Written by

Eric

Share this article

.svg)

Subscribe to updates

Whenever I talk to homebuyers or fellow loan professionals, one common frustration always comes up: mortgage guidelines are painfully complex and constantly changing. If you're wondering how to check mortgage eligibility in 2026, you're definitely not alone. Figuring out whether a borrower qualifies traditionally takes hours of digging through massive PDF manuals.

But the process is evolving. While everyday buyers still need to understand the basic requirements to do a quick self-check, mortgage professionals can now instantly verify mortgage eligibility with accurate sources using AI-native tools like Zeitro, which even offers free daily queries to get started.

What is Mortgage Eligibility?

Mortgage eligibility is simply the set of financial criteria lenders use to decide if you can afford to repay a home loan. When I evaluate a file, I look at factors like income history, debts, credit, and down payment. Since limits update annually, here are the baseline minimum requirements for 2026:

- Conventional Loans: You'll need a minimum credit score of 620 and at least 3% down. The 2026 baseline conforming loan limit for most U.S. counties is $832,750 for a single-family home, with high-cost areas up to $1,249,125.

- FHA Loans: Ideal for lower credit. You need a 580 score for a 3.5% down payment.

- VA & USDA Loans: Both offer 0% down options for eligible veterans or rural buyers, though most lenders prefer a 620-640 credit score.

- Non-QM Loans: These skip traditional W2 requirements. If you're self-employed, you can qualify using alternative methods like bank statements or DSCR (Debt Service Coverage Ratio) for investment properties.

Also Read:

- What Are FHA Mortgage Guidelines? How to Verify FHA & Overlays Quickly?

- Conventional Mortgage Guidelines: What and How to Check Quickly?

- VA Mortgage Guidelines: What Are They and How to Check Them Quickly?

- Foreign National Mortgage Guidelines: Verify Eligibility Fast

- How to Determine Mortgage Eligibility? Verify Guidelines in Seconds

- Max DTI for Mortgage: Requirements By Loan Types

Who Needs to Comply with Mortgage Eligibility?

You might think these rules only apply to the person buying the house, but compliance is actually a two-way street. Both sides of the transaction must strictly follow the guidelines to ensure a successful closing.

- Borrowers: Whether you are a standard W-2 employee seeking a conventional mortgage or a real estate investor applying for a Non-QM loan, you must prove you meet the lender's financial thresholds to get approved.

- Lenders and Loan Professionals: Brokers, loan officers, and wholesalers must meticulously verify every applicant against massive rulebooks. If we approve a loan that doesn't actually comply with the stated mortgage eligibility guidelines, the lender risks massive financial penalties or holding unsalable loans.

Why Do You Need to Check Mortgage Eligibility?

I always advise my clients and colleagues to run the numbers before even opening Zillow. Why? Because checking your status upfront saves a lot of heartbreak and wasted time.

- Understand Purchasing Power: You immediately know your realistic price range, preventing you from falling in love with a home you simply can't finance.

- Identify Red Flags Early: A quick check reveals credit reporting errors or high debts, giving you time to fix them before officially applying.

- Speed Up Pre-qualification: Having your numbers ready makes the formal pre-qualification process much faster, letting you make aggressive offers in a competitive market

- Find the Right Loan Program: It helps match you to the perfect product. If your tax returns don't show enough income, checking early reveals that you should pivot to a Non-QM bank statement loan instead.

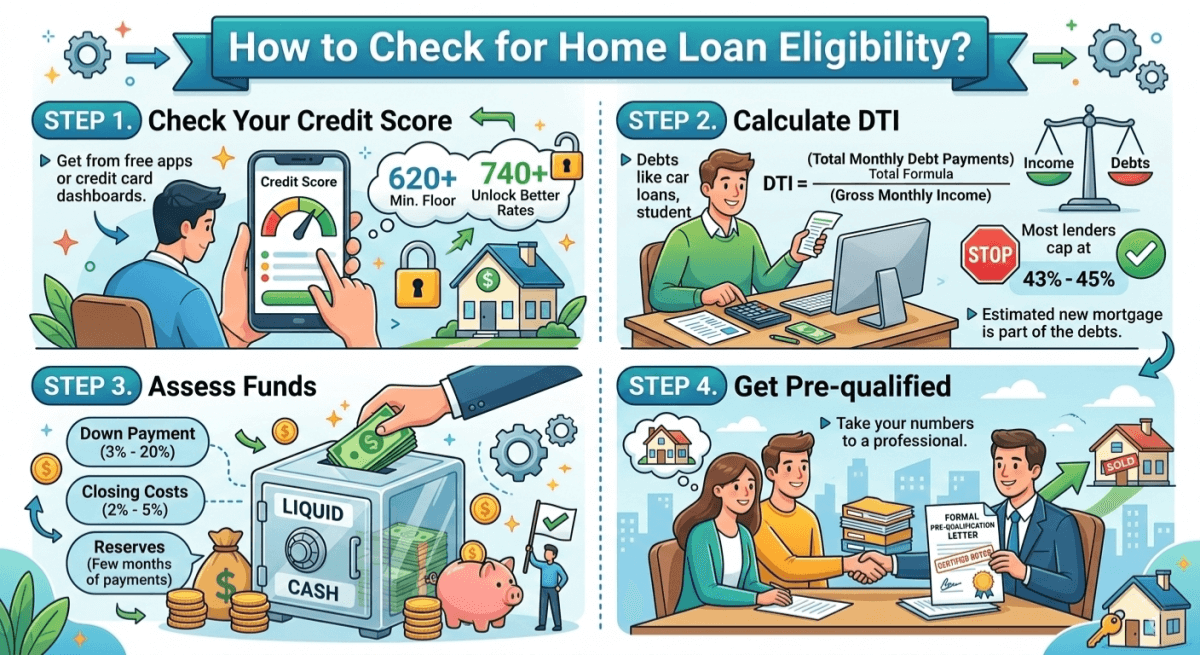

How to Check for Home Loan Eligibility?

If you want to know where you stand, doing a basic self-assessment is easier than you think. Here are the steps I recommend to check for home loan eligibility before contacting a bank.

STEP 1. Check Your Credit Score

Your credit dictates almost everything. Pull your score from a free app or your credit card dashboard. Keep in mind that a 620 is the floor for conventional options, but pushing that score above 740 will unlock significantly better interest rates and cheaper mortgage insurance.

STEP 2. Calculate DTI

Lenders care deeply about your Debt-to-Income (DTI) ratio. Take your total monthly debt payments (car loans, minimum credit card payments, student loans) plus your estimated new mortgage payment, and divide that by your gross monthly income. Most QM (Qualified Mortgage) lenders cap this at 43% to 45%.

STEP 3. Assess Funds

Look at your liquid cash. You need enough to cover the down payment (anywhere from 3% to 20%), plus closing costs (usually 2% to 5% of the loan amount). Lenders also like to see "reserves," which is a few months of mortgage payments sitting safely in your bank account.

STEP 4. Get Pre-qualified

Once you've run your own numbers, take them to a professional. A loan officer can run a soft credit pull and give you a formal pre-qualification letter, which proves to sellers that you are a serious and capable buyer.

How to Verify Mortgage Eligibility? (For Professionals)

While borrowers can do a rough self-check, loan officers and brokers face a much harder task. We have to cross-reference borrower data against 300+ constantly shifting guidelines to verify eligibility. It used to be a nightmare of manual reading, but now, I rely on Zeitro Strata AI.

Zeitro is an AI-native SaaS platform built exclusively for the U.S. mortgage industry. This mortgage AI is an incredibly powerful mortgage guideline assistant that completely transforms how we work. Here is what it brings to the table:

- Instant DeepSearch with Citations: Instead of spending 30 minutes reading PDFs, you can type a scenario and get an accurate answer in seconds. It cross-checks over 100 investors and provides exact citations, so you always have a verifiable source.

- Comprehensive Non-QM & QM Coverage: It doesn't just know Fannie Mae and FHA. Zeitro Strata AI covers complex Non-QM scenarios, like Asset Utilization, DSCR, ITIN, and Foreign National loans, from mainstream lenders like AD Mortgage and Luxury.

- Customizable Scenario Analysis: You can narrow searches using custom tags for specific loan types or lenders. If an answer seems complicated, the "Explain" feature acts as a secondary AI review to break down the logic further.

- Boost Efficiency & Close Rates: Using Zeitro saves professionals over 7 hours per loan file and delivers 2.5x faster pre-qualifications. Plus, it currently offers 3 free queries a day, making it easy to test out.

FAQs About Checking Mortgage Eligibility

Does checking my mortgage eligibility hurt my credit score?

Usually, no. An initial pre-qualification check by a lender only requires a "soft pull," which has zero impact on your credit score. It's only when you move forward with a formal, full application that a "hard pull" occurs.

Can I get a mortgage with a high DTI ratio?

Yes, it's definitely possible. If your DTI exceeds the traditional 45% limit, you might need to make a larger down payment, pay off smaller debts, or explore Non-QM loans that offer much more flexible debt-to-income underwriting standards.

What is the difference between Pre-qualification and Pre-approval?

Pre-qualification is a quick estimate of how much you can borrow based on unverified information you provide. Pre-approval carries much more weight because the lender has thoroughly verified your tax returns, bank statements, and actual credit report.

How do Non-QM loans affect eligibility?

Non-QM (Non-Qualified Mortgage) loans drastically expand eligibility for people who don't fit the standard mold. Instead of requiring traditional W-2s, they allow self-employed buyers or investors to qualify using alternative documents like bank statements or property rental income.

Also Read: Non-QM Loan Guidelines: How to Check and Verify with AI Accuracy

How long does a mortgage eligibility check take?

For a buyer doing a basic self-assessment, it takes just a few minutes. For mortgage professionals using modern AI tools like Zeitro, verifying complex, multi-layered investor guidelines now literally takes seconds instead of hours.

Conclusion

Understanding your borrowing power is the crucial first step in any real estate journey. Whether you're aiming for a standard conventional loan or a complex DSCR setup, knowing your 2026 limits and requirements saves everyone involved massive amounts of time.

- If you are a mortgage professional tired of manually digging through guidelines, you need to modernize your workflow. I highly recommend trying Zeitro Strata AI. It gives you fast, fully-cited answers and you can start with 3 free queries every day to instantly boost your productivity.

- On the other hand, if you are a homebuyer ready to find out exactly what you qualify for, head over to Bluerate. There, you can connect directly with top-tier loan officers equipped with the best technology to get a free consultation and personalized rate quotes today.

People Also Read

- Reverse Mortgage Eligibility: Check Requirements and Criteria Here

- Best No Income Verification Mortgage Lenders

- Best DSCR Loan Lenders: Which to Choose from?

- 8 Best Non-QM Mortgage Lenders: Which to Choose?