Written by

Eric

Share this article

.svg)

Subscribe to updates

If you are anything like the clients I talk to daily, you are probably exhausted. For the better part of three years, we have been playing a waiting game, checking apps every morning, hoping for a miracle drop in interest rates. As we close out 2025, the fatigue is real. You want to know: are mortgage rates expected to go down in 2026, or is this simply the new reality we have to accept?

I'm not going to sugarcoat it, we aren't going back to 2021. However, looking at the data heading into 2026, there is finally a legitimate path toward relief. It won't be a crash, but a slow, steady thaw. Here is my deep dive into what the numbers say for the year ahead.

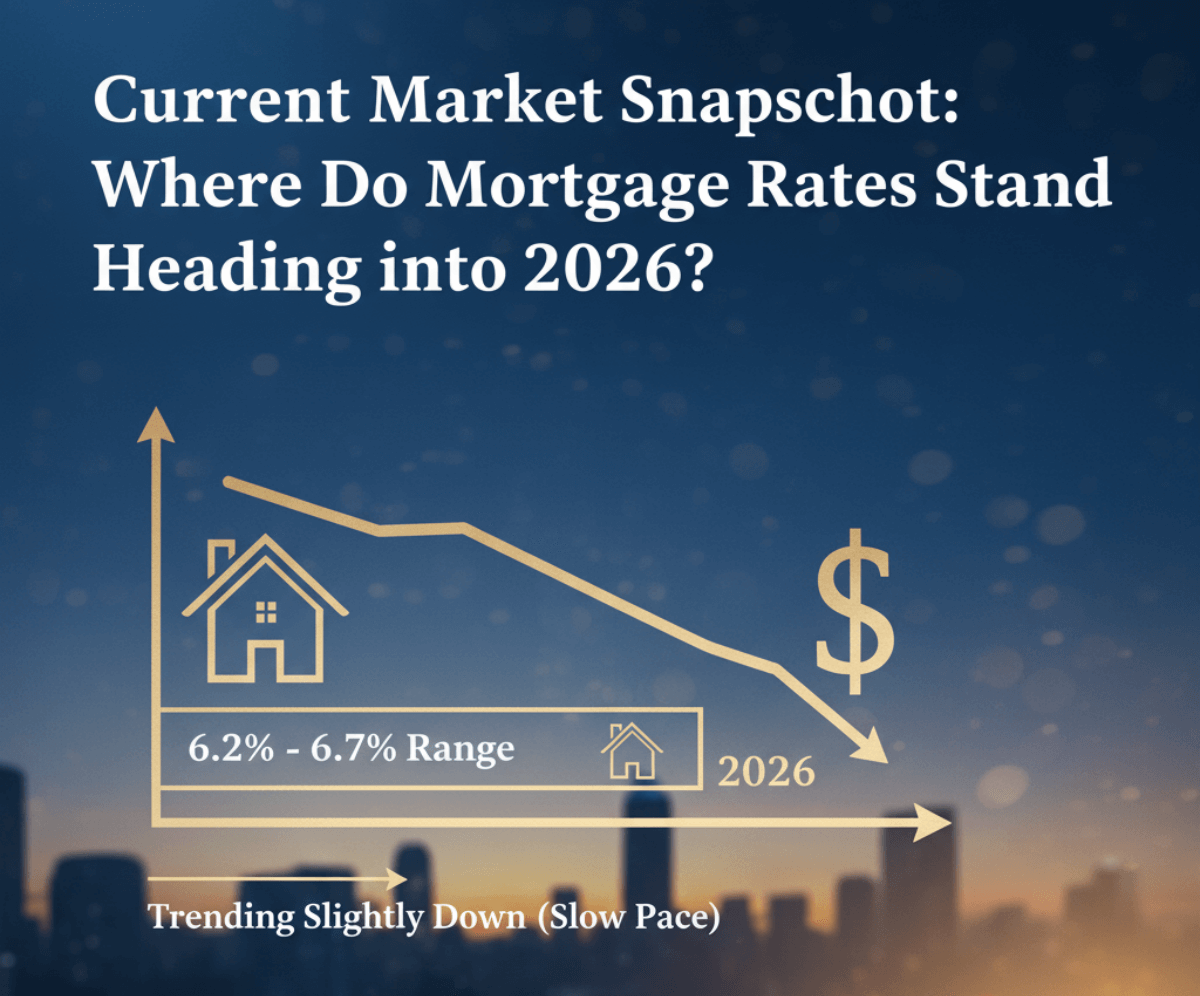

Current Market Snapshot: Where Do Mortgage Rates Stand Heading into 2026?

As we stand here in December 2025, the market feels like it's holding its breath. We aren't seeing the wild volatility of 2023, but we haven't seen a massive plummet either. Currently, the 30-year fixed mortgage rate is hovering in the 6.2% to 6.7% range depending on your credit score and loan type.

The question on everyone's mind is are mortgage rates going up or down from this baseline? The short answer is: they are trending slightly down, but the pace is agonizingly slow. We saw rates dip briefly below 6.2% earlier this quarter, only to bounce back up on strong labor data. This "sticky" behavior is frustrating, but it establishes a floor. We are entering 2026 with stability, which, while boring, is better than the unpredictability of previous years.

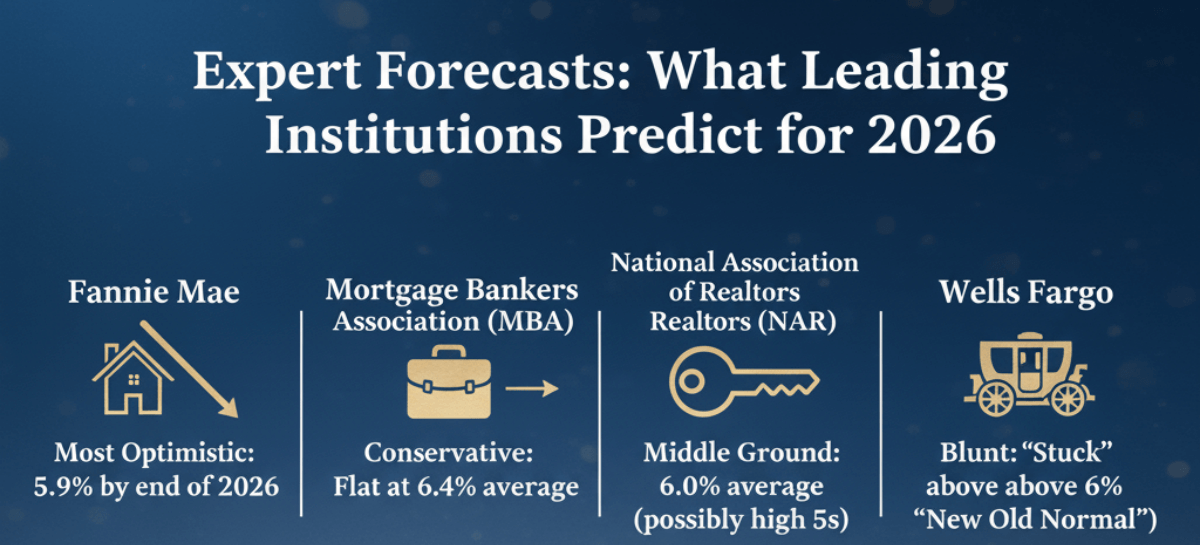

Expert Forecasts: What Leading Institutions Predict for 2026

I always tell homebuyers to never rely on just one opinion. To get a clear picture of when are mortgage rates going down, we need to look at the consensus from the major movers in the industry.

Here is what the heavy hitters are projecting for 2026:

- Fannie Mae: They are currently the most optimistic, forecasting that rates will slowly descend throughout the year, potentially ending 2026 around 5.9%. They are betting on the Federal Reserve making consistent cuts as inflation stabilizes.

- The Mortgage Bankers Association (MBA): The MBA takes a more conservative stance. Their latest forecast suggests rates will remain relatively flat, averaging around 6.4% for most of 2026. They believe economic headwinds will keep lenders cautious.

- National Association of Realtors (NAR): NAR sits in the middle but leans optimistic. They project rates could average 6.0%, with a possibility of dipping into the high 5s if the bond market cooperates.

- Wells Fargo: Their economists are blunt, they see rates "stuck" above 6% for the foreseeable future, viewing this as the "new old normal."

The consensus is a range between 5.9% and 6.4%. No major institution is predicting a return to 4% next year.

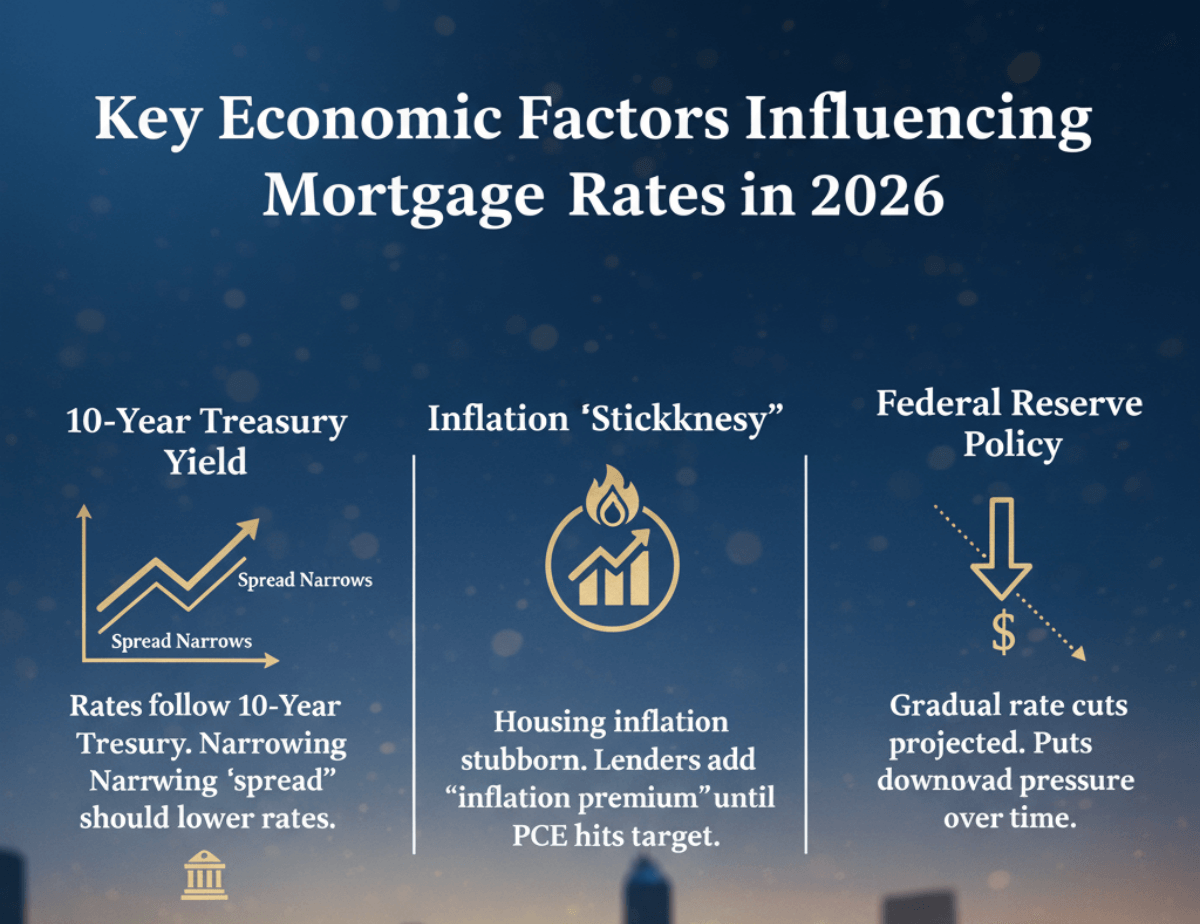

Key Economic Factors Influencing Mortgage Rates in 2026

To understand why are mortgage rates going down (even slowly), we have to look under the hood of the economy. It's not just about what the Fed says. It's about three specific levers:

- The 10-Year Treasury Yield: Mortgage rates don't follow the Fed Funds Rate directly. They follow the 10-year Treasury note. Right now, the "spread" (the difference between the Treasury yield and mortgage rates) is still historically high. As economic fear subsides in 2026, this spread should narrow, naturally lowering rates even if Treasury yields stay flat.

- Inflation "Stickiness": We have made progress, but inflation in the housing services sector remains stubborn. Until the Personal Consumption Expenditures (PCE) index hits the Fed's target consistently, lenders will bake an "inflation premium" into your rate.

- Federal Reserve Policy: The Fed is walking a tightrope. They are cutting rates to support the labor market, but they are moving slowly to avoid reigniting inflation. Their "dot plot" for 2026 suggests continued, gradual cuts, which puts downward pressure on mortgage rates over time.

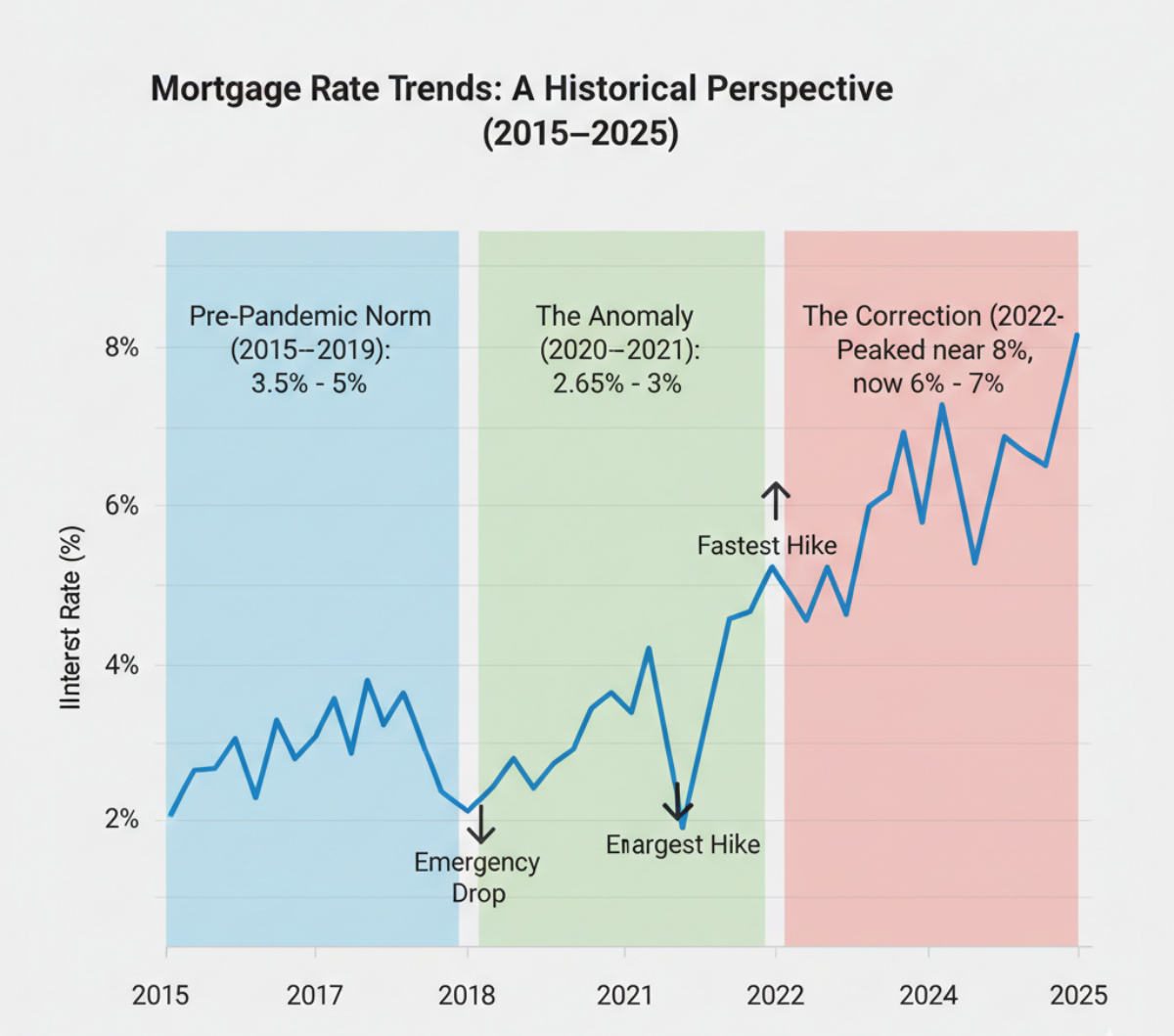

Mortgage Rate Trends: A Historical Perspective (2015–2025)

Context is everything. If you only look at the last five years, your perception is likely skewed.

- The Pre-Pandemic Norm (2015–2019): Rates fluctuated between 3.5% and 5%. It was a healthy, balanced market.

- The Anomaly (2020–2021): Rates dropped to 2.65% – 3%. This was an emergency response to a global crisis, not a normal market feature.

- The Correction (2022–2025): We saw the fastest rate hike in history, peaking near 8% and settling into the 6% – 7% range we see today.

When we zoom out, 2026 looks a lot more like 2005 or 2018 than 2021. We are returning to historical averages, painful as that might be to admit.

Long-Term Outlook: Mortgage Rate Forecast for the Next 5 Years

Looking beyond 2026, experts suggest we are settling into a "New Normal." The structural forces that kept rates low for a decade (like globalization and cheap labor) are shifting.

For the next 5 years (2026–2030), the baseline expectation is for rates to settle in the 5.5% to 6.5% corridor. Why? Demographics. The Millennial and Gen Z cohorts are the largest home-buying generations in history. This massive demand creates a floor for how low rates can go. Unless there is a severe economic recession, we likely won't see sub-4% rates in this 5-year cycle.

The "Lock-in" Effect: Will Inventory Increase in 2026?

One of the biggest reasons home prices haven't crashed is the "lock-in" effect. About 80% of mortgage holders have a rate below 6%, and many are sitting on 3%. Why sell and trade a 3% rate for a 6.5% one?

However, heading into 2026, the cracks are forming. Life happens, people get divorced, have triplets, or relocate for jobs. They have to sell. Realtor.com forecasts an 8.9% increase in active inventory for 2026. While we are still below pre-pandemic inventory levels, this increase will give buyers more leverage than they've had in years. It's not a flood of homes, but it's a steady stream.

Strategic Decision: Should You Buy Now or Wait Until 2026?

This is the million-dollar question. Should you pull the trigger now or wait for that predicted 5.9%?

The Cost of Waiting Calculator (Scenario Analysis)

Let's do the math on a $400,000 home.

- Scenario A (Buy Now): You buy at $400k with a 6.5% rate.

- Monthly P&I: ~$2,528.

- Scenario B (Wait 1 Year): Rates drop to 5.9%, but home prices appreciate by a modest 3% (historically conservative). The home is now $412,000.

- Monthly P&I: ~$2,443.

The Result: Waiting saves you about $85/month. However, you missed a year of amortization (paying down debt) and missed out on $12,000 in equity growth. Often, the increase in home prices eats up the savings from a slightly lower rate.

Strategies for Buying in a High-Rate Environment

If you decide to buy in 2026, don't just accept the headline rate.

- 2-1 Buydown: Ask the seller to pay for a temporary rate reduction (2% lower year 1, 1% lower year 2). This buys you time to refinance.

- ARM (Adjustable Rate Mortgage): If you plan to move in 7 years, a 7/1 ARM often offers a rate significantly lower than the 30-year fixed.

- Date the Rate": Secure the house price now. When rates drop to 5.5% in the future, refinance. You can change your loan. You can't change the purchase price.

FAQs: Understanding Future Mortgage Rate Movements

Q1. Will interest rates realistically drop to 4% in 2025 or 2026?

No. I have seen zero credible data to support this. Unless the U.S. enters a catastrophic recession (which brings other problems like job loss), a 4% rate is not in the cards for this cycle. Plan for 6%, be happy with 5%.

Q2. Will mortgage rates ever see 3% again?

"Ever" is a long time, but in the near future? Highly unlikely. 3% was a "Black Swan" event caused by a global pandemic. Basing your financial future on the return of a crisis anomaly is a dangerous strategy.

Q3. How does the Fed Funds Rate impact my mortgage rate?

It's an indirect relationship. The Fed controls short-term rates (credit cards, HELOCs). Mortgage rates track long-term bonds. Sometimes the Fed cuts rates, and mortgage rates actually go up because the market had already "priced in" the cut. Don't expect a 1-to-1 drop.

Q4. Is 2026 projected to be a buyer's or seller's market?

It is shaping up to be a Balanced Market, leaning slightly towards sellers due to low supply. While inventory is rising (up ~9%), there are still more qualified buyers than there are good homes. You will have more choices than in 2024, but don't expect fire-sale bargains.

Conclusion: Navigating the 2026 Housing Market

So, are mortgage rates expected to go down in 2026? Yes, modestly. But if you are waiting for the "perfect" time, you might be waiting forever.

The housing market of 2026 is about trade-offs. We are looking at a year of stability, slightly lower rates, and slowly increasing inventory. My advice? Stop trying to time the market perfectly. Professionals get it wrong half the time. Look at your monthly budget. If you can afford the payment comfortably at 6.4%, and you plan to stay in the home for 5+ years, buying is still a solid move.

You can always refinance a rate. You cannot refinance the price you paid. Stay informed, stay patient, and focus on what you can control.

People Also Read

- 8 Best Non-QM Mortgage Lenders in 2026: Which to Choose?

- Best CRM for Loan Officers 2026: Which One Suits You Most?

- Full Guide: What is a non-QM Loan? Everything to Learn