Written by

Eric

Share this article

.svg)

Subscribe to updates

If you're a loan officer or broker in today's market, you know the "guideline grind" all too well. We've moved into an era where Non-QM and niche products aren't just options. They are essential for survival. Non-QM securitizations surged significantly in 2025, with Q3 issuance hitting a record $20.9 billion, nearly double Q3 2024, according to industry reports. We are dealing with more complex scenarios than ever.

I've spent countless hours scrolling through 500-page PDFs just to find one overlay. It's a bottleneck that kills momentum. In this guide, I'll show you how we've finally moved past manual research to verify mortgage eligibility in seconds using AI-driven precision.

Why Do You Need to Determine Mortgage Eligibility?

In my experience, speed to lead is only half the battle. Speed to answer is what actually closes deals. Determining eligibility early isn't just about compliance. It's about protecting your most valuable asset: time. With average industry profits per loan fluctuating around $600–$1,200 in 2025, we can't afford to waste "green time" on files that will eventually be rejected by underwriting.

Accurate eligibility checks help us:

- Build Instant Authority: When I can tell a self-employed borrower exactly why they qualify for a Bank Statement loan during the first call, I win their trust immediately.

- Reduce Fallout: Misinterpreting a DSCR or ITIN guideline leads to dead files and frustrated Realtors.

- Maximize Throughput: Top producers aren't smarter. They are more efficient. By filtering out non-starters in seconds, you focus only on high-probability closings.

Also Read:

- Best AI Mortgage Underwriting Software for Loan Professionals

- Max DTI for Mortgage: Requirements By Loan Types

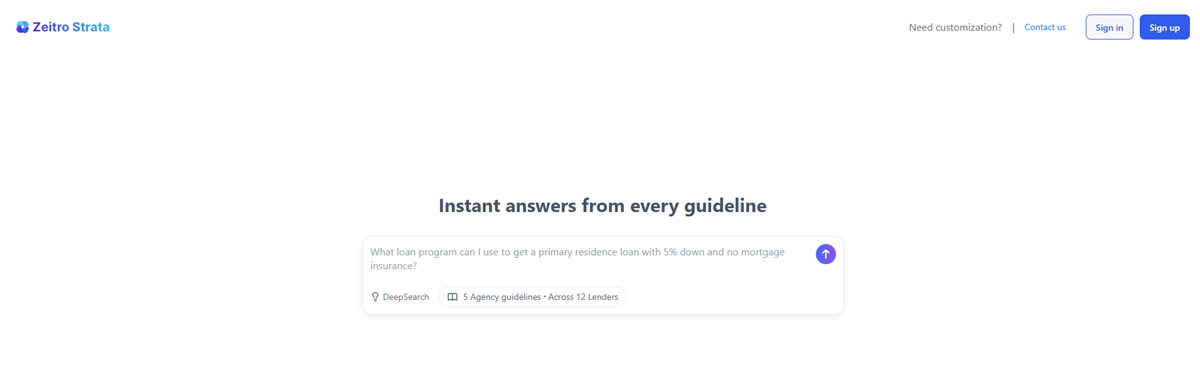

How to Determine Mortgage Eligibility Using Zeitro Strata?

When I first encountered Zeitro Strata, I realized the game had changed. It's an AI-native assistant designed specifically for our industry's complexity. It doesn't just "guess". It cross-checks over 300 guidelines from 100+ top investors like AAA Lending, Freedom Mortgage, and HomeXpress.

Here is exactly how I use it to get answers in real-time:

- Define Your Scope: I start by selecting the specific guidelines or investors I want to search. If I'm working on a tricky Non-QM case, I'll tag "Asset Utilization" or "Foreign National" to narrow the field.

- Ask Your Scenario: I type in specific questions just like I'm talking to an AE. For example: "What is the max LTV for a 680 FICO borrower using 12-month bank statements for a primary residence?"

- Review Cited Answers: Within seconds, Zeitro provides a precise answer. The best part? It includes Citations. I can click the source to see the exact paragraph in the lender's manual, ensuring I'm 100% compliant.

- Deep Dive with "Explain": If a guideline is particularly dense, I use the "Explain" feature. It re-analyzes the source to break down the logic, which is a lifesaver for complex vesting or income-layering questions.

What Else Can Zeitro Do for You?

Beyond just verifying guidelines, I've found that the Zeitro ecosystem replaces several disconnected tools I used to pay for individually. It's a full-stack solution for the modern originator.

- GrowthHub: I used this to launch a branded microsite. It's optimized for SEO, helping me capture organic leads by showcasing my expertise and live rates in a professional format.

- Digital 1003 (POS): This is a game-changer for borrower experience. It's a mobile-friendly application that calculates DTI in real-time and exports data in FNM 3.4 format, which makes my processors very happy.

- Pricing Engine: I can pull accurate quotes for both QM and Non-QM products in seconds. Being able to apply custom overlays directly in the engine means the quote I give is the quote they get.

FAQs About Determining Mortgage Eligibility

Q1. How accurate is the AI when reading these guidelines?

It's highly precise because it's built on "Source Transparency." Unlike general AI, Zeitro links every answer to a specific investor's PDF, so you can verify the source yourself in one click.

Q2. Does it support complex Non-QM products?

Yes, this is where it shines. It covers DSCR, ITIN, Bank Statements, P&L only, and even Asset Utilization across 100+ investors.

Q3. How often are the guidelines updated?

The system is updated continuously. As lenders release new announcements or update their manuals, the AI indexes that data to ensure you aren't looking at "stale" info.

Q4. Can I use it for free?

Yes, Zeitro offers 3 free queries per day, which is perfect for trying out a few tough scenarios before committing to a plan.

Q5. Is the data secure for my borrowers?

Absolutely. Zeitro is SOC 2 Type II certified, meaning they meet the highest enterprise-grade security standards for protecting financial data.

Conclusion

The mortgage landscape is shifting. In 2025, the "manual" loan officer is a dying breed. We are seeing a fundamental realignment toward technology that empowers us to do more with less. By integrating Zeitro Strata into my daily workflow, I've managed to save over 7 hours per loan file and increase my closing rate by 30%.

Whether you are navigating the nuances of a Foreign National file or just trying to get a quick answer on FHA overlays, the ability to verify eligibility in seconds is a massive competitive advantage. Don't let your "green time" be swallowed by PDF research. I highly recommend visiting Zeitro today to see how these AI tools can help you close faster and build a more resilient business.