Written by

Eric

Share this article

.svg)

Subscribe to updates

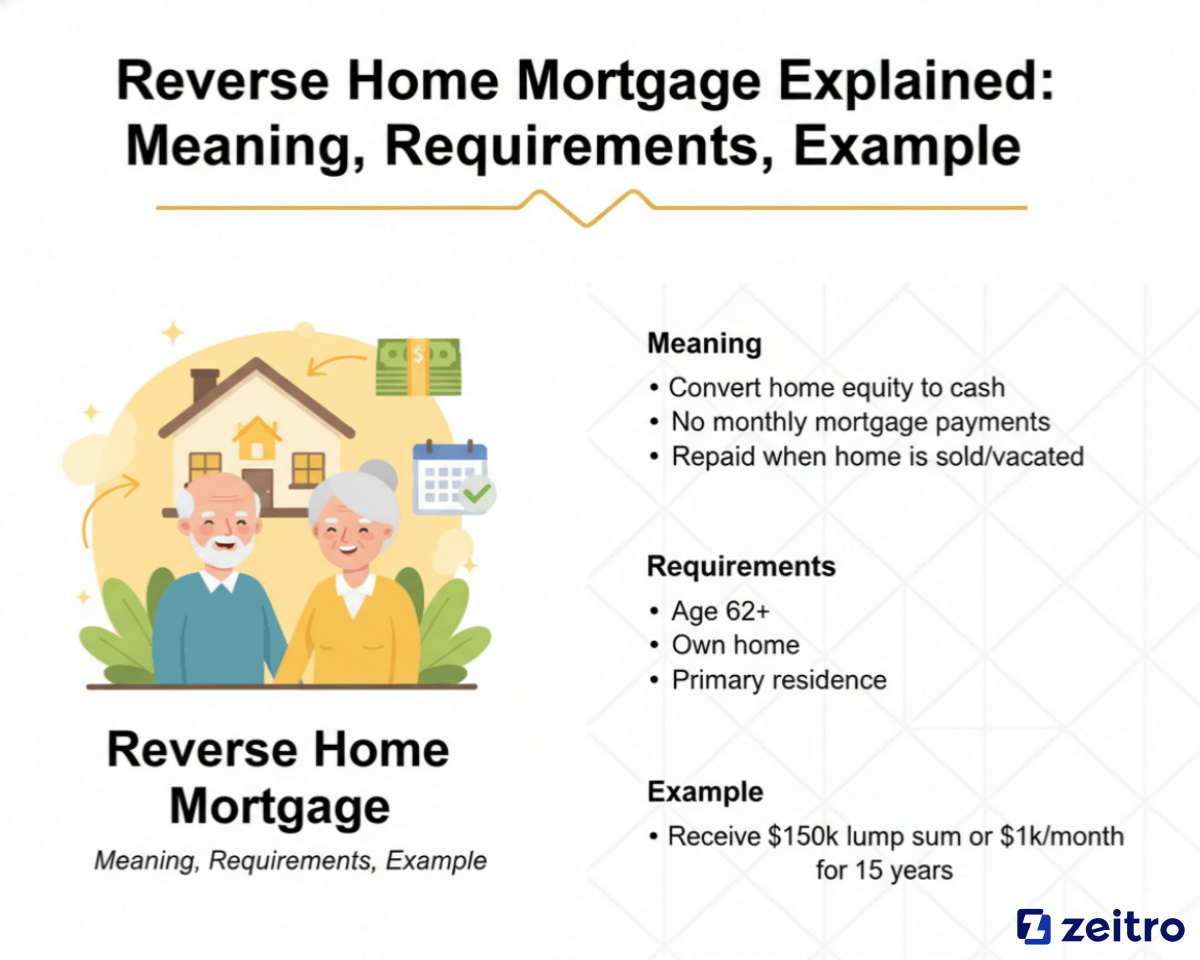

What is a reverse home mortgage, exactly? Basically, it lets homeowners 62 and older turn their house's equity into usable cash, without selling the place or taking on new monthly mortgage bills. After years in the lending industry, I constantly see seniors struggling with fixed incomes while sitting on a goldmine: their home. While the concept sounds simple, the actual 2026 rules can get pretty tangled.

For borrowers, knowing the basics is everything. For my fellow loan officers, leveraging AI tools like Zeitro helps us instantly verify reverse mortgage eligibility, so we can give clients the accurate, fast answers they desperately need.

What is a Reverse Mortgage?

Think of a traditional mortgage as you slowly buying your house from the bank. A reverse mortgage flips that script, the lender actually pays you based on the equity you've already built up. You skip the monthly principal and interest payments entirely.

This setup is exclusively for older homeowners. Whenever I sit down with clients, their first question is almost always, "Will the bank own my house?" Let me be crystal clear: you keep your title and ownership. You just live there like normal. The loan balance is only repaid when you permanently move out, sell the property, or pass away. It's simply a practical way to pad your retirement fund, cover unexpected medical bills, or afford basic home renovations without the heavy burden of a monthly payment hanging over your head.

Reverse Mortgage Example

Let's look at a realistic scenario. Take John, a 65-year-old retiree whose house is worth $500,000. He finally paid off his original mortgage years ago, but his current pension barely covers groceries and utilities.

By taking out a reverse mortgage, John taps into that $500,000 value. Since he has full equity, he qualifies for a tax-free line of credit. Instead of taking a massive lump sum, he sets up a $1,000 monthly payout to make life easier. Every month, his loan balance slowly grows because interest is added to what he borrows. But John still owns his home, lives comfortably, and never has to write a check to a lender.

Pros and Cons of a Reverse Mortgage

No financial product is perfect. I always insist my clients look closely at both sides of the coin before signing anything. Here is the honest breakdown:

Pros:

- Zero monthly mortgage bills: You stop paying monthly principal and interest.

- Tax-free money: The IRS treats the cash as loan proceeds, not taxable income.

- You stay put: You remain the legal owner and can live there forever.

- Payout choices: Pick a lump sum, monthly checks, or a standby line of credit.

Cons:

- Your debt grows: Interest piles up, increasing your total loan balance over time.

- Smaller inheritance: Your kids will inherit less equity.

- Steep upfront costs: Closing fees and mandatory insurance premiums aren't cheap.

- Ongoing property costs: You absolutely must keep paying property taxes and home insurance. Miss these, and you could face foreclosure.

What are the 3 Types of Reverse Mortgages?

If you decide this path makes sense, you'll need to pick the right program. Generally, the market offers three main types, depending on your home's worth and why you need the cash.

Home Equity Conversion Mortgages (HECMs)

HECMs are the industry standard. Because they are insured by the Federal Housing Administration (FHA), they offer great safety nets, like the guarantee that you'll never owe more than the home's market value.

However, the government sets strict boundaries. For 2026, the FHA capped the maximum claim amount at $1,249,125. So, if your house is worth $2 million, the lender still calculates your loan based on that $1.24 million ceiling. Also, to make sure older folks aren't being taken advantage of, the FHA forces every single applicant to complete a financial counseling session with an independent, HUD-approved advisor before the loan can move forward.

Proprietary Reverse Mortgages

Sometimes called jumbo reverse mortgages, these are private loans created by individual lending companies instead of the government. They are built specifically for borrowers sitting on multi-million dollar properties who want to borrow far past the FHA's limits.

Note for Mortgage Professionals: Handling proprietary products means dealing with messy, investor-specific Non-QM overlays. It used to take me hours to hunt down specific criteria. Now, top loan officers use Zeitro Strata AI to deep-search through 100+ investor guidelines. You can literally ask a vague scenario question and get a precise, fully-cited answer in seconds. It completely removes the guesswork when you are trying to structure a complex jumbo loan for a high-net-worth senior.

Single-Purpose Reverse Mortgages

These are the cheapest option out there, but they come with a major catch. Usually offered by local state agencies or non-profits, single-purpose loans restrict exactly how you spend the cash.

Just like the name says, the lender dictates the purpose. Typically, you can only use the funds for urgent home repairs, like fixing a collapsed roof, or catching up on past-due property taxes to avoid losing the house. While the fees and interest rates are rock-bottom compared to standard HECMs, you can't just use the money to pay for a vacation or daily groceries. Plus, these programs aren't available in every state, so you have to check with your local housing authority first.

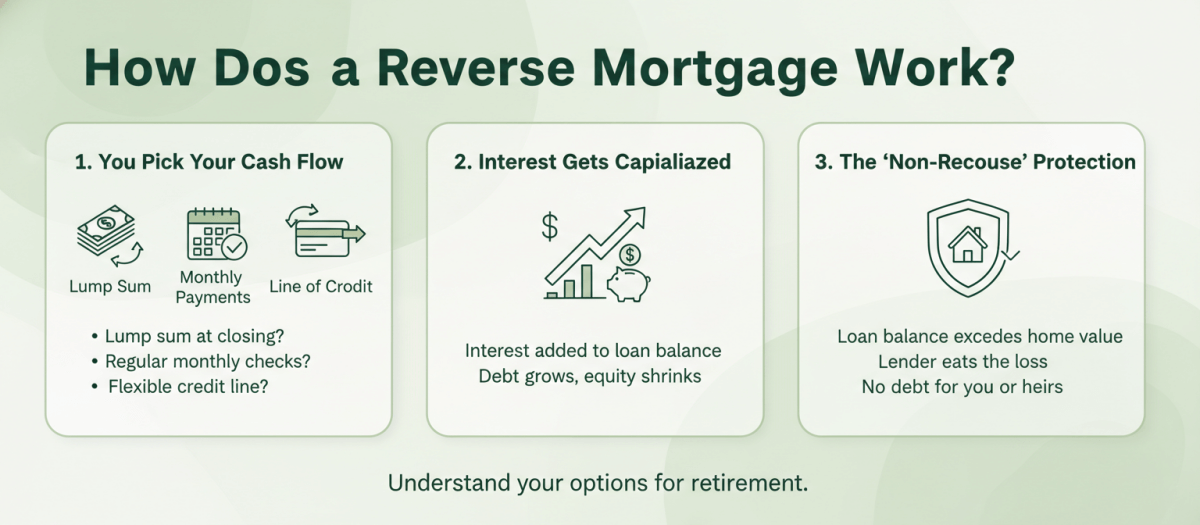

How Does a Reverse Mortgage Work?

The mechanics of these loans often confuse people. Let me break down exactly what happens to the money once you are approved:

- You Pick Your Cash Flow: Do you want a lump sum right at closing? Regular monthly checks? Or a line of credit you can tap into whenever you want? You get to choose the structure.

- Interest Gets Capitalized: Since you aren't sending the bank a check every month, the lender just adds that month's interest directly to your loan balance. Slowly but surely, your debt grows while your remaining home equity shrinks.

- The "Non-Recourse" Protection: This is huge. These are strictly non-recourse loans. If the housing market crashes and your loan balance eventually grows larger than what your house is worth, the lender eats the loss. Neither you nor your kids will ever have to pay the difference out of your own pockets.

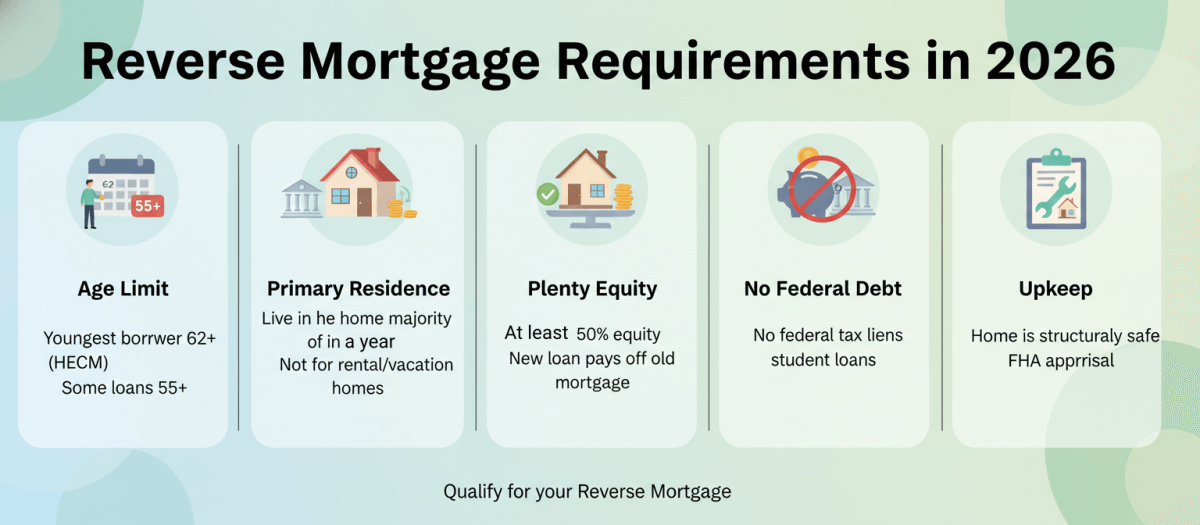

Reverse Mortgage Requirements in 2026

You can't just walk into a bank and demand a reverse mortgage. The 2026 rulebook has some pretty firm hurdles you have to clear first. Let's check the reverse mortgage eligibility below:

- Age Limit: The youngest borrower on the property title must be at least 62 for a standard HECM. Some proprietary jumbo loans may allow 55, but confirm with the specific lender

- Primary Residence: You actually have to live there for the majority of the year. Forget about using this on a beach house or a rental property.

- Plenty of Equity: A good rule of thumb is having at least 50% equity. The new reverse loan must be big enough to completely wipe out any old mortgage you still have.

- No Federal Debt: If you owe the IRS back taxes or defaulted on federal student loans, you're usually disqualified.

- Upkeep: An FHA appraiser will check to ensure the house is structurally safe and sound.

How Do You Qualify for a Reverse Mortgage?

Beyond the basic age and equity rules, lenders need to know you won't default on your basic homeowner duties. The approval process starts with that mandatory HUD counseling I mentioned earlier, just to prove you understand what you're signing up for.

Then comes the Financial Assessment. There is no minimum credit score requirement. Lenders assess your overall financial patterns to confirm ability to pay property taxes, insurance, and HOA fees. We have to verify you bring in enough cash every month to easily cover your property taxes, homeowners insurance, and HOA fees.

Chasing down borrower documents for this assessment is notoriously slow. Smart brokerages are moving to POS systems like Zeitro's Digital 1003. It lets borrowers self-pre-qualify online in minutes while AI instantly crunches the Debt-to-Income (DTI) ratios. It delivers pre-qualifications 2.5x faster and literally saves loan officers over 7 hours of manual data entry per file.

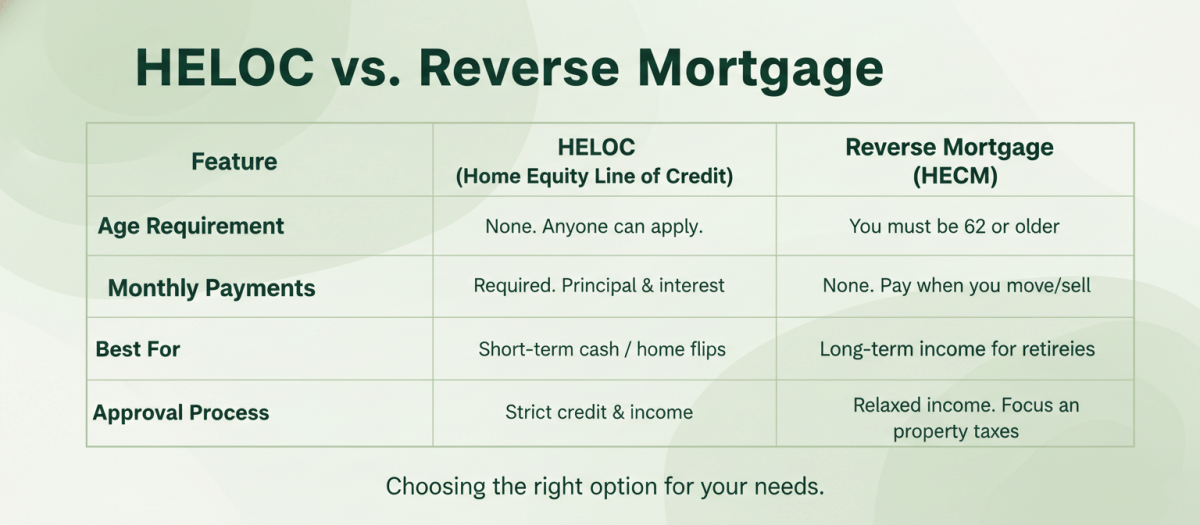

HELOC vs. Reverse Mortgage

"Should I just get a HELOC instead?" I hear this question constantly. While both let you turn your home's value into cash, they are entirely different animals. A Home Equity Line of Credit (HELOC) works like a massive credit card secured by your house, and it expects you to pay the money back right away. A reverse mortgage is built for long-term retirement survival.

Here is how they stack up against each other:

Basically, if you can afford another monthly bill, a HELOC is cheaper. If you need cash but cannot handle another payment, go with the reverse option.

FAQs About Reverse Home Mortgage

Q1. How to get out of a reverse mortgage?

By law, you get a three-day "Right of Rescission" to cancel the deal right after closing without any penalties. After that window closes, your only way out is to pay off the balance by selling the house or refinancing it into a traditional loan.

Q2. How do you pay back a reverse mortgage?

The debt typically comes due when the last borrower dies or permanently moves into a care facility. Heirs usually handle this by selling the house, paying off the lender, and keeping whatever profit is left over. Alternatively, they can use their own money to pay off the loan and keep the family home.

Q3. Is reverse mortgage interest deductible?

Not immediately. Because you aren't actually making monthly payments, you can't deduct the interest on your taxes every year. You only get to claim that mortgage interest deduction in the specific year the loan is entirely paid off.

Q4. How long does it take to get a reverse mortgage?

Expect the process to take roughly 30 to 45 days. It drags on a bit longer than a standard mortgage because you have to schedule the mandatory HUD counseling session and wait for a specialized FHA appraisal.

Q5. How much can I get from a reverse mortgage?

Your final number depends on your exact age, current interest rates, and the appraised value of your home. Generally, the older you are and the more your house is worth, the bigger your payout will be. You can pull personalized, instant rate quotes for clients using the Zeitro Pricing Engine, which grabs live pricing for both conventional and Non-QM products, so you can show borrowers real numbers in seconds.

Q6. How much equity do you need for a reverse mortgage?

Most lenders want to see that you own the home outright or have at least 50% equity. Since the new reverse loan has to pay off your old traditional mortgage first, you need a large cushion of equity to ensure you actually get cash in your pocket.

Conclusion: Is a Reverse Mortgage a Good Idea?

After guiding hundreds of families through this process, I firmly believe a reverse mortgage is a fantastic tool if used correctly. It's a lifesaver if you want to age in your own home, need to kill off your current mortgage bill, and want extra breathing room in your budget. But if you plan on moving soon, or if leaving a massive paid-off house to your kids is your top priority, skip it. Always sit down with a financial advisor first.

Handling these loans requires patience. By bringing AI solutions like Zeitro into your workflow, using DeepSearch for guidelines or setting up personal landing pages via GrowthHub, you can answer clients' questions instantly. It builds incredible trust and helps you close loans up to 20% faster when folks need your help the most.

People Also Read

- Full Guide: What is a non-QM Loan? Everything to Learn

- 8 Best Non-QM Mortgage Lenders in 2026: Which to Choose?

- Refinance Meaning: What Refinancing a Mortgage Really Means

- Breakdown: How Much Does It Cost to Refinance a Mortgage?