Written by

Eric

Share this article

.svg)

Subscribe to updates

Last Checked and Updated on August, 2026

I've lost count of how many pre-approval calls start the same way. A buyer glances at their bank balance, then at the loan amount the lender just quoted, and asks some version of: "How can I qualify for this much when my paycheck is nowhere close?"

The short answer: lenders don't look at what lands in your checking account. They look at your gross income — the number before taxes, insurance, and retirement contributions come out. Loan programs treat this baseline a little differently depending on how you earn your money, but gross income is where almost every mortgage calculation starts.

Your budget, though, is a different story. Once you're living in the house, it's your net income — your actual take-home pay — that has to cover the mortgage, the groceries, and everything else. Here's how the two numbers work, and why mixing them up can set you up for a rough first year of homeownership.

Quick answer: For most home loans — Conventional, FHA, and VA — lenders qualify you using gross income, the amount you earn before taxes and deductions. You still need to budget with your net income, the amount that actually lands in your bank account.

Key Takeaways

- Lenders qualify you on gross income. It's the standard input for your debt-to-income (DTI) ratio.

- Employment type changes the math. W-2 employees, self-employed borrowers, and applicants with non-taxable income are each evaluated differently.

- Approval isn't affordability. Build your household budget around net income, not the higher number a lender hands you.

Do You Use Gross or Net Income for a Mortgage?

For standard Conventional, FHA, and VA loans, lenders qualify you on gross monthly income. Everything you earn before federal and state taxes, Social Security, Medicare, and retirement contributions are subtracted.

There's a practical reason for this. Two people earning the same salary can end up with very different take-home pay depending on their tax bracket, their 401(k) contribution rate, or whether they're covering a family on their health plan. Gross income strips all of that out, giving underwriters one consistent number to compare across every applicant.

If you've come across a finance-class question asking what your gross income is, here's the answer: it's your income before taxes and other deductions are taken out — not your take-home pay, and not income limited to a single job or paycheck. That's the figure lenders start with.

Also Read:

- Guide: How to Calculate Gross Income for a Mortgage?

- Ultimate Guide: How to Calculate Net Income for a Mortgage?

- How to Calculate Employment Income for a Mortgage?

- How to Calculate Self-Employed Income for a Mortgage?

- Income Needed for Mortgage: Methods, Examples & Requirements

- How to Verify Income for Mortgage: Detailed Guide for Loan Pros

- Income Verification Documents: A Complete Guide to Check

Core Differences: Gross vs. Net Income in Mortgage Applications

These two numbers play completely different roles in your homebuying journey. One is for the underwriter's spreadsheet, and the other is for your personal peace of mind. Here is how they compare.

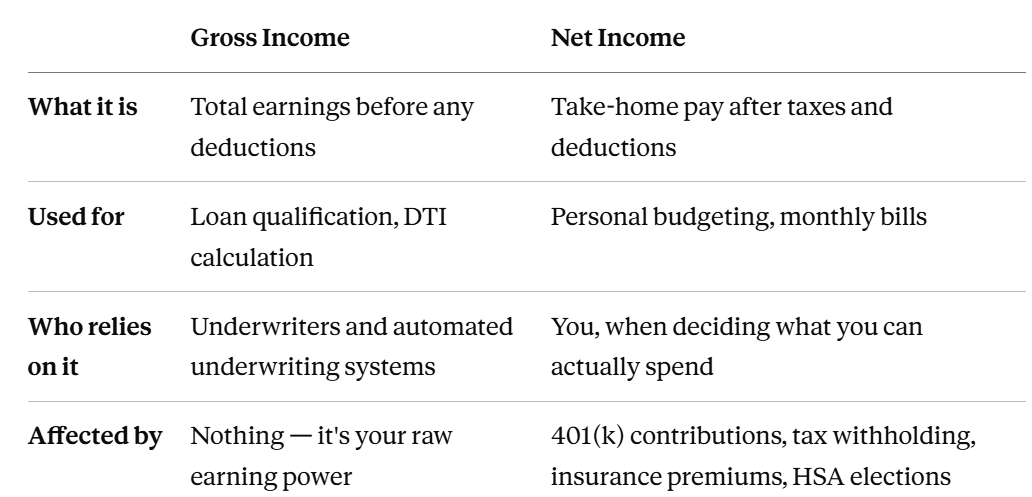

Your gross income is the figure at the very top of your pay stub, before a single dollar comes out for taxes, union dues, or health coverage. Net income is what's left after every mandatory and voluntary deduction — the number that actually shows up in your checking account. Confusing the two is one of the fastest ways to misjudge what you can really afford.

Definition

Your Gross Income is the big number at the very top of your pay stub. It represents all the money you earned during a pay period before a single dime is taken out for federal or state taxes, Social Security, Medicare, union dues, or health insurance.

On the flip side, Net Income is what we often call your "take-home pay." It is the exact amount that eventually gets deposited into your checking account after all mandatory and voluntary deductions are stripped away. Understanding this distinction is step one, because mixing them up is the easiest way to derail an application right out of the gate.

Purpose in Loan Approval

Banks rely heavily on gross income because it acts as the denominator when calculating your Debt-to-Income (DTI) ratio. Whether they are looking at your front-end DTI (just your housing costs) or your back-end DTI (your housing costs plus credit cards, student loans, and auto loans), the math always starts with your pre-tax earnings.

This is the primary metric lenders use to assess your absolute highest repayment capacity. They essentially want to know your raw earning power before your personal lifestyle choices or tax strategies shrink that number down. If you make $8,000 gross a month, that is the exact figure the automated underwriting system uses to greenlight your file.

Non-Discretionary vs. Discretionary Deductions

Have you ever wondered why lenders don't just look at what hits your bank account? It is because many paycheck deductions are entirely voluntary, or "discretionary." For example, if you aggressively contribute 15% of your paycheck to a 401(k) or overpay your taxes to get a big refund, your net income looks artificially low.

A lender knows that, if push comes to shove and you need to make your mortgage payment, you could simply pause those retirement contributions. Because you have the power to control these optional deductions, banks feel comfortable basing your loan approval on your gross earning potential.

Budgeting Reality for Borrowers

Here's what I tell every client before they get too excited about their approval letter: just because the bank uses your gross income doesn't mean you should build your life around it. This gap is exactly how buyers end up house-rich and cash-poor.

Say a lender approves you for a $4,000 monthly payment based on $10,000 in gross income. That's only a rough ceiling — actual approval also depends on your other debts, insurance, taxes, and the specific loan program. What it doesn't account for is that your real take-home pay might only be $6,500.

After that mortgage payment, you could be left with very little room for groceries, gas, or a surprise car repair. Run your own budget using net income, not the maximum number a lender hands you.

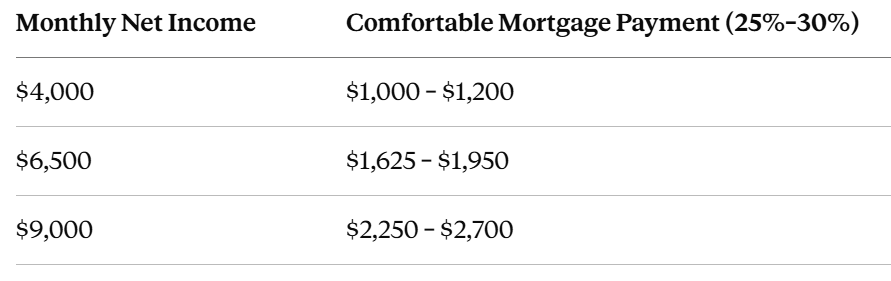

What Percentage of Your Net Income Should Go to Your Mortgage?

Lenders talk in terms of gross income, but your household budget should run on take-home pay. A common, conservative benchmark: keep your total mortgage payment — principal, interest, taxes, and insurance — at or under 25% to 30% of your net monthly income.

Say your net income is $6,500 a month. Staying inside that range puts a comfortable mortgage payment somewhere between roughly $1,625 and $1,950 — often well below what a lender's gross-income-based approval would allow.

This is a personal-finance guideline, not an underwriting rule — no lender will ever ask for your net-income percentage during the loan process. Think of it as a gut check you run for yourself, separate from whatever number appears on your pre-approval letter.

It's also worth noting this is a different measure entirely from the classic 28% rule, which is based on gross pay and used by lenders. Both are useful in their own way: one tells you what a bank might approve, the other tells you what you'll actually feel comfortable paying every month.

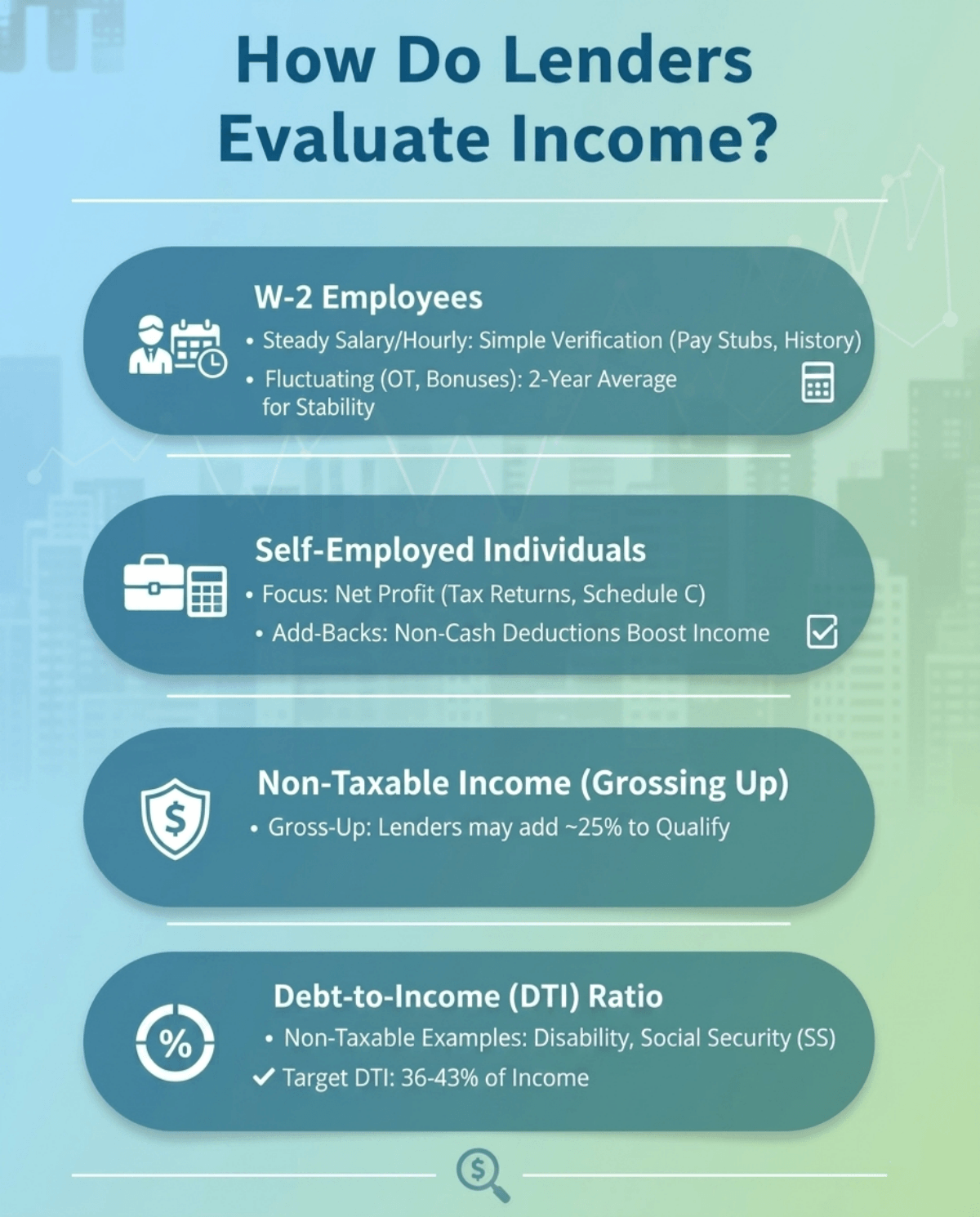

How Do Lenders Evaluate Income?

When an underwriter reviews your file, they don't just glance at a W-2 and call it a day. The way they calculate your qualifying income depends heavily on how you earn your money.

- W-2 Employees: If you earn a steady salary or hourly wage, the process is usually straightforward, but lenders still verify employment history, recent pay stubs, and other supporting documents. But if your income fluctuates with overtime, bonuses, or commissions, lenders will generally require a two-year track record. They will average out those extra earnings over 24 months to ensure stability.

- Self-Employed Individuals: This is where things flip. If you own a business, lenders actually look at your tax returns (like Schedule C) and focus on your Net Profit—your business revenue minus expenses. However, there is a silver lining. Underwriters will do "add-backs," returning non-cash deductions like depreciation to your bottom line, which artificially boosts your qualifying income.

- Non-Taxable Income (Grossing Up): If you receive tax-free money, like disability benefits or Social Security, underwriters apply a neat trick called "grossing up." For certain non-taxable income types, lenders may apply a gross-up adjustment, often 25%, depending on program rules and the income source.

- Debt-to-Income (DTI) Ratio: Once they finalize your gross figure, they use it to ensure your total monthly debts don't exceed that sweet spot of 36% to 43% of your income.

What are the Mortgage Income Requirements?

Income isn't just about the raw number. Stability and the type of mortgage you apply for matter just as much. Looking at the latest 2026 lending guidelines, here is what you need to know before you apply:

- The 2-Year Rule: WFor variable or self-employed income, underwriters often want a 24-month history of stable earnings, while salaried W-2 income may be evaluated based on current verified employment and pay history. Job hopping within the same industry is usually fine, but sudden career changes can raise red flags.

- Loan Types Matter: Your loan program dictates how strictly your income is judged. Conventional loans can allow higher DTIs in some cases, with common limits around 36% for manually underwritten loans, up to 45% for certain eligible cases, and up to 50% for DU findings. VA loans place special emphasis on residual income, while FHA loans mainly rely on DTI and other underwriting factors.

- Alternative Proof of Income: If you are self-employed and your tax returns don't reflect your true cash flow, 2026 brings great news. Some Non-QM loans can use bank statements or alternative documentation instead of traditional tax-return-based income verification, depending on the product. Instead, lenders verify your income using 12 to 24 months of personal or business bank statements.

Also Read: Mortgage Income Requirements : Learn Before You Apply

2026 Update: Does "No Tax on Tips" or "No Tax on Overtime" Change Your Qualifying Income?

If you earn tips or regularly work overtime, you've probably heard about the new federal deduction that lets eligible workers write off up to $25,000 in tips or $12,500 in overtime pay each year (roughly double for joint filers), starting with the 2025 tax year. It's a genuine tax benefit, but it doesn't touch your mortgage file.

Here's the distinction that matters: this is a deduction you claim when you file your return, not a change to how your employer reports your wages. Your W-2 still shows your full tip and overtime earnings, and that's still the number your lender uses to calculate gross income and DTI. The new tax break can put more money back in your pocket every spring, but it won't move your loan qualification math at all.

Also Read:

- How to Calculate Overtime Income for a Mortgage?

- How to Calculate Commission Income for Mortgage?

- Can I Use Child Support Income for a Mortgage?

- Can I Use Foreign Income to Qualify for a Mortgage?

FAQs About Net vs. Gross Income

Q1. Why do lenders use gross income instead of net income?

Net income varies wildly from person to person based on tax brackets, health insurance premiums, and retirement contributions. Gross income gives lenders a universal, standardized baseline to fairly compare the financial strength and borrowing capacity of every applicant.

Q2. Is the 28% rule gross or net?

The classic 28% rule is always based on your Gross Income. This financial rule of thumb suggests that your total monthly housing expenses, including principal, interest, property taxes, and home insurance, should not exceed 28% of your pre-tax monthly earnings.

Q3. Is a mortgage 33% of gross income?

Traditionally, lenders prefer your front-end DTI (housing costs alone) to sit between 28% and 33% of your gross pay. However, some loan programs, like FHA loans, may allow your housing payment to consume up to 40% of your gross income if you have great credit.

Q4. What percentage of your income should go towards your mortgage?

While a lender might approve a mortgage taking up 28% to 30% of your gross income, personal finance experts advise a safer route. For true financial wellness, try to keep your mortgage payment under 25% to 30% of your net (take-home) pay.

Q5. Do mortgage lenders use gross or net income for self-employed?

For traditional conventional or FHA loans, lenders look at your business's Net Profit on your tax returns, plus allowable "add-backs" like depreciation. However, if you use a Non-QM bank statement loan, the lender may qualify you based on your gross business deposits.

Q6. Is gross income calculated differently from lender to lender?

No — it's the same starting point everywhere. Conventional, FHA, VA, and USDA loans all qualify borrowers using gross income, so that's not a place where one lender will "beat" another. What actually varies between lenders is the DTI ceiling they'll accept and which loan programs they offer, and that's worth comparing.

Q7. What does a "pre-tax mortgage payment" mean?

This phrase confuses a lot of people. Your mortgage payment itself is paid with after-tax dollars, just like any other bill — there's no such thing as a truly pre-tax mortgage payment. What people usually mean is that lenders measure your ability to pay using pre-tax, gross income, even though the money leaving your account each month is after-tax.

Conclusion

Navigating the mortgage approval process can feel overwhelming, but understanding how banks view your money is half the battle. Remember the golden rule: lenders use your gross income to maximize your borrowing power, but you must use your net income to ensure you can actually afford the monthly payments. Before you start touring homes, I highly recommend getting your paperwork in order.

Gather your last two years of W-2s or tax returns, and plug your numbers into an online mortgage income calculator to estimate your DTI. Taking this step early makes qualifying for a mortgage much smoother. It helps you figure out the maximum loan you can get, and more importantly, what you can comfortably pay without losing sleep.

People Also Read

- Ultimate Guide: How to Calculate Monthly Mortgage Payment?

- How to Calculate Mortgage Interest: Manually & Automatically

- [Solved] What Percentage of Income Should Go to Mortgage?

- [Solved] At What Income Level Do You Lose Mortgage Interest Deduction?