Written by

Eric

Share this article

.svg)

Subscribe to updates

Non-QM loans are booming, but navigating their extremely fragmented guidelines is an absolute nightmare. I've spent over a decade as a loan professional, and nothing drains my energy faster than digging through a 300-page PDF from a private investor just to verify one specific detail for a borrower. The sheer lack of standardization leads to deal-killing mistakes, lost hours, and massive frustration.

Fortunately, the days of relying on endless scrolling and manual searches are officially over. Today, you can check Non-QM loan guidelines with 100% accuracy and verify complex borrower scenarios in seconds using AI tools like Zeitro Strata.

What are Non-QM Loans?

Put simply, a Non-Qualified Mortgage (Non-QM) is a loan that doesn't fit the strict "Qualified Mortgage" rules set by the CFPB. While traditional QM loans conform to standardized Fannie Mae and Freddie Mac criteria, Non-QM loans offer incredible flexibility. The biggest difference? Non-QM lending focuses on alternative income verification and the borrower's true ability to repay (ATR) rather than demanding standard W-2s or pristine credit histories.

They are perfect for high-quality borrowers, like self-employed individuals or real estate investors, who just happen to fall outside the traditional lending box.

Here are the most common Non-QM loan types:

- Bank Statement Loans: Verifies income using 12 to 24 months of business or personal bank deposits.

- DSCR (Debt Service Coverage Ratio) Loan: Uses the property's rental cash flow to qualify rather than personal income.

- ITIN Loans: For borrowers who pay US taxes using an ITIN instead of a Social Security Number.

- Asset Utilization: Allows borrowers to qualify based on liquid assets instead of monthly income.

- Foreign National Loans: Designed for non-U.S. citizens purchasing property stateside.

- 1099 Loans: Tailored for gig workers and independent contractors.

What are Non-QM Loan Guidelines?

Non-QM loan guidelines are the specific underwriting rules and requirements established by private investors and lenders rather than government agencies. Because these aren't backed by the GSEs, private capital sets the rules.

Unlike conventional loans where you have one clear rulebook, Non-QM guidelines are issued by individual lenders, such as AD Mortgage, AmWest, CMG Financial, First Colony, Greenbox, and dozens of others. If you want to check a rule, where do you go? Traditionally, you have to log into each respective lender's broker portal, download their massive PDF manuals, or try to decode a complex, multi-tab matrix spreadsheet. Because every investor's risk appetite is unique, their guidelines are completely fragmented, making working with these loans notoriously challenging.

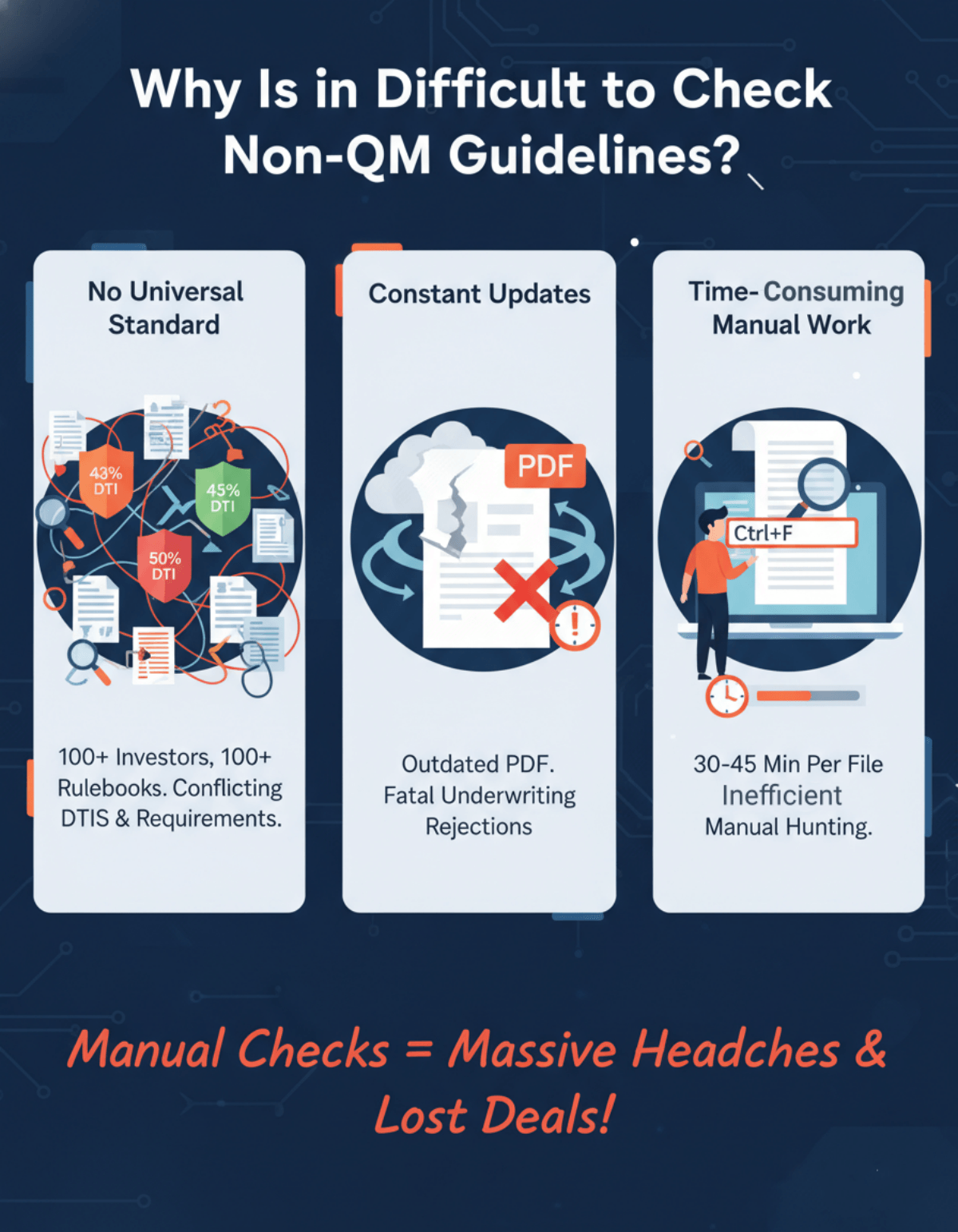

Why Is It Difficult to Check Non-QM Guidelines?

Over my career, I've lost count of how many times a seemingly solid deal was derailed at the underwriting stage because of a single overlooked requirement. Checking these guidelines manually is a massive headache. Here is why:

- No Universal Standard: If you have 100 different investors, you have 100 different sets of rules. One lender might allow a 50% DTI, while another caps it at 43% for the exact same scenario.

- Constant Updates: Private investors frequently update their matrices and risk models without much fanfare. That downloaded PDF on your desktop? It might already be outdated, leading to fatal underwriting rejections.

- Time-Consuming Manual Work: Using "Ctrl+F" to hunt through a dense, 300-page document for a niche guideline can easily waste 30 to 45 minutes per loan file. It's a completely inefficient use of your valuable time.

What are the Requirements for a Non-QM Loan?

Because there is no universal standard, it's crucial to remember that exact requirements completely depend on the specific investor and loan program you select. However, there are some general frameworks you can expect when structuring a deal:

- Credit Score Flexibility: Non-QM programs are much more forgiving. You can often qualify borrowers with scores in the low 600s or even recent credit events, but lower scores usually require a larger down payment to offset the risk.

- Income Verification: This is where Non-QM shines. Instead of tax returns and W-2s, underwriters will look at business bank statements, 1099s, or even the cash flow of an investment property (DSCR).

- Reserves & Down Payments: Because investors take on slightly more risk, they typically require larger liquid cash reserves (often 3-6 months) and slightly higher down payments, generally starting around 10% to 20%, depending on the exact scenario.

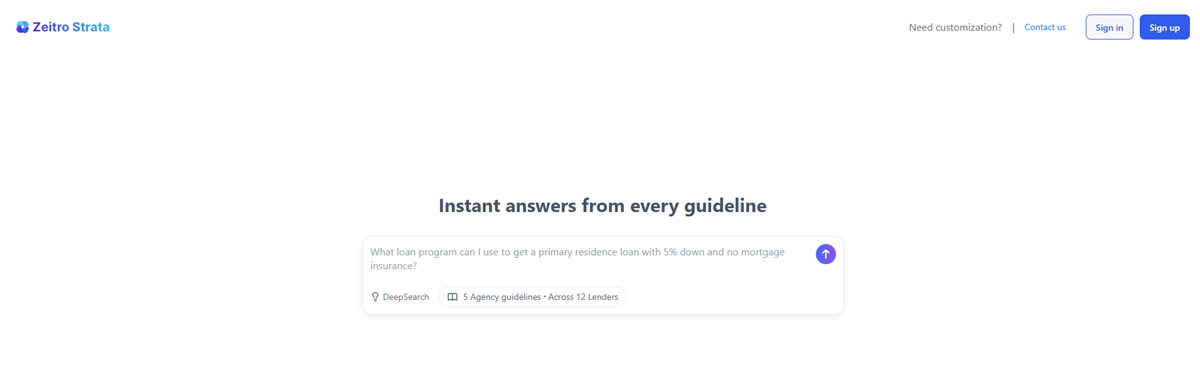

Zeitro Strata: Quickly and Accurately Check Non-QM Guidelines

The days of manual PDF hunting are over. In my practice, the ultimate weapon for boosting efficiency has been an AI tool specifically designed for mortgage professionals: Zeitro Strata. It's a powerful, AI-powered Mortgage Guideline Assistant that transforms how you check and verify complex scenarios.

Explore Features of Zeitro Strata

DeepSearch & Comprehensive Data: Zeitro Strata actively monitors and cross-checks over 300+ continuously updated guidelines from 100+ top lenders, including AD Mortgage, AmWest, Forward Lending, and Luxury. Whether you need info on DSCR, Bank Statement, or Jumbo loans, it's all in one place.

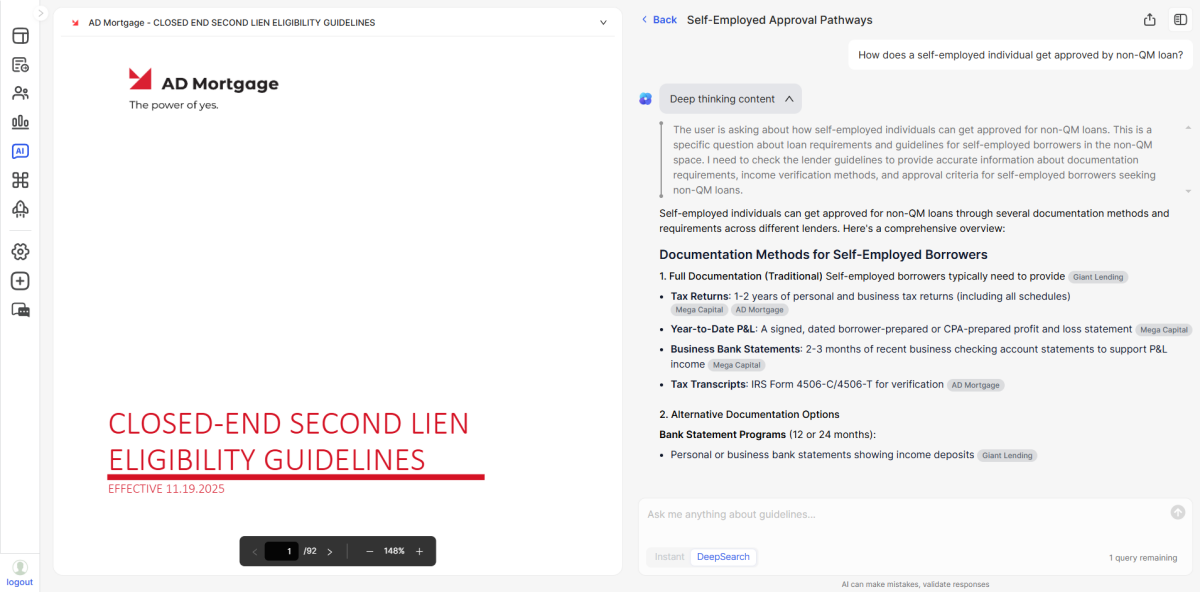

- 100% Accuracy with Citations: The AI doesn't just guess. It provides exact source citations. You can trace every answer back to the actual guideline, giving you absolute confidence when quoting terms to your borrowers.

- Massive Time Savings: It cuts manual lookup time from 30 minutes down to seconds. My team saves roughly 7+ hours per loan file, allowing us to deliver pre-qualifications 2.5x faster and close up to 30% more loans.

- Flexible Scenarios & Multi-language: You can ask vague questions like "What is eligibility for..." or input highly specific borrower scenarios. Plus, it supports both English and Chinese queries seamlessly.

How to Use Zeitro Strata?

Step 1: Use customizable tags to instantly narrow your search parameters to specific loan types (like ITIN or DSCR) or specific lenders.

Step 2: Type in your exact borrower scenario.

Step 3: Within seconds, you get an accurate, professional answer backed by a citation link. If a nuance is tricky, just hit the "Explain" button to have the AI break it down further. You can even share the link directly with your team via email.

FAQs About Non-QM Underwriting Guidelines

Q1. What are the loan limits for non-QM loans?

Unlike conforming loans, which cap out at $832,750 (or $1,249,125 in high-cost areas for 2026), Non-QM limits are significantly higher. Many private investors offer Jumbo Non-QM products allowing loan limits up to $3 million, $5 million, or even more, depending strongly on LTV and credit score.

Q2. Can a non-QM loan be conforming?

No, a Non-QM loan cannot be conforming. By definition, conforming loans must adhere to the strict standards set by Fannie Mae and Freddie Mac. Non-QM loans exist specifically for borrowers whose financial profiles fall completely outside of these traditional agency guidelines.

Q3. Is a non-QM loan risky?

While they carry slightly more risk for the lender, they are not the "subprime" loans of the past. Non-QM loans are still strictly governed by Ability-to-Repay (ATR) rules. They simply use alternative, logical methods to verify a strong borrower's cash flow and financial health.

Q4. How long does it take to close a non-QM loan?

Traditionally, the manual back-and-forth could drag the process out to 30-45 days. However, by using AI-driven verification tools like Zeitro Strata to handle pre-qualifications and guideline checks accurately upfront, you can easily accelerate closing times by up to 20%.

Q5. Is a non-QM loan a hard money loan?

No. Hard money loans are short-term, asset-based loans typically used by real estate flippers. In contrast, Non-QM loans are designed as long-term residential mortgages that still evaluate the borrower's long-term capacity to repay the debt, just using non-traditional documentation.

Conclusion

Non-QM loans represent a massive growth opportunity for brokers and loan officers, especially as the gig economy expands and more borrowers seek alternative financing. However, the sheer complexity of investor guidelines has traditionally been the biggest roadblock to scaling your business. As we move through the current market, relying on outdated PDFs and manual document searches is no longer just inefficient. It's costing you deals.

It's time to stop wasting your day digging through manuals and start focusing on what really matters: building relationships and closing loans. If you want to deliver pre-qualifications 2.5x faster and drastically reduce human error, you need the right tech stack. I highly recommend heading over to Zeitro.com to try out Zeitro Strata. With their freemium model offering 3 free queries a day, you can instantly experience how AI transforms the way you verify guidelines!

People Also Read

- Mortgage Guidelines: What Are They? How to Verify?

- Best Mortgage Underwriter Software: AI & Guideline Verification

- Best AI Mortgage Underwriting Software for Loan Professionals

- How to Determine Mortgage Eligibility? Verify Guidelines in Seconds

- AI Mortgage Underwriting Explained: Will You Be Replaced?

![[Solved] How to Calculate Commission Income for Mortgage?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a3ce1b02009d0aba39b3174_how-to-calculate-commission-income-banner.png)