![[2026 Update] 8 Highest-Rated Reverse Mortgage Companies for You](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/69a9410f689f89e0ab014f5a_best-reverse-mortgage-companies-banner.png)

Written by

Eric

Share this article

.svg)

Subscribe to updates

Last checked and updated in June 2026.

When my parents first considered tapping into their home equity to fund their retirement, the sheer number of reverse mortgage lenders left us completely overwhelmed. If you're a homeowner over 62, you probably feel the same way—anxious about hidden fees, aggressive sales tactics, and making an irreversible mistake with your biggest asset. You want a trustworthy partner, not just a sales pitch. That's why I've done the heavy lifting to evaluate the top lenders for 2026.

However, if navigating through endless reviews feels like too much work, you can skip the guesswork. I highly recommend using Bluerate's free AI Chat. It instantly matches you with top-rated, local loan officertailored to your specific financial situation, saving you time and stress.

How I Evaluated These Best Reverse Mortgage Companies

I didn't just skim marketing pages. For each lender, I checked four things: their Better Business Bureau rating and complaint history, their Trustpilot score and the substance behind recent reviews (not just the star count), their standing on the NMLS registry, and whether they're actively originating loans right now. That last point matters more than people realize — the reverse mortgage industry has consolidated fast over the past year, and a company that looked great in an old "best of" list might not even be taking new applications anymore.

I also leaned on my own family's experience going through the counseling and application process, plus conversations with loan officers who work in this space daily. Where a company's public reviews and its marketing didn't match up, I said so.

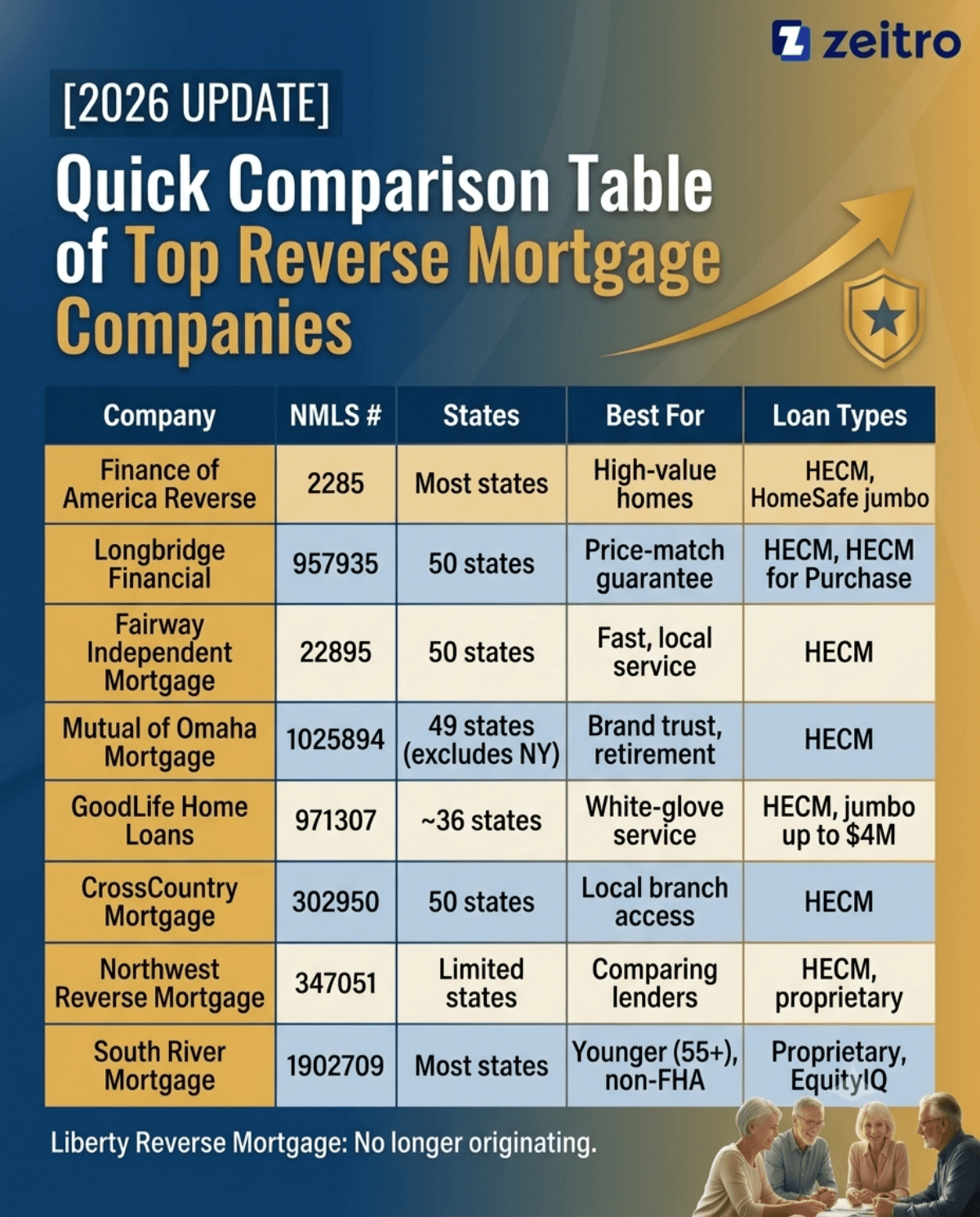

Quick Comparison Table of Top Reverse Mortgage Companies

8 Best Reverse Mortgage Companies to Consider

Below is my curated list of the top eight reverse mortgage companies for 2026. Keep in mind that these aren't ranked from best to worst. Rather, each has its own unique strengths. Whether you need the lowest fees, face-to-face service, or a massive jumbo loan, you'll find a match here.

1. Finance of America

NMLS Number: 2285

States: Available in most states (Not all 50)

Best for: Homeowners with high-value properties who need a jumbo option, or anyone who remembers AAG and wants continuity.

If your home is worth more than the 2026 FHA lending limit of $1,249,125, Finance of America Reverse (FAR) is one of the few lenders that can still get you meaningful proceeds. Its HomeSafe jumbo program goes up to $4 million and doesn't charge the mortgage insurance premium that standard HECMs require. FAR also absorbed American Advisors Group (AAG), the company behind the Tom Selleck ads you've probably seen, a few years back, so if you remember AAG, you're really looking at FAR today.

Borrowers I've read about consistently describe loan officers who explain the math rather than rush the sale, and the company keeps solid marks with the BBB. The tradeoff is size: with a large national footprint comes longer hold times if you need a specific loan officer, and their underwriting on proprietary jumbo products can be stricter than a standard FHA HECM.

Pros:

- Massive variety of proprietary products (like the HomeSafe loan).

- Minimum age of 55 for certain non-FHA loans.

Cons:

- Not licensed in every single U.S. state.

- Interest rates are middle-of-the-road compared to discount brokers.

2. Longbridge Financial

NMLS Number: 957935

States: All 50 states plus Washington, D.C.

Best for: Cost-conscious borrowers who want price transparency and don't mind a mostly digital process.

Founded in 2012, Longbridge Financial has built a reputation around borrower education and low costs. They are one of the few lenders actively trying to modernize the industry. For example, their newly launched "Platinum Preserve" product is fantastic. It allows you to tap into your home equity now while keeping 10% to 40% of it safely tucked away for your kids or future medical emergencies.

From my research, Longbridge really shines in customer service. They boast a stellar rating on Trustpilot (around 4.8/5), with thousands of seniors highlighting how transparent their fee structure is from day one. They even have a solid mobile presence, which is surprisingly uncommon in this sector. If you want a lender that operates nationwide, keeps origination fees competitive, and actively encourages you to explore alternatives before signing, Longbridge is a top-tier choice.

Pros:

- Licensed in all 50 states for maximum accessibility.

- Unique "Platinum Preserve" product lets you intentionally save equity for heirs.

Cons:

- Some proprietary products require higher minimum property values.

- The third-party appraisal process can occasionally be slow.

3. Fairway Independent Mortgage Corporation

NMLS Number: 2289

States: All 50 states plus Washington, D.C.

Best for: Homeowners who want in-person guidance and a quicker timeline to closing.

Sometimes, you just want to sit across a desk from a real human being and shake their hand. If that sounds like you, Fairway Independent Mortgage is exactly what you need. With over 30 years in the business and physical branches scattered across the entire country, they bring a local, personalized touch to a very intimidating financial decision. Fairway is famous in the real estate world for its speed.

While a typical reverse mortgage can take 30 to 45 days to close due to counseling and appraisals, Fairway's dedicated reverse underwriting team often cuts that time down significantly. Customer reviews across the web consistently highlight the warmth and responsiveness of their local agents. They might not have the flashiest digital tools, but their hands-on, face-to-face guidance provides incredible peace of mind for older homeowners.

Pros:

- Exceptional A+ BBB rating and huge local branch network.

- Known for closing loans significantly faster than the industry average.

Cons:

- Lacks a dedicated mobile app for reverse mortgage management.

- Rates can be slightly higher than online-only brokers.

4. Mutual of Omaha Mortgage

NMLS Number: 1025894

States: 49 states (Excludes New York)

Best for: Borrowers who value brand recognition and want the loan discussed in the context of their full retirement picture.

When it comes to financial products for seniors, name recognition matters. Mutual of Omaha has been a household name since 1909, and its mortgage division carries that same commitment to stability and trust. In recent years, they have been among the top HECM lenders in the United States by dollar volume, often ranking #1. What makes them stand out is how they view the reverse mortgage.

Their loan officers don't just sell you a loan. They look at how a HECM fits into your broader retirement portfolio, ensuring it won't negatively impact your Medicare or Social Security benefits. Online reviews frequently mention the relief of working with a legacy brand rather than a fly-by-night operation. They hold an A+ rating with the BBB. The only downside is that their conservative, careful approach means their underwriting process is rigorous.

Pros:

- Backed by a highly trusted, 100-year-old insurance and financial legacy.

- Excellent at treating home equity as part of a holistic retirement plan.

Cons:

- Underwriting guidelines can be quite strict.

- Not licensed to operate in New York.

5. GoodLife Home Loans

NMLS Number: 1325840

States: 38 states

Best for: Anyone who wants a "white glove," high-touch experience and lives in a state GoodLife serves.

This is the addition I most wanted to make to this list. GoodLife is a family-owned, Bellevue, Washington–based lender that's been quietly originating some of the highest-volume reverse mortgages in the country, and its customer satisfaction numbers are hard to argue with: an A+ BBB rating with essentially no unresolved complaints, and a Trustpilot average near 4.9 out of 5 across hundreds of reviews, with the vast majority landing at five stars. Reviewers repeatedly mention the same thing — loan officers who stay in touch daily and explain each document before asking for a signature.

The catch is availability. GoodLife doesn't lend in every state (New York, Massachusetts, and a handful of others are excluded), and you'll still need to work with a loan officer directly rather than complete everything online.

Pros:

- Borrowers can eliminate their current mortgage payments, freeing up monthly cash flow.

- By cutting out middlemen, GoodLife typically offers lower origination fees, closing costs, and competitive interest rates.

- The company holds an A+ BBB rating and generally excellent reviews on platforms like Trustpilot, with borrowers citing helpful and communicative loan officers.

- Borrowers can choose to receive funds as a lump sum, fixed monthly payments, or a line of credit.

Cons:

- Borrowers must be at least 62 years old, have significant equity (usually 50%+), and live in the home as their primary residence.

- Borrowers are still entirely responsible for paying property taxes, homeowners insurance, and home maintenance. Failing to do so can lead to foreclosure.

6. CrossCountry Mortgage

NMLS Number: 3029

States: All 50 states

Best for: Borrowers who prioritize a big national lender with local offices and are comfortable vetting their specific loan officer.

CrossCountry Mortgage is a giant in the traditional retail mortgage world, originating 1 in every 35 homes in the U.S. Recently, they have made a massive push into the reverse mortgage space, bringing over top-tier industry executives to build out a dedicated, highly trained reverse division. The main advantage of using CrossCountry is their sheer scale and resources.

They have access to over 170 investor outlets, meaning they can usually find a creative solution for unique property types or financial situations. Because they are so large, you can easily find a local branch in your town. The caveat, based on customer reviews, is that your personal experience will depend heavily on the specific loan officer you get. However, when you connect with one of their certified reverse specialists, the service is prompt and highly professional.

\

Pros:

- Licensed nationwide with a huge network of over 3,500 loan officers.

- Offers a true one-stop shop for both forward and reverse mortgages.

Cons:

- Reverse mortgages are a newer core focus compared to their traditional loans.

- Customer experience can vary widely depending on your specific local branch.

7. Northwest Reverse Mortgage

NMLS Number: 347051

States: 28 states

Best for: Homeowners who want a single broker to shop multiple lenders on their behalf.

Unlike the direct lenders on this list, Northwest Reverse Mortgage operates primarily as a specialized niche broker. I absolutely love this model for borrowers who want to comparison shop without making a dozen phone calls. Because they aren't tied to a single bank's products, Northwest can pull quotes from places like Finance of America, Longbridge, and others to find you the absolute best deal. They are particularly strong in the Pacific Northwest but are licensed in 28 states.

They offer everything from standard FHA HECMs to highly specific products like second-lien reverse mortgages. Reviews for Northwest are overwhelmingly positive, with clients praising their transparent, consultative approach. They act more like financial advisors than mortgage brokers. If you live in their service area, they are a phenomenal choice.

Pros:

- As a broker, they shop multiple lenders to find you the best rate.

- Access to unique products like the HomeSafe Second loan.

Cons:

- Limited geographic footprint (only available in 28 states).

- They originate the loan but don't service it long-term.

8. South River Mortgage

NMLS Number: 1854524

States: 28 states

Best for: Homeowners between 55 and 61, or anyone who wants a non-FHA proprietary option.

If you already have a reverse mortgage and are looking to refinance it to get a better rate or pull out more cash, South River Mortgage should be at the top of your list. They have carved out a very specific niche in HECM-to-HECM refinancing and have grown rapidly into the fourth-largest reverse lender in the country by volume.

South River is heavily technology-driven, which is how they manage to close loans in an average of just 26 days—lightning fast for this industry. While they only operate in about 28 states, their rates consistently rank among the lowest available. Looking at their Trustpilot feedback, homeowners are thrilled with the speed and the low fees. Once you start working with their team, the process is smooth, efficient, and highly professional.

Pros:

- Highly competitive interest rates, especially for refinancing.

- Extremely fast closing process (averaging around 26 days).

Cons:

- Limited state availability.

- Initial marketing outreach can feel a bit aggressive to some.

A Note on Liberty Reverse Mortgage — Why It's No Longer on This List

If you've seen Liberty Reverse Mortgage recommended elsewhere, here's what you need to know: as of early 2026, Liberty's parent company, Onity Group (formerly Ocwen, which also operates PHH Mortgage), stopped originating new reverse mortgages entirely and sold roughly 40,000 existing loans — about $9.6 billion in unpaid balance — to Finance of America Reverse. Onity said the move lets it focus resources on its forward-mortgage business.

If you already have a Liberty loan, nothing about your existing terms changes; PHH will continue servicing those loans under a multi-year agreement while Finance of America becomes the long-term owner. But if you're shopping for a new reverse mortgage today, Liberty simply isn't taking applications anymore, which is why I moved Finance of America Reverse — the company that now owns most of Liberty's book of business — to the top of this list instead.

Red Flags to Watch For, Regardless of Which Company You Choose

I'd be doing you a disservice if I only told you what to look for in a good lender and skipped what makes a bad one. Across the complaints I've read on the Consumer Financial Protection Bureau's public database and various review sites, a few patterns show up again and again:

- High-pressure sales tactics, especially urging you to sign before a required HUD counseling session is complete

- Vague answers about the margin and expected rate, which directly determine how much money you actually receive

- Downplaying the requirement to keep paying property taxes and homeowners insurance, since falling behind on either can trigger foreclosure even though there's no monthly mortgage payment

- Steering every borrower toward the same product regardless of age or home value, instead of comparing a standard HECM against proprietary alternatives

None of the companies above are on any official "avoid" list, but a legitimate lender should never make you feel rushed. If a loan officer gets impatient when you ask for numbers in writing, that's a reason to call someone else.

What to Know Before You Sign Anything

A reverse mortgage isn't free money, and I don't want this guide to make it sound like one. You're still responsible for property taxes, homeowners insurance, and basic home maintenance for as long as you live there — miss those and the loan can become due immediately. Interest accrues on the balance the entire time you hold the loan, which means your home equity shrinks as the years go on. And because it's a negative-amortization loan, the amount you (or your heirs) eventually owe can end up larger than what you originally borrowed, though federal insurance guarantees neither you nor your heirs will ever owe more than the home is worth at the time it's sold.

HUD requires independent, third-party counseling before you can close on a HECM specifically so someone without a financial stake in your decision walks you through all of this. Don't skip it, and don't let anyone rush you through it.

FAQs About Top Reverse Mortgage Companies

Q1. What is the dark side of reverse mortgage?

The main downside is the high upfront costs and compounding interest. Because you aren't making monthly payments, the interest rolls into the loan balance, which grows larger every month. Additionally, if you fail to pay your property taxes or home insurance, you face the very real risk of losing your home to foreclosure.

Q2. How much can a 70-year-old borrow on a reverse mortgage?

There isn't a single flat number. It entirely depends on your home's appraised value, current interest rates, and the exact age of the youngest borrower. Generally speaking, the older you are, the more equity you can access. A 70-year-old might qualify for roughly 45% to 55% of their home's value in today's market.

Q3. What is better than a reverse mortgage?

It depends on your goals. If you have the income to make monthly payments, a Home Equity Loan or a Home Equity Line of Credit (HELOC) usually has much lower closing costs. Alternatively, simply downsizing, selling your large house and buying a smaller, cheaper one with cash, is often the cleanest financial move.

Q4. Is a reverse mortgage a good idea for seniors?

Yes, but only in the right circumstances. It's an excellent tool if you plan to "age in place" and stay in your current home for the rest of your life. However, if you plan to move into an assisted living facility or relocate closer to your grandkids in the next few years, the high upfront fees make it a poor short-term choice.

Q5. Can a 90-year-old get a reverse mortgage?

Absolutely, yes. In fact, because the loan amounts are calculated based on life expectancy, a 90-year-old will be able to access a significantly higher percentage of their home's equity compared to a 62-year-old. There is no maximum age limit for these FHA loans.

Q6. What disqualifies you from a reverse mortgage?

You will be disqualified if the youngest homeowner is under 62 (for FHA loans) or 55 (for some jumbo loans). You also won't qualify if you lack sufficient equity (usually you need at least 50%), fail the financial assessment proving you can pay ongoing property taxes, or have delinquent federal debt.

Q7. Why do banks not recommend reverse mortgages?

Traditional big banks like Chase or Wells Fargo largely exited the reverse mortgage market years ago. These loans are highly regulated, complex, and carry reputational risks if a senior faces foreclosure due to unpaid taxes. Traditional banks prefer to sell you a standard HELOC because the profit model is simpler and less risky for them.

Q8. What is the 95% rule on a reverse mortgage?

The 95% rule allows heirs to repay a reverse mortgage by paying the lesser of the full loan balance or 95% of the home's current appraised value if they want to keep the house. They simply have to pay 95% of the home's current appraised value, and the FHA insurance covers the remaining deficit.

Q9. What is the 2026 HECM lending limit?

The Federal Housing Administration set the 2026 HECM lending limit at $1,249,125, up from $1,209,750 in 2025. This is the maximum home value the FHA will count when calculating your loan proceeds — if your home is worth more, only the amount up to that limit is used, unless you go with a proprietary jumbo product instead.

Q10. What are the alternatives to a reverse mortgage?

The most common alternatives are a home equity line of credit (HELOC), a cash-out refinance, downsizing to a smaller home, or a home equity agreement (HEA), which lets you sell a share of future appreciation for cash today. Each comes with different repayment timelines and risks, so it's worth comparing at least one alternative before committing to a reverse mortgage.

Conclusion: What Company is Best for a Reverse Mortgage?

Deciding to take out a reverse mortgage is one of the most significant financial choices you will make in retirement. It's not just about getting cash. It's about securing your long-term comfort while fully understanding the costs involved.

If you want a quick recap, here is my Best For list of reverse mortgage companies:

- Finance of America: Best overall options and jumbo loans.

- Longbridge Financial: Best for keeping upfront costs low.

- Fairway: Best if you want in-person, local customer service.

- Mutual of Omaha: Best for brand trust and retirement planning.

- Northwest: Best for having a broker compare rates for you.

Every homeowner's situation is entirely unique, and I always suggest talking to an independent financial advisor before signing anything. If you are ready to explore your exact numbers but don't want to deal with endless sales calls, try Bluerate AI Agent. It's the smartest way to safely connect with a vetted, local professional who actually understands your specific needs today.

People Also Read

- 8 Best Non-QM Mortgage Lenders in 2026: Which to Choose?

- Best DSCR Loan Lenders in 2026: Which to Choose from?

- Should Mortgage Lender and Broker Build In-House AI Tools?

- Mortgage Guidelines 2026: What Are They? How to Verify?

- Reverse Mortgage Eligibility: Check Requirements and Criteria Here