Written by

Eric

Share this article

.svg)

Subscribe to updates

I still remember my first few weeks as a junior mortgage underwriter. I was staring at a massive stack of 1003 applications, tax transcripts, and credit reports, absolutely terrified of making a mistake. The mortgage industry moves fast, and the pressure to be perfectly accurate is intense.

If you're feeling overwhelmed by the sheer volume of lending guidelines, you're not alone. To survive and actually thrive on the desk, you need solid training. I've reviewed the best online mortgage underwriter training programs out there right now. We'll find the right fit so you can stop second-guessing your conditions and start clearing files with confidence.

Key Takeaways

- Guidelines change constantly: Relying on outdated rules leads to loan buybacks. Consistent training keeps you compliant and employed.

- Certifications give you leverage: Programs from NAMU or MBA Education provide the industry-recognized credentials you need to negotiate a higher salary.

- You don't always have to pay: If you are a beginner, Fannie Mae's official Learning Center is a fantastic, zero-cost starting line.

- Tech is the new standard: Modern professionals use tools like Zeitro to cut out the busywork, saving 7+ hours per loan file by automating manual reviews.

Why Do You Need to Take Mortgage Underwriting Training?

You might think you can just learn on the job as a mortgage underwriter, but agency guidelines update constantly. Relying on last year's rules is a fast track to compliance nightmares. Taking a structured training course gives you a massive advantage:

- Bulletproof compliance: You'll actually understand the why behind federal regulations, ensuring every file meets strict legal standards.

- Faster risk assessment: Spotting income red flags on a self-employed borrower's tax return becomes second nature, dropping your error rate significantly.

- Better pay and leverage: Certified underwriters simply make more money. It's the easiest way to jump from a junior role to a senior desk.

- Less daily stress: When you know the guidelines inside out, you clear conditions faster and sleep much better at night.

Top Mortgage Underwriter Training Programs

Finding a course that actually teaches real-world mortgage underwriting rather than just reading guidelines out loud is tough. I've narrowed down the top options based on curriculum quality, industry respect, and actual usefulness on the desk.

NAMU (National Association of Mortgage Underwriters)

NAMU is pretty much the most recognized name when it comes to industry credentials. They host intensive boot camps covering everything from processing basics to complex manual underwriting. This is really built for professionals who want a heavy-hitting credential on their resume to negotiate a higher salary. Their Official Underwriter Boot Camp includes multiple webinars that dive deep into FHA/VA loans, fraud detection, and tax return analysis.

Completing this program and passing the required proctored exam earns you the Certified Master Mortgage Underwriter (CMMU) designation. Most folks get through the core boot camp in about two to three weeks, but you get a full year of 24/7 access to review the material whenever you're stuck on a weird file. The full boot camp costs roughly $995. Individual classes are cheaper (around $99 to $495). It's pricey, but hiring managers actively look for NAMU certs.

Fannie Mae

You can't talk about underwriting without going straight to the source. The Fannie Mae Originating and Underwriting Learning Center is their official platform, packed with policy updates and direct guidance on what the secondary market actually buys. Honestly, every single person touching a loan file needs this bookmarked. It's the perfect starting point for rookies who need to learn conventional rules without spending their own money.

You'll find modules on navigating Desktop Underwriter (DU), calculating variable income, and interpreting the Selling Guide. The time commitment is totally up to you. You might spend ten minutes checking a specific job aid or an afternoon working through interactive eLearning modules. Best of all? It's 100% free. Since Fannie dictates the rules for most conventional loans anyway, building your foundation here costs nothing and pays off immediately in your day-to-day file reviews.

CampusUnderwriter

Acting as the training arm for NAMP and NAMU, CampusUnderwriter brings a virtual classroom vibe directly to your home office. They focus on instructor-led, recorded webinars taught by people who have actually spent decades on an underwriting desk. If you're a visual learner who zones out reading dry PDF guidelines and prefers a more hands-on, practical teaching approach, this is a great fit.

Their catalog is set up like an a la carte menu. You can pick highly specific workshops, like deep dives into calculating complex Debt-to-Income (DTI) ratios, reviewing tricky appraisals, or figuring out the quirks of USDA rural housing loans. A typical webinar takes a few hours to get through, and you retain access to the video recordings and training manuals for a full year.

Single classes typically run between $99.99 and $395.00. They also offer bundled packages if you need to tackle a few different weak spots in your knowledge base at once.

MBA Education

The Mortgage Bankers Association (MBA) is a massive player in housing advocacy and education. Their single-family residential loan production courses are known for being academically tough and highly respected by major banks and lenders nationwide. This path is definitely best for ambitious individuals gunning for management roles, corporate underwriting teams, or anyone wanting a broader understanding of the entire loan lifecycle.

They cover everything from basic fraud mitigation up to the prestigious Certified Residential Underwriter (CRU) designation, which requires completing a multi‑level curriculum and passing rigorous proctored exams.

The coursework is incredibly thorough. Depending on the track you choose, a self-study module might take just a few hours, whereas completing a full CRU certification requires weeks of intense studying and passing strict proctored exams. Pricing heavily depends on whether your employer is an MBA member. Members often get basic courses for free, while extensive certificate programs can range from $550 for members to over $1,100 for non-members.

OnCourse Learning

OnCourse Learning is a major provider of regulatory and compliance training across the financial sector. Their mortgage-specific catalog is strictly designed to keep lending staff out of trouble with state and federal regulators. I usually recommend this for underwriters working at regional banks, credit unions, or institutions that require structured, compliance-heavy continuing education to check off corporate HR requirements. Their underwriting modules are very procedural.

They walk you through evaluating a borrower's overall financial health, properly structuring a file for final approval, and spotting the common underwriting mistakes that lead to costly buybacks. These courses are entirely online and self-paced.

A comprehensive underwriting or pre‑licensing track often requires around 20 hours of online study. For a standard 20-hour comprehensive course, expect to pay around b. Costs scale down if your lending institution buys licenses in bulk for the whole underwriting department.

Coursera

You might not expect a tech-focused platform like Coursera to teach mortgage principles, but they partner with universities to offer surprisingly relevant content. Their "Mortgage for Underwriters" material offers a slightly different flavor, mixing traditional credit risk assessment with modern technological trends.

This is an awesome choice for tech-curious beginners or mid-level underwriters who want a fast, affordable look at how the industry is shifting toward predictive analytics and automated workflows. The curriculum is very forward-thinking. Alongside standard modules on credit reports and compliance, you'll learn about machine learning applications in risk analysis and how AI is changing underwriting desks.

It is highly flexible and bite‑sized, with many learners reporting that they complete the video lectures and readings in about 3 hours. It is also extremely budget-friendly. Access depends on your monthly Coursera subscription (usually around $39 to $59 a month), letting you explore this and thousands of other courses without a massive upfront commitment.

Comparison of Best Mortgage Underwriter Training

If you are juggling a packed pipeline today and just want the quick breakdown, I've organized this comparison table for you. Picking the right program depends entirely on where you are in your career. Are you trying to land your first junior role, or do you need a heavyweight certification to secure a promotion? Check out the stats below to make a fast decision.

My advice? Start reading Fannie Mae's guides for free to build your baseline, then ask your employer to sponsor your NAMU certification once you're established.

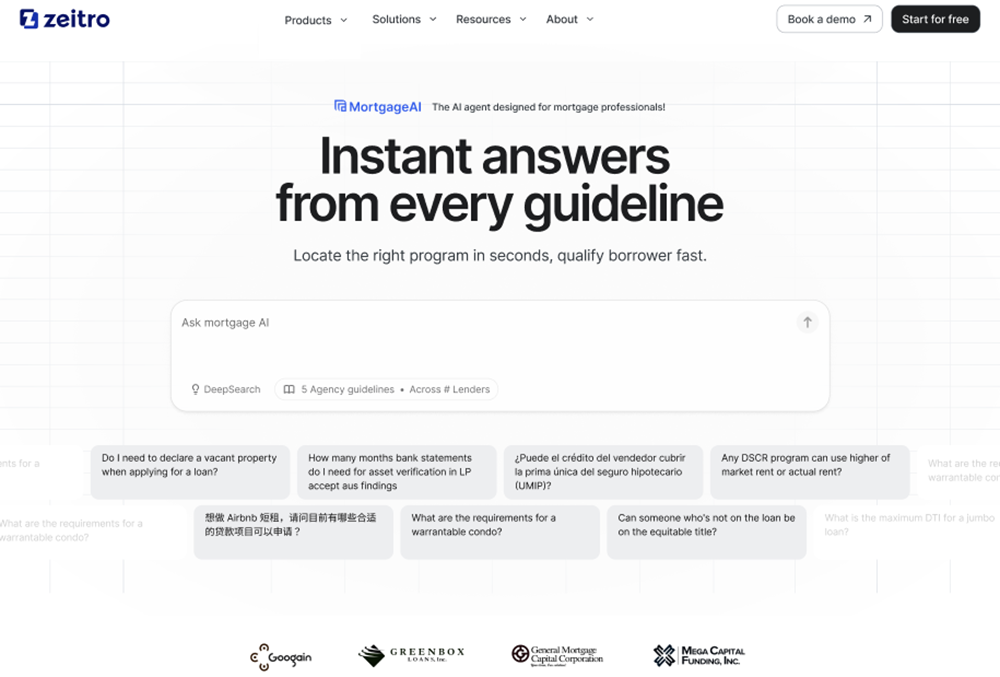

Bonus Tip: Leverage AI to Supercharge Your Underwriting Career

After you finish your training, reality hits. The actual day-to-day origination process is exhausting. Staring at hundreds of pages of bank statements and W-2s to manually calculate income will quickly burn you out. This is where leaning into smart tech becomes the best career hack you can use.

Top professionals aren't just working harder. They are using tools like Zeitro to eliminate the grunt work. Zeitro is an AI agent built specifically for US mortgage professionals. It doesn't replace your underwriting judgment. It actually empowers you to clear conditions up to 20% faster and save over 7 hours per loan file. Here is how their setup makes life easier:

- Zeitro Strata AI: Instead of frantically searching through a 1,000-page PDF manual, you just ask this AI assistant your vague QM or Non-QM guideline questions and get accurate, sourced answers in seconds.

- GrowthHub: If you're a broker or loan officer, this lets you launch a branded microsite to show off your expertise, display live rates, and capture organic borrower leads online on Bluerate.

- Digital 1003 (POS): This system automates the tedious application side. It pulls financial data, instantly calculates AI-driven DTI, and exports FNM 3.4 files, letting borrowers pre-qualify in just 5 minutes.

- Pricing Engine: A super-fast rate quote tool for conventional and Non-QM products, allowing you to apply custom overlay adjustments and price out loans instantly.

FAQs About Mortgage Underwriter Training

Q1. What are the 4 C's of mortgage underwriting?

The 4 C's of mortgage underwriting are Capacity, Capital, Collateral, and Credit. Capacity measures the borrower's ability to repay the debt using their DTI ratio. Capital looks at their down payment and cash reserves. Collateral evaluates the property's value through an appraisal. Finally, Credit reviews their past payment history to predict future reliability.

Q2. How long does it take to become a certified mortgage underwriter?

It generally takes anywhere from a few weeks to several months to get officially certified and become a mortgage underwriter. It depends entirely on your background and the program. A NAMU boot camp, for example, might require two to three weeks of focused study. However, getting truly comfortable making lending decisions on a live desk takes months of practice.

Q3. What certifications should I get for underwriting?

I usually suggest starting with the Certified Master Mortgage Underwriter (CMMU) from NAMU or the MBA's Certified Residential Underwriter (CRU). If you are processing a lot of government loans, obtaining your FHA Direct Endorsement (DE) or VA LAPP/SAR authority is basically mandatory for advancing your career and boosting your salary.

Q4. Are there free mortgage underwriting training?

Yes. The Fannie Mae Originating and Underwriting Learning Center is completely free and provides incredible modules on conventional lending rules. You can also find solid walkthroughs on YouTube. Just keep in mind that while these free options are great for your own knowledge, they won't give you the formal certificates employers look for.

Q5. What is the salary of a mortgage underwriter?

The average US mortgage underwriter salary is around $65,000 to $85,000 a year, according to recent job market data. But that number scales fast. Senior underwriters, or those holding specialized designations like a DE certification, can often reach or exceed $100,000 in high‑volume markets or specialized Non‑QM lending sectors.

Conclusion

Stepping into an underwriting role doesn't have to feel like you're constantly guessing. Investing a little time into a quality online training program is the fastest way to build your technical skills and stop second-guessing your loan decisions. Whether you decide to grab a premium certification from NAMU to boost your resume, or you just spend tonight reading through Fannie Mae's free resources, the most important thing is to start learning.

Pick the course from the table above that fits your current situation. And remember, once you've got those foundational guidelines memorized, don't hesitate to use modern AI tools like Zeitro to cut out the tedious manual data entry. Your pipeline, and your sanity, will thank you!

People Also Read

- AI Mortgage Underwriting Explained: Will You Be Replaced?

- Best AI Mortgage Underwriting Software for Loan Professionals

- Mortgage Underwriting Automation: What Is It? How Does It Work?

- Best Mortgage Underwriter Software: AI & Guideline Verification

- How to Check Mortgage Eligibility? Quick and Accurate with Sources

- Best Mortgage Loan Processor Training for Beginners

- 30 Mortgage Underwriter Interview Questions to Prepare First

![[Solved] How to Calculate Commission Income for Mortgage?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a3ce1b02009d0aba39b3174_how-to-calculate-commission-income-banner.png)