![[Solved] How Much Will My Monthly Payment Be?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a0a8b1f89bcb9d995d94157_how-much-will-my-monthly-payment-be-banner.png)

Written by

Eric

Share this article

.svg)

Subscribe to updates

I remember the exact moment I started house hunting: I fell in love with a place, looked at the sticker price, and immediately panicked. Guessing your actual budget can be incredibly stressful. You might think your monthly mortgage payment is just repaying the bank, but hidden costs often catch first-time buyers off guard.

I've been there, staring blankly at confusing math. Let me reassure you that you don't need a finance degree to figure this out. In this guide, I'll break down exactly what goes into your monthly bill and show you how to calculate every penny without the headache.

Key Takeaway

- Your monthly mortgage isn't just principal and interest. It includes taxes and insurance (known as PITI).

- Manual calculations are prone to math errors and usually ignore essential fees.

- Using a comprehensive online calculator is the fastest, most accurate way to budget.

- Strategies like extra down payments or biweekly payments significantly lower your costs.

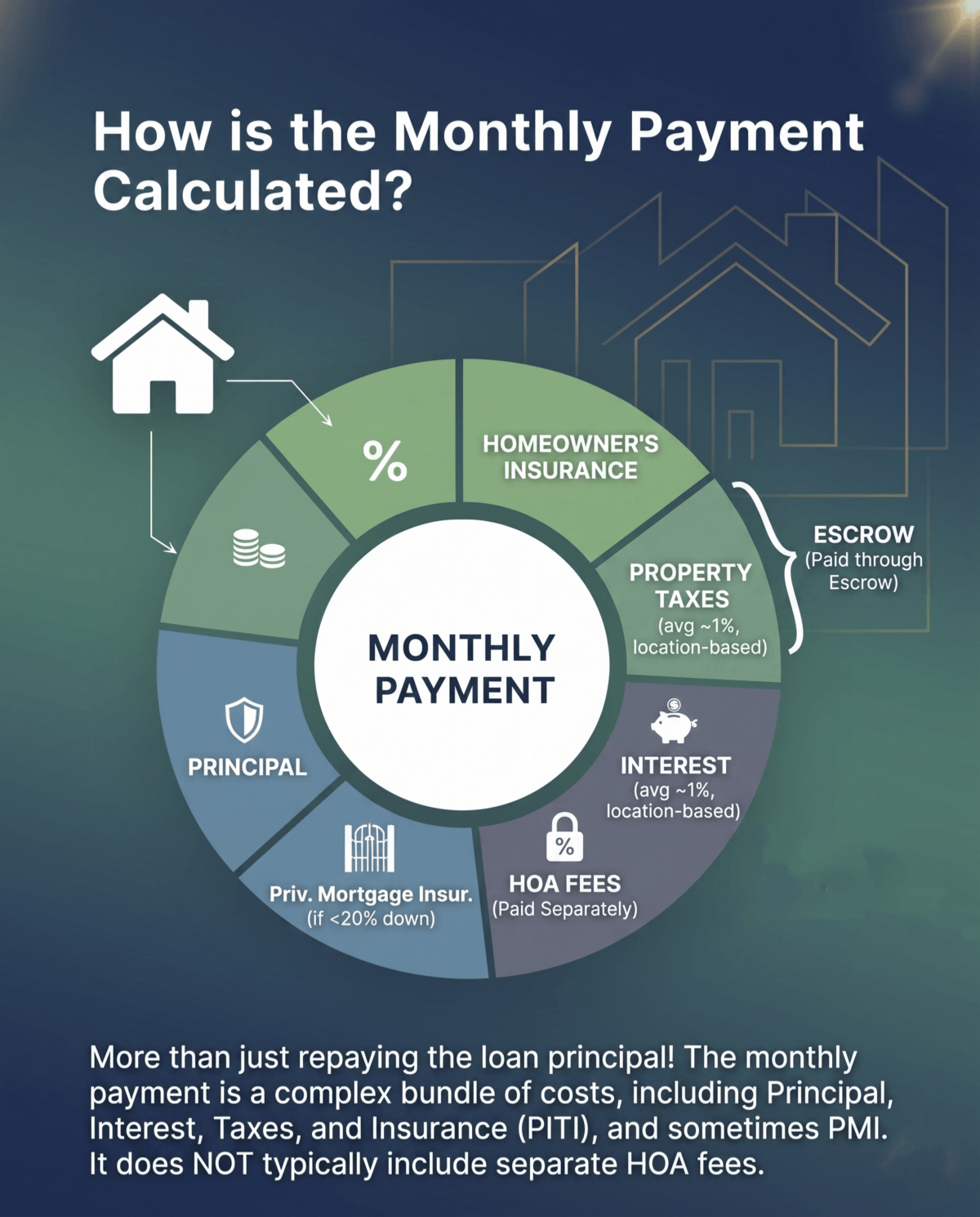

How is the Monthly Payment Calculated?

When I bought my first home, I quickly learned that your monthly payment is much more than just handing money back to the lender. It's actually a bundle of different costs wrapped into one check. Here is the industry terminology you need to know:

- Principal: The original loan amount you borrowed to buy the house.

- Interest: The fee the lender charges you for borrowing their money (averaging around 6.5% for a 30-year fixed rate in 2026).

- Property Taxes: Local taxes that vary by state and county and are often collected through an escrow account. The effective rate nationwide is roughly around 1%, depending on location.

- Homeowner's Insurance: Mandatory protection against damage to your property.

- PMI (Private Mortgage Insurance): A lender-required fee if your down payment is under 20%.

- HOA Fees: Homeowners association dues, if applicable. They are usually paid separately and are not typically included in your mortgage payment.

Also Read:

- How to Calculate Mortgage Interest: Manually & Automatically

- When Does PMI Go Away? How to Get PMI Removed?

- How to Calculate PMI? Do the Math On Your Own

- [Solved] How Much Interest Will I Pay on My Mortgage?

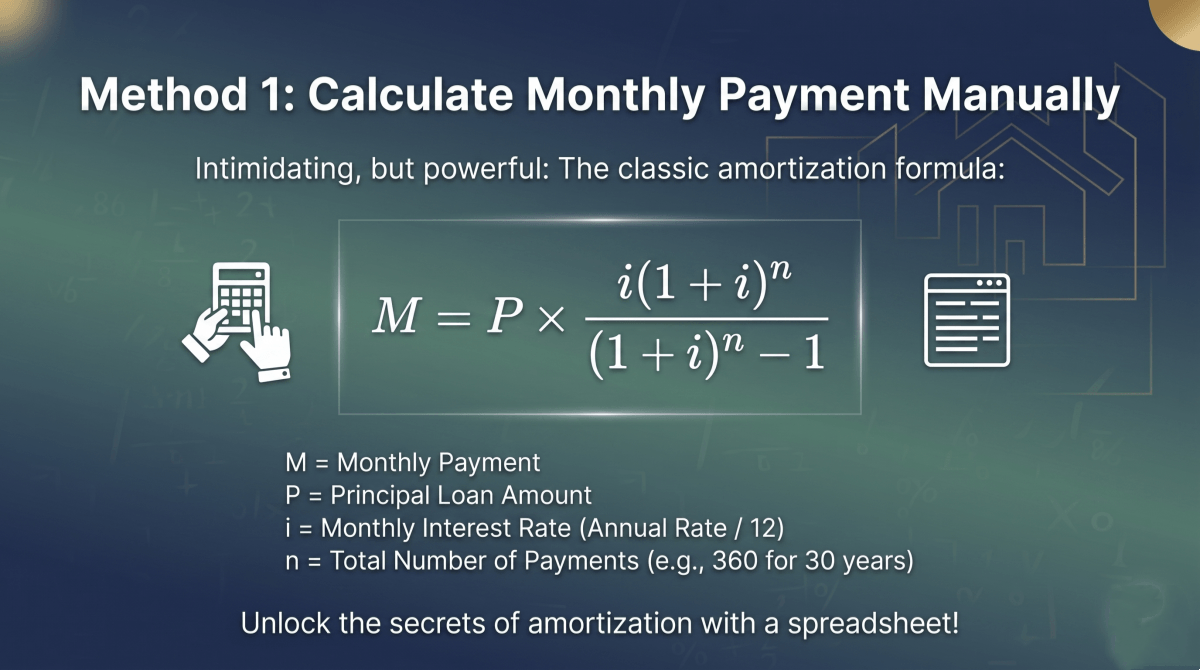

Method 1: Calculate Monthly Payment Manually

If you're a math nerd who loves spreadsheets, you can absolutely calculate your base mortgage by hand. The industry-standard formula looks intimidating, but here it is: M=P×i(1+i)^n/(1+i)^n-1

Let me translate that for you: M is your monthly payment, P stands for the principal loan amount, i is your monthly interest rate (your annual rate divided by 12), and n represents the total number of payments (360 months for a standard 30-year loan).

Pros:

- Helps you deeply understand the mathematical logic behind your debt.

- Requires no internet connection—just a piece of paper and a calculator.

Cons:

- The formula is incredibly complex, making math errors highly likely.

- It only calculates principal and interest, so it will underestimate your total monthly housing cost if you also need to pay taxes, homeowners insurance, or mortgage insurance.

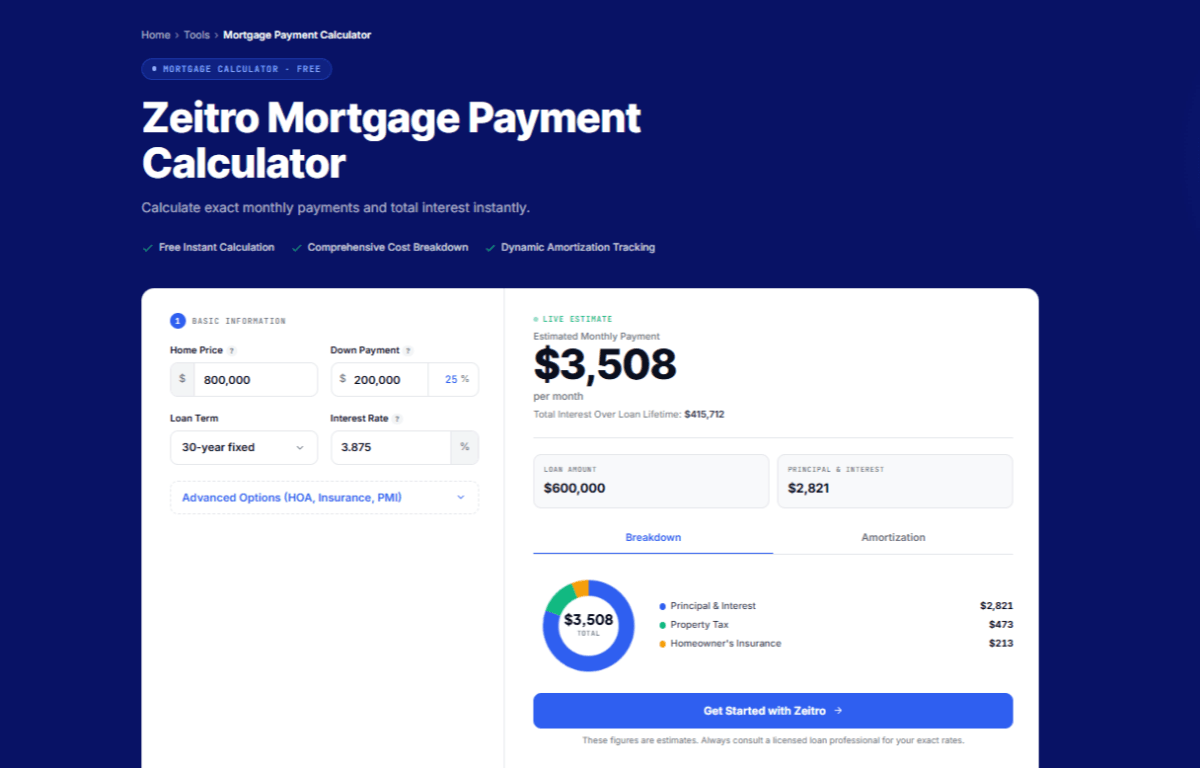

Method 2: Use an Online Mortgage Payment Calculator

Since doing the math manually completely ignores taxes and insurance, I highly recommend saving yourself the headache. The best alternative is using a robust tool like the Zeitro Mortgage Calculator.

Here's how it works: You input your home price, down payment (as a dollar amount or percentage), loan term, and interest rate. To get ultra-accurate, use the advanced options to plug in HOA fees, homeowner's insurance, and state property tax rates. Instantly, the tool outputs your estimated monthly payment, total lifetime interest, and an interactive amortization breakdown showing exactly where your money goes each year.

Pros:

- 100% free and delivers instant, visual results.

- Includes taxes and insurance for a realistic budget.

- Lets you easily test different down payment scenarios.

Cons:

- The results are strictly estimates. You still need to consult a licensed loan officer to lock in your actual, personalized interest rate.

Tips to Pay Off Your Mortgage Quicker

Once you've figured out your monthly payment, you might get a little sticker shock seeing the total interest over 30 years. Fortunately, if you want to shorten your loan term and save thousands, you can take control with a few strategic moves.

Here are my favorite strategies:

- Make extra principal-only payments: Even an extra $50 a month applied directly to the principal shaves years off your debt.

- Switch to biweekly payments: By paying half your monthly bill every two weeks, you naturally make one extra full payment each year.

- Throw windfalls at the debt: Direct your tax refunds, work bonuses, or inheritance straight into your mortgage.

- Request a mortgage recast: If you make a large lump-sum principal payment, you may be able to request a mortgage recast, but eligibility depends on your lender and loan type.

Also Read:

- Must-Read Tips for Paying Off Mortgage Early in 2026

- Ultimate Guide to Biweekly Mortgage Payments: Is It Worth It?

- 10 First-Time Home Buyer Tips: What to Know in 2026

FAQs About How Much Will My Monthly Payment Be

Q1. Does my monthly mortgage payment include property taxes and insurance?

Typically, yes. If you set up an escrow account, your lender conveniently bundles your principal, interest, taxes, and insurance (PITI) into one single monthly payment.

Q2. How much down payment do I need to lower my monthly payment?

The larger your down payment, the less money you borrow, which directly lowers your monthly bill. Plus, hitting the magical 20% mark eliminates costly PMI fees, saving you even more.

Q3. Why did my estimated monthly payment go up?

If you have a fixed-rate loan, your principal and interest never change. Increases are almost always due to rising property taxes or a hike in your homeowner's insurance premiums. If you have an ARM (adjustable-rate mortgage), your interest rate likely reset.

Q4. What is a mortgage amortization schedule?

Think of it as a detailed timeline of your debt. It clearly shows how much of your monthly check goes toward shrinking the principal balance versus paying off the interest over the life of the loan.

Q5. Is a 15-year or 30-year mortgage better for my monthly payment?

A 30-year term generally gives you a lower monthly payment, while a 15-year term usually requires a higher monthly payment but reduces total interest over time.

Final Word

Buying a house is one of the biggest milestones of your life, and understanding your numbers puts you in the driver's seat. Knowing how principal, interest, taxes, and insurance come together means you won't be blindsided when the first bill arrives in the mail.

Please, put down the pen and paper—don't let manual math stress you out. Take the guesswork out of your budget today by heading over to the Zeitro Mortgage Calculator. Visualize your future costs instantly and step into your homebuying journey with absolute confidence!

![[Solved] Can I Use K-1 Income to Qualify a Borrower?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a44cb55129383ad19f46080_can-i-use-k-1-income-to-qualify-a-borrower-banner.png)