![[Explained] Bank Statement Loans: Requirements, Pros & Cons](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a0428043d5087bc7742c128_bank-statement-loans-banner.png)

Written by

Eric

Share this article

.svg)

Subscribe to updates

As a mortgage broker, I see this frustrating scenario every day: high-earning freelancers and business owners getting rejected for traditional mortgages. Why? Because legal tax write-offs crush their "net income" on paper. If your actual cash flow is fantastic but your tax returns don't show it, don't panic. A bank statement mortgage loan might be your perfect solution. Let me break down exactly how it works.

Key Takeaways

- What it is: A Non-QM loan using your actual bank deposits (cash flow) instead of tax returns to verify your income.

- Who it's for: Self-employed individuals, freelancers, gig workers, and small business owners.

- Top Benefit: Protects your tax deductions while still getting you approved for a home.

- Top Drawback: You'll face slightly higher interest rates (usually 0.5% to 2% higher) and need a larger down payment.

What is a Bank Statement Mortgage Loan?

A bank statement loan is a specific type of Non-QM (Non-Qualified Mortgage) loan designed for people whose tax returns simply don't reflect their true earning power.

With a traditional conventional loan, underwriters obsess over your net income after deductions. But with a bank statement loan, lenders evaluate your bank deposits over a 12 to 24-month period, typically applying an expense factor or other adjustments to estimate your qualifying income. They primarily evaluate your cash flow using bank statements, and may not rely on tax returns in the same way as traditional loans, though some lenders may still request them for verification.

In my practice, I frequently recommend this product to:

- Freelancers and gig economy workers

- Small business owners with heavy business expenses

- Real estate investors scaling their portfolios

- Independent contractors (1099 earners)

It's a powerful tool because it doesn't penalize you for taking the legal tax deductions your CPA recommended. You get the house, and you keep your tax savings.

Also Read:

- Explained: What is a Bank Statement? Everything to Know

- How to Calculate Self-Employed Income for a Mortgage?

- 8 Best Non-QM Mortgage Lenders: Which to Choose?

Bank Statement Mortgage Loan Example

Let me give you a real-world example from a recent client of mine, Sarah. She runs a successful creative agency, grossing $150,000 annually. However, after legally deducting equipment, travel, and home office expenses, her taxable "net income" on her tax returns dropped to $50,000. Traditional banks immediately rejected her for a $400,000 house, claiming she didn't earn enough.

Instead, we used a bank statement loan. By providing 12 months of her business bank statements, the underwriter saw her steady, high-volume deposits. Her true cash flow was recognized, and we got her approved and closed in under 40 days.

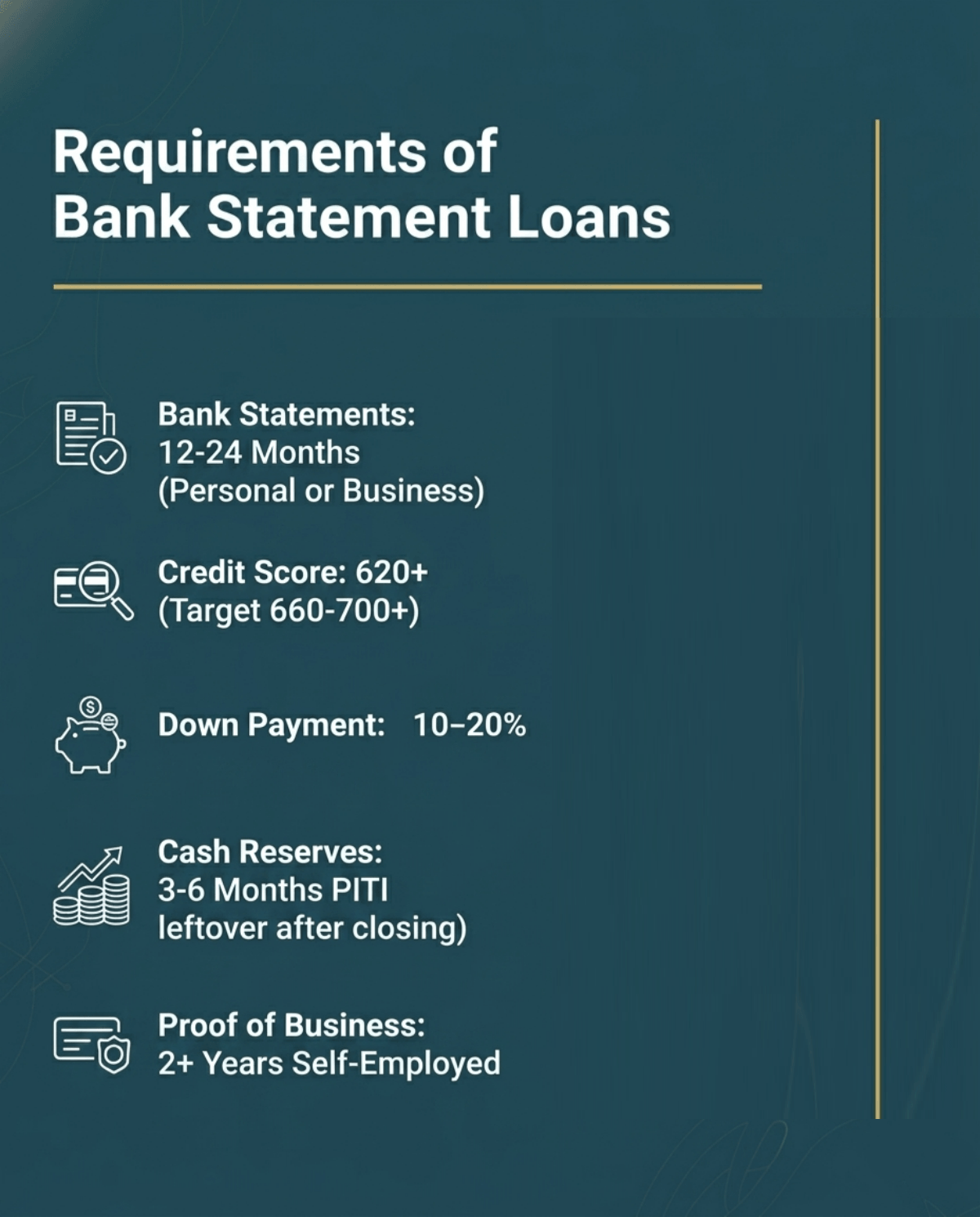

Requirements of Bank Statement Loans

Because lenders aren't relying on Fannie Mae or Freddie Mac standard guidelines, they take on more risk. To offset that risk in today's 2026 market, here are the core conditions you must meet:

- Bank Statements: You'll need to provide 12 to 24 months of consecutive personal or business bank statements. Underwriters want to see consistent, healthy deposit patterns.

- Credit Score: While some traditional loan programs (such as FHA) allow lower credit scores, bank statement loans often require a minimum of around 620 or higher, with more competitive terms typically starting at 660–700+.

- Down Payment: Low down payments, like 3%, are generally not available. Most lenders require around 10% to 20%, though some programs may allow slightly lower with stricter terms. The lower your credit profile, the higher the down payment required.

- Cash Reserves: Lenders want a safety net. You usually need 3 to 6 months of PITI (Principal, Interest, Taxes, and Insurance) liquid cash reserves leftover after closing.

- Proof of Business: You must prove you've been self-employed for at least 2 years (often verified via a CPA letter or business license).

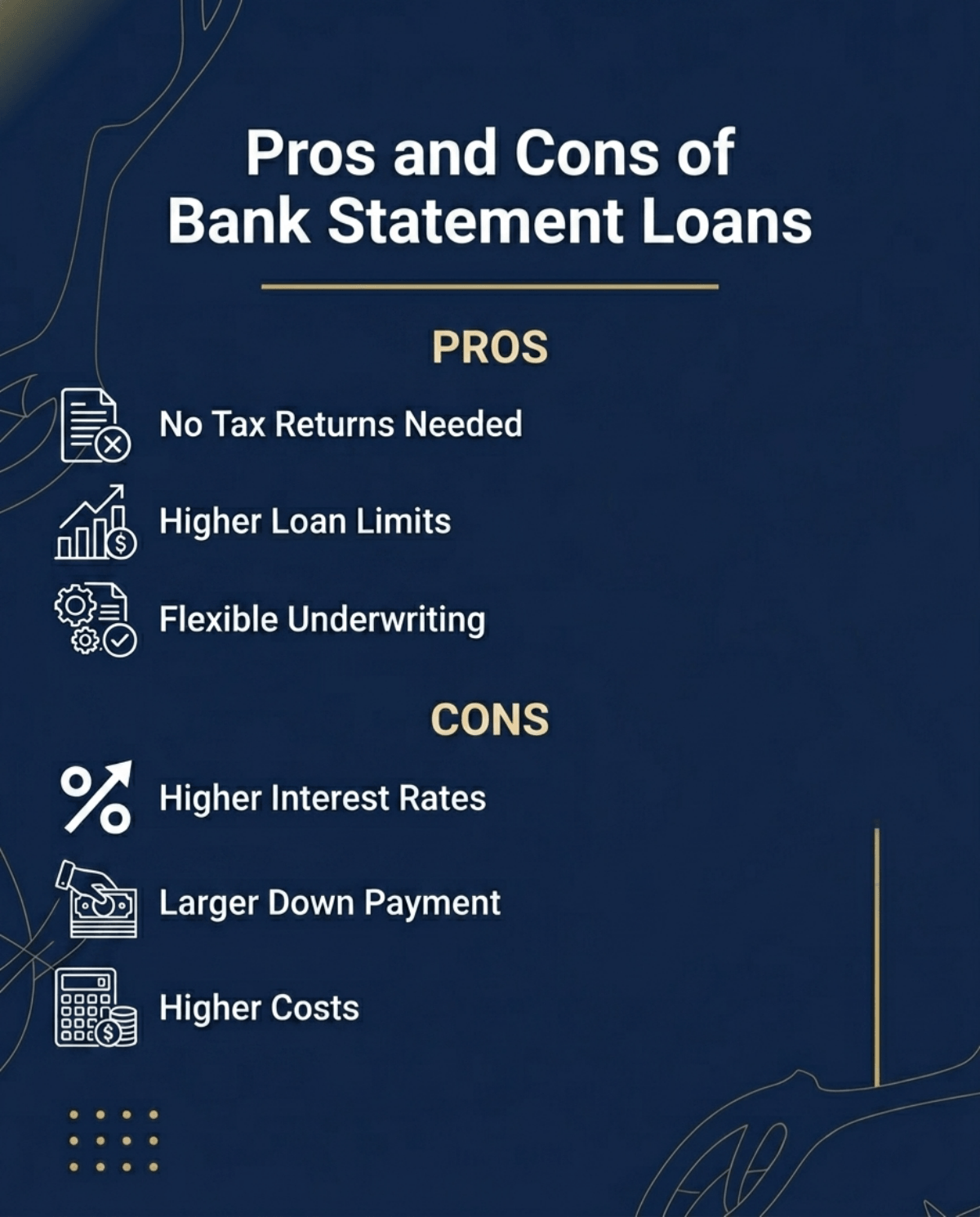

Pros and Cons of Bank Statement Loans

Before you commit, it's crucial to weigh the good against the bad. I always tell my clients to look at the full financial picture objectively.

Pros:

- No Tax Returns Needed: Protects your valuable tax write-offs and saves you from amending past returns.

- Higher Loan Limits: You may qualify for a larger loan amount if your cash flow supports it, since income is evaluated differently than with traditional tax-return-based methods.

- Flexible Underwriting: Focuses on your real-world cash flow rather than outdated agency formulas.

Cons:

- Higher Interest Rates: Expect to pay about 0.5% to 2% more in interest compared to conventional loans.

- Larger Down Payment: Tying up 10% to 20% of your cash in equity is mandatory.

- Higher Costs: Closing costs and potential prepayment penalties can make this loan slightly more expensive upfront.

How to Get a Bank Statement Mortgage Loan?

Ready to move forward? The process is a bit different from walking into your local retail bank. Here is exactly how I guide my clients to apply:

- Find a Non-QM Specialist: Don't waste time at traditional mega-banks. Work with a licensed mortgage broker who has direct access to wholesale Non-QM lenders. Or, you can freely talk with a vetted loan officer nearby on Bluerate.

- Organize Your Statements: Download your last 12-24 months of bank statements.Stop transferring money randomly between your accounts a few months before applying, as it muddies your deposit history.

- Draft Explanations: Prepare a Letter of Explanation (LOE) for any unusually large or out-of-the-ordinary deposits. Lenders need to verify the money is actual business revenue, not a secret loan.

- Submit and Wait: Submit your application alongside your CPA letter. Manual underwriting takes time, so closing typically takes around 30 to 45 days, though timelines can vary depending on the lender and documentation

Alternatives to Bank Statement Loans

If a bank statement loan doesn't perfectly fit your situation, maybe you don't have the 10% down payment or you hate the higher rate, there are other alternative financing paths:

- 1099 Income Loans: If you are an independent contractor, lenders can qualify you using solely your 1099 forms from the past 1-2 years, bypassing bank statements entirely.

- DSCR Loans: For real estate investors, the Debt Service Coverage Ratio loan ignores your personal income completely and bases approval purely on the property's rental income.

- Asset-Based Loans (Asset Depletion): If you have massive savings or retirement accounts but no current income, lenders can derive a monthly income by applying a discount to your eligible assets and dividing them over a set period (such as 60–120 months), depending on the program.

Also Read:

- Best USDA Loan Lenders: Top-Rated List

- Non-QM Loan Guidelines: How to Check and Verify with AI Accuracy

- [Tutorial] How to Estimate What Mortgage You Can Afford?

FAQs About Bank Statement Loans

Q1. Can I use bank statements to get a mortgage?

Yes, absolutely. By applying for a Non-QM bank statement loan, you bypass standard W-2 requirements. Lenders will calculate your qualifying income based entirely on 12 to 24 months of consistent bank deposits, making it an excellent path for the self-employed.

Q2. What are red flags on bank statements for mortgages?

When reviewing your statements, underwriters look for major red flags like unsourced large deposits, frequent overdrafts (NSF fees), and declining revenue trends. Unexplained transfers between different accounts also cause hesitation, as lenders want to ensure your business's cash flow is stable.

Q3. Are interest rates higher on bank statement loans?

Yes. Because these loans cannot be sold to Fannie Mae or Freddie Mac, lenders carry more risk. To offset this, bank statement loans typically carry interest rates about 0.5% to 2% higher than conventional mortgages, depending on your credit score and down payment.

Q4. What mortgage lenders don't look at bank statements?

Almost all lenders review recent bank statements to verify where your down payment funds came from. However, if you want a loan that doesn't use bank statements to calculate income, traditional lenders rely on tax returns, and DSCR lenders only care about property rental income.

Conclusion: Should You Get a Bank Statement Loan?

Ultimately, a bank statement loan is a brilliant financial tool, but it isn't for everyone. It comes down to weighing the cost of a higher interest rate against the massive tax savings you get to keep.

You should get one if:

- You have heavy legal tax write-offs that artificially lower your on-paper net income.

- Your business has healthy, consistent, and verifiable cash flow.

- You have at least 10% to 20% liquid cash ready for a down payment.

You shouldn't get one if:

- You can easily qualify for a traditional W-2 mortgage.

- You have a low credit score or minimal cash reserves, which could lead to denial.

Don't let tax deductions keep you from buying your dream home. I highly recommend consulting with a licensed mortgage broker who specializes in Non-QM products to review your last 12 months of statements and see exactly how much you can qualify for today!

(Disclaimer: The information provided is for educational purposes only and does not constitute financial advice. Mortgage rates and guidelines are subject to change. Always consult with a licensed mortgage professional regarding your specific situation.)

![[Solved] How to Calculate Commission Income for Mortgage?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a3ce1b02009d0aba39b3174_how-to-calculate-commission-income-banner.png)