Written by

Eric

Share this article

.svg)

Subscribe to updates

I've seen countless clients sit across my desk, totally overwhelmed by loan options. I completely get it. If there's one thing most homebuyers crave, it's peace of mind, and that's exactly what a fixed-rate mortgage delivers.

As a loan officer, I often recommend this straightforward product because it locks in your interest rate, giving you a high level of financial predictability for decades. In this guide, I'll break down exactly what a fixed-rate mortgage is, its pros and cons, and answer the most common questions I hear from borrowers every day.

Key Takeaways

- Total Predictability: Your interest rate and principal-and-interest payment stay exactly the same for the entire life of the loan.

- Best for Long-Term Buyers: It is often a good choice if you plan to stay in your home long enough to benefit from long-term stability, commonly estimated at around 5–10 years, depending on market conditions.

- ARMs vs. Fixed: Unlike Adjustable-Rate Mortgages (ARMs), you are protected from future interest rate hikes.

- Budgeting Made Easy: Knowing your core housing cost never changes makes long-term financial planning much simpler.

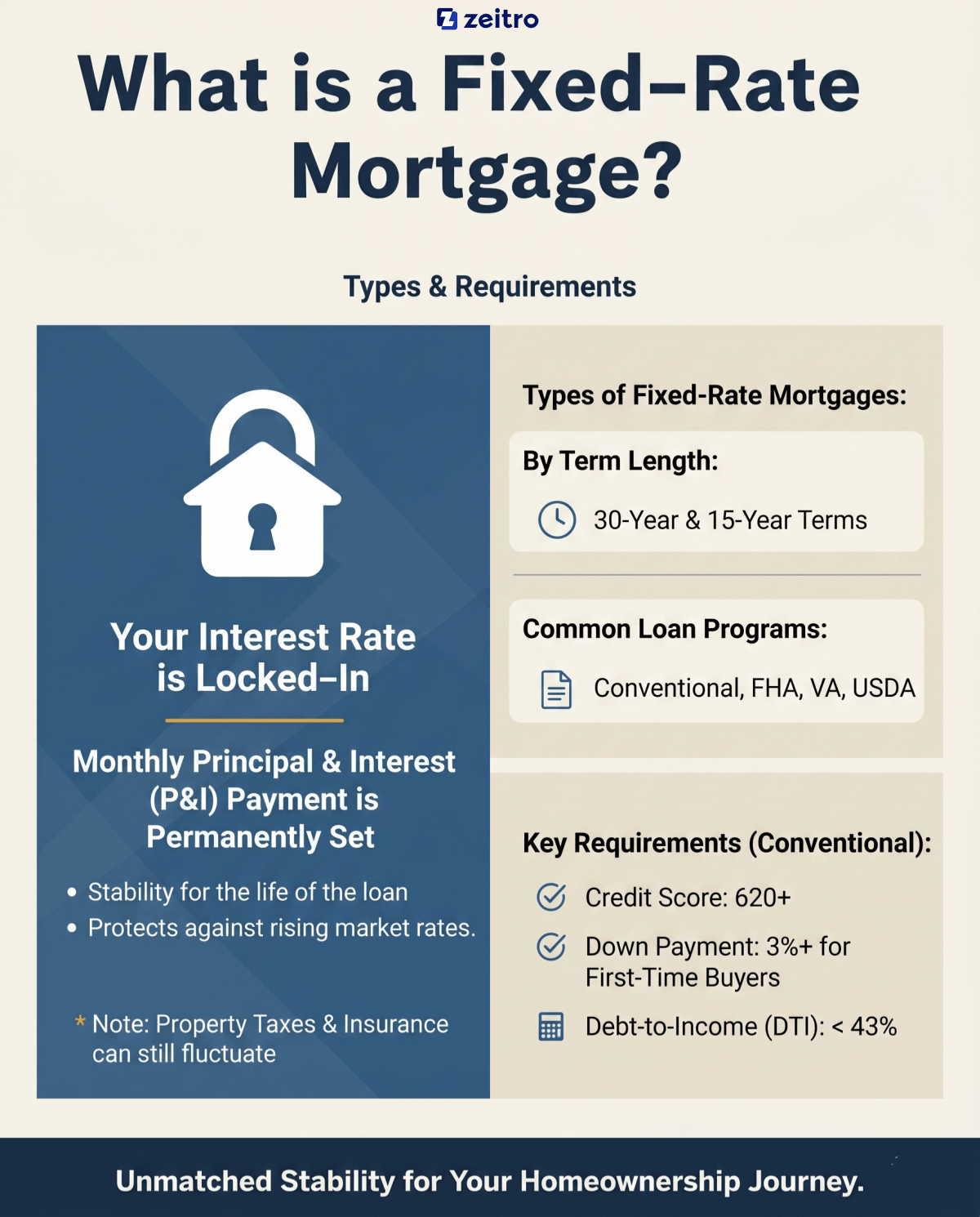

What is a Fixed-Rate Mortgage?

A fixed-rate mortgage is exactly what it sounds like: a home loan where your interest rate remains locked from the day you close until the day you pay it off.

Whether the broader economy crashes or market rates skyrocket to 10%, your rate won't budge. This fixed interest rate means your monthly principal and interest payment is permanently set. When I explain this to first-time buyers, I can literally see their shoulders drop with relief.

However, it's crucial to understand that while the lender guarantees your P&I won't change, your total monthly housing expense might still fluctuate. Why? Because property taxes and homeowners insurance, which are typically rolled into your monthly payment, can and often do increase over time. Still, locking in the core cost of your home for the life of the loan provides unmatched stability.

Types of Fixed-Rate Mortgages

Fixed-rate mortgages aren't one-size-fits-all. They come in several different shapes and sizes to fit your specific financial goals.

- By Term Length: The most popular options are 30-year and 15-year terms, though 10-year and 20-year options exist. The 30-year gives you the lowest monthly payment, while the 15-year saves you a ton on interest.

- Conventional Loans: The standard mortgage not backed by the government. It's the most common choice I see.

- FHA Loans: Government-backed loans perfect for buyers with lower credit scores.

- VA Loans: Exclusive, zero-down-payment loans for veterans and active military.

- USDA Loans: Designed for rural and suburban homebuyers meeting specific income limits.

The 30-year conventional fixed-rate mortgage is by far the crowd favorite, but we can always tailor the type to your unique situation.

Requirements of Fixed-Rate Mortgages

Every loan program has its own rulebook, but generally, to get approved for a fixed-rate mortgage in today's US market, you'll need to meet these baselines:

- Credit Score: For a conventional loan, you'll need a minimum score of 620. However, to snag the best interest rates, I always advise my clients to aim for 740 or higher. (FHA loans can sometimes accept scores down to 500-580).

- Down Payment: Gone are the days of needing 20% down! First-time buyers can often qualify with just 3% down on conventional loans, or 3.5% for FHA.

- Debt-to-Income (DTI) Ratio: This compares your monthly debt payments to your gross income. We typically look for a DTI below 43%, though some automated underwriting systems might approve up to 50% with strong compensating factors.

These are general guidelines. Your specific requirements will depend on the lender and loan type.

How Does a Fixed-Rate Mortgage Work?

Understanding how your payments work behind the scenes is crucial. Here is how your fixed-rate loan actually operates over time:

- The Amortization Schedule: This is a banking term for how your loan is paid off. Your fixed monthly payment is split between paying down the principal (the loan balance) and the interest (the lender's fee).

- Early Years: In the beginning, the vast majority of your monthly payment goes toward interest. Only a small fraction chips away at the principal.

- Later Years: As the years roll on, the balance shifts. You start paying much more toward the principal and less toward interest.

- Consistent Total: Even though the ratio of principal to interest changes every single month, your total P&I payment remains exactly the same.

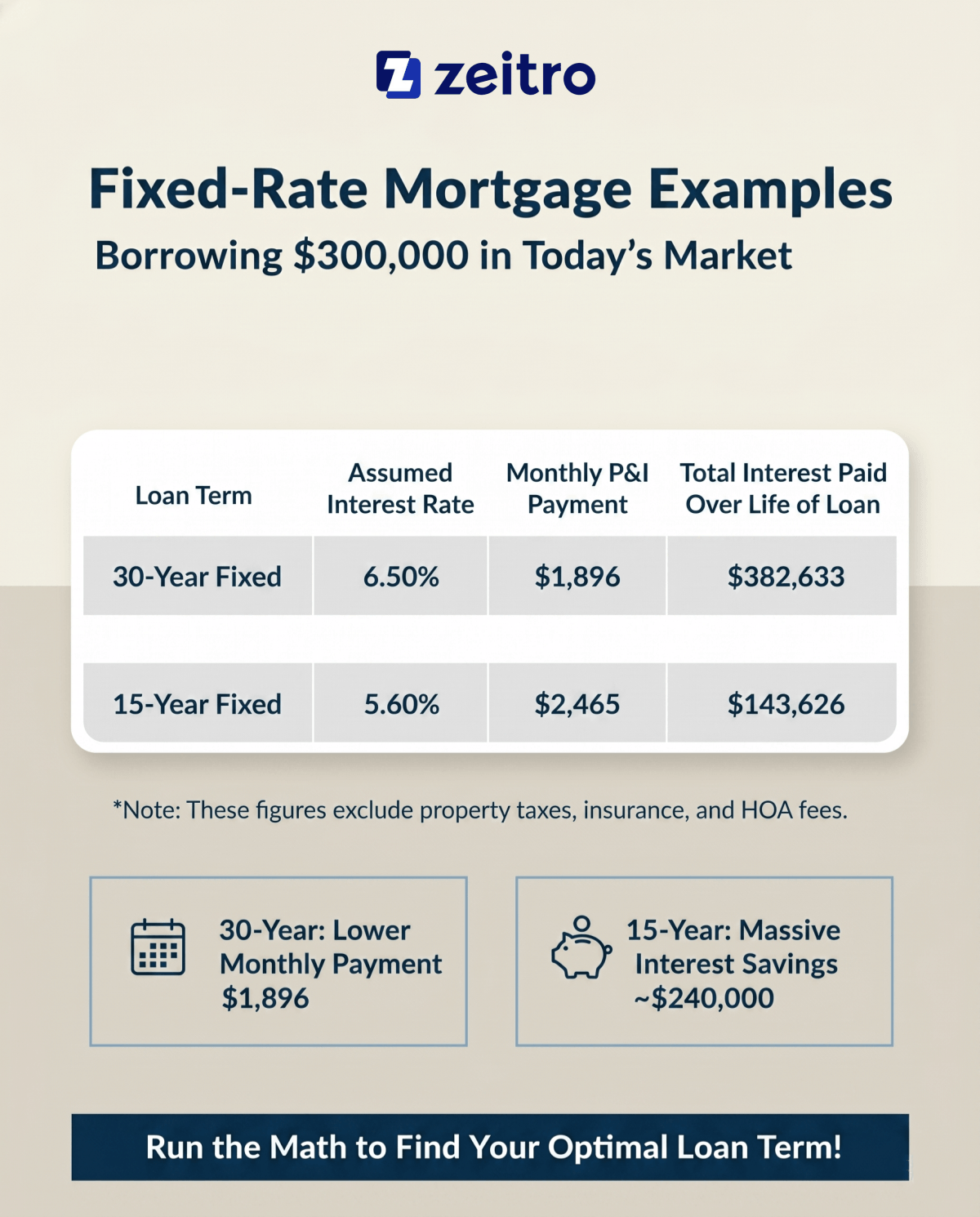

Fixed-Rate Mortgage Examples

To give you a real-world perspective, let's look at a typical scenario I might run for a client right now. Let's assume you are borrowing $300,000 to buy a home in the current market.

Here is how the numbers shake out depending on the term you choose, using hypothetical interest rates for illustration purposes:

Note: These figures exclude property taxes, insurance, and HOA fees.

As you can see, the 30-year gives you a much more manageable monthly payment of $1,896. However, the 15-year option, despite costing roughly $569 more per month, saves you nearly $240,000 in total interest! This is why running the math is so critical.

Also Read:

- Ultimate Guide: How to Calculate Monthly Mortgage Payment?

- How to Calculate Mortgage Interest: Manually & Automatically

- How to Calculate Employment Income for a Mortgage?

Pros and Cons of a Fixed-Rate Mortgage

No mortgage is perfect. As a loan officer, I believe in absolute transparency. Here is the balanced truth about fixed-rate loans:

Pros:

- Budget Predictability: You'll never lose sleep over rising interest rates. Your principal and interest payments are shielded from inflation, though other housing costs may still rise.

- Simple to Understand: There are no confusing adjustment periods or index margins to track.

- Long-Term Security: It's the safest vehicle for building equity over decades without payment shocks.

Cons:

- Higher Initial Rates: Fixed rates typically start out slightly higher than the initial introductory rates offered on ARMs.

- Refinancing Costs: If market rates drop significantly, your rate won't automatically adjust down. You have to actively refinance, which involves paying closing costs again.

- Stricter Qualification: Because the rate is higher than an ARM's starting rate, it pushes your DTI up, meaning you might qualify for a slightly smaller maximum loan amount.

When to Get a Fixed-Rate Mortgage?

So, when do I actually tell a borrower to pull the trigger on a fixed rate? Usually, it comes down to these three scenarios:

- You're Planting Roots: If you plan to live in the home for more than 7 to 10 years, a fixed rate is almost always the winner. You mitigate long-term risk.

- You're Risk-Averse: If the thought of your mortgage payment randomly increasing by $400 a month in the future makes your stomach drop, secure a fixed rate. "Sleep equity" is real.

- Rates are Historically Favorable: When the overall market dips, locking in a low fixed rate for three decades is one of the smartest financial moves you can make.

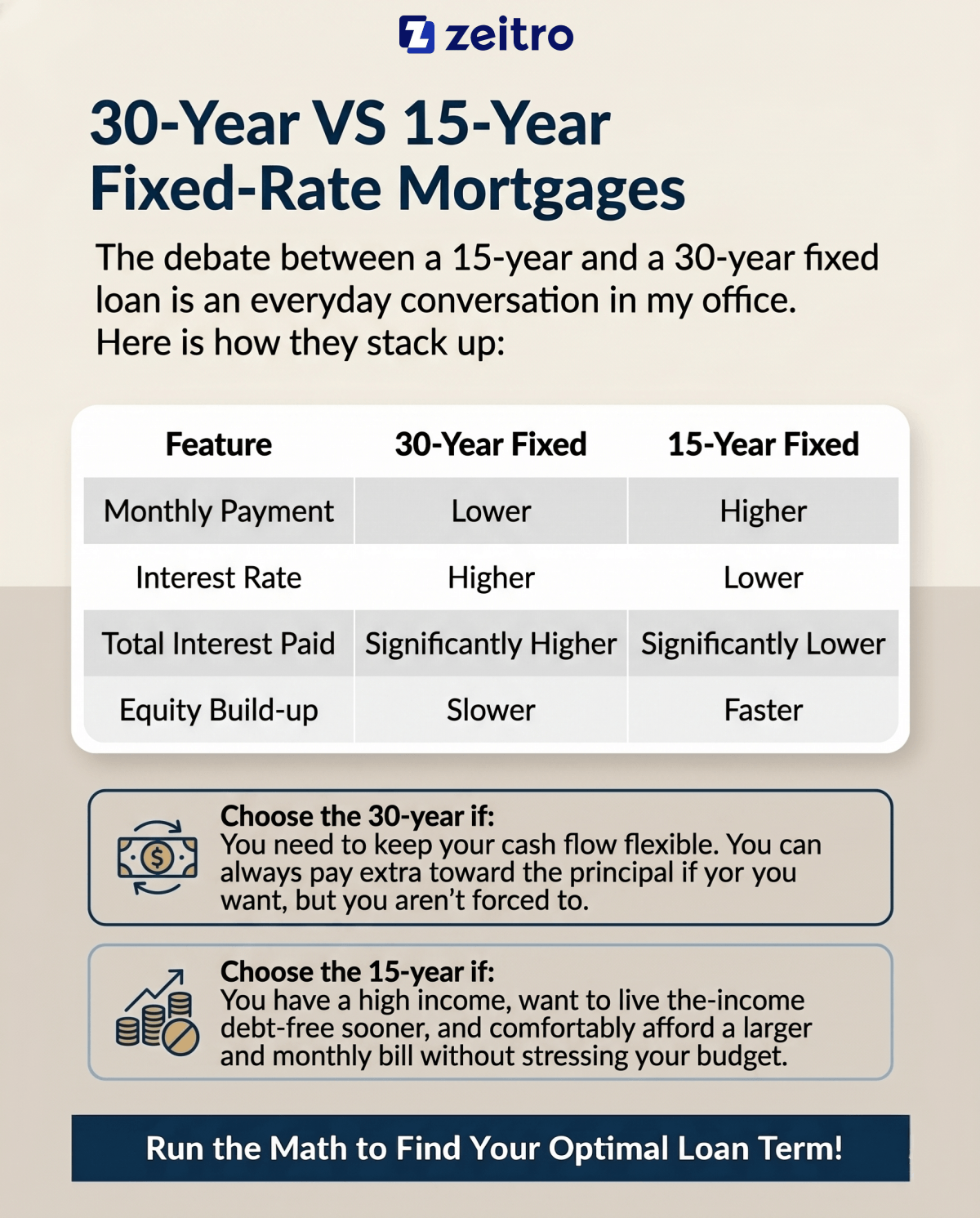

30-Year VS 15-Year Fixed-Rate Mortgages

The debate between a 15-year and a 30-year fixed loan is an everyday conversation in my office. Here is how they stack up:

- Choose the 30-year if: You need to keep your cash flow flexible. You can always pay extra toward the principal if you want, but you aren't forced to.

- Choose the 15-year if: You have a high income, want to live debt-free sooner, and comfortably afford a larger monthly bill without stressing your budget.

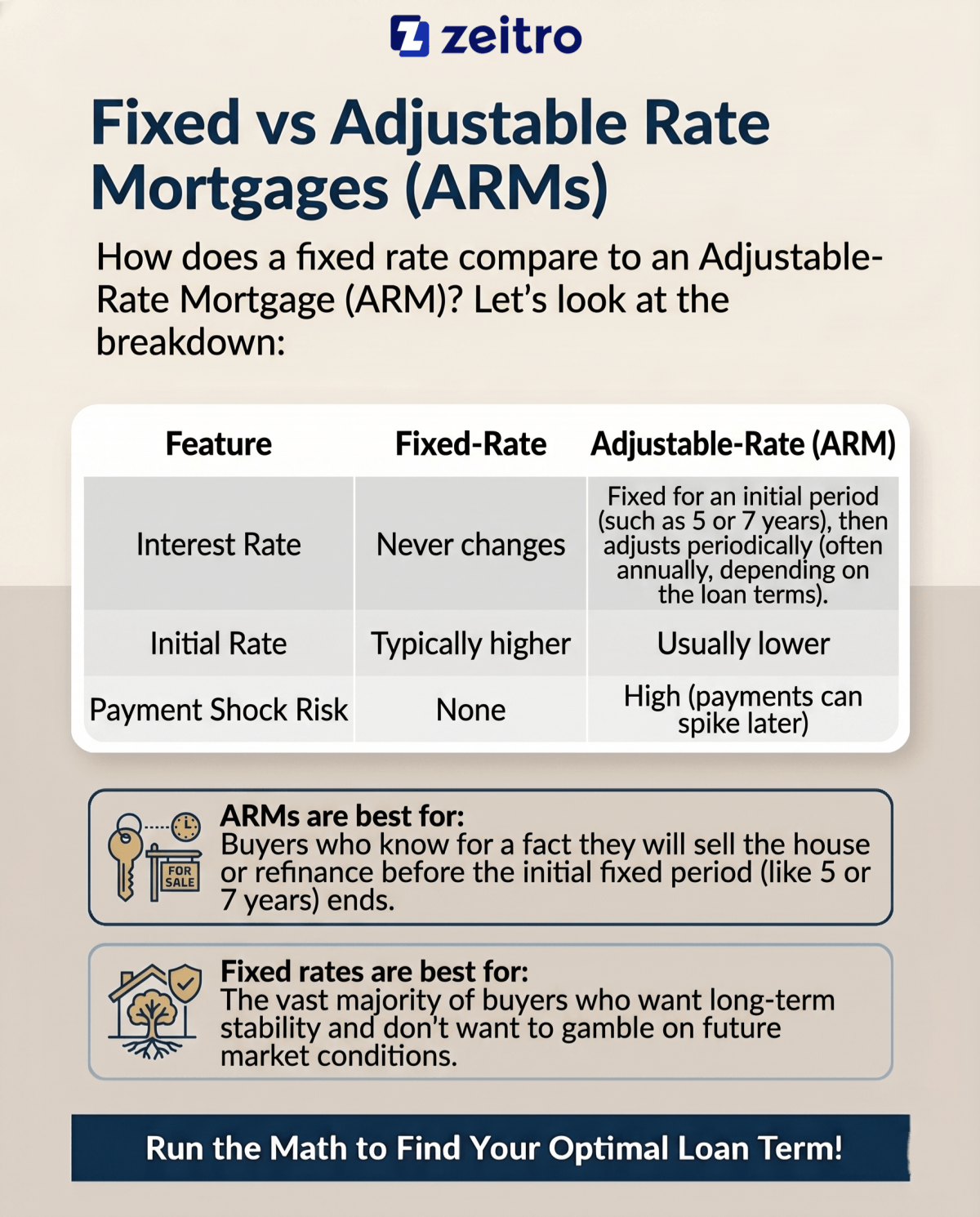

Fixed vs Adjustable Rate Mortgages (ARMs)

How does a fixed rate compare to an Adjustable-Rate Mortgage (ARM)? Let's look at the breakdown:

- ARMs are best for: Buyers who know for a fact they will sell the house or refinance before the initial fixed period (like 5 or 7 years) ends.

- Fixed rates are best for: The vast majority of buyers who want long-term stability and don't want to gamble on future market conditions.

FAQs About Fixed-Rate Mortgages

Q1. Can you refinance a fixed-rate mortgage?

Yes, absolutely. If the market cools down and interest rates drop below your current locked rate, you can refinance to a new, lower fixed-rate loan. Just remember that refinancing involves paying closing costs again, so you'll need to run a break-even analysis.

Q2. Can my monthly payment change on a fixed-rate mortgage?

Yes. While your actual loan principal and interest are permanently locked, your property taxes and homeowners' insurance, which sit in your Escrow account, adjust annually. If local tax assessments rise, your total monthly output will increase accordingly.

Q3. Is it better to pay off a fixed-rate mortgage early?

It depends. Paying it off early saves a massive amount in interest. However, you must weigh the "opportunity cost." If your mortgage rate is 4% but you can earn 8% investing that extra cash, investing is mathematically smarter. Also, check for prepayment penalties.

Q4. How is the fixed interest rate determined?

Your specific rate is a mix of macroeconomic factors, like the 10-year Treasury yield, and your personal financial profile. While I can't control the bond market, your credit score, down payment size, and loan type directly dictate how good a rate we can offer you.

Q5. Are fixed-rate mortgages assumable?

Usually, conventional loans are not assumable. However, government-backed fixed-rate loans, like FHA, VA, and USDA mortgages, often are. This means a qualified buyer can actually take over your remaining loan balance at your original low interest rate when you sell!

Conclusion

As a loan officer, I've navigated just about every market cycle, and the fixed-rate mortgage remains the ultimate tool for financial stability. It takes the guesswork out of homeownership, allowing you to budget with absolute confidence while building equity over time. Whether you opt for a 30-year term to maximize your monthly cash flow or a 15-year term to crush your debt early, locking in your rate is a powerful strategy.

Because everyone's financial fingerprint is unique, there is no universal right answer. I highly recommend chatting with a local, licensed mortgage professional to run a personalized cost analysis for your situation. Ready to see what you qualify for? Reach out to your loan officer today to get started.

People Also Read

- Ultimate Guide to Biweekly Mortgage Payments: Is It Worth It?

- Make Extra Payments on Mortgage: Is It Worth It?

- Average PMI Cost: How Much Does it Cost?

- [Guide] How to Calculate DTI Ratio for Mortgage?

![[Solved] Can I Use K-1 Income to Qualify a Borrower?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a44cb55129383ad19f46080_can-i-use-k-1-income-to-qualify-a-borrower-banner.png)