Written by

Eric

Share this article

.svg)

Subscribe to updates

I've seen countless real estate deals hinge on one crucial number: the Loan-to-Value (LTV) ratio. Whether you are a homebuyer trying to figure out your down payment to avoid PMI, or a Loan Officer (LO) matching a borrower to the right QM or Non-QM product, getting this calculation right is everything.

It literally dictates interest rates, loan approvals, and insurance costs. In this guide, I will walk you through exactly how to calculate it, from simple formulas for buyers to advanced AI verification tools for industry professionals.

Key Takeaways

- LTV defines your risk: It compares your mortgage amount to the property's value, heavily influencing your interest rate.

- Calculation is straightforward: You can use a manual formula or free online calculators for quick financial estimates.

- Loan Officers need more than math: Professionals should use AI tools like Zeitro Strata to instantly verify if a specific scenario meets complex lender guidelines.

- Different loans, different limits: FHA allows up to 96.5%, while Conventional programs can go up to 97%.

What is the LTV Ratio?

The Loan-to-Value (LTV) ratio is a financial metric lenders use to assess the risk of your mortgage application. Simply put, it measures how much money you are borrowing against the actual worth of the home. The higher the percentage, the riskier the loan appears to the bank.

Here is an insider tip from my underwriting days: lenders don't just use the asking price. When calculating this metric, they always use the lower of the purchase price or the appraised value. If you agree to buy a house for $400,000 but the appraiser says it's only worth $380,000, your lender will base their math on that $380,000.

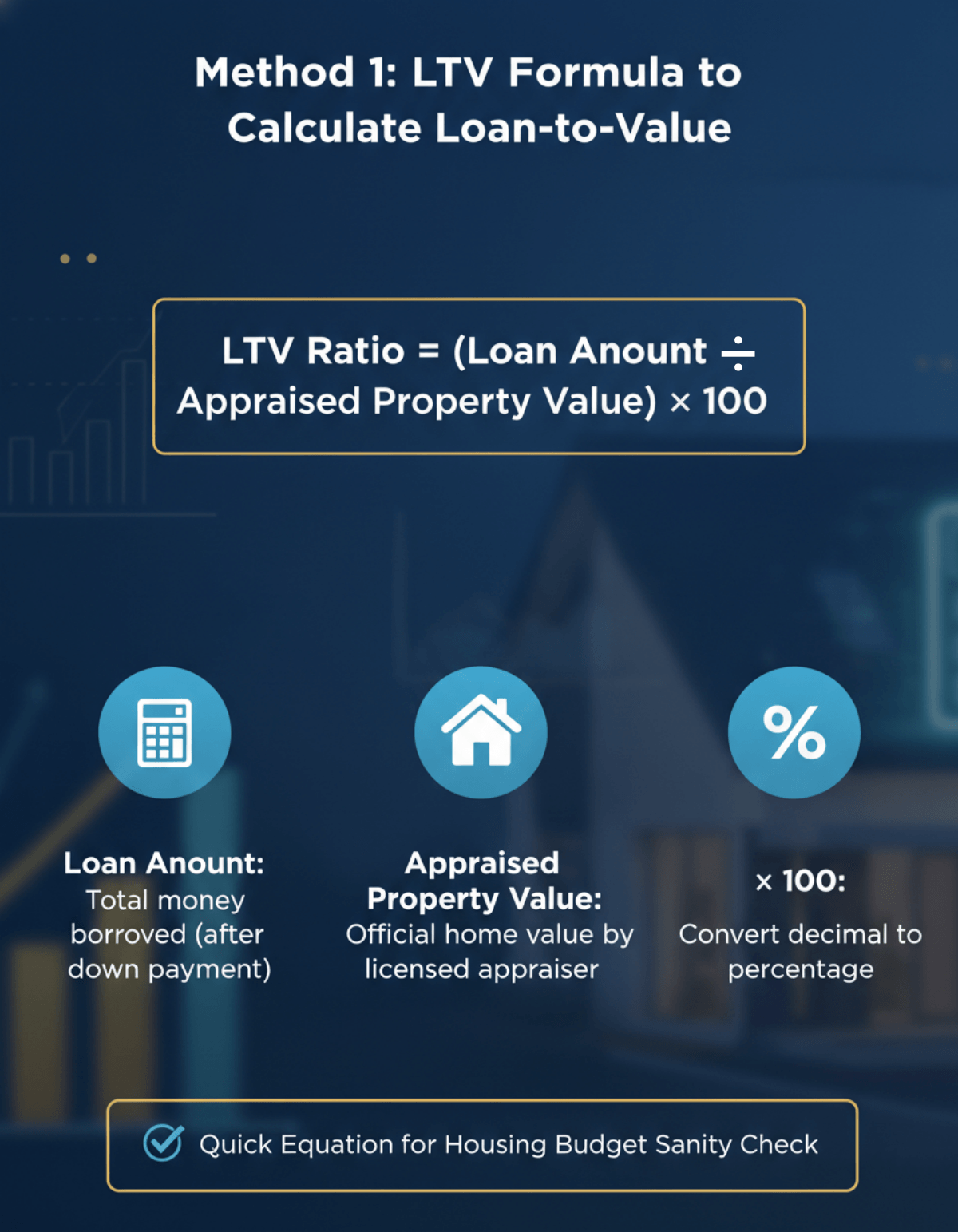

Method 1: LTV Formula to Calculate Loan-to-Value

If you prefer crunching the numbers yourself, the math is actually quite simple.

The universal LTV formula is: LTV Ratio = (Loan Amount ÷ Appraised Property Value) × 100.

Let's break down those variables. The "Loan Amount" is the total money you need to borrow after subtracting your down payment. The "Appraised Property Value" is what the home is officially worth, as determined by a licensed appraiser. To calculate, simply divide the mortgage amount by the property's value. Then, multiply that resulting decimal by 100 to get your percentage.

I always tell my clients to run this quick equation before we even start house hunting. It gives you a realistic baseline of your purchasing power. It is the most fundamental logic out there, perfect for buyers who want to grab a calculator and do a rapid sanity check on their housing budget.

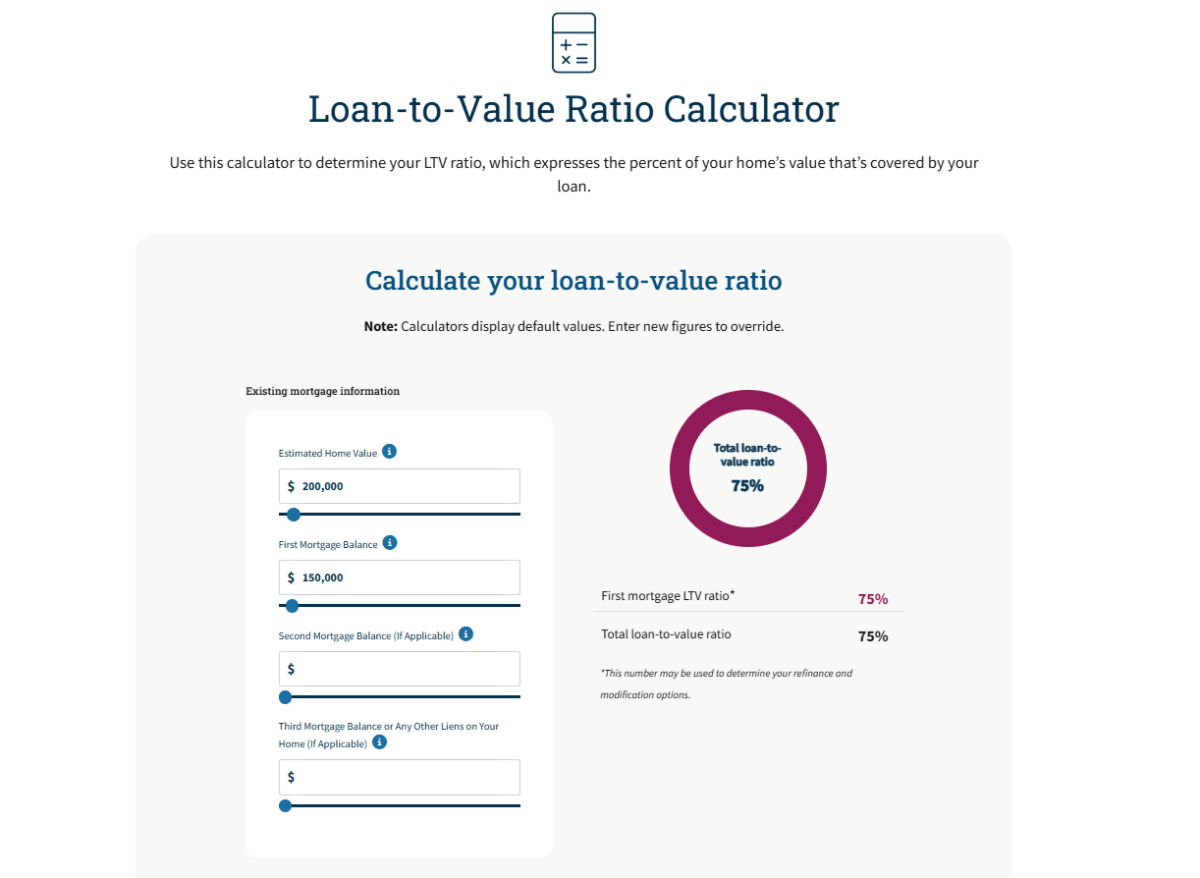

Method 2: Use an Online LTV Calculator to Calculate LTV

You certainly don't have to do the math manually. There are plenty of reliable online calculators that do the heavy lifting instantly. For instance, the Fannie Mae LTV Calculator is excellent because it comes straight from an authoritative government-sponsored enterprise. Another great, user-friendly option is the Bankrate LTV Calculator, which features interactive sliders.

The biggest advantage here is convenience. They are free, incredibly intuitive, and perfect for everyday consumers needing a quick figure. However, they have a glaring downside: they only give you a raw number. A basic calculator cannot tell you if an 85% LTV will actually get approved for a specific program or if it aligns with a lender's current rulebook. They lack the context needed for complex underwriting decisions, which brings us to the professional approach.

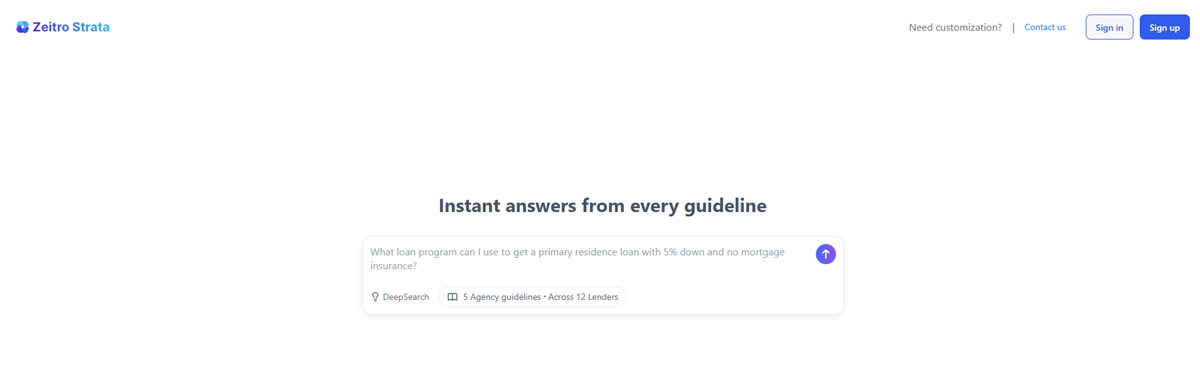

Method 3: Zeitro Strata to Calculate and Verify LTV Ratio

For Mortgage Loan Officers and Brokers, getting the raw percentage is only step one. The real challenge is knowing if that number actually qualifies under hundreds of ever-changing investor rules. That's why I recommend Zeitro Strata as the ultimate AI-powered mortgage guideline assistant. It goes far beyond a standard calculator by verifying your scenario against real-world criteria.

Using its DeepSearch feature, you can cross-check a specific LTV against 100+ investors and 300+ guidelines (covering everything from Conventional to tricky Non-QM loans like DSCR or Bank Statement) in seconds.

Every answer includes a direct Citation, so you can trace it back to the source with complete confidence. You can ask it a specific scenario like, "What is the max LTV for a DSCR loan with a 680 FICO?" in English or Chinese. If a detail seems confusing, its "Explain" function clarifies it instantly. Best of all, their "Explorer" tier lets you ask 10 free queries a day, while full access is just $8/month.

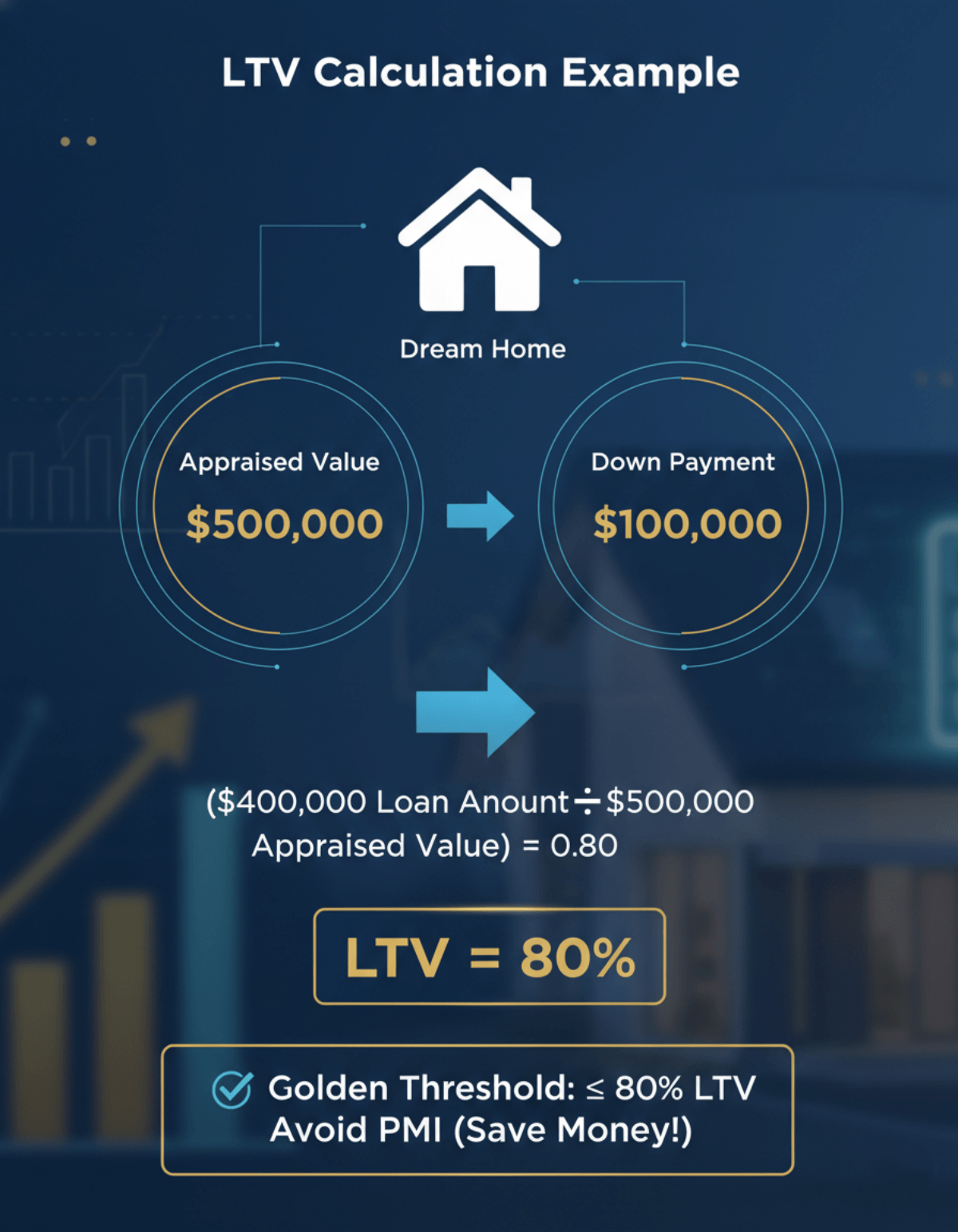

LTV Calculation Example

Let's look at a real-world scenario to see how this plays out in practice. Suppose you find your dream home, and the appraised value comes in at $500,000. You have saved up a solid 20% down payment, which equals $100,000. This means you need to borrow the remaining $400,000 from the bank.

Plugging these figures into our standard formula: ($400,000 ÷ $500,000) = 0.80. Multiply that by 100, and your LTV is exactly 80%.

Why is this specific example so important? In the mortgage industry, 80% is the golden threshold. By keeping your loan-to-value at or below this mark, you typically avoid paying Private Mortgage Insurance (PMI), saving you hundreds of dollars on your monthly payment.

Max LTV Requirements by Loan Types

Even if your math is perfectly correct, your loan still needs to fit within standard industry limits. Different programs have varying risk tolerances. Here is a quick reference guide for maximum LTV allowances:

- Conventional Loans: Up to 97% for qualified first-time homebuyers meeting automated underwriting approval (e.g., Desktop Underwriter) and other eligibility criteria.

- FHA Loans: Up to 96.5% (3.5% minimum down payment) for first-time buyers with credit scores of 580 or higher purchasing homes at or below HUD limits. 90% max for scores below 580.

- VA and USDA Loans: Can go up to an incredible 100% (zero down payment required) for eligible veterans or rural homebuyers.

- Non-QM Loans (e.g., DSCR, ITIN): Highly variable, typically strictly capped between 70% and 80%.

Because Non-QM standards fluctuate wildly between lenders like AAA Lending or AD Mortgage, LOs should absolutely use Zeitro Strata's customizable tags to instantly filter and lock down the exact guideline for specific investors.

FAQs About LTV Ratio Calculation

Q1. What is the difference between LTV and CLTV?

While standard LTV only looks at your primary mortgage, Combined Loan-to-Value (CLTV) includes every single debt tied to the property, such as a HELOC or a second mortgage. Lenders use CLTV for secondary financing approvals to calculate total borrowing against the home's value.

Q2. Does a higher LTV mean a higher mortgage rate?

Yes, it usually does. A higher percentage indicates more risk for the financial institution lending you the money. To compensate for that elevated danger of default, banks will typically charge you a higher interest rate and require costly private mortgage insurance until your equity increases.

Q3. What is a good LTV ratio?

Generally, reaching a ratio of 80% or lower is considered the "golden rule" in the lending world. Hitting this exact target shows you have strong initial equity, which helps you easily avoid paying expensive mortgage insurance while securing the most competitive interest rates available.

Q4. Why do max LTV requirements change?

Maximum limits shift constantly due to broader macroeconomic conditions, the specific type of loan product (QM vs. Non-QM), and internal risk management at individual banks. Financial institutions frequently update their internal guidelines to protect their capital investments during volatile housing markets.

Conclusion

Understanding your Loan-to-Value ratio isn't just a simple math exercise. It is the foundation of a successful real estate transaction. For everyday homebuyers, knowing this number empowers you to budget for down payments correctly and anticipate potential insurance costs. I highly encourage consumers to leverage free online calculators to plan their finances.

However, if you are a mortgage professional, basic math isn't enough. Stop wasting hours manually digging through PDF guidelines. I strongly suggest signing up for the free Explorer tier of Zeitro Strata AI. It will instantly verify your complex scenarios, boost your overall ROI, and dramatically elevate the speed of service you provide to your clients.

People Also Read

- Max DTI for Mortgage: Requirements By Loan Types

- How to Calculate DTI Ratio for Mortgage?

- AI Mortgage Underwriting Explained: Will You Be Replaced?

- What is Mortgage Eligibility Checker? Best Tool to Verify Guidelines

- Mortgage Guidelines: What Are They? How to Verify?

- [Tutorial] How to Estimate What Mortgage You Can Afford?

![[Solved] Can I Use K-1 Income to Qualify a Borrower?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a44cb55129383ad19f46080_can-i-use-k-1-income-to-qualify-a-borrower-banner.png)