Written by

Eric

Share this article

.svg)

Subscribe to updates

"Am I making enough to actually buy this house?" As a loan officer, I hear this panic daily. Borrowers constantly stress over whether they'll qualify. Honestly, figuring out your buying power isn't a guessing game. It comes down to specific math.

Below, I'm going to break down exactly how we calculate your required salary, complete with real-world examples based on current 2026 interest rates.

Key Takeaway

- Forget the old "2.5 to 3 times your salary" rule. Today's rates require looking closer at your actual monthly debt.

- Your Debt-to-Income (DTI) ratio matters way more than just your gross paycheck.

- Traditional W-2 employees usually fit into Qualified Mortgages (QM), while self-employed folks often need Non-QM flexibility.

Mortgage Income Requirements

When I sit down with a new client to review their file, the first thing I look at is how we'll prove their ability to repay. The route we take totally depends on how you earn your living.

- QM (Qualified Mortgages): This is the standard Fannie Mae/Freddie Mac route. Underwriters want a predictable, documented paper trail. They typically target a DTI around 43% for Qualified Mortgages, but higher ratios, sometimes up to 50% or more, can be approved depending on factors like credit score, reserves, and automated underwriting results.

- Non-QM (Non-Qualified Mortgages): If you run your own business, standard tax returns might not reflect your real spending power. That's where Non-QM saves the day. We can use alternative methods, like looking at 12 months of bank deposits or even the cash flow of an investment property, using alternative documentation methods, such as bank statements or asset-based calculations, instead of relying primarily on W-2 income.

Also Read: Mortgage Income Requirements: Learn Before You Apply

How to Calculate How Much Income is Needed for a Mortgage?

You don't need a finance degree to estimate your target salary. Here is how I usually walk my clients through it:

- The Rule of Thumb: A commonly cited rule of thumb suggests your home price be about 2.5 to 3 times your annual income, though this has never been a formal lending standard. Honestly, with 2026 interest rates, this old trick is getting a bit outdated, but it's an okay starting point.

- Online Tools: Do yourself a favor and run your numbers through a good Mortgage Calculator first. It accounts for local taxes.

- AI Chat: You may consider using AI-powered tools like Zeitro Strata to estimate the income needed for a mortgage. Plus, verify income guidelines with ease.

Steps to Take:

- Calculate your Gross Income (what you make monthly before the IRS takes its cut).

- Tally up your Current Debt (just the minimum monthly payments on cars, student loans, or cards).

- Check your Ratios. Make sure your projected new house payment plus those existing debts is ≤43% of your gross pay.

Also Read:

- How to Calculate Employment Income for a Mortgage?

- How to Calculate Self-Employed Income for a Mortgage?

- Gross vs. Net Income for a Mortgage: What Lenders Use & Why

- Must-Read Tips for Paying Off Mortgage Early

Examples of Income Needed for Mortgage

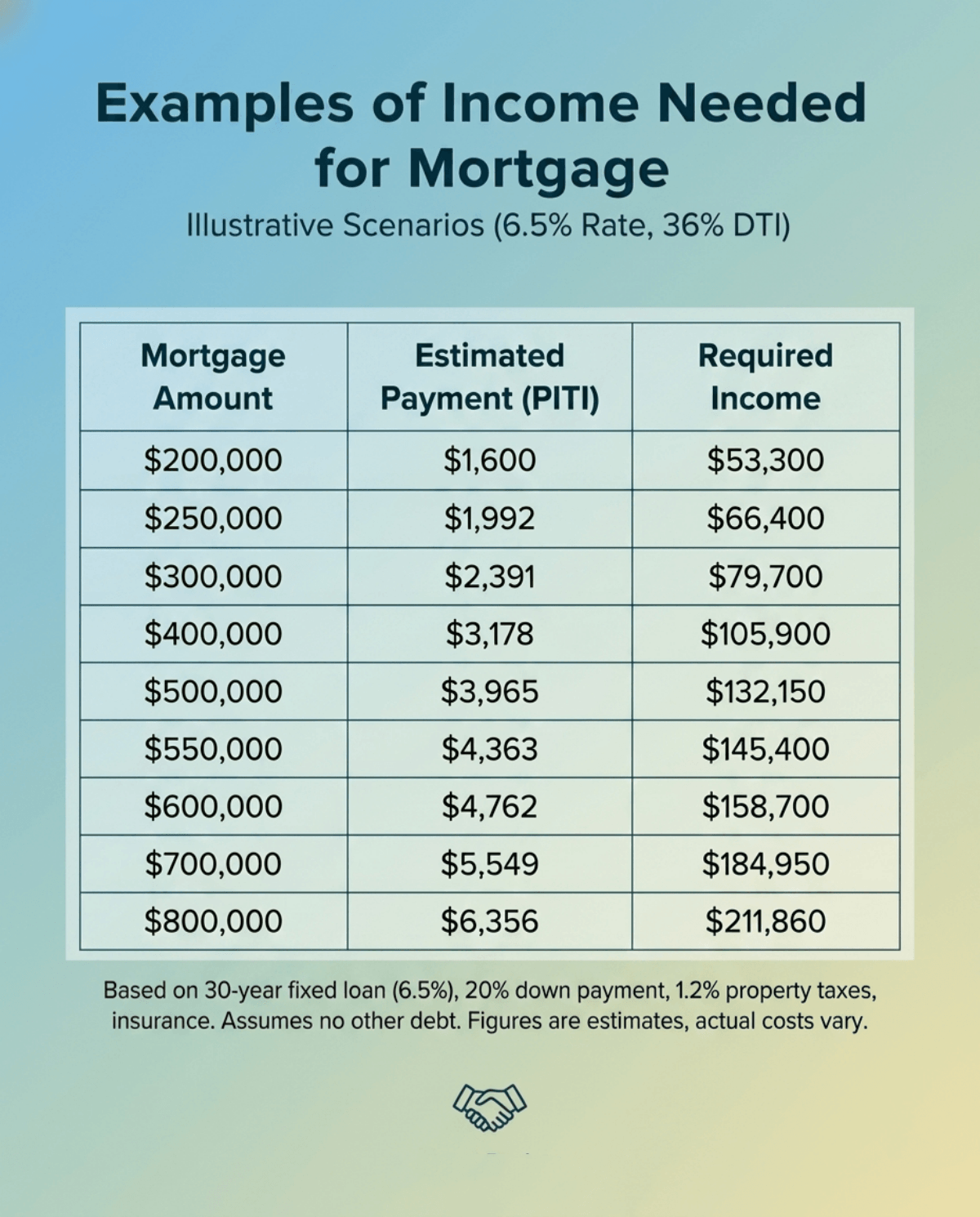

Let's look at some actual numbers. To give you a realistic baseline, I'm using an illustrative assumption of a 6.5% 30-year fixed rate for 2026, 20% down, roughly 1.2% for property taxes, plus standard insurance. Most importantly, I'm building these estimates targeting a safe 36% DTI, assuming you don't carry any other monthly debt.

These figures are rough estimates based on typical assumptions. Actual payments can vary significantly depending on location, taxes, insurance, and loan terms.

Income Needed for 200k Mortgage

To comfortably manage a $200k mortgage in today's market, you should aim for an estimated annual salary of about $53,300. It's a great entry point for many first-time buyers in affordable regions.

- Estimated Monthly Payment (PITI): $1,600

- Recommended Monthly Gross Income: $4,444

- Recommended Annual Gross Income: $53,300

Income Needed for 250k Mortgage

Taking on a $250k loan bumps up your housing costs slightly, primarily because property taxes and insurance scale with the home's value. You'll need just north of $66,000 to keep your budget balanced.

- Estimated Monthly Payment (PITI): $1,992

- Recommended Monthly Gross Income: $5,533

- Recommended Annual Gross Income: $66,400

Income Needed for 300k Mortgage

For a $300k mortgage, the financial commitment becomes more substantial. Reaching a gross household pay of nearly $80,000 ensures you won't end up house-poor while managing daily living expenses.

- Estimated Monthly Payment (PITI): $2,391

- Recommended Monthly Gross Income: $6,641

- Recommended Annual Gross Income: $79,700

Income Needed for 400k Mortgage

Crossing into the $400k territory typically requires a six-figure salary. At this level, I see many couples combining their W-2 earnings to easily meet the DTI requirements.

- Estimated Monthly Payment (PITI): $3,178

- Recommended Monthly Gross Income: $8,827

- Recommended Annual Gross Income: $105,900

Income Needed for 500k Mortgage

Securing a half-million-dollar loan means your monthly PITI approaches four grand. A stable, robust earnings history of around $132,000 is necessary to safely absorb these housing costs alongside other life expenses.

- Estimated Monthly Payment (PITI): $3,965

- Recommended Monthly Gross Income: $11,013

- Recommended Annual Gross Income: $132,150

Income Needed for 550k Mortgage

If you are eyeing a slightly more expensive property, a $550k mortgage demands around $145,400 annually. Keep in mind, this assumes you don't carry heavy auto loans or high credit card balances.

- Estimated Monthly Payment (PITI): $4,363

- Recommended Monthly Gross Income: $12,119

- Recommended Annual Gross Income: $145,400

Income Needed for 600k Mortgage

A $600k mortgage requires a household earning near $160,000. In my experience, buyers in this bracket often look at jumbo loans depending on the county, which can sometimes carry stricter reserve requirements.

- Estimated Monthly Payment (PITI): $4,762

- Recommended Monthly Gross Income: $13,227

- Recommended Annual Gross Income: $158,700

Income Needed for 700k Mortgage

Handling a $700k loan pushes your required yearly pay closer to $185,000. Because property taxes take a bigger bite here, keeping your other liabilities low is critical for approval.

- Estimated Monthly Payment (PITI): $5,549

- Recommended Monthly Gross Income: $15,413

- Recommended Annual Gross Income: $184,950

Income Needed for 800k Mortgage

To tackle an $800k mortgage, you generally need to pull in over $210,000 a year. At this significant loan size, we heavily scrutinize your overall financial portfolio to ensure long-term stability.

- Estimated Monthly Payment (PITI): $6,356

- Recommended Monthly Gross Income: $17,655

- Recommended Annual Gross Income: $211,860

Income Documents to Be Prepared

I always tell my clients: nothing stalls a closing faster than scrambling for paperwork at the last minute. Getting your file together early makes my job, and the underwriter's job, much easier.

- For standard QM loans: The checklist is pretty rigid. Gather your last 2 years of W-2s, 2 years of federal tax returns, the most recent 30 days of pay stubs, and 2 solid months of bank statements.

- For Non-QM loans: The required paperwork is completely different. Instead of W-2s, we usually ask for 12 or 24 months of bank statements to analyze your actual cash deposits. Depending on the exact program, you might also need to hand over 1099s, a signed CPA letter, or recent Profit and Loss (P&L) statements.

Factors that Affect Mortgage Income Needed

Your base salary is only one part of the equation. Several moving pieces actively change the exact amount you need to earn:

- DTI Ratio Limits: Conventional guidelines usually cap your DTI between 36% and 50%, while FHA loans often allow higher DTI ratios, sometimes above 50%, especially with strong compensating factors. Less outside debt equals lower income requirements.

- Loan Type & Rates: A higher interest rate significantly reduces buying power. At 2026's 6.5% average, your interest burden is way higher than a few years ago, forcing your required salary up.

- Down Payment & Costs: Putting down less than 20% means paying for Private Mortgage Insurance (PMI). That extra monthly fee means you need more income to qualify.

- Income Types: You aren't stuck using just base pay. Freelance cash and bonuses work too, but underwriters demand a consistent two-year history before counting it.

FAQs About Income Needed to Buy a House

Q1. What is the minimum income needed for a mortgage?

There's no absolute legal minimum. Approval depends entirely on the home's price and your debt load. In lower-cost areas, borrowers with modest incomes may still qualify for FHA or USDA loans, depending on home prices and debt levels.

Q2. Can I use bonus or overtime income to qualify for a mortgage?

Yes, but lenders won't just take your word for it. We need to see a continuous two-year track record of you receiving that extra money. The underwriter will then average that total overtime or bonus amount over 24 months to find your qualifying figure.

Q3. How does my existing debt affect the income required for a home loan?

It changes the math significantly. Since lenders care deeply about your Debt-to-Income ratio, high car payments or maxed-out credit cards destroy your borrowing power. The more outside debt you have, the higher your salary must be to cover the new mortgage safely.

Q4. Can self-employed borrowers get a mortgage if their tax returns show low income?

Absolutely. A lot of business owners write off heavy expenses, leaving a tiny net profit on paper. Using Non-QM "Bank Statement" loans, we can calculate your buying power using your actual monthly business deposits instead of relying on what the IRS sees.

Q5. Does a higher credit score lower the income needed for a mortgage?

Indirectly, yes. Having excellent credit unlocks the lowest interest rates and gets you much cheaper Private Mortgage Insurance (PMI). By lowering those monthly expenses, your overall PITI drops, which means the threshold for how much money you need to make drops right along with it.

Conclusion

At the end of the day, figuring out your required salary goes way beyond a simple multiplier. It's a balancing act between your current debt, DTI limits, and whatever the 2026 interest rate market is doing right now.

Honestly, try not to let the raw math discourage you. Whether your financial life fits perfectly into a traditional QM box, or you need the creative flexibility of a Non-QM bank statement loan, there's usually a way to make the numbers work.

Your next step shouldn't involve stressing over spreadsheets.

- Jump onto our mortgage calculator or Zeitro Strata to run your specific scenario.

- Or better yet, reach out to a professional loan officer for a free pre-approval. We'll handle the math so you can focus on house hunting.

People Also Read

- Zeitro Mortgage Affordability Calculator Free and Online

- How to Calculate PMI? Do the Math On Your Own

- Ultimate Guide: How to Calculate Monthly Mortgage Payment?

- How to Calculate Mortgage Interest: Manually & Automatically

- [Guide] How to Calculate DTI Ratio for Mortgage?

![[Solved] How to Calculate Commission Income for Mortgage?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a3ce1b02009d0aba39b3174_how-to-calculate-commission-income-banner.png)