Written by

Eric

Share this article

.svg)

Subscribe to updates

It's finally happening. After years of "holding the line," we are seeing current mortgage refinance rates average 6.14% to 6.23% for 30-year conventional loans, with top-tier borrowers accessing rates around 5.5-5.6% on 15-year terms, but 30-year rates remain above 6% for most. If you bought your home in late 2023 or 2024 with a rate near 7.5% or 8%, the math for refinancing is starting to look undeniably attractive.

But here is the catch that trips up homeowners every single day: The headline rate isn't the price you pay.

I've sat across from countless borrowers who were ready to sign, only to be blindsided by the "Cash to Close" line item. Refinancing isn't free. It is a reinvestment in your financial future. To make it work, you need to understand exactly where every dollar goes and, more importantly, when you'll earn it back.

In this guide, I'm breaking down the real cost of refinancing in 2026, cutting through the industry jargon to show you the hidden fees, the negotiable line items, and the exact math to decide if this move is right for you.

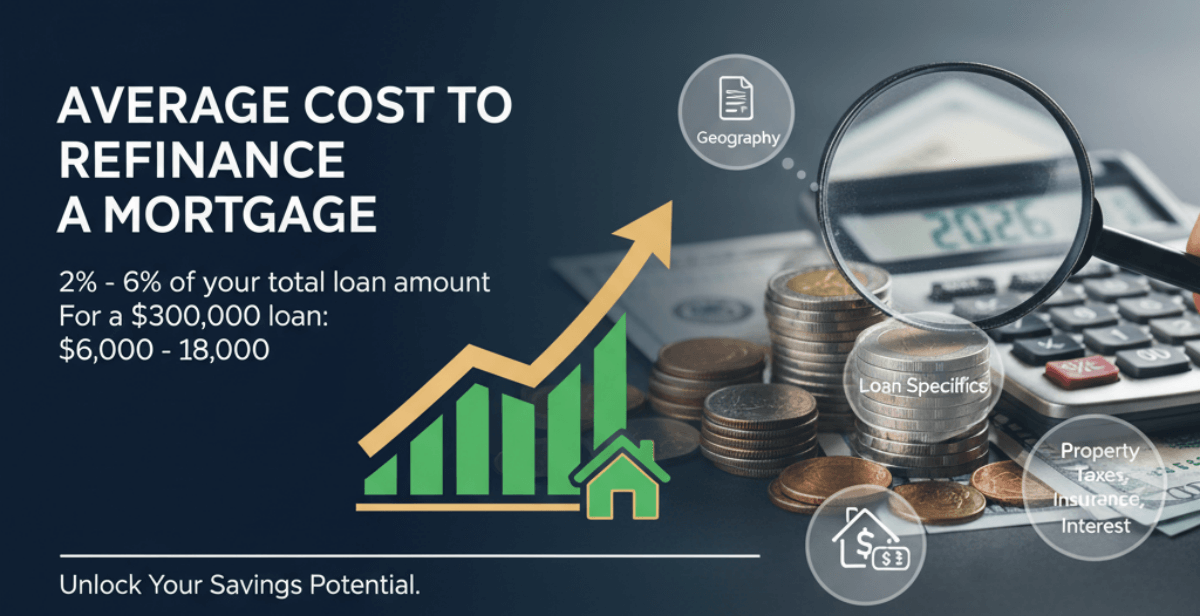

Average Cost to Refinance a Mortgage

Let's cut straight to the chase. In 2026, the average cost to refinance a mortgage typically falls between 2% and 6% of your total loan amount.

For a standard $300,000 refinance, this means you should expect to pay anywhere from $6,000 to $18,000 in total costs.

Why is that range so wide? It comes down to geography and loan specifics.

- The Base Cost: Recent ClosingCorp data shows average refinance closing costs (including taxes and recording) at about $2,403 or 0.72% of the loan amount for 2024, with median non-tax fees around $1,802. Freddie Mac aligns with 3-6% total, but no specific $2,400-$3,000 core figure is confirmed for 2026. For a $300,000 refinance, total costs range from $6,000-$18,000 (2-6%), which matches industry standards.

- The Variable Cost: The rest of that 2-6% chunk usually comes from prepaid items like property taxes, homeowners insurance, and daily interest.

In refinances, transfer taxes (mortgage recording taxes) vary: New York has high mortgage recording taxes (0.8-1.8%+ depending on amount), but Florida and Pennsylvania have low or no transfer taxes on refinances. Florida exempts them entirely. States like New York, California, or D.C. with high mortgage recording taxes push costs higher.

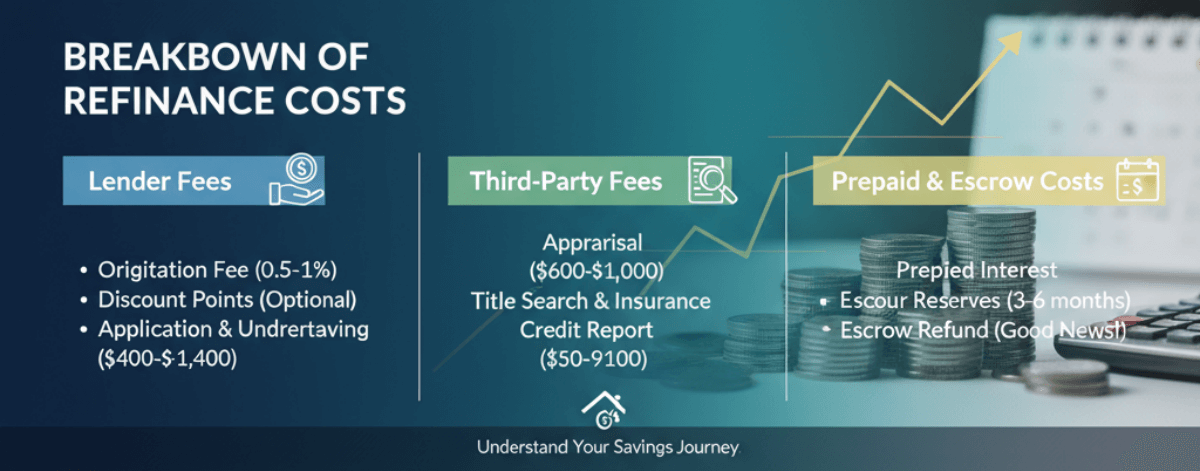

Breakdown of Refinance Costs

When you receive your Loan Estimate (LE), it can look like a wall of numbers. To make it digestible, I categorize these costs into three distinct buckets: Lender Fees, Third-Party Fees, and Prepaids.

Lender Fees

This is the money you pay directly to the mortgage company to process your loan. This category is also where you have the most room to negotiate.

- Origination Fee: This is the commission the lender charges for their service. It typically ranges from 0.5% to 1% of the loan amount ($1,500 - $3,000 on a $300k loan).

- Discount Points: This is optional. You can choose to pay an upfront fee ("points") to lower your interest rate permanently. In 2026, many borrowers are paying 1 point to get that rate under 6%.

- Application & Underwriting Fees: These are administrative costs for verifying your income and assets. These fees typically total $400-$1,400 combined (application $75-$500, underwriting $400-$900), often lower than stated.

Third-Party Fees

These are "pass-through" fees. Your lender doesn't keep this money. They collect it to pay the vendors who verify the property and your legal standing.

- Appraisal Fee ($600 - $1,000): Refinancing almost always requires a new appraisal to confirm the home's current market value. Prices have risen lately due to high demand and a shortage of appraisers in some areas.

- Title Search & Lender's Title Insurance ($400 - $900): This protects the lender against past ownership disputes. Note: You do not need to buy Owner's Title Insurance again, but Lender's Insurance is mandatory.

- Credit Report Fee ($50 - $100): The cost to pull your tri-merge credit report.

Prepaid & Escrow Costs

This is the most misunderstood section. Borrowers often get angry seeing these numbers, but this is technically your money.

- Prepaid Interest: You pay interest from the day you close until the end of the month.

- Escrow Reserves: Your new lender will likely require you to deposit 3-6 months' worth of property taxes and home insurance into a new escrow account.

Here's the good news. If you have an escrow account with your current lender, you will get a refund check for that balance about 30 days after you pay off the old loan. It eventually washes out, but you need the cash upfront to fund the new account.

Factors That Influence Refinance Costs

Not everyone pays the same price tag. I've seen two neighbors refinance the same floor plan but pay drastically different closing costs. Here is what moves the needle:

- Credit Score: This is the biggest driver. If your score is below 720, you might get hit with "Loan-Level Price Adjustments" (LLPAs). These are essentially risk fees added to your closing costs or your rate.

- Loan-to-Value (LTV) Ratio: If you have less than 20% equity in your home, you might have to pay higher fees or continue paying Private Mortgage Insurance (PMI).

- Loan Amount: There is an economy of scale here. A $500,000 loan doesn't cost much more to process than a $150,000 loan in terms of fixed fees like appraisal and title, so the percentage cost is often lower on larger loans.

- Property Type: Condos and multi-family homes often carry higher interest rates and origination fees than single-family detached homes because lenders view them as slightly riskier.

Real Refinance Cost Examples

To give you a realistic picture, let's look at the numbers for a standard $300,000 mortgage in three different situations.

Rate-and-Term Refinance Example

The Goal: Lower the interest rate and the monthly payment.

- Borrower Profile: 760 Credit Score, Single-Family Home.

- Lender Fees: $2,500

- Third-Party Fees: $2,200

- Prepaids/Escrow: $1,800

- Total Cost: $6,500

Verdict: This is the "cleanest" refinance with the lowest fees.

Cash-Out Refinance Example

The Goal: Take out $50,000 in equity for home renovations.

- Borrower Profile: 740 Credit Score, increased loan balance to $350,000.

- Lender Fees: $3,500 (Higher due to cash-out risk adjustments).

- Third-Party Fees: $2,500

- Prepaids/Escrow: $2,200

- Total Cost: $8,200

Verdict: Cash-out loans are viewed as riskier, so lenders often charge higher origination fees or slightly higher interest rates.

Investment Property Refinance Example

The Goal: Refinance a rental property.

- Borrower Profile: 720 Credit Score, Non-Owner Occupied.

- Lender Fees: $4,500 (Includes "points" to buy down the rate).

- Third-Party Fees: $2,500

- Prepaids/Escrow: $2,500

- Total Cost: $9,500+

Verdict: Investment properties always come with a premium. Expect to pay 0.5% to 0.75% more in rate or fees compared to your primary home.

How to Lower the Cost to Refinance a Mortgage

You are not helpless when it comes to these fees. Here are four proven strategies to reduce your "Cash to Close":

- Ask for an Appraisal Waiver: If you have significant equity (usually 30%+), ask your Loan Officer to run the automated underwriting system. You might get a waiver, instantly saving you $600−$1,000.

- Negotiate the "Reissue Rate": If you bought your home or refinanced within the last few years, ask the title company for a "reissue rate" on the lender's title insurance. This can slash the premium by up to 40%.

- Boost Your Credit Score: Even a 20-point bump can move you into a better pricing tier, reducing those hidden LLPA fees.

- Shop Around (The Smart Way): This is the single most effective way to save. However, avoid the "lead aggregator" websites that sell your phone number to 50 aggressive cold-caller.

I recommend using platforms like Bluerate.ai. Unlike traditional sites, Bluerate connects you directly with experienced Loan Officers rather than assigning you a random salesperson. You can compare real, transparent quotes and fees from different officers side-by-side without the spam. It puts the control back in your hands.

Can You Refinance with No Closing Costs?

You will often see ads screaming "No Closing Cost Refinance!" It sounds amazing, but as an insider, I have to tell you: There is no such thing as a free lunch.

In a "No-Cost" refinance, the fees don't disappear. they just move.

- The Trade-off: The lender gives you a "Lender Credit" to cover your $6,000 in closing costs. In exchange, they charge you a higher interest rate (e.g., 6.5% instead of 6.0%).

- When to do it: If you plan to sell the house or move in less than 5 years, this is a brilliant strategy. You save the upfront cash, and you won't hold the loan long enough for the higher interest rate to hurt you.

- When to avoid it: If this is your "forever home," take the lower rate and pay the closing costs upfront. Over 30 years, that 0.5% difference will cost you tens of thousands of dollars, far more than the closing costs you "saved."

Refinance Cost vs Savings: How to Calculate the Break-Even Point

Before you sign any paperwork, you must do this one calculation. It determines if the refinance is an investment or a waste of money.

The Formula: Total Closing Costs ÷ Monthly Savings = Months to Break Even

Example:

- Total Closing Costs: $5,000

- New Monthly Savings: $250

- Calculation: $5,000 ÷ $250 = 20 Months

Here's the rule. If you plan to stay in the home longer than 20 months, the refinance is a win. If you think you might move in a year, don't do it. You will lose money.

Checklist: Ideal Candidates for Refinancing in 2026

Is this guide for you? If you can check at least one of these boxes, you should be getting a quote today:

- Rate Drop: Your current rate is at least 0.75% to 1% higher than today's market rate (e.g., you are at 7.25% or higher).

- Credit Improvement: Your credit score has improved by 50+ points since you bought the house (qualifying you for cheaper insurance or rates).

- PMI Removal: Your home value has risen enough that you now have 20% equity and can eliminate expensive Mortgage Insurance.

- ARM Expiration: You have an Adjustable Rate Mortgage (ARM) that is about to reset to a higher rate.

Cost to Refinance Mortgage: FAQs

How much does it cost to refinance a $300,000 mortgage?

On average, for a $300,000 loan, you can expect total closing costs to range between $6,000 and $18,000. This includes lender fees, title work, and your prepaid escrow items. The "sunk costs" (fees that don't go toward your escrow) are typically around $3,000 - $5,000.

Are refinance costs tax-deductible?

Generally, no. Unlike when you buy a home, standard closing costs on a refinance for a primary residence are not deductible. However, if you pay discount points to lower your rate, you can deduct them over the life of the loan. Note: For rental properties, these rules differ, and costs are often deductible as business expenses.

Is it better to roll closing costs into the loan?

If you are short on cash, rolling costs into the loan balance is a convenient option. However, be aware that you will pay interest on those costs for the next 30 years. It's better to pay cash upfront if you can afford it to keep your loan balance low.

Why is my refinance quote higher than expected?

If your quote seems high, check the Prepaids section. You might be funding a brand new escrow account for taxes and insurance. Also, if your credit score has dipped or you are taking cash out, lenders may have applied risk-based fees (LLPAs) that drove up the cost.

Final Verdict: Is Refinancing Worth the Cost in 2026?

Refinancing is not just about bragging rights for the lowest interest rate at a dinner party. It is a mathematical decision.

In 2026, with rates stabilizing and offering relief from the highs of the past two years, the opportunity is real. If you can lower your rate by 0.75% or more and plan to stay in your home past the break-even point, the upfront cost is a temporary hurdle for years of long-term savings.

My final piece of advice? Do not accept the first offer you receive. Loan Officers have different compensation structures, and fees can vary wildly.

To ensure you aren't overpaying, I highly recommend using Bluerate.ai. It's the modern way to shop: you get direct access to top-rated Loan Officers who compete for your business, giving you a clear, transparent view of the costs without the middleman markups.

Run the numbers, shop the rate, and make 2026 the year you take control of your mortgage.