Written by

Eric

Share this article

.svg)

Subscribe to updates

In my years working as a loan officer, Ive seen countless homebuyers feel completely overwhelmed by today's tricky interest rate environment. You aren't alone if you're stressing over monthly payments. Thats why I often recommend looking into an Adjustable Rate Mortgage (ARM).

Put simply, its a home loan where your interest rate is locked in at first, but later floats up or down based on the market. In this guide, Ill walk you through exactly how ARMs work, their pros and cons, and whether this strategy actually makes financial sense for your specific situation.

Key Takeaways

- Introductory period: An ARM starts with a lower, fixed interest rate for the first few years before transitioning into a variable phase.

- Market-driven: Once the fixed term ends, your new rate is calculated using a baseline Index plus a fixed Margin.

- Rate caps: These built-in safety nets limit exactly how high your interest can spike.

- Best use case: These loans can be a good fit if you plan to sell the property or refinance before the adjustable period begins.

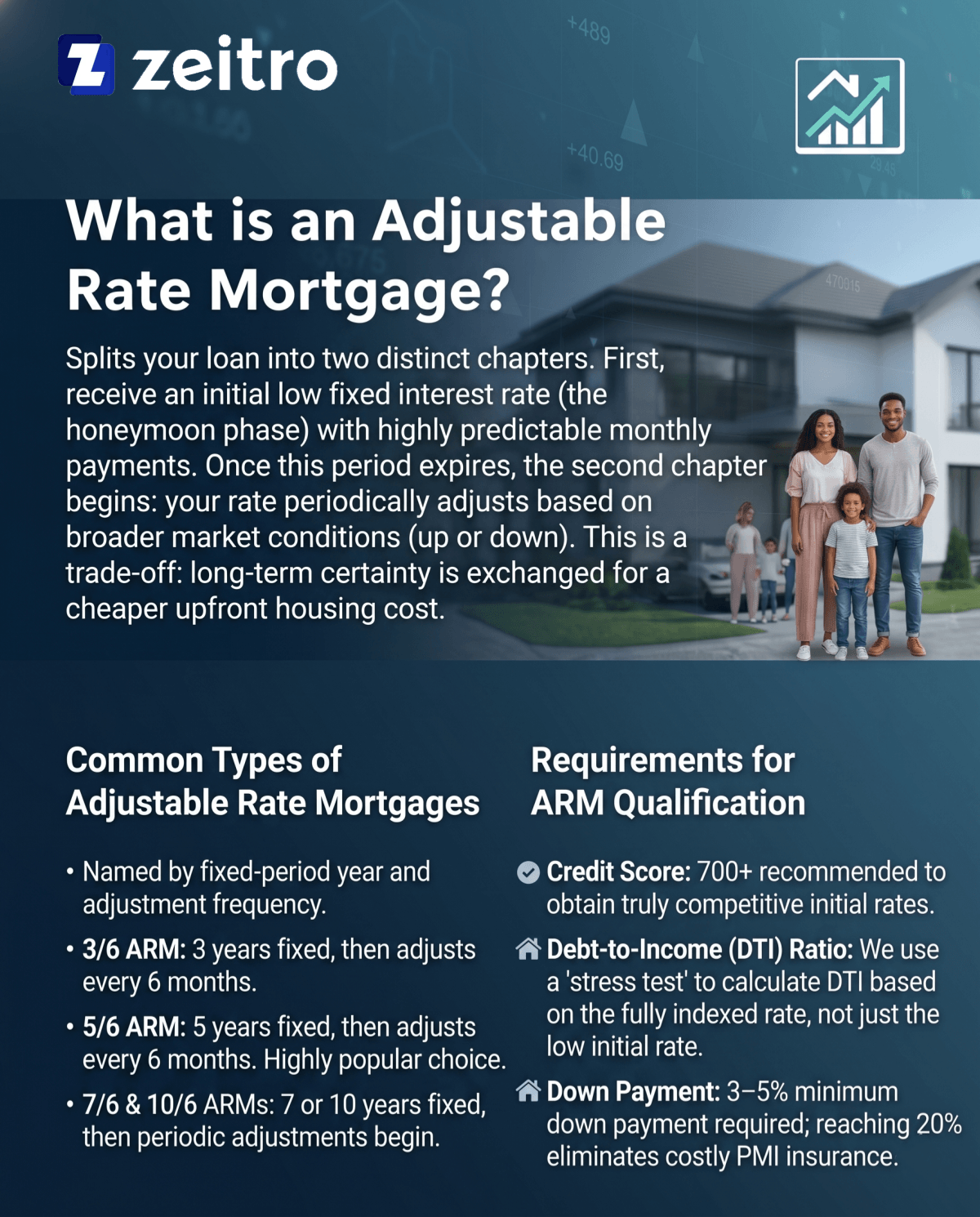

What is an Adjustable Rate Mortgage?

When you sit at my desk and ask for a traditional fixed-rate mortgage, you get the exact same interest rate for 30 years. An Adjustable-Rate Mortgage is fundamentally different. It splits your loan into two distinct chapters.

During the first phase, you receive an initial fixed interest rate, which is often lower than that of a standard fixed-rate mortgage. This introductory interest rate is typically lower than what you'd find on a standard fixed-rate loan, giving you highly predictable, manageable monthly payments right out of the gate.

However, once that initial honeymoon phase expires, chapter two begins. Your rate will periodically adjust based on broader market conditions. If national rates fall, your mortgage payment drops. But if the market heats up, your monthly obligations will increase. That unpredictability is the core tradeoff: you are exchanging long-term certainty for a cheaper upfront housing cost. Its a powerful tool, but as I always warn my borrowers, you have to be prepared for those future rate fluctuations.

Types of an Adjustable Rate Mortgage

Mortgage lenders use a two-number naming system to categorize these loans. The first number tells you how many years the rate is locked, while the second indicates how often it changes afterward. Many modern ARMs adjust every six months and are commonly tied to the SOFR index, although adjustment periods can vary depending on the loan structure.

Here are the most common options I write for clients:

- 3/6 ARM: Your rate stays the same for the first three years. After that, it adjusts twice a year.

- 5/6 ARM: You get five years of stability before the biannual adjustments begin. This is currently a very popular choice.

- 7/6 and 10/6 ARMs: These offer seven or ten years of fixed payments. They act very similarly to traditional 30-year loans but offer a slight discount on the initial interest.

Requirements of an Adjustable Rate Mortgage

Qualifying for a variable-rate loan actually requires jumping through a few more hoops than standard financing. From my underwriting experience, here is what we look for:

- Credit Score: While conventional guidelines from Fannie Mae or Freddie Mac technically allow a 620 minimum, youll usually want a score of 700 or higher to get a truly competitive teaser rate.

- Debt-to-Income (DTI) Ratio: This is where it gets tough. Lenders don't just qualify you based on the low starting rate. We use a "stress test" by calculating your DTI based on the fully indexed rate (the current index plus margin), rather than the initial introductory rate. We want to make sure you won't default if your bill goes up.

- Down Payment: You can secure an ARM with as little as 3% to 5% down, though reaching 20% eliminates costly private mortgage insurance (PMI).

How Does an Adjustable Rate Work?

Many homebuyers worry that lenders can just arbitrarily raise their rates. I always reassure them that the math is strictly regulated by your contract.

Once your introductory period ends, we determine your new bill using a very specific formula: Index + Margin = Fully Indexed Rate.

- The Index: This is a public financial benchmark reflecting the current US economy. Today, the industry standard is the 30-day average Secured Overnight Financing Rate (SOFR), which fluctuates with market conditions and changes over time.

- The Margin: This is the lenders fixed profit percentage, agreed upon when you sign your closing documents. It never changes.

If your margin is 2.75% and the SOFR index hits 3.60%, your new mortgage interest rate becomes 6.35%. It is entirely transparent.

What are ARM Rate Caps?

The biggest fear my clients have is "payment shock", waking up to an unaffordable mortgage bill. Thankfully, variable loans feature strict consumer protections called caps, which act as a ceiling for your rate.

We usually format these as three numbers on your paperwork, like 5/2/5.

- Initial Cap (The first 5): Your rate cannot jump by more than 5% during the very first adjustment.

- Periodic Cap (The 2): On any subsequent adjustment date, the rate can never increase by more than 2% at a time.

- Lifetime Cap (The final 5): Over the entire 30-year lifespan of the debt, your interest will never exceed 5% above your original teaser rate.

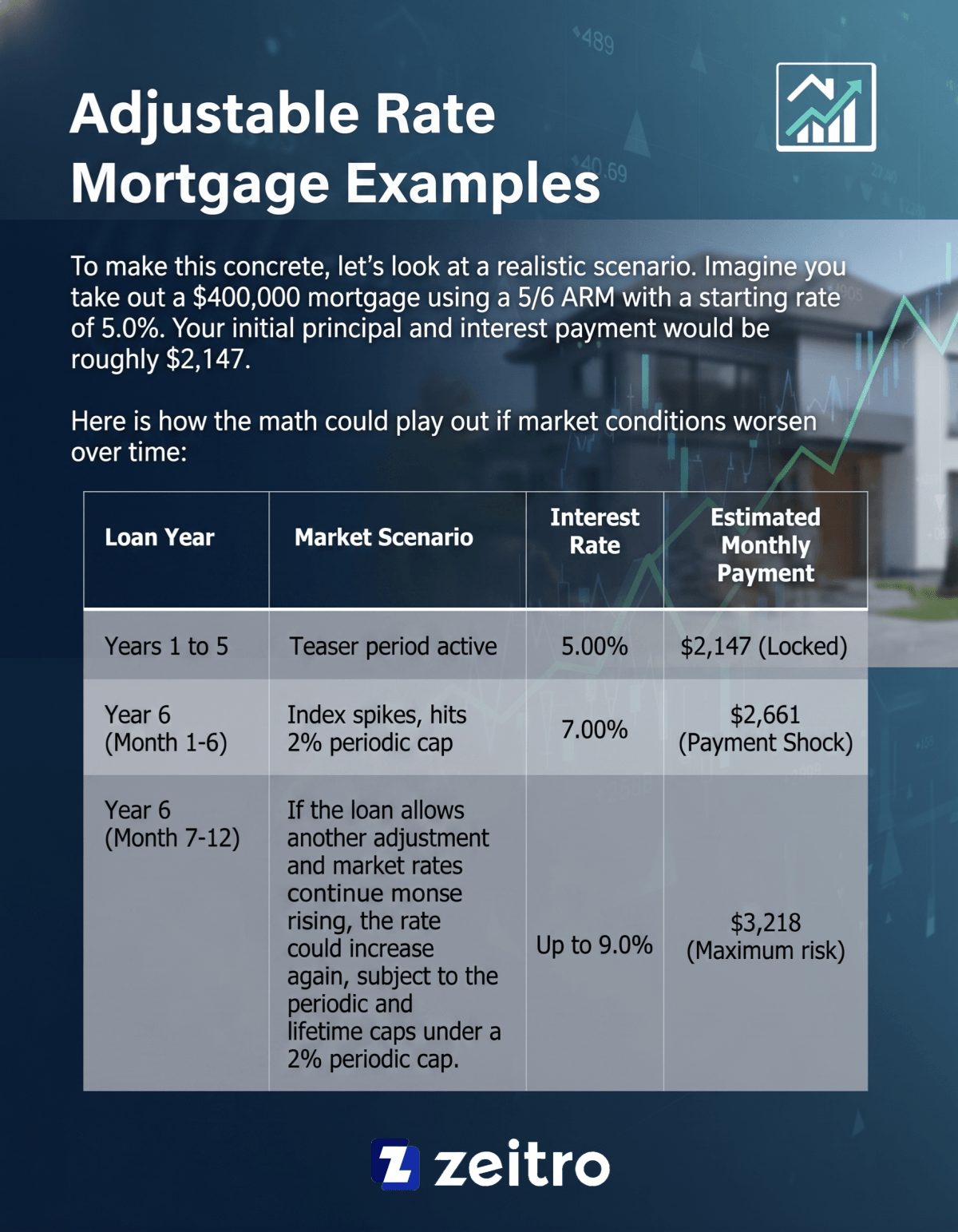

Adjustable Rate Mortgage Examples

To make this concrete, lets look at a realistic scenario. Imagine you take out a $400,000 mortgage using a 5/6 ARM with a starting rate of 5.0%. Your initial principal and interest payment would be roughly $2,147.

Here is how the math could play out if the market gets worse:

As you can see, by the end of year six, your housing cost could increase by over $1,000. This stark contrast highlights why having a solid exit strategy is absolutely crucial.

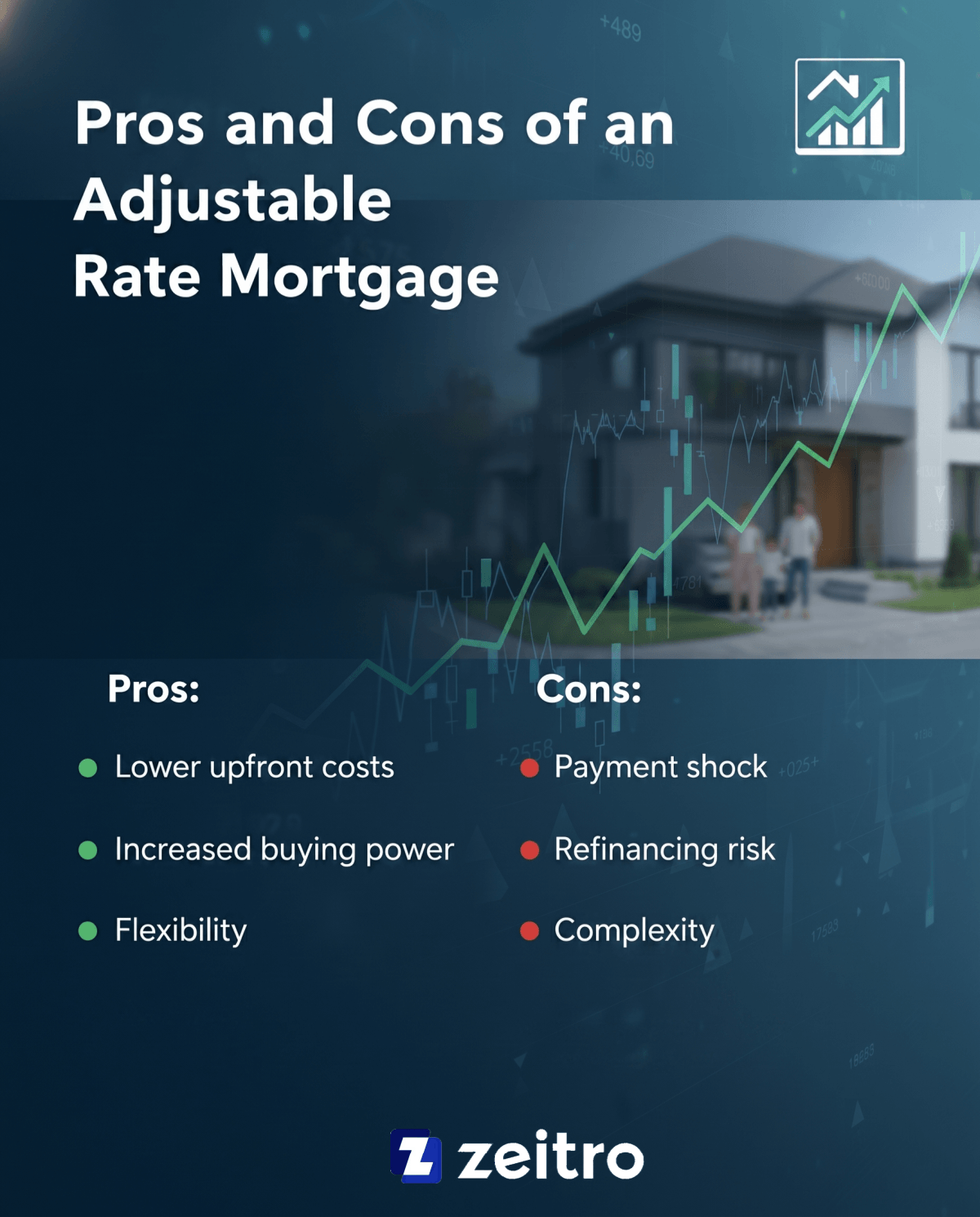

Pros and Cons of an Adjustable Rate Mortgage

As a mortgage professional, I never push a client into an ARM unless they fully understand both sides of the coin. Its a fantastic financial lever, but it's not without its dangers.

Pros:

- Lower upfront costs: You secure a cheaper rate than standard 30-year fixed options, saving thousands during the initial phase.

- Increased buying power: Lower initial payments mean you might qualify for a slightly more expensive home right now.

- Flexibility: Its a brilliant short-term hack if you plan to move quickly or expect a massive boost in your salary down the road.

Cons:

- Payment shock: The possibility of drastic monthly bill increases once the floating period begins.

- Refinancing risk: If your property value drops, you might not be able to refinance out of the loan before the rate adjusts.

- Complexity: The contracts are filled with index margins and cap structures that can be somewhat confusing to manage.

Who are Adjustable-rate Mortgages Best for?

So, when do I actively recommend this route to my borrowers? Generally, I suggest variable financing if you fit into one of these specific profiles:

- Short-term homeowners: If you are buying a "starter home" and know for a fact youll upgrade and sell within five to seven years.

- Future refinancers: Buyers who expect national interest rates to drop soon and plan to refinance into a fixed mortgage before their teaser period ends.

- Aggressive savers: Clients who intend to put extra cash toward their principal every month to pay off the debt early.

- High-trajectory earners: Medical residents or young professionals who reasonably expect significant income growth by the time higher payments begin.

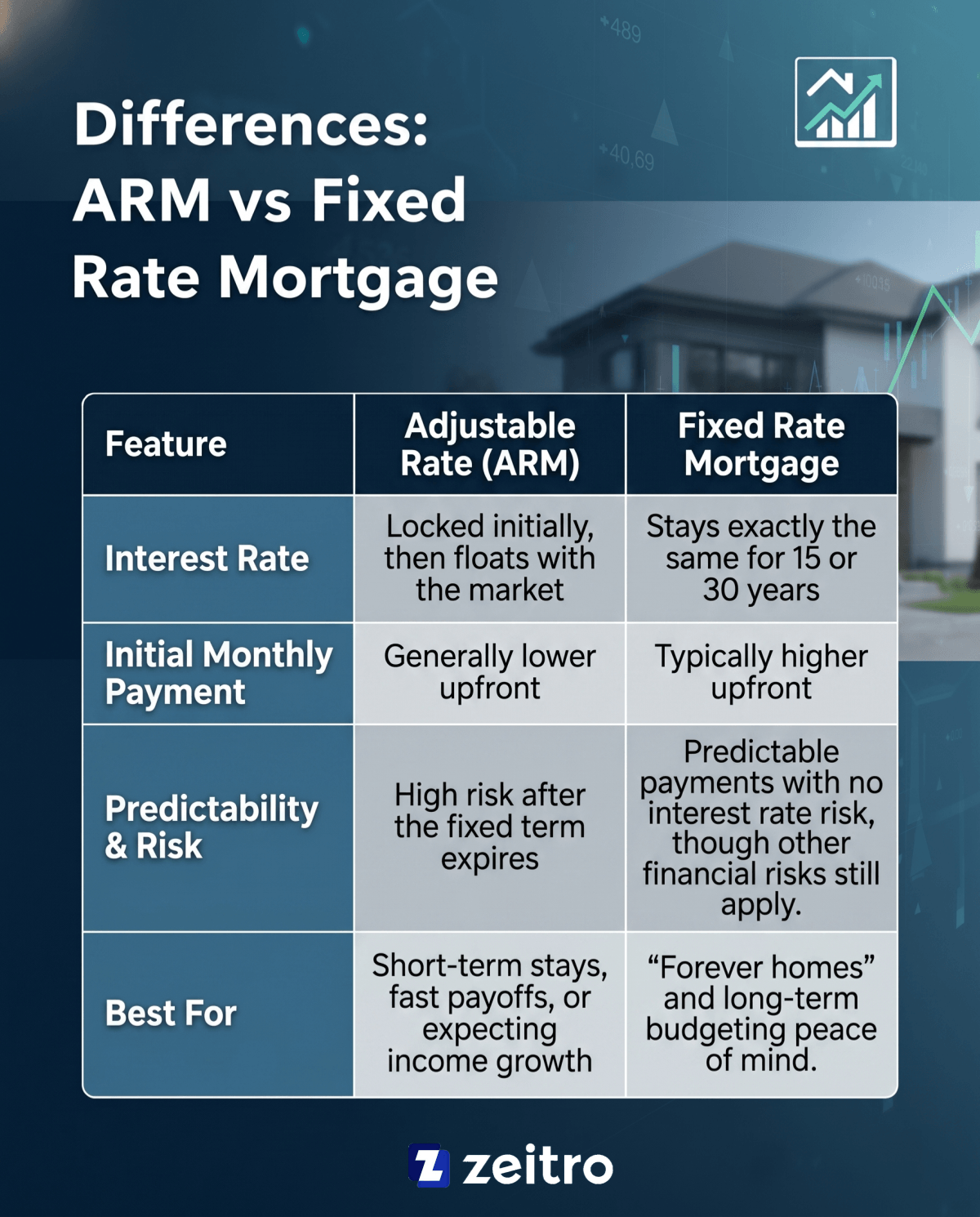

Differences: ARM vs Fixed Rate Mortgage

Making the final call between variable and fixed financing usually comes down to your personal risk tolerance. I created this simple comparison to help my buyers weigh their options quickly:

There is no universally "better" choice here. It entirely depends on your timeline and how well you sleep at night knowing your payment could shift.

FAQs About Adjustable Rate Mortgages

Q1. What are the downsides of an adjustable-rate mortgage?

The biggest drawback is unpredictability. Once your introductory period finishes, a high-rate environment can trigger "payment shock." If you aren't prepared for your monthly housing bill to potentially increase by hundreds of dollars, this financial product can put immense strain on your budget.

Q2. How to read ARM labels?

Loan labels use two numbers, like a "5/6 ARM." The first number (5) means your introductory interest rate is locked for five years. The second number (6) means that after those five years, your rate will adjust every six months based on current market indices.

Q3. Can I refinance an ARM into a fixed-rate mortgage?

Yes, absolutely. I frequently help clients use an ARM for the initial savings, then refinance them into a stable fixed-rate loan before their first adjustment hits. Just remember that refinancing requires a new appraisal and closing costs, so you need enough home equity to qualify.

Q4. Are ARM loans harder to qualify for than fixed-rate loans?

Yes, in many cases. Lenders won't just look at whether you can afford the cheap teaser rate. We underwrite your file using the fully indexed rate, the highest possible payment after adjustments, to ensure your debt-to-income ratio can handle a worst-case scenario.

Q5. What happens when my ARM adjusts?

You won't be caught completely off guard. Your lender will mail you a written notice weeks before the adjustment date. Your new rate is calculated by adding your contract's Margin to the current public Index, strictly limited by your established rate caps.

Conclusion

At the end of the day, an Adjustable Rate Mortgage is essentially trading future uncertainty for immediate financial relief. Its a highly strategic move that works beautifully for the right person, but it can be devastating if you don't have a solid exit plan.

Before signing anything, I strongly encourage you to run some numbers through a mortgage calculator to see your worst-case scenarios. Better yet, sit down with a local, trusted loan officer who can evaluate your unique income trajectory and timeline. With the right guidance, you can use these tools to confidently build your wealth.

People Also Read

- 10 First-Time Home Buyer Tips: What to Know

- Ultimate Guide: How to Buy a House for the First Time?

- Best First-Time Home Buyer Programs: Get the Right Choice

- Ultimate Guide: How to Calculate Monthly Mortgage Payment?

- Must-Read Tips for Paying Off Mortgage Early in 2026

- Make Extra Payments on Mortgage: Is It Worth It?

Also Try Tools:

- Zeitro Mortgage Affordability Calculator Free and Online

- Zeitro Mortgage Payment Calculator with Interest & Taxes

![[Solved] Can I Use K-1 Income to Qualify a Borrower?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a44cb55129383ad19f46080_can-i-use-k-1-income-to-qualify-a-borrower-banner.png)