Written by

Eric

Share this article

.svg)

Subscribe to updates

Getting ready for an underwriting interview is tough. I've sat on both sides of the hiring desk, and I can tell you that managers don't just want a robot who recites guidelines. They want to see how your brain handles messy, real-world loan scenarios. I built this guide to give you a realistic look at the questions I actually ask when hiring.

Key Takeaways

- Focus on showing how you evaluate the 'Four Cs': credit, capacity, collateral, and capital.

- Be ready to pivot between automated DU/LPA systems and strict manual underwriting guidelines.

- Know your compliance rules, from TRID disclosures to the 2026 baseline conforming loan limit.

- Highlight your communication skills, especially when delivering tough, guide-backed decisions to loan officers.

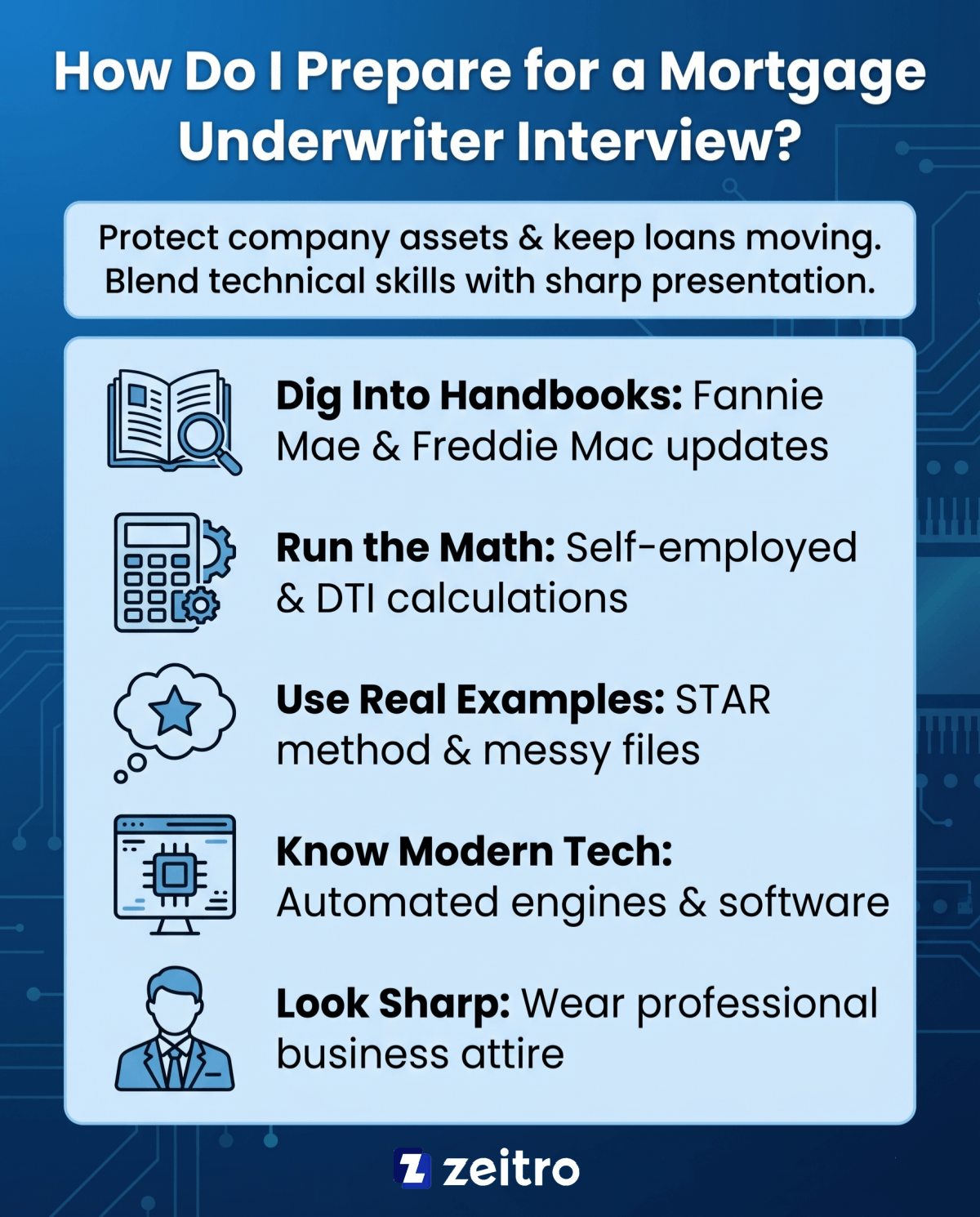

How Do I Prepare for a Mortgage Underwriter Interview?

If you want to nail your interview, you have to blend technical chops with sharp presentation. When I prep, I focus on proving I can protect the company's money while keeping loans moving. Here is my personal checklist:

- Dig Into the Handbooks: Refresh yourself on recent Fannie Mae and Freddie Mac updates.

- Run the Math: Practice tricky self-employed calculations and complex debt-to-income scenarios.

- Use Real Examples: Tell stories using the STAR method and focus on how you saved a messy file.

- Look Sharp: Wear clean, professional business attire to show you respect the role's detail-oriented nature.

- Know Modern Tech: Mention automated engines and newer guideline-lookup software.

Also Try:

- Zeitro Down Payment Assistance Search Tool

- Zeitro Mortgage Employment Income Calculator for Loan Pros

- Zeitro DSCR & Rental Income Calculator for Mortgage

- Zeitro Private Mortgage Insurance (PMI) Calculator

- Zeitro Mortgage Payment Calculator with Interest & Taxes

30 Mortgage Underwriter Interview Questions to Prepare

These are the thirty questions I use to grill candidates. I've broken them down into five logical sections so you can study them step-by-step and walk in feeling completely confident.

Mortgage Underwriting Fundamentals

Let's start with the basics. These questions test your everyday workflow, standard document knowledge, and the core rules of residential mortgage lending.

Q1. Can you explain the mortgage underwriting process from start to finish?

Strategy: Walk through the file lifecycle.

Response: "I take the file, review the credit and application, and run DU/LPA. Next, I verify assets, income, and appraisal. I then issue a conditional approval and sign off once processors clear those conditions."

Q2. How do you assess a borrower's creditworthiness?

Strategy: Look beyond the FICO score.

Response: "FICO matters, but I look at payment history, credit mix, and revolving balances. If there are late payments or derogatory marks, I demand a logical explanation to evaluate the actual risk."

Q3. What factors do you consider when evaluating a mortgage application?

Strategy: Rely on the industry's four pillars.

Response: "I rely on the 'Four Cs': Credit history, Capacity to repay through DTI, Collateral value via the appraisal, and Capital reserves to make sure they aren't left entirely broke after closing."

Q4. What are the most common red flags you look for in a loan file?

Strategy: List realistic file discrepancies.

Response: "I watch out for recent large bank deposits without paper trails, job titles that don't match the income bracket, mismatched addresses, and new credit inquiries right before closing."

Q5. What are the key differences between manual underwriting and automated underwriting?

Strategy: Highlight rules vs. human logic.

Response: "Automated systems like DU use math to approve files quickly. Manual underwriting puts the burden on me. I have to physically verify everything and follow stricter limits on DTI and reserves."

Q6. How do you determine whether a loan meets agency guidelines?

Strategy: Explain active guide checking.

Response: "I keep Fannie Mae and Freddie Mac guidelines open on my screen. I never guess. I cross-reference the loan metrics directly with current selling guides to ensure everything is perfectly compliant."

Q7. What is a Uniform Residential Loan Application (Form 1003)?

Strategy: Keep it practical and mention the update.

Response: "It is the standard form we use to capture a borrower's financial snapshot. The redesigned version was created to support more complete loan application data collection in a digital format."

Also Read:

- Mortgage Application Form 1003 (URLA): Everything You Need to Know

- Tutorial: How to Generate a 1003 Form in 3 Ways?

Q8. What is RESPA, and why is it important in mortgage lending?

Strategy: Focus on consumer protection and TRID.

Response: "RESPA prevents kickbacks and keeps closing costs transparent. Today, TRID is the integrated disclosure framework that governs Loan Estimates and Closing Disclosures within specific legal timelines."

Q9. What is the conforming loan limit, and how does it impact underwriting?

Strategy: Give the exact 2026 limit.

Response: "It is the maximum cap for agency-backed loans. For 2026, the baseline limit for a one-unit property is $832,750. Loans above that limit are generally considered non-conforming and may be jumbo loans, which requires us to use much stricter non-conforming guidelines."

Q10. How do you calculate and evaluate a borrower's debt-to-income (DTI) ratio?

Strategy: Explain the math naturally.

Response: "I divide the housing payment by gross income for the front ratio, then add monthly liabilities to get the back ratio. I check this total against agency limits to verify repayment capacity."

Also Read: [Guide] How to Calculate DTI Ratio for Mortgage?

Income & Asset Analysis

This is where the real digging begins. These questions test your ability to spot hidden debts, calculate messy self-employed returns, and source bank funds.

Also Read:

- Guide: How to Calculate Gross Income for a Mortgage?

- Mortgage Income Requirements: Learn Before You Apply

- How to Calculate Employment Income for a Mortgage?

- Income Needed for Mortgage: Methods, Examples & Requirements

Q11. How do you verify income for a self-employed borrower?

Strategy: Target business and personal tax returns.

Response: "I pull two years of personal and business tax returns, K-1s, and a current year-to-date profit and loss statement to make sure the business is stable and actually profitable."

Q12. What documents do you typically review to verify employment and income?

Strategy: State standard documents.

Response: "I require 30 days of consecutive paystubs, W-2s from the last two years, and a direct verification of employment from the HR department right before closing."

Q13. How do you analyze tax returns for self-employed applicants?

Strategy: Mention Fannie Form 1084 and adjustments.

Response: "I use Fannie Mae's Form 1084. I use Fannie Mae's Form 1084 to analyze cash flow, starting with tax return income and then adjusting for items like depreciation and other non-cash expenses."

Q14. How do you evaluate rental income when qualifying a borrower?

Strategy: Address tax schedules and vacancies.

Response: "I check Schedule E of their tax returns or look at current lease agreements. For FHA 3-4 unit properties, I typically apply the 75% rental income rule to account for vacancy."

Q15. How do you verify assets and identify large unexplained deposits?

Strategy: Focus on bank statements and paper trails.

Response: "I examine recent bank statements and ask for a clear paper trail or source documentation when deposits cannot be readily explained."

Q16. How would you handle a borrower with inconsistent income history?

Strategy: Averaging and conservative logic.

Response: "I average their earnings over two years to find a baseline. But if their income is dropping, I don't average it. I use the lower, current figure to stay safe."

Risk Assessment & Decision Making

Underwriting is rarely black and white. These questions assess how you handle the gray areas and make safe, sensible decisions on borderline files.

Q17. Describe your process for assessing overall loan risk.

Strategy: Define risk layering.

Response: "I look for risk layering, which is when a borrower has several weak points at once, like low credit and high DTI. I balance those out by finding strong compensating factors."

Q18. How do you balance risk management with business objectives?

Strategy: Focus on counter-offers.

Response: "My job isn't to say 'no'—it's to find a safe 'yes.' If a loan is risky, I work to restructure it so it meets guidelines while still helping the borrower."

Q19. Can you describe a challenging or unusual loan scenario you handled?

Strategy: Tell a quick success story.

Response: "I once had a complex borrower with multiple LLCs. By digging into their tax structures, I found enough paper depreciation to write off, qualifying them safely while staying strictly compliant."

Q20. What would you do if an applicant barely misses a qualification requirement?

Strategy: Restructure the file.

Response: "I look for high cash reserves to offset the risk. If they don't have that, I might suggest a larger down payment or adding a co-signer to improve the file."

Q21. How do you decide whether to approve, suspend, or deny a loan?

Strategy: Categorize decisions based on guidelines.

Response: "If it meets the guides, I approve it. If I need more paperwork to make a call, I suspend and list conditions. I only deny when there is no compliant path."

Q22. What compensating factors might justify approving a higher-risk borrower?

Strategy: List strong offsets.

Response: "Excellent compensating factors include substantial cash reserves, a very low loan-to-value ratio, a strong history of saving money, or a minimal jump in their monthly housing payment."

Q23. How do you evaluate a loan application that contains conflicting information?

Strategy: Verify and explain.

Response: "I stop and verify the data with independent third parties. I will also ask the borrower for a detailed explanation letter to clear up the confusion before making my final decision."

Compliance & Industry Knowledge

Regulations can change overnight. These questions evaluate your grasp of federal mortgage law and your familiarity with modern underwriting software.

Q24. How do you stay current with mortgage regulations, investor guidelines, and industry changes?

Strategy: Mention daily habits and modern tools.

Response: "I read agency bulletins weekly and take regular compliance classes. I also use modern AI search platforms like Zeitro Strata AI to look up complex guidelines in real time."

Q25. What experience do you have with FHA, VA, USDA, and Conventional loans?

Strategy: Show versatility.

Response: "I've handled conventional conforming loans, FHA guidelines, VA residual income requirements, and USDA property limits. I'm comfortable switching between these different rulebooks on the fly."

Q26. How do you ensure your underwriting decisions remain compliant with federal regulations?

Strategy: Reference specific laws.

Response: "I run every loan through strict compliance checklists to ensure we satisfy ATR/QM rules. I also apply identical standards to every borrower to stay compliant with Fair Lending laws."

Q27. What underwriting software and automated systems have you used?

Strategy: Name standard software.

Response: "I routinely use ICE Encompass alongside DU and LPA. I've also incorporated modern tools like Zeitro Strata AI to quickly verify complex self-employed income and guideline details."

Behavioral & Situational Questions

Managers want to see how you deal with people. These questions test how you handle stressful deadlines and friction with sales teams.

Q28. Tell me about a time you had to meet a tight underwriting deadline.

Strategy: Explain priority management.

Response: "When volume spiked, I triaged my queue. I cleared easy conditions first to get those files closed, which gave me quiet blocks of time to handle my complex loans."

Q29. Describe a situation where you had to communicate a difficult loan decision.

Strategy: Focus on solution-oriented teamwork.

Response: "I had to deny a deal close to settlement. I called the loan officer directly, explained the guideline constraint, and offered a counter-offer that got the deal closed safely."

Q30. What strategies do you use to maintain accuracy while managing a high volume of loan files?

Strategy: Keep it organized.

Response: "I use a strict checking routine and block my calendar for deep work. Using Zeitro Strata AI to verify guidelines saves me time, letting me focus on actual risk assessment."

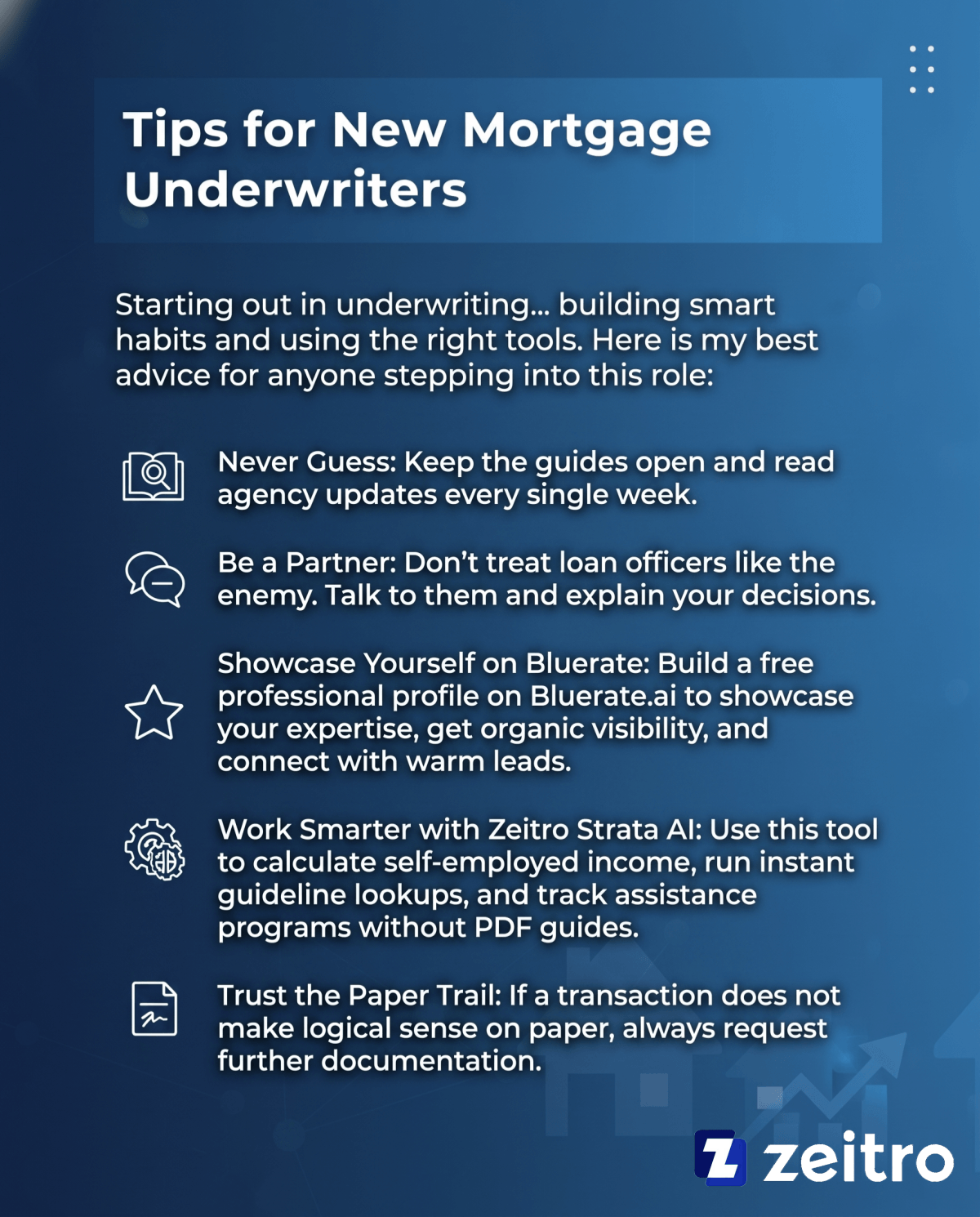

Tips for New Mortgage Underwriters

Starting out in underwriting can feel like drinking from a firehose. Over my career, I've learned that success comes down to building smart habits and using the right tools. Here is my best advice for anyone stepping into this role:

- Never Guess: Keep the guides open and read agency updates every single week.

- Be a Partner: Don't treat loan officers like the enemy. Talk to them and explain your decisions.

- Showcase Yourself on Bluerate: Build a free professional profile on Bluerate.ai to showcase your expertise, get organic visibility, and connect with warm leads if you do contract work.

- Work Smarter with Zeitro Strata AI: Use this tool to calculate self-employed income, run instant guideline lookups, and track down down payment assistance programs without getting lost in PDF guides.

- Trust the Paper Trail: If a transaction does not make logical sense on paper, always request further documentation.

Conclusion

Nailing your underwriting interview comes down to proving you have both the technical knowledge and the analytical sanity to protect your company's investments. By studying these thirty questions and practicing how you talk about risk, you can walk into that room feeling completely ready. Remember that modern underwriting is moving fast.

Showing that you know how to leverage new software while maintaining traditional, bulletproof compliance makes you incredibly valuable to hiring managers. You've got this. Good luck with your preparation—your commitment to truly mastering this craft is going to show the moment you start speaking in that interview.