Written by

Eric

Share this article

.svg)

Subscribe to updates

If you've been watching the headlines, you know the mortgage landscape is finally shifting in 2026. After seeing rates hover near or above 7% for what felt like ages, the recent dip toward the low 6% range, and even seeing some 5-handles, has everyone buzzing. You might be hearing neighbors or coworkers talk about "refi-ing" to save hundreds a month.

But here's the truth: refinancing isn't just a magic button you press to save money. It's a strategic financial maneuver. In this guide, I'm going to strip away the banking jargon and explain exactly what refinancing means, how the math works, and most importantly, how to figure out if it's the right move for your wallet right now.

What Is Home Refinance?

Refinancing is the act of trading in your old mortgage for a brand-new one.

I often tell my clients to think of it like a balance transfer on a credit card, but with much higher stakes and more paperwork. You aren't just "editing" the terms of your current loan with your bank. Instead, you are technically applying for a completely new loan, whether with your current lender or a new one. This new loan pays off your existing debt entirely, and you start fresh with a new interest rate, a new term (length of the loan), and a new monthly payment.

Because this is a new loan, it triggers a "do-over" on the approval process. The bank will underwrite you all over again. They will check your credit score, verify your current income, and usually require an appraisal to see what your home is worth today compared to when you bought it. It's a restart button for your home debt, designed to get you better terms than you had before.

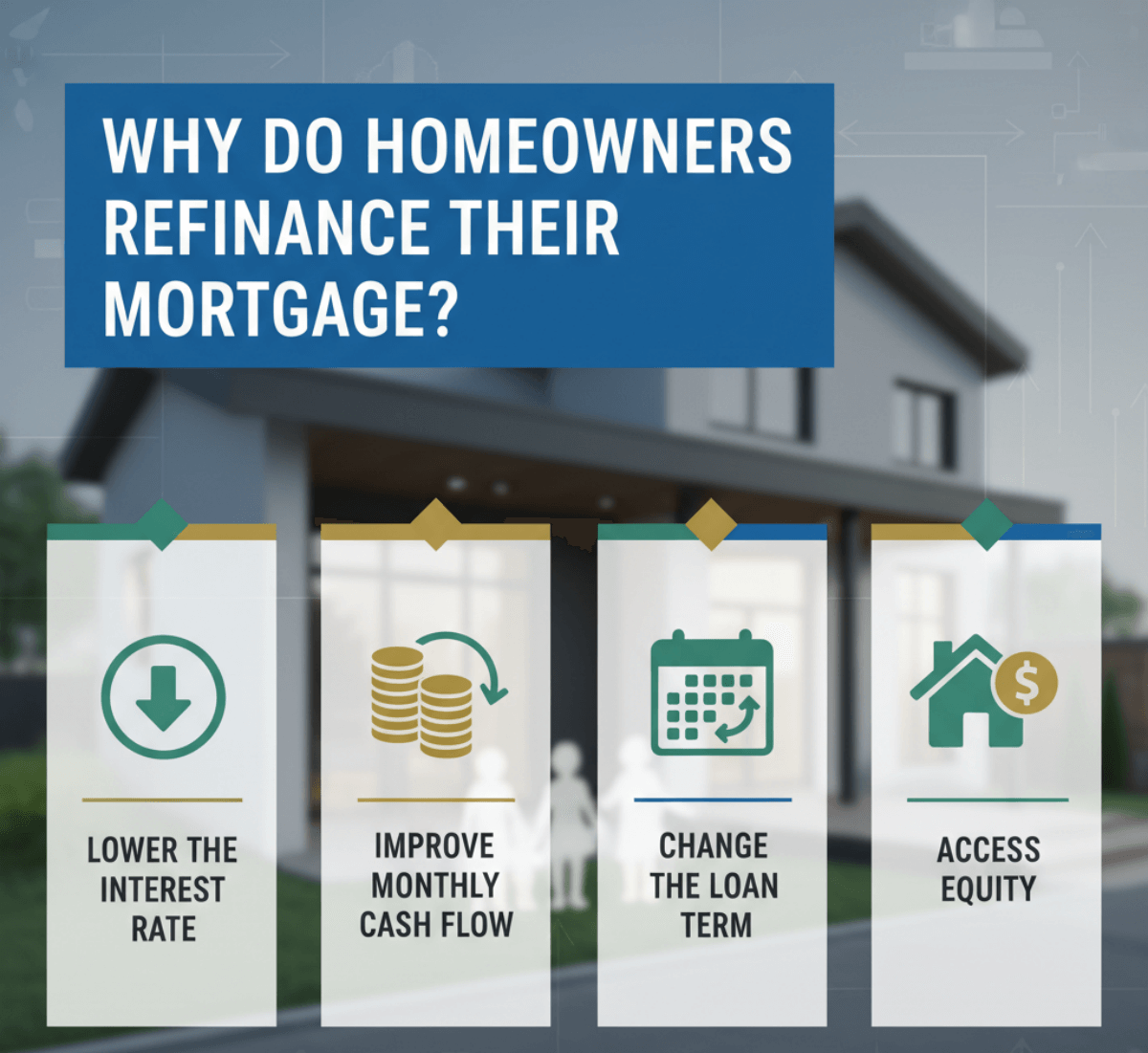

Why Do Homeowners Refinance Their Mortgage?

Why go through the hassle of paperwork again? Usually, it comes down to one of four major motivations, and it's rarely just about "saving money."

- Lower the Interest Rate: This is the big one. If you bought your home in 2023 or 2024 when rates were peaking, swapping that 7.5% rate for a 6% rate in today's market can save you significant interest over the life of the loan.

- Improve Monthly Cash Flow: Sometimes, life gets expensive. By refinancing to a lower rate, or extending your loan term back out to 30 years, you can drastically shrink your monthly obligation, freeing up cash for bills or savings.

- Change the Loan Term: I've seen many homeowners who want to be debt-free faster refinance from a 30-year to a 15-year mortgage. Your monthly payment might go up, but you'll pay way less interest to the bank in the long run.

- Access Equity: If your home's value has skyrocketed, you can "cash out" some of that profit to pay off high-interest credit cards or fund a renovation, effectively using your house as a low-interest piggy bank.

How Does Home Refinancing Work?

Let's look under the hood at the mechanics of this transaction. It can seem confusing because you stay in the same house, but the debt instrument changes completely.

When you close on a refinance, your new lender (let's call them Lender B) wires a lump sum of cash to your old lender (Lender A). This sum covers the remaining balance of your original mortgage. Lender A marks your account as "Paid in Full" and sends a lien release to your county recorder. The old debt is dead.

Simultaneously, you sign a new promissory note with Lender B. This new note is the legal agreement that dictates your new 6.2% interest rate or whatever you locked in and your new payment schedule.

Behind the scenes, this swap requires the same level of scrutiny as your first purchase. The new lender is taking on risk, so they need to validate that your house is still sufficient collateral (the appraisal) and that you are still capable of paying (income verification). Once the dust settles, you simply start sending your payments to the new address, often skipping one month of payments in the transition, a nice little bonus for your cash flow.

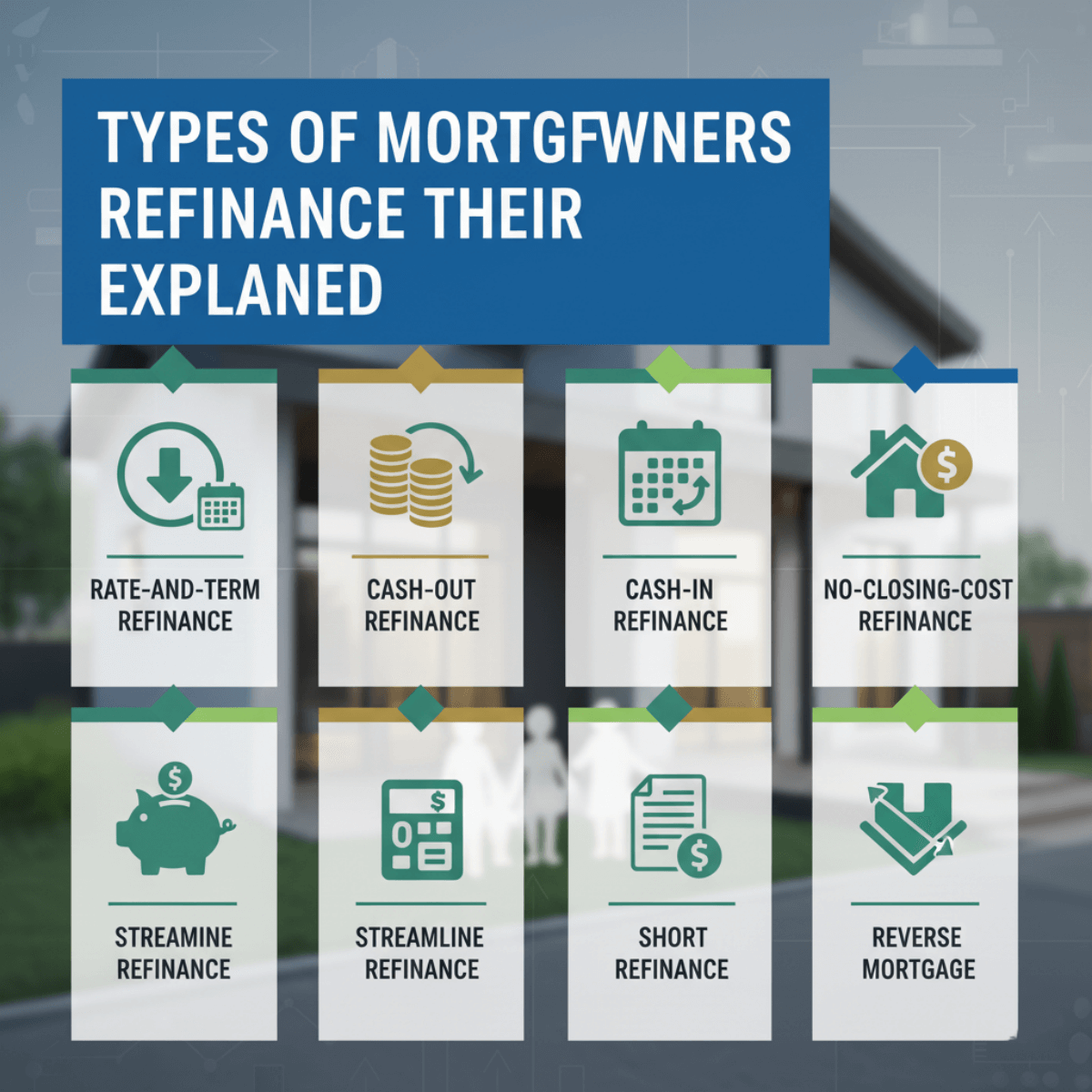

Types of Mortgage Refinance Explained

Not all refinances are built the same. The right strategy for you depends entirely on why you are making the switch.

Rate-and-Term Refinance

This is the "vanilla" option and the most common type I see. You aren't trying to pull cash out of your home. you are simply changing the interest rate or the term, like moving from 30 years to 15 years. The goal here is purely financial efficiency, spending less on interest or paying the house off sooner.

Cash-Out Refinance

Here, you take out a new loan that is bigger than what you currently owe. The difference is paid to you in tax-free cash at closing. For example, if you owe $200,000 but your home is worth $400,000, you might get a new loan for $260,000 and pocket the $60,000 difference. Just remember: you must usually leave at least 20% equity in the home.

Cash-In Refinance

This is the opposite of a cash-out. You bring a lump sum of cash to the closing table to pay down your loan balance. Why? Maybe you want to get your Loan-to-Value (LTV) ratio below 80% to finally get rid of that pesky Private Mortgage Insurance (PMI), or perhaps you want to qualify for a lower interest rate tier.

No-Closing-Cost Refinance

Let's be real: "No cost" is a marketing myth. The loan officers, appraisers, and title companies still need to get paid. In this scenario, the lender pays your closing costs for you, but in exchange, they charge you a slightly higher interest rate. You save money upfront, but you pay for it monthly. It's a trade-off, not a free lunch.

Streamline Refinance (FHA/VA/USDA)

If you already have a government-backed loan (like FHA or VA), you might qualify for a "Streamline." These are fantastic because they cut through the red tape, often requiring no appraisal and minimal income documentation. However, there are rules, like the "210-day wait period" for FHA loans, ensuring you've made enough on-time payments before applying.

Special or Less Common Refinance Options

Short Refinance: Rarely seen unless the economy is in trouble, this involves the lender agreeing to lower the principal balance because the house is worth less than the loan (underwater).

Reverse Mortgage: Designed for homeowners aged 62+, this allows you to convert equity into cash without making monthly mortgage payments. The loan is repaid when you move out or pass away.

Pros and Cons of Refinancing a Home Loan

Refinancing is a powerful tool, but like any power tool, you can hurt yourself if you don't use it correctly.

Advantages of Refinancing

The benefits can be transformative. If you drop your rate by just 1%, you could save tens of thousands of dollars in interest over the life of the loan. Refinancing can also stabilize your budget. If you are currently in an Adjustable-Rate Mortgage (ARM) that is about to spike, switching to a Fixed-Rate loan gives you peace of mind. Furthermore, consolidating high-interest credit card debt (often 20%+) into a mortgage (around 6-7%) via a cash-out refi can save huge amounts of monthly cash.

Disadvantages and Risks to Consider

The biggest downside is the cost. Refinancing isn't free. Closing costs typically run between 2% and 6% of the loan amount. If you refinance a $300,000 loan, you could pay up to $18,000 in fees. There is also the "clock reset" risk. If you've been paying your 30-year mortgage for 10 years and then refinance into a new 30-year loan, you are extending your debt sentence to 40 years total. This often means paying more total interest, even with a lower rate.

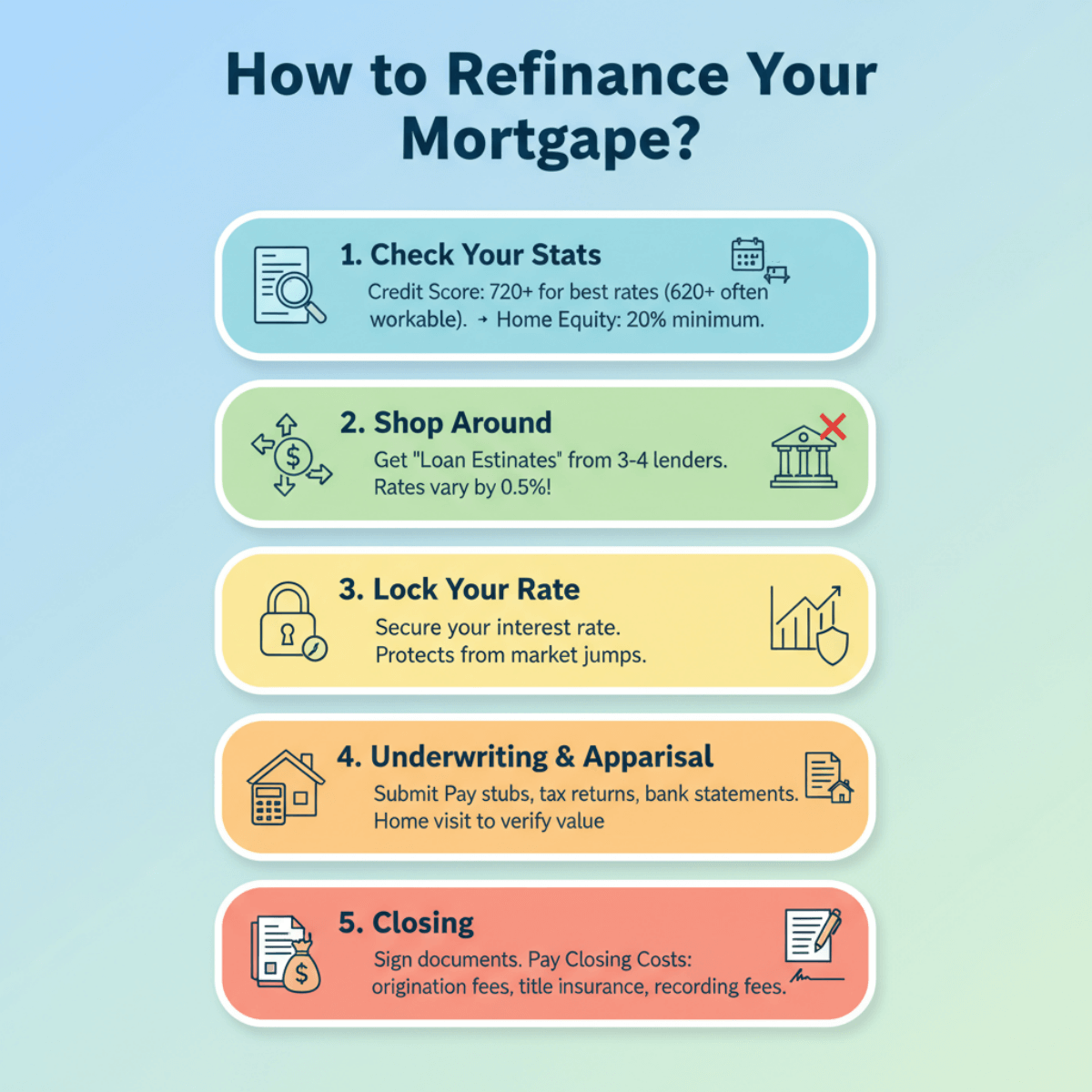

How to Refinance Your Mortgage?

Ready to pull the trigger? Here is your actionable roadmap. This process generally takes 30 to 45 days from start to finish.

- Check Your Stats: Before applying, pull your credit report. In late 2025, lenders are looking for scores above 720 for the best rates, though 620+ is often workable. Also, estimate your home equity, you usually need at least 20% equity to get the best deal.

- Shop Around: Don't just sign with your current bank. Get "Loan Estimates" from 3-4 different lenders. I've seen rates vary by 0.5% between lenders on the same day. That's massive savings you shouldn't leave on the table.

- Lock Your Rate: Once you find a winner, "lock" the rate. This protects you if market rates jump up while your paperwork is being processed.

- Underwriting & Appraisal: You'll submit pay stubs, tax returns, and bank statements. An appraiser will visit your home to verify its value.

- Closing: You'll sign a stack of documents, which is similar to when you bought the house. You will also pay your Closing Costs, which cover origination fees, title insurance, and recording fees.

When Does Refinancing Make Sense and When It Doesn't

Deciding to refinance shouldn't be based on a gut feeling. It's a math problem. The magic number you need to find is your Break-Even Point.

Here is the formula I use:Total Closing Costs ÷ Monthly Savings = Months to Break Even.

Let's look at a real-world example. Say your refinance will cost you $5,000 in fees, butit lowers your monthly mortgage payment by $200.$5,000 ÷ $200 = 25 months.

- It Makes Sense IF: You plan to live in the home for more than 25 months. After month 25, that $200 savings is pure profit in your pocket.

- It Doesn't Make Sense IF: You plan to sell the house next year. You would spend $5,000 to save $2,400 (12 months x $200), leaving you with a net loss of $2,600.

Also, be careful if you are nearly finished paying off your loan. Refinancing a small balance with only 5 years left into a new 30-year term is rarely a smart financial move.

Home Refinance FAQs

Does refinancing always save you money?

No. If you extend your loan term significantly or pay high closing costs for a very small rate reduction, you might end up paying more in total interest over the long run, even if your monthly payment drops.

Can you get cash when you refinance?

Yes, via a Cash-Out Refinance. However, you typically cannot withdraw 100% of your home's value. Lenders generally require you to keep 20% equity (80% Loan-to-Value ratio) in the property to protect their investment.

Does refinancing reset your mortgage term?

Yes, it usually does. If you take out a new 30-year loan, the clock starts at year zero. However, you can choose a shorter term (like 15, 20, or even a custom 22-year term) to avoid extending your debt timeline.

Is it better to refinance or make extra payments?

It depends on your goal. If you want to lower your required monthly obligation for safety, refinance. If your goal is strictly to pay off the house faster and save interest, making extra principal payments on your current loan is often cheaper since it costs $0 in fees.

Final Thoughts: Is Refinancing a Smart Financial Move?

Refinancing is one of the most powerful levers you can pull to improve your financial health, but it demands precise timing and clear math. It's not just about chasing the lowest headline rate. It's about ensuring the closing costs don't eat up your savings and that the new loan aligns with your long-term life plans.

Every homeowner's situation, credit history, equity position, and future goals, is unique. Online calculators are great for a rough estimate, but they can't predict underwriting nuances. To ensure you're making the most profitable decision for your specific situation, I highly recommend speaking with a loan officer at Bluerate. Our experts can offer a free, no-obligation consultation to analyze your numbers and help you secure the best possible rate in today's shifting market.

People Also Read

- Full Guide: What is a non-QM Loan? Everything to Learn

- Mortgage Loan Officer Salary: How Much Do Loan Officers Make?

- What Does a Loan Officer Do? Duties, Pros, Cons, and Outlook

![[Solved] Can I Use K-1 Income to Qualify a Borrower?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a44cb55129383ad19f46080_can-i-use-k-1-income-to-qualify-a-borrower-banner.png)