Written by

Eric

Share this article

.svg)

Subscribe to updates

Navigating the mortgage industry can feel like a maze, especially when you're aiming for the role of a mortgage underwriter, the ultimate gatekeeper of loan approvals. In my experience, while many talented professionals enter this field through grit and on-the-job learning, the market has shifted significantly. Today, proving your expertise isn't just an "extra". It's a career-defining move.

Whether you are just starting or looking to climb the ladder at a top-tier lender, choosing the right certification is your most strategic play. In this guide, I'll break down the best mortgage underwriter certifications in the U.S., helping you decide which path will actually move the needle for your salary and professional standing.

Takeaway

- Not Mandatory, but Essential: Certifications aren't legally required like MLO licenses, but they are often the "tie-breaker" in hiring.

- NAMU vs. MBA: NAMU offers great specialized niches.MBA is the "Gold Standard" for prestige and long-term executive paths.

- Tech is the New Skill: Modern underwriters must pair their certification with AI tools like Zeitro to stay competitive.

Do You Have to Have a Certification to Become a Mortgage Underwriter?

One of the most common questions I hear from newcomers is whether they need a license to start. Technically, the answer is no.

Unlike Mortgage Loan Originators (MLOs), who must obtain an NMLS license under the SAFE Act, mortgage underwriters typically work in back‑office roles and are not, as a category, required by federal law to hold an MLO license. However, if an underwriter also performs loan‑originating activities (for example, receiving production‑based compensation), some states or lenders may require an NMLS‑MLO license under local rules.

Don't let that fool you. From what I've seen in current job postings at major banks, resumes without a certification often end up at the bottom of the pile. A certification acts as a "seal of trust," signaling to employers that you understand complex FHA/VA guidelines and federal regulations (like TRID or HMDA) without needing months of expensive hand-holding.

Top Mortgage Underwriter Certifications to Know

The following certifications are issued by the National Association of Mortgage Underwriters (NAMU) and the Mortgage Bankers Association (MBA). These are the most respected bodies in the U.S. mortgage landscape.

Also Read:

- Best Mortgage Underwriter Training Online: Improve Your Expertise

- 30 Mortgage Underwriter Interview Questions to Prepare First

NAMU-CMU (Certified Mortgage Underwriter)

I often recommend the CMU as the "Foundational Step." It covers the bread and butter of underwriting, including tax return analysis, credit report navigation, and basic appraisal reviews. It's a moderate difficulty level designed to ensure you won't make "rookie mistakes" that lead to buy-backs.

- Suitable for: Entry-level professionals or Loan Officers looking to transition into underwriting.

- Requirements: You must complete a series of online training modules and pass the final exam with a score of 75% or higher. There is no strict "years of experience" requirement, making it the perfect entry point for those wanting to prove they have the technical knowledge to handle a file.

NAMU-CMMU (Certified Master Mortgage Underwriter)

CMMU is the "Heavyweight" title within NAMU. It signals that you've moved beyond basic checklists and can handle complex scenarios, such as self-employed borrowers with multiple business entities. In my view, having "Master" in your title significantly increases your leverage during salary negotiations.

- Suitable for: Senior underwriters and those aiming for management or team lead positions.

- Requirements: This requires more rigorous testing than the CMU. You'll need to demonstrate a deep understanding of advanced underwriting concepts. This exam is typically recommended for candidates with at least 2–3 years of field experience, as it involves more nuanced case studies.

NAMU-CAMU (Certified Ambassador Mortgage Underwriter)

The CAMU is less about "how to underwrite" and more about "how to lead." It represents the highest level of NAMU recognition. It's perfect for professionals who want to train others or open their own contract underwriting firm.

- Suitable for: Industry veterans, consultants, and those who want to be recognized as "Thought Leaders."

- Requirements: This certification requires an extensive background in the industry. It's often the culmination of holding other NAMU certifications and showing a commitment to continuing education and ethical standards in the mortgage space.

NAMU-CFMU (Certified FHA Mortgage Underwriter)

FHA loans have very specific, often rigid guidelines (HUD 4000.1). Being a CFMU means you are an expert in these government nuances. Given that FHA loans are a staple for first‑time homebuyers in the U.S., this certification can make your skill set more resilient during economic downturns.

- Suitable for: Underwriters working in retail or wholesale lending where government-backed loans are a priority.

- Requirements: The curriculum focuses exclusively on FHA-specific guidelines, mortgage insurance premiums, and property requirements. You must pass a specialized exam that tests your ability to interpret HUD handbooks accurately.

NAMU-CMRC (Certified Mortgage Regulatory Compliance)

With the CFPB constantly updating rules, compliance is the biggest headache for lenders. I've found that underwriters who understand the legal side, TILA, RESPA, and Fair Lending, are the most valued. The CMRC certificate proves you can keep a lender out of legal trouble.

- Suitable for: Compliance officers, QC specialists, and senior underwriters.

- Requirements: You'll study federal regulations and audit procedures. The exam is detail-oriented and requires a high level of precision, reflecting the nature of compliance work itself.

NAMU-CMQCS (Certified Mortgage Quality Control Specialist)

CMQCS focuses on the "Post-Closing" and "Pre-Funding" audit side. It's for people who love finding the "needle in the haystack." If you prefer auditing files for errors rather than live production, this is your niche.

- Suitable for: Quality Control (QC) staff and Risk Management professionals.

- Requirements: Candidates must master audit workflows and learn how to report findings to management. It requires passing a focused exam on quality assurance protocols.

NAMU-CCUP (Certified Commercial Underwriting Professional)

Commercial underwriting is a different beast entirely. You're looking at Debt Service Coverage Ratios (DSCR) and rent rolls instead of just W-2s. This CCUP certification is the bridge for residential pros wanting to enter the commercial space.

- Suitable for: Those looking to leave residential lending for the high-stakes world of Commercial Real Estate (CRE).

- Requirements: This is a high-difficulty certification. It requires learning complex financial statement analysis and commercial property valuation methods.

MBA-CRU (Certified Residential Underwriter)

If NAMU is the specialist, the MBA is the "Ivy League." The CRU designation is globally recognized and highly prestigious. In my experience, if you want a C-suite or VP role at a national bank like Chase or Wells Fargo, the CRU is your best bet.

- Suitable for: Career-focused professionals seeking the highest level of industry prestige.

- Requirements: This is a multi-level program (Levels I, II, and III). It requires a combination of professional experience, points earned through MBA courses, and passing a comprehensive final examination. It is a long-term commitment that usually takes a year or more to complete.

How to Maintain Your Certification and Stay Compliant?

Getting your certificate is a massive milestone, but I always tell my peers: don't let it gather dust. In the mortgage world, guidelines from Fannie Mae, Freddie Mac, and HUD are constantly shifting. To keep your credentials active and respected, you must follow specific maintenance protocols.

- For NAMU designations, you generally need to pay an annual renewal fee (typically around $95) and may be required to complete several hours of Continuing Education (CE) each year. This ensures you stay updated on the latest anti-fraud measures and regulatory changes.

- On the other hand, the MBA-CRU requires recertification every three years. You'll need to earn "points" through professional development, attending industry seminars, or taking advanced courses.

In my experience, showing an "Active" status on your LinkedIn or resume is a huge trust signal for recruiters—it proves you aren't just relying on old knowledge, but are actively staying ahead of the curve in a volatile market.

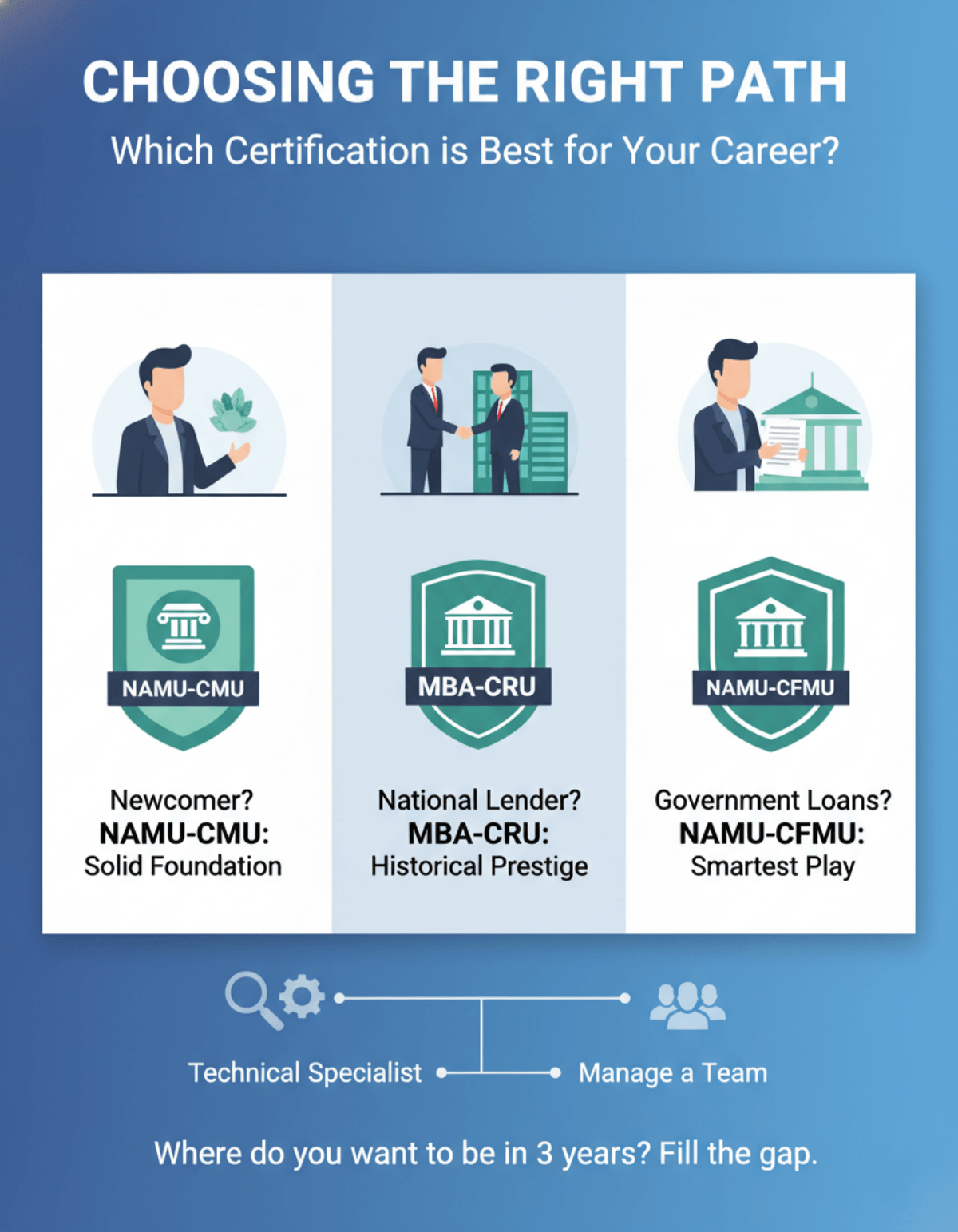

Choosing the Right Path: Which Certification is Best for Your Career?

Picking a certification shouldn't be a guessing game.

- If you are a newcomer, I suggest starting with the NAMU-CMU to build a solid foundation.

- If your goal is to work for a major national lender, the MBA-CRU carries the most weight due to its historical prestige.

- For those who want to carve out a niche in government-backed loans, the NAMU-CFMU is the smartest play.

Think about where you want to be in three years. Do you want to manage a team or be a technical specialist? Pick the credential that fills that specific gap in your resume.

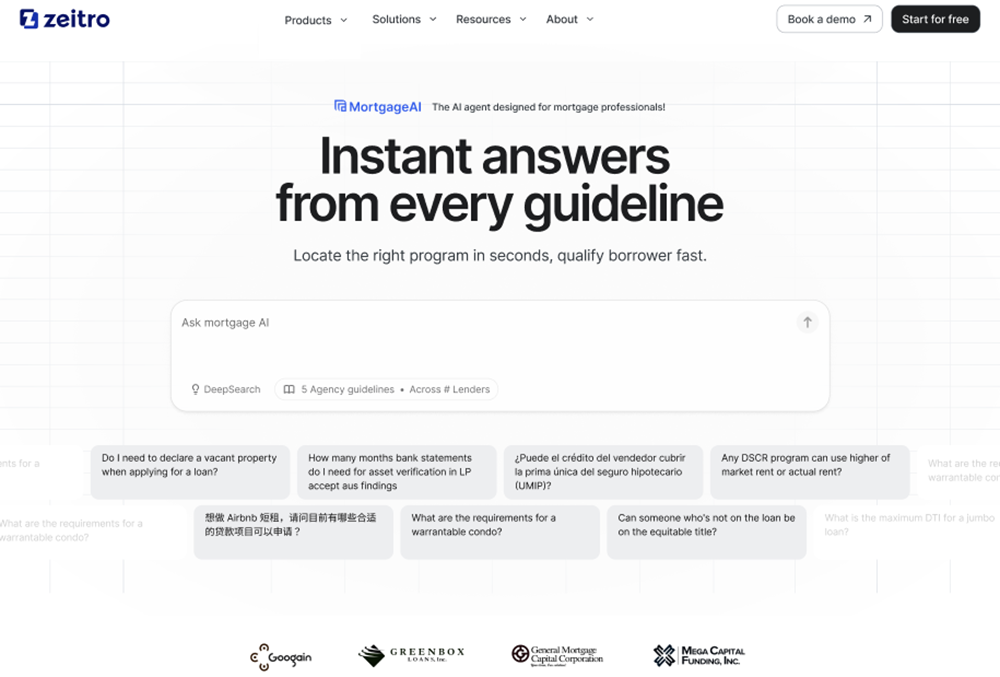

Zeitro: The Missing Piece Beyond Certifications

Even with the best certifications, the sheer volume of data in modern lending is overwhelming. I've realized that professional knowledge is only half the battle. The other half is efficiency. That's where Zeitro comes in. It's an AI-powered SaaS designed specifically for U.S. mortgage professionals to bridge the gap between "knowing the rules" and "applying them fast."

- Zeitro Strata AI is a lifesaver for verifying complex Non-QM guidelines. Instead of flipping through a 500-page PDF, you can ask specific questions and get sourced answers in seconds. Beyond guidelines,

- Zeitro's Digital 1003 and Pricing Engine automate the tedious parts of the application and DTI calculations. I've seen it save underwriters 7+ hours per loan file.

- By using the GrowthHub to showcase your expertise on a branded site, you're not just an underwriter. You're a tech-savvy pro. In today's market, pairing your certification with a tool like Zeitro allows you to close loans 20% faster while maintaining 85%+ accuracy.

FAQs About Best Mortgage Underwriter Certifications

Q1. Can I become an underwriter without a degree?

Yes. While some large banks prefer candidates with a degree in finance, many mortgage lenders place significant weight on hands‑on experience and certifications like the NAMU‑CMU, and may value them as much as or more than a diploma.

Also Read: [NO Experience] How to Become a Mortgage Underwriter?

Q2. What certifications should I get for underwriting?

Start with the NAMU-CMU for general residential work. If you want to specialize, look into the NAMU-CFMU (FHA) or the MBA-CRU for high-level career paths.

Q3. Is NAMU certification worth it?

In my opinion, yes. It is the most accessible and widely recognized specialized training for underwriters, often leading to immediate pay raises or better job offers.

Q4. How long does it take to become a certified underwriter?

For NAMU, you can finish the coursework in a few weeks. The MBA-CRU is more intensive and can take 6–12 months depending on your pace.

Q5. Do mortgage underwriters make good money?

Absolutely. According to recent U.S. labor data, senior underwriters often earn between $65,000 and $85,000, with those holding specialized certifications and using AI tools reaching the higher end of that bracket.

Conclusion

To wrap things up, becoming a top-tier mortgage underwriter in the current U.S. market requires a blend of formal credentials and modern tech skills. While you can technically start without a certification, I've found that those who invest in their education early on see much faster promotions and higher salary ceilings.

However, don't stop at the certificate. The industry is evolving, and manual "PDF-checking" is being replaced by AI. By combining a reputable certification like the MBA-CRU or NAMU-CMU with a powerful AI agent like Zeitro, you position yourself as an indispensable asset to any lender. It's about being more than just a "checker". It's about being a high-efficiency expert who knows how to leverage the best tools to close more loans, faster.

People Also Read

- AI Mortgage Underwriting Explained: Will You Be Replaced?

- Best AI Mortgage Underwriting Software for Loan Professionals

- Mortgage Underwriting Automation: What Is It? How Does It Work?

- Best Mortgage Underwriter Software: AI & Guideline Verification

- How to Check Mortgage Eligibility? Quick and Accurate with Sources

![[Solved] How to Calculate Commission Income for Mortgage?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a3ce1b02009d0aba39b3174_how-to-calculate-commission-income-banner.png)