Written by

Eric

Share this article

.svg)

Subscribe to updates

I remember the days when my desk was literally buried under stacks of tax returns, bank statements, and W-2s. The pressure to clear a pipeline while maintaining 100% accuracy was, frankly, exhausting. You're constantly worried about a missed decimal point or an overlooked line of credit. That's why the mortgage industry is sprinting toward AI underwriting.

It's not just a tech trend. It's a survival mechanism for an industry prone to burnout and human error. As a mortgage underwriter, I've watched these tools evolve from simple calculators to complex decision-makers. But the question remains: is the machine coming for my job, or is it just coming to help?

What is AI Mortgage Underwriting?

AI mortgage underwriting isn't exactly new, but its current "brainpower" is a massive leap forward. We've moved far beyond the basic Automated Underwriting Systems (AUS) like Fannie Mae's Desktop Underwriter (DU), which have been industry staples since the 1990s. Today, we are talking about machine learning, systems that learn from millions of past loan outcomes to predict future risk. Since the 2020 pandemic forced a digital-first shift, adoption has skyrocketed.

According to Fannie Mae's Mortgage Lender Sentiment Survey, a growing number of lenders are now using AI to automate the "stare and compare" work. The trend is moving away from simple "yes/no" logic toward predictive modeling that can evaluate a borrower's creditworthiness in seconds, even for those with non-traditional financial backgrounds.

Also Read:

- Best AI Mortgage Underwriting Software for Loan Professionals

- Best Mortgage CRM for Brokers, Lenders, MLOs

- Best Loan Origination Software for LOs/Brokers

- Best CRM for Loan Officers: Which One Suits You Most?

- What is Mortgage Eligibility Checker? Best Tool to Verify Guidelines

- 30 Mortgage Underwriter Interview Questions to Prepare First

- What Conditions Will Underwriting Ask for? Get to Know

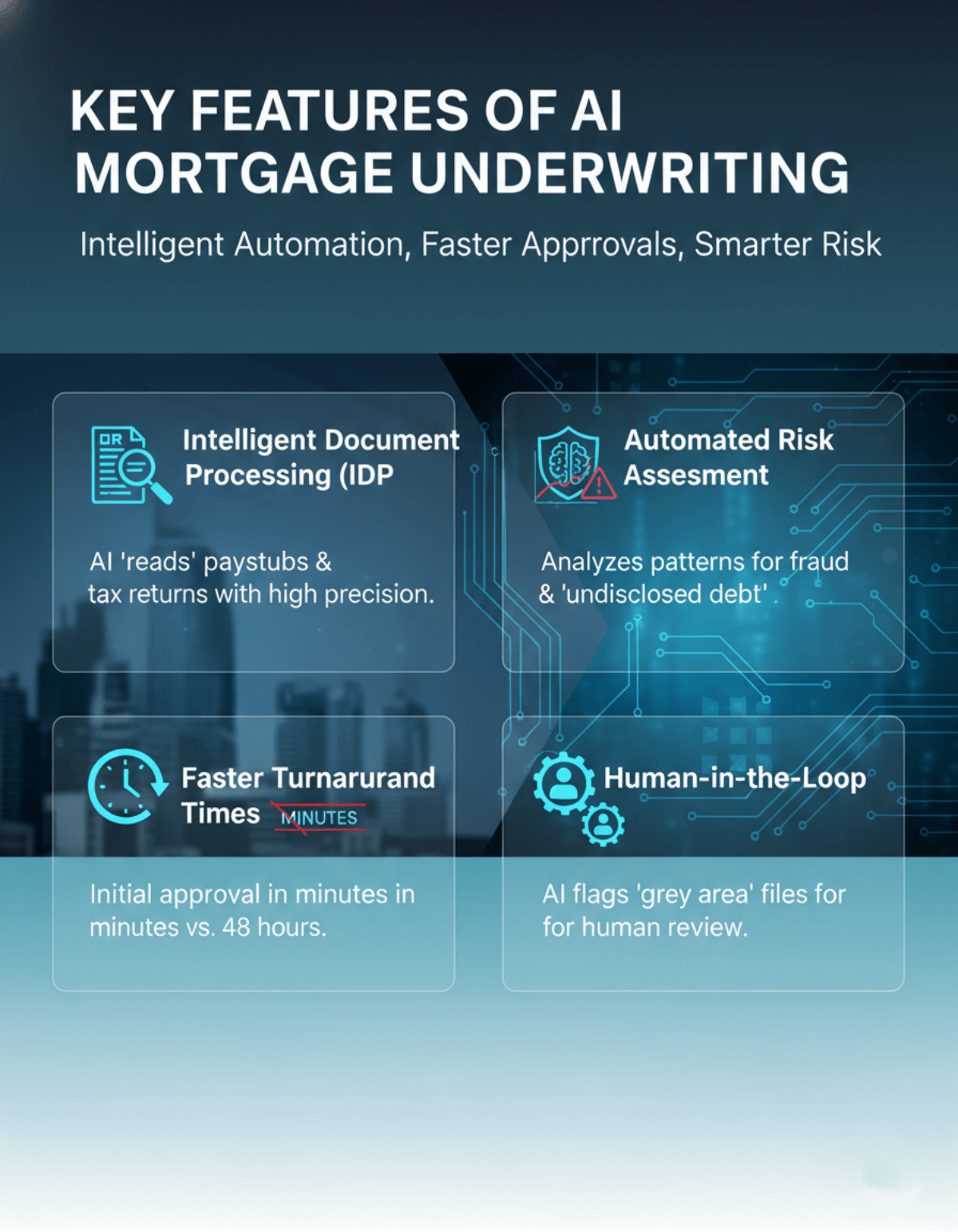

Key Features of AI Mortgage Underwriting

In my daily workflow, these tools have shifted from "optional" to "essential." Here is how AI is actually functioning behind the scenes:

- Intelligent Document Processing (IDP): This is a lifesaver. Using OCR and machine learning, the system "reads" paystubs and tax returns, extracting data with higher precision than a tired human eye.

- Automated Risk Assessment: AI analyzes patterns humans might miss, such as subtle inconsistencies in bank statements that could signal "undisclosed debt" or fraud.

- Faster Turnaround Times: While a traditional manual review might take me 48 hours to issue an initial approval, AI can do it in minutes, significantly lowering the "time-to-close."

- Human-in-the-Loop: This is the safety net. The AI flags "grey area" files, and I step in to make the final call. It handles the easy files, so I can focus on the complex ones.

Pros and Cons of AI Mortgage Underwriting

From my side of the desk, the benefits are obvious, but the drawbacks keep me cautious. On the positive side, AI eliminates "Friday afternoon fatigue", those errors that happen when you're on your tenth file of the day. It also creates a much better borrower experience. In a competitive housing market, getting an approval in hours instead of weeks is a game-changer.

However, the "black box" nature of some algorithms is a real concern. If an AI denies a loan, we must be able to explain exactly why to satisfy the Equal Credit Opportunity Act (ECOA). Furthermore, there is the risk of "algorithmic bias." If the historical data used to train the AI contains past systemic biases, the machine might unintentionally repeat those patterns. High implementation costs also mean smaller credit unions may struggle to keep up with the tech giants.

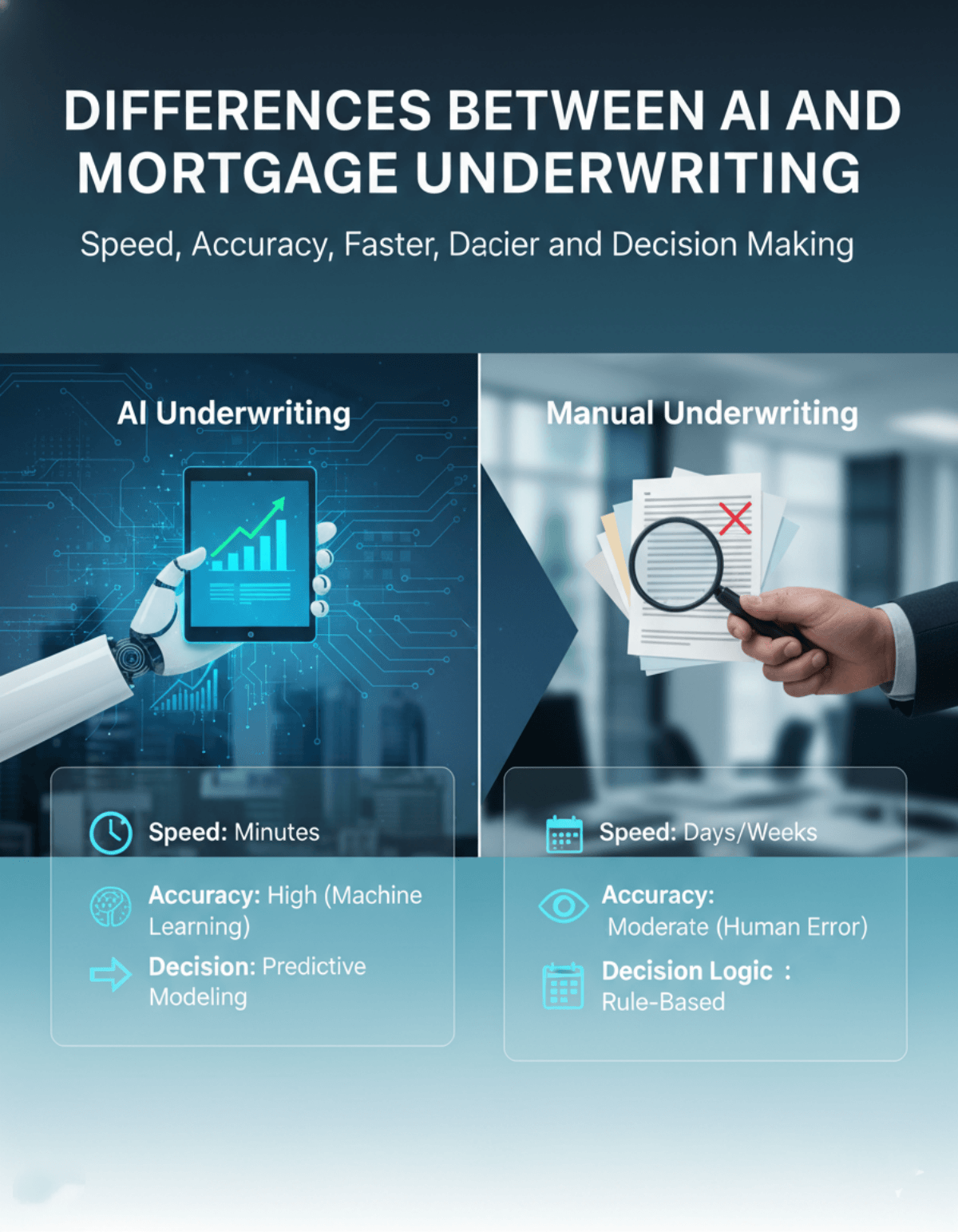

Differences Between AI and Manual Mortgage Underwriting

The real difference lies in "nuance." AI is binary. It sees data as black and white. If a borrower has a unique situation, perhaps they are a self-employed freelancer with four different income streams, the AI might get confused and issue a hard "no."

That's where manual underwriting shines. I can look at the "story" behind the numbers. Humans offer empathy and situational judgment, we can understand that a one-time medical emergency five years ago shouldn't necessarily disqualify a borrower today. Manual underwriting is a craft, while AI is a high-speed factory. We need the factory for the bulk of standard, "clean" loans, but we still need the craftsman for the complex cases that don't fit a standard mold.

The Role of Compliance and Ethics in AI Underwriting

In the U.S., we operate under strict laws like the Equal Credit Opportunity Act (ECOA). The Consumer Financial Protection Bureau (CFPB) has made it clear that lenders cannot hide behind the "algorithm" when it comes to discriminatory outcomes. Lenders remain legally responsible for their AI decisions and are required to provide specific reasons for adverse actions under fair‑lending laws.

This is why "Explainable AI" (XAI) and model interpretability are becoming so critical in our industry, as regulators increasingly demand transparency in automated credit decisions. We have to be able to pull back the curtain and prove the decision was based on creditworthiness, not protected characteristics. As an underwriter, my role is increasingly becoming one of a "Compliance Auditor" for the AI.

FAQs About AI Mortgage Underwriting

Q1: How is AI used in loan underwriting?

It's used to verify identities, calculate income from complex tax returns, assess property valuations (AVMs), and flag potential fraud by comparing data against millions of historical records.

Q2: Will AI replace mortgage underwriters?

No. It will replace the tasks of data entry and basic verification. The role is shifting from "processor" to "risk strategist." We are moving toward what some call a "bionic underwriter" model, a metaphor for the partnership where technology handles the data and humans retain the final judgment.

Q3: Does AI improve loan approval rates?

Potentially, yes. By using "trended data" (such as patterns in bank account balances and transactions over time), AI can help "thin‑file" borrowers, those with limited traditional credit histories, get approved when a human might have rejected them for lack of data. Some models also incorporate alternative data like consistent rent or utility payments to further support these borrowers.

Q4: Is AI underwriting compliant with Fair Lending laws?

Only if monitored correctly. Federal regulators like the CFPB require lenders to ensure their AI models don't result in "disparate impact" against protected classes.

Q5: How can underwriters prepare for an AI-driven future?

The best thing you can do is "up-skill." Learn how to interpret data analytics and get comfortable with platforms like Fannie Mae's DU or Freddie Mac's LPA. Your value will be in your ability to manage the technology, not compete with it.

Conclusion

After years in the trenches, I've realized that AI isn't my replacement. It's my "co-pilot." It takes away the mind-numbing task of cross-referencing bank statements so I can focus on high-level risk strategy and helping borrowers with complex needs.

The mortgage underwriter of 2030 is unlikely to be a data entry clerk. They may instead be a "digital pilot" overseeing sophisticated AI systems. If you're in this industry, don't fear the tech. Instead, learn how the algorithms work. The future of lending is faster and smarter, and there's still plenty of room for those of us who know how to navigate the human side of homebuying.