Written by

Eric

Share this article

.svg)

Subscribe to updates

Last checked and updated on July, 2026

I've been in this industry long enough to remember when "technology upgrade" meant switching from a fax machine to email. 2026 feels different. Guidelines keep getting more layered, especially anything touching Non-QM or DSCR files, and borrowers expect an answer in hours, not days. If you're still cross-checking overlays by hand at midnight, the problem isn't your work ethic. It's your stack.

I spent the last few months putting the major AI mortgage underwriting platforms through their paces on real files, not demo scripts. Here's what actually held up, what I'd recommend for which type of shop, and where the market is heading next.

The Benefits of Using AI Mortgage Underwriting

The old, manual way of processing loans is quietly becoming a competitive disadvantage. The Mortgage Bankers Association's most recent production cost data puts independent mortgage banks at roughly $11,000 to $12,200 per loan to originate, and depositories even higher, north of $16,000. Most of that gap traces back to labor-heavy, manual steps that software already knows how to remove.

What surprised me most wasn't the speed gain, though that's real. It was how much calmer the process felt once an AI agent took over data entry and guideline cross-referencing. I could actually focus on the parts of the job I like: talking to clients and getting deals to the finish line. A few reasons I now consider AI non-negotiable in a modern underwriting software stack:

- Speed that compounds: turning an application into a solid pre-qualification often takes minutes instead of days.

- Fewer missed line items: AI doesn't get tired at 11 PM, which matters when you're recalculating DTI off a messy bank statement.

- Guideline access on demand: you get answers on Fannie, Freddie, or niche Non-QM overlays without waiting on a help desk that closes at 5 PM.

- Less burnout: the repetitive, low-judgment work gets absorbed by the machine, leaving you the higher-value strategy calls.

- A cleaner audit trail: every decision leaves a digital record, which makes SOC 2 reviews and compliance audits far less painful.

What to Look for in AI Mortgage Underwriting Software

Not every "AI-powered" tool is solving the same problem, so it helps to know which category you actually need before you start demoing vendors. In my experience, the strongest platforms tend to check most of these boxes:

- Explainability. You should be able to see exactly why a file was flagged or approved, not just get a score. Regulators care about this as much as you do (more on that below).

- Guideline coverage. Does it handle QM only, or can it actually parse Non-QM, DSCR, and bank statement overlays too?

- Integration depth. A tool that doesn't talk to your LOS or POS just becomes another tab you have to babysit.

- Document intelligence. Can it read messy, scanned bank statements and pay stubs accurately, or does it choke on anything that isn't a clean PDF?

- Compliance and audit trail. Look for SOC 2 Type II certification at minimum, plus a record of how every automated decision was reached.

- Pricing that fits your volume. Enterprise-grade decisioning engines are often overkill, and overpriced, for a two-person brokerage.

6 Top-Rated AI Mortgage Underwriting Software

Your best fit really depends on your volume and the loan types you handle most. Here's how the leading platforms stack up right now.

#1. Zeitro - Best for SMBs and Independent Mortgage Professionals

Zeitro has become my go-to recommendation for independent brokers and smaller teams who want enterprise-grade power without an enterprise-grade price tag. Founded by former Google and Apple engineers, it's built as a full AI mortgage agent rather than just a document reader. The Zeitro Strata AI tool lets you ask detailed questions about QM and Non-QM guidelines and get sourced, traceable answers back, which is the closest thing I've found to having a senior underwriter on call around the clock. Better yet, it's now upgraded to come with more features like automatic income calculation, AMI lookup, DPA program search, etc.

Pros:

- Saves roughly 7+ hours per loan file by automating guideline research.

- Lender-neutral, so the guidance you get isn't steering you toward a specific investor.

- All-in-one POS with a digital 1003, credit pulls, and an AI-driven DTI calculator built in.

- GrowthHub gives you a branded site to capture leads and display live rates.

- Income calculation accuracy above 85%, well ahead of manual entry.

- Upload income documents to automatically calculate qualifying income.

- Look for AMI and down payment program in your area.

Cons:

- Built primarily around the U.S. market.

- Some features may go unused by a very low-volume, single-loan-officer shop.

- The pricing engine's deeper customization takes a bit of setup time upfront.

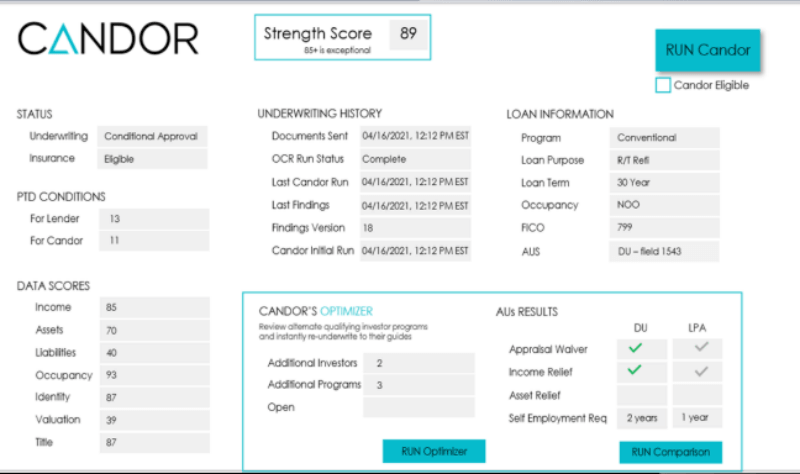

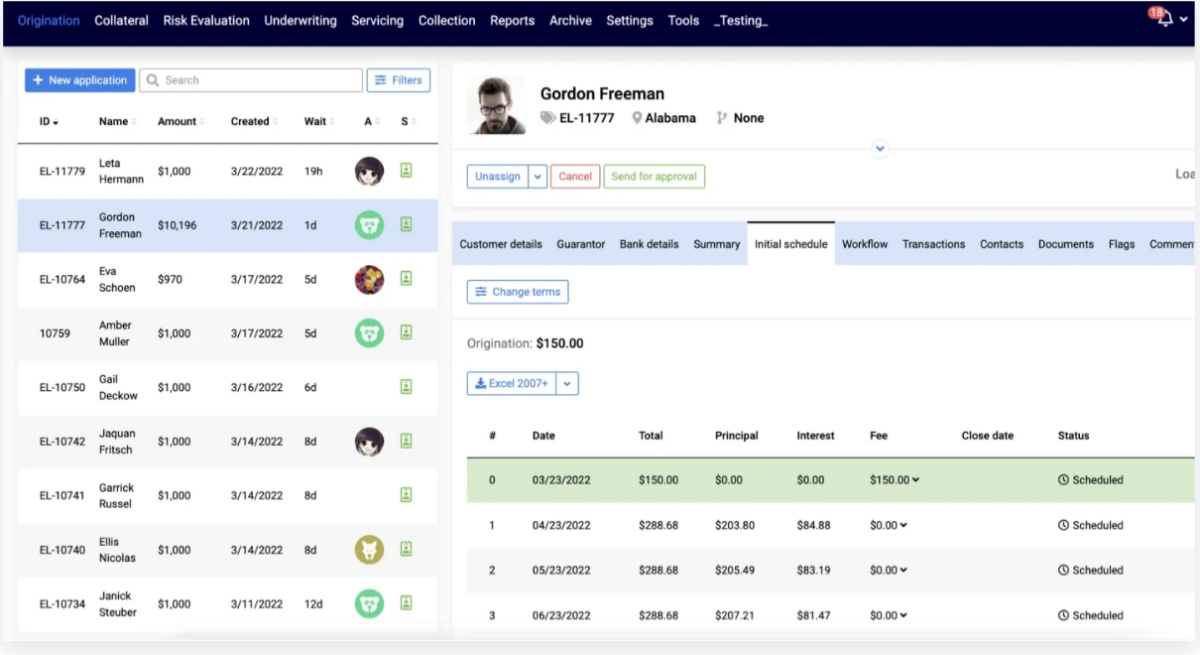

#2. Candor - Best for Automated Decision Certainty

Candor works less like a document scanner and more like a reasoning engine. Its patented "Expert System" mimics the same cognitive steps a mortgage underwriter would take, which makes it a strong fit for mid-sized lenders trying to automate their path to clear-to-close.

Pros:

- Dynamic "Conditions" management that updates in real-time.

- Reduces the need for multiple touches on a single file.

- Very strong at handling conventional, government, and jumbo loans.

Cons:

- The implementation process can be a bit heavy for very small shops.

- Less focus on the front-end borrower experience compared to Zeitro.

- Pricing is geared toward higher-volume institutions.

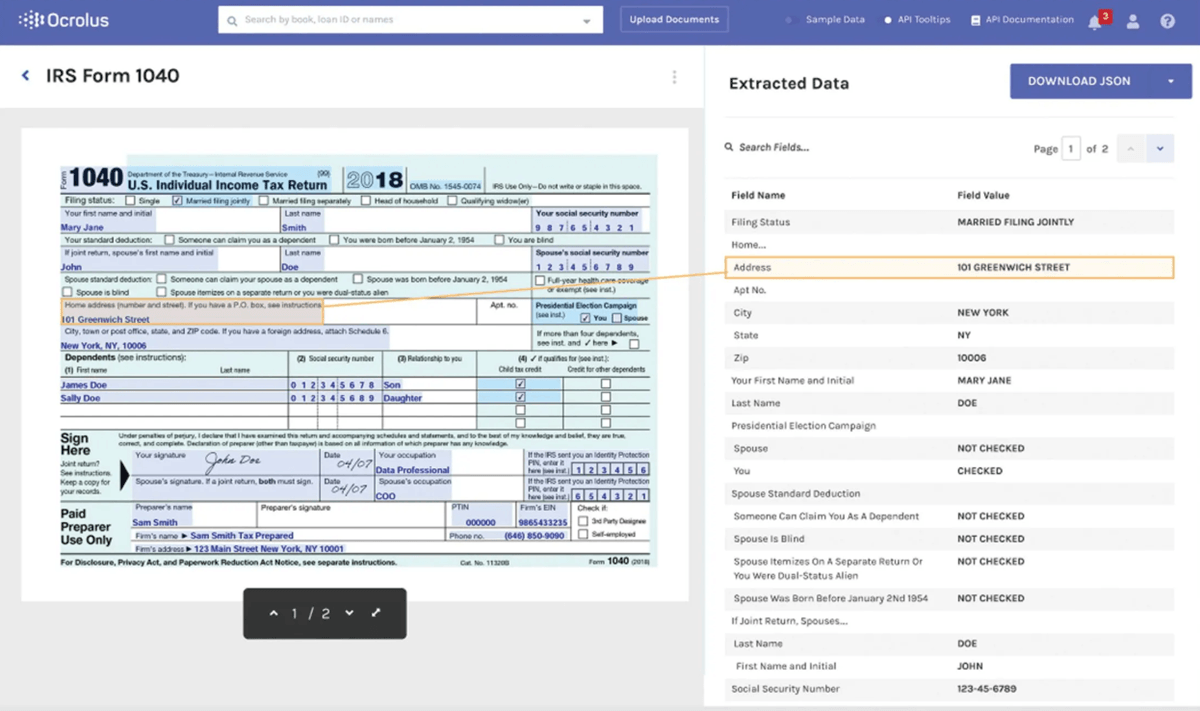

#3. Ocrolus - Best for Document Automation & Income Verification

When the real bottleneck is messy paperwork, Ocrolus is still the standard I'd point people toward. It turns unstructured input, scanned bank statements, pay stubs, tax transcripts, into clean, verified data. It's also worth knowing that 2026 has brought a sharp rise in AI-generated fraud attempts, including doctored bank statements and synthetic income documentation, so a platform built specifically to catch document tampering carries more weight than it used to.

Pros:

- Best-in-class OCR accuracy on scanned and low-quality documents.

- Strong fraud detection tuned to catch altered or synthetic bank statements.

- Integrates with nearly every major LOS on the market.

Cons:

- Focused on data extraction and conditioning rather than a full underwriting decision engine.

- Works best paired with a separate tool for complete guideline checks.

- Per-document pricing can add up fast on paper-heavy files.

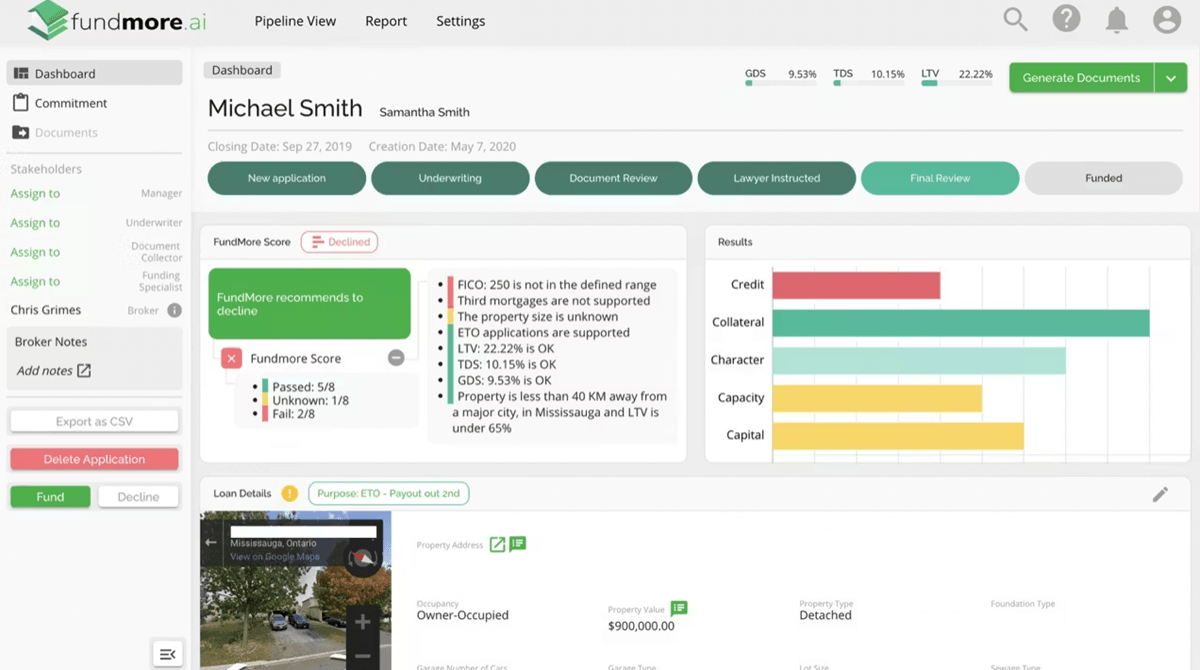

#4. Fundmore AI - Best for Cloud-Native Workflow Optimization

Fundmore is built for teams that want a clean interface and automated task tracking more than deep guideline research. It's a solid pick if your priority is making sure nothing slips through the cracks during the loan lifecycle.

Pros:

- Intuitive interface with a short learning curve.

- Automated checklists that keep borrowers and processors on the same page.

- Good API connectivity for teams with in-house developers.

Cons:

- Guideline research isn't as deep as Zeitro Strata AI.

- Works best layered on top of an existing, solid LOS.

- Reporting could be more robust.

#5. Turnkey-Lender - Best for Multi-Product Lenders

If your shop handles more than mortgages, think personal loans or commercial credit alongside residential, Turnkey-Lender offers an end-to-end platform that uses AI for credit scoring and risk management across product lines.

Pros:

- Manages multiple credit product types on a single platform.

- Proprietary AI scoring models with real depth.

- Automates the full path from origination through collections.

Cons:

- Can feel like overkill if you only originate residential mortgages.

- Higher cost of entry for smaller businesses.

- More complex interface given how many features it packs in.

#6. Friday Harbor - Best for High-Volume Operation Efficiency

Friday Harbor is built for large-scale operations looking to squeeze efficiency out of an already high-volume pipeline, finding bottlenecks that are easy for humans to miss at scale.

Pros:

- Strong at surfacing bottlenecks across large underwriting teams.

- Helps standardize decisions across hundreds of underwriters.

- Meaningful reduction in cost per loan for enterprise operations.

Cons:

- Not built with the individual broker or small team in mind.

- Longer sales cycle and setup time than plug-and-play tools.

- Limited depth on Non-QM or niche loan products.

A Note on Enterprise-Scale Alternatives

If you're evaluating this at the enterprise or bank level, it's worth knowing that legacy LOS providers are moving fast here too. ICE Mortgage Technology, for example, has rolled out generative AI tools for guideline questions and automated conditioning, plus AI voice and chat agents on the servicing side. These platforms make sense if you're already deep in that ecosystem, but for independent brokers and smaller IMBs, they tend to bring more complexity, and cost, than you actually need.

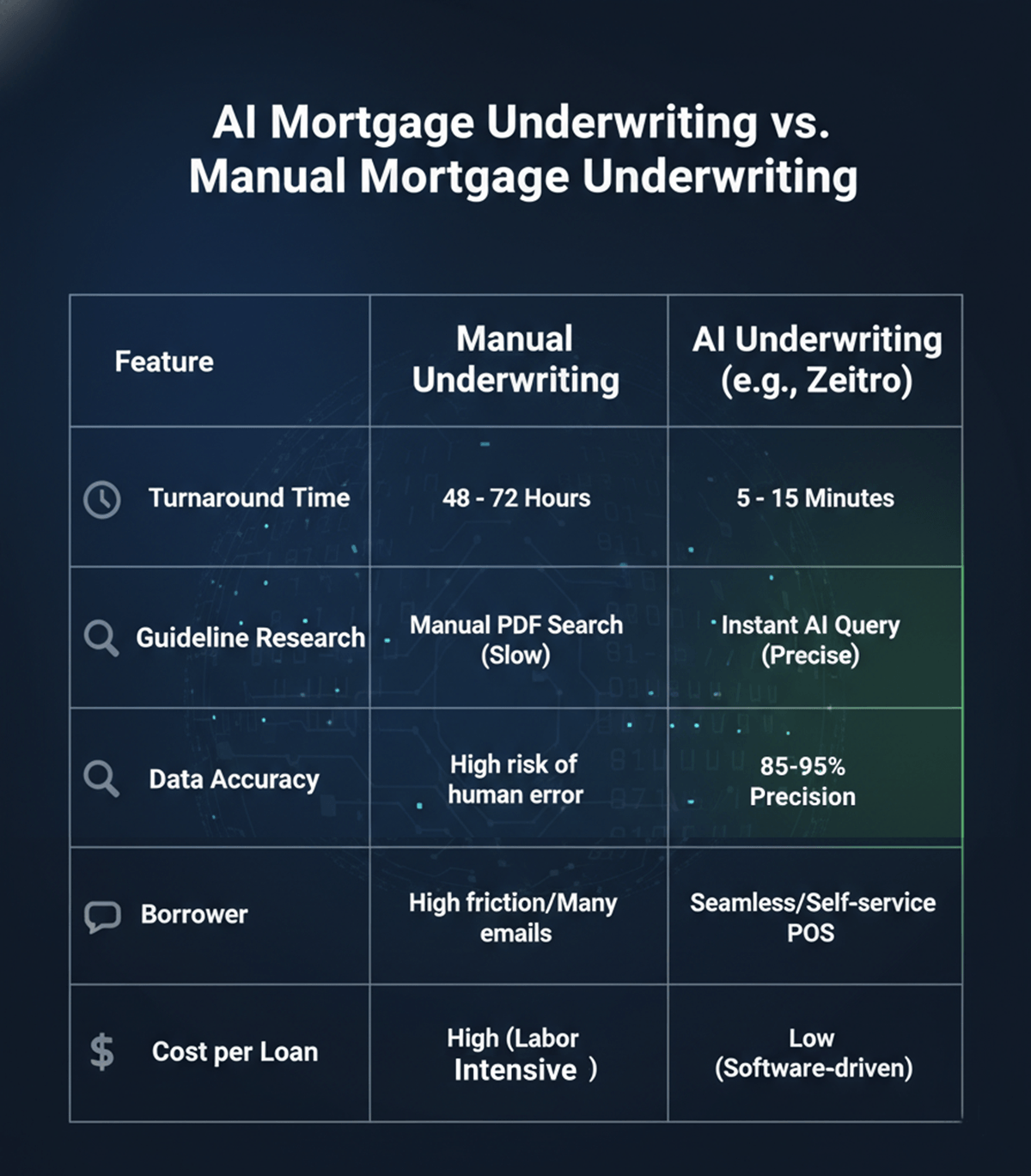

AI Mortgage Underwriting vs. Manual Mortgage Underwriting

Comparing manual mortgage underwriting to an AI-driven process in 2026 feels a bit like comparing a paper map to GPS. Manual work still has a place for judgment calls, but it's slow, and fatigue is a real factor when someone's reviewing their fortieth file of the week.

AI hasn't replaced my judgment. It just hands me better data to use it on. Speed, accuracy, and availability all shift heavily in AI's favor, while manual review still holds a slight edge on handling truly unusual, one-off borrower situations that don't fit any pattern. In practice, most experienced brokers I know use AI to handle the first 90% of the file and save their own judgment for the exceptions.

Compliance and Fair Lending: What to Know Before You Automate

This part gets skipped in a lot of "best AI tools" roundups, and it shouldn't be. Under ECOA and Regulation B, lenders are required to give applicants specific, accurate reasons for any adverse credit action, and that requirement doesn't go away just because a machine-learning model made the call. A vendor cannot ship you a black box and let you off the hook for explaining a denial.

Practically, that means you want a platform that shows its work: which factors drove a decision, and how those map to a reason a consumer can actually understand. It's also worth asking any AI underwriting vendor directly how their model documentation and fair lending testing process work, not just how fast it processes files. The tools that lead on explainability today are the ones that will save you the most trouble in an exam.

Choosing the Right Platform by Business Type

There's no single "best" answer here, it depends on where you sit:

- Independent brokers and small IMBs: Zeitro's combination of guideline research, POS, and lender-neutral pricing tends to offer the best value for the size.

- Mid-sized lenders focused on decisioning: Candor's expert system approach is built for exactly this.

- Teams drowning in paperwork: Ocrolus solves the document and fraud-detection bottleneck specifically.

- Multi-product lenders: Turnkey-Lender's breadth across credit types is hard to match.

- Enterprise and high-volume shops: Friday Harbor or an existing LOS-integrated solution like ICE Mortgage Technology will scale better than a broker-focused tool.

FAQs About AI Mortgage Underwriting

Q1. Is my borrower's data safe with AI?

Yes, provided you use enterprise-grade tools. Leading platforms like Zeitro are SOC 2 Type II certified, meaning they meet the highest security standards for data protection and privacy.

Q2. Will AI replace human loan officers?

I don't think so. Borrowers still want a human to guide them through the biggest purchase of their lives. AI just removes the boring, technical work so we can spend more time being advisors.

Q3. Can AI handle complex Non-QM or DSCR loans?

Absolutely. In fact, that's where tools like Zeitro Strata AI shine. They can parse through thousands of pages of niche lender overlays much faster than any human.

Q4. How much time does AI actually save?

On average, most professionals report saving 7 to 10 hours per loan file. That's an extra day of work every week you get back.

Q5. How hard is it to switch to an AI system?

Modern "AI-Native" tools are designed to be "plug-and-play." You can often start running guideline queries or pricing loans the same day you sign up.

Q6. What does AI mortgage underwriting software typically cost?

Pricing varies a lot by category. Broker-focused platforms like Zeitro often include a free tier plus affordable paid plans built for individuals and small teams, while enterprise decisioning engines and multi-product platforms are typically priced around volume and can run into the tens of thousands annually.

Q7. Can AI tools pre-qualify a borrower before full underwriting?

Yes, most of the platforms above can move an application to a solid pre-qualification in minutes by cross-referencing income, credit, and guideline data upfront, though a full underwriting decision still requires the complete file.

Q8. Are there AI tools built specifically for mortgage compliance and fair lending review?

Some platforms are starting to bundle explainability and audit-trail features directly into the underwriting workflow, but as of 2026, this is still an emerging category rather than a fully mature one. When comparing tools, ask vendors directly how they document model decisions for fair lending purposes.

Conclusion

If you want to stay competitive in 2026, the AI partner you choose needs to actually fit your business model, not just check a features list. After testing the field, here's where I'd land:

- Individual broker or SMB: Zeitro is the clear pick. It's versatile, handles Non-QM well, and that 7-hour time savings per loan adds up fast.

- High-volume document cleanup: Ocrolus remains the strongest option for taming the paperwork.

- Enterprise-level decisioning: Candor or Friday Harbor offer the depth larger teams need.

My honest advice: start small. Run your next complex pre-approval through one of these tools and see how much faster you get to "yes." Your clients, and your sleep schedule, will notice the difference.

People Also Read

- [Solved] How Long Does Mortgage Underwriting Take?

- How to Determine Mortgage Eligibility? Verify Guidelines in Seconds

- Best Mortgage CRM for Brokers, Lenders, MLOs

- Best Mortgage Companies for New Loan Officers