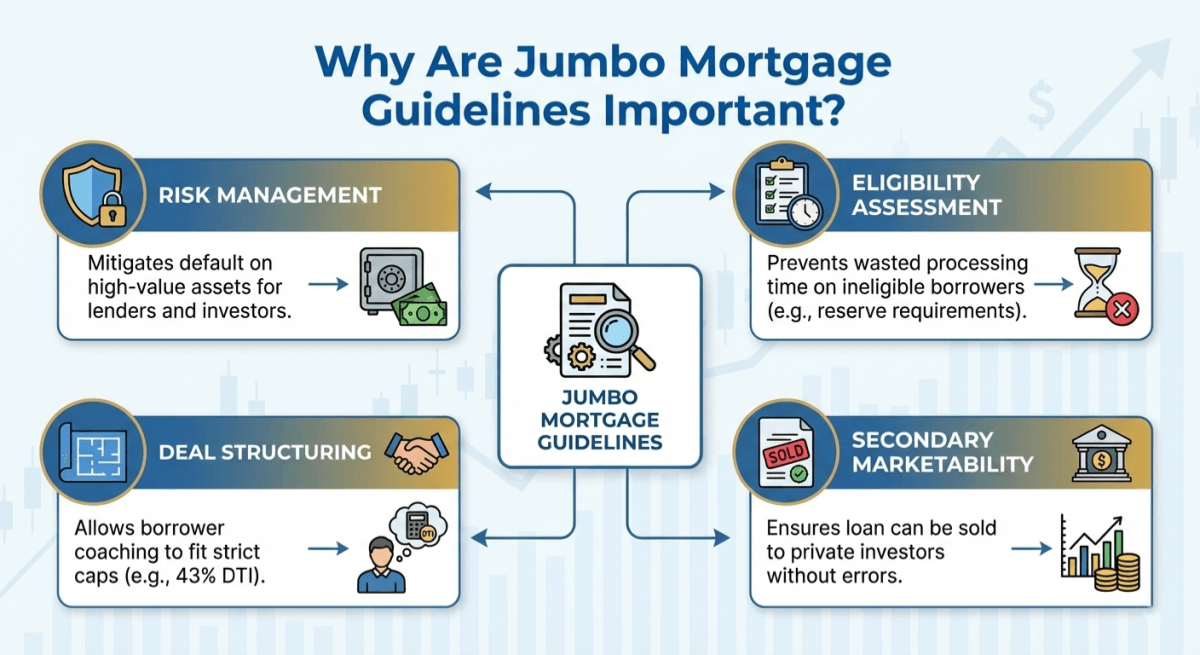

Why Are Jumbo Mortgage Guidelines Important?

It's not just about getting an approval. It's about structuring a deal that actually funds. Ignoring the nuances of these guidelines can lead to disastrous consequences, like a denial days before closing.

Here is why accurate guideline verification is non-negotiable:

- Risk Management: Lenders are holding these loans in their portfolios or selling them to strict private investors. Adhering to guidelines mitigates the risk of default on these high-value assets.

- Eligibility Assessment: You don't want to waste weeks processing a loan for a borrower who was never eligible in the first place due to a missed "reserve requirement."

- Deal Structuring: Understanding the guidelines allows you to coach your borrower, perhaps paying down a small debt to fit a strict 43% DTI cap.

- Secondary Marketability: For lenders, the loan must meet the guideline perfectly to be sold on the secondary market. A single foot-fault makes the loan unsellable.

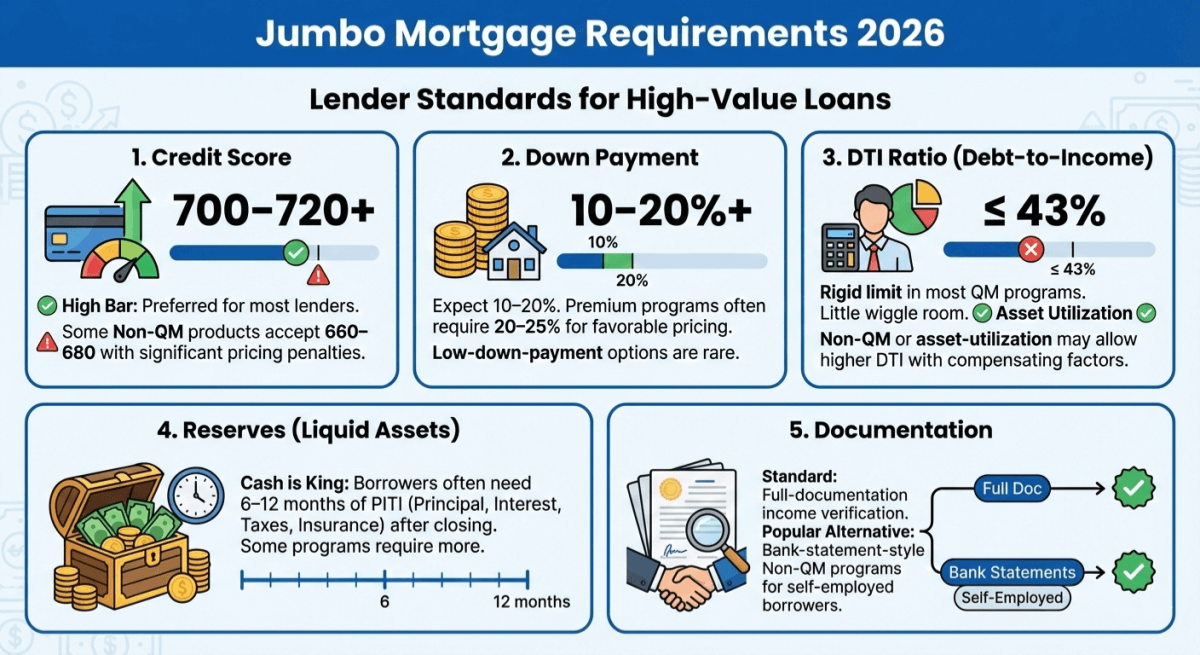

Jumbo Mortgage Requirements 2026

While every lender has their own "flavor," the market in 2026 has settled on some baseline expectations for Jumbo loans. These are stricter than what we saw a few years ago.

Here is what you typically need to prepare your client for:

- Credit Score: The bar is high. Most lenders prefer a FICO of 700–720 or higher. While some Non‑QM Jumbo products may accept scores around 660–680, the pricing penalties are usually significant.

- Down Payment: Expect to put down 10–20%, with many premium programs requiring closer to 20–25% for the most favorable pricing. The days of low-down-payment Jumbo loans are rare unless you have compensating factors.

- DTI Ratio: Rigid adherence to 43% or lower in most QM programs. However, some Non‑QM or asset‑utilization Jumbo products may allow higher DTI with compensating factors. Unlike FHA, there is very little wiggle room here unless you are using an Asset Utilization program.

- Reserves: Cash is king. Borrowers often need 6–12 months of PITI (Principal, Interest, Taxes, Insurance) in liquid assets after closing, though some programs may ask for more.

- Documentation: Full‑documentation income verification is standard, though bank‑statement‑style Non‑QM income programs are a popular alternative for self‑employed Jumbo borrowers.

How to Quickly Check Jumbo Mortgage Guidelines?

In the past, checking these requirements meant logging into five different lender portals and reading the fine print. It was exhausting and prone to human error.

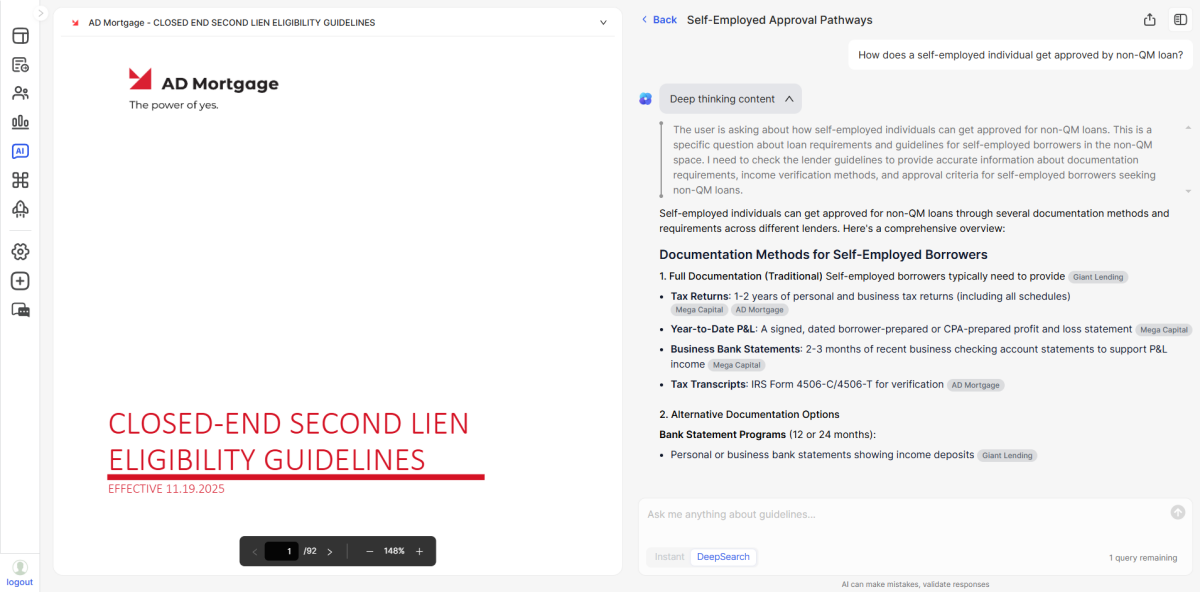

This is where Zeitro's Scenario AI comes in. It is an AI-Powered Mortgage Guideline Assistant specifically designed for us like Loan Officers, Processors, and Underwriters. It currently covers nearly 300 guidelines (and growing), including 34 specific Jumbo Mortgage Guidelines from major lenders like AD Mortgage, AmWest, CMG Financial.

Here is why I use it to streamline my research:

- Chat-Based Search: You don't need keywords. You can ask, "Does AD Mortgage allow a 680 FICO on a Jumbo loan with 15% down?" and get an answer in seconds. It handles both specific eligibility questions and vague "what if" scenarios.

- Accuracy: This is the biggest selling point. The AI doesn't just guess. It provides Citations. It links back to the exact page in the guideline source. This gives me the confidence (Trust) to quote clients because the answer is evidence-based.

- Comprehensive Coverage: It's not just for Jumbo. It covers QM and Non-QM, including DSCR, Bank Statement, ITIN, and Foreign National programs across 15+ mainstream lenders.

- Explain Feature: If a guideline is confusing (legalese is tough), you can use the "Explain" function to get a breakdown of what that specific clause actually means for your borrower.

- Cost-Effective: It starts at just $8/month. Considering it saves me hours of reading per week, the ROI is massive. Plus, you get 3 free queries a day to test it out.

FAQs About Jumbo Mortgage Guidelines

Q1. What are the rules for a jumbo mortgage?

The rules are defined by the specific investor but generally include: loan amounts exceeding FHFA limits, higher credit scores (typically 700+ on competitive programs), lower DTI ratios (usually max 43%), and significant post‑closing liquid reserves.

Q2. Do you have to put 20% down on a jumbo?

Not always. While 20% is the industry standard to secure the best rates and avoid mortgage insurance, many lenders offer Jumbo products with 10% or 15% down, usually requiring higher credit scores or slightly higher interest rates.

Q3. Are jumbo loans harder to get approved for?

In most cases, yes. Because they are typically not backed by Fannie Mae or Freddie Mac, Jumbo loans usually involve more manual underwriting, with lenders scrutinizing income stability, asset sourcing, and credit history more closely than on standard conforming loans.

Q4. What is Jumbo loan minimum?

The minimum is any amount that exceeds the FHFA‑set conforming loan limit for the county where the property is located. In 2026, that limit is $832,750 for one‑unit properties in most U.S. counties. Amount above that threshold generally triggers Jumbo guidelines.

Q5. Are Jumbo loan closing costs higher?

Generally, yes. Because the loan amount is higher, costs calculated as a percentage, like title insurance or origination fees will be higher. Additionally, you may pay for multiple appraisals.

Q6. Why avoid a jumbo loan?

Borrowers might avoid them because they typically come with stricter qualification requirements and often higher interest rates relative to conforming loans, though market spreads and competition can narrow this gap.

Final Word

Navigating the complex world of Jumbo Mortgages doesn't have to be a headache. Whether you are dealing with a picky underwriter or a complex borrower scenario, having accurate information at your fingertips is the key to closing more deals.

I highly recommend trying Zeitro's Scenario AI. It combines the speed of AI with the precision of actual lender guidelines, giving you a competitive edge. Stop guessing and start verifying with confidence. With a plan starting as low as $8/month and free daily queries, it is a tool that pays for itself on the very first deal you save.

Check your eligibility scenarios now at Zeitro.com.

People Also Read:

- What Are FHA Mortgage Guidelines? How to Verify FHA & Overlays Quickly?

- Conventional Mortgage Guidelines: What and How to Check Quickly?

- How to Get a DSCR Loan? Step-by-Step for Real Estate Investors

- 8 Best Non-QM Mortgage Lenders in 2026: Which to Choose?

- Mortgage Guidelines 2026: What Are They? How to Verify?

![[Solved] How to Calculate Commission Income for Mortgage?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a3ce1b02009d0aba39b3174_how-to-calculate-commission-income-banner.png)