Written by

Eric

Share this article

.svg)

Subscribe to updates

As a loan officer, I hear it every single week: "I just want this house paid off." That drive for debt-free peace of mind is totally understandable. But with 2026 mortgage rates shifting unpredictably, rushing to wire your bank extra cash isn't always the smartest move. Could prepaying save you thousands, or will it secretly drain your wealth? Let's dive into the real-world strategies and hidden traps.

Key Takeaways

- Target the principal: Extra payments only work if they hit the principal directly. Try biweekly schedules for an effortless boost.

- Watch for fees: Prepayment penalties are rare in modern U.S. mortgages due to federal regulations, but confirm your loan terms and read your loan agreement first.

- Do the math: Always compare your mortgage rate against what you could earn in today's stock market or high-yield savings accounts.

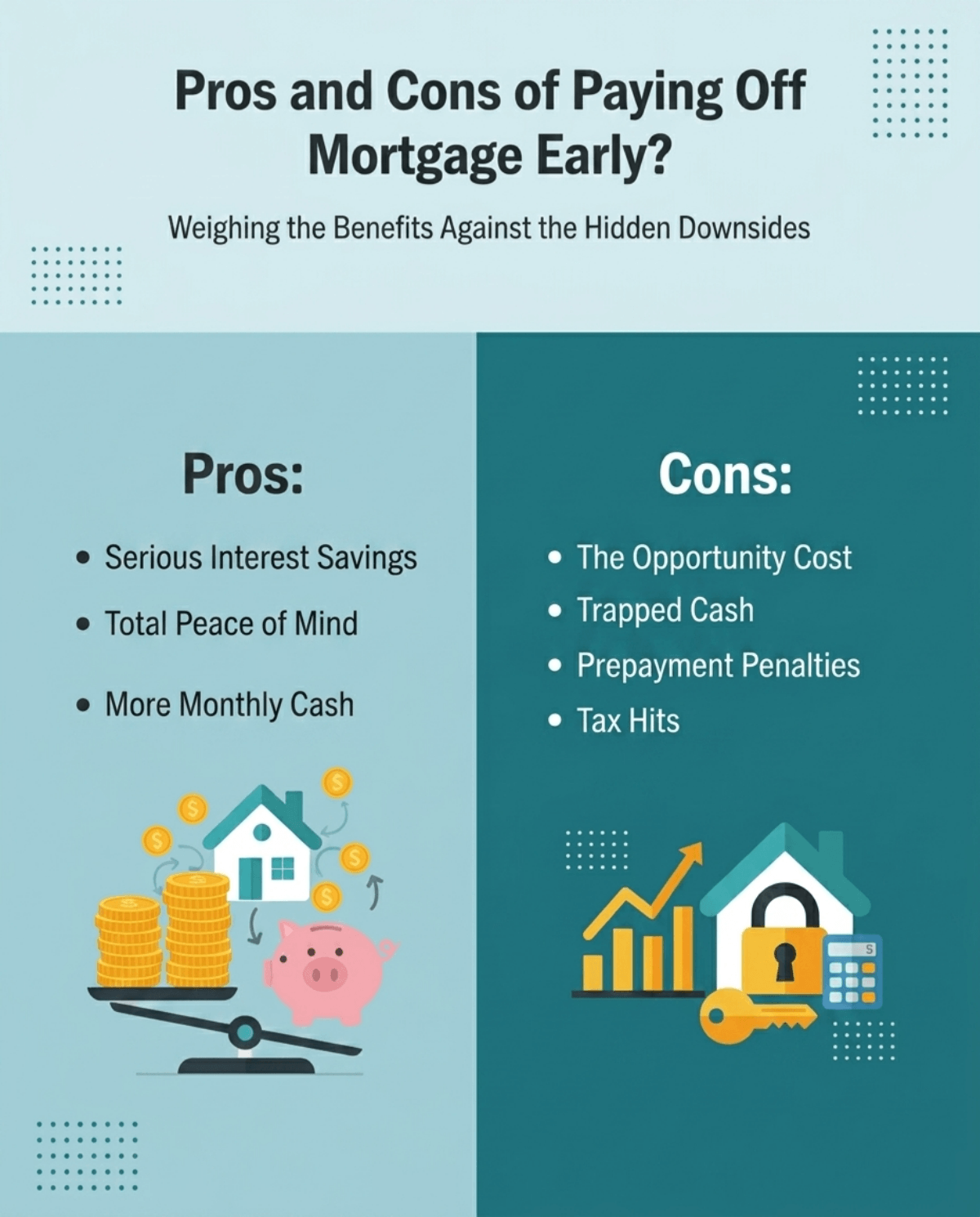

Pros and Cons of Paying Off Mortgage Early

Deciding to crush your home loan is a heavy financial move. Before you start writing bigger checks, you really have to weigh the actual benefits against the hidden downsides.

Pros:

- Serious Interest Savings: Knocking years off your timeline keeps thousands of dollars in your pocket instead of the bank's.

- Total Peace of Mind: Owning your home free and clear is the ultimate sleep-at-night insurance against job loss or a bad economy.

- More Monthly Cash: Losing that giant monthly payment permanently frees up serious money for travel or retirement.

Cons:

- The Opportunity Cost: This is huge. If you hold an old 3% rate but the market returns 8%, locking extra cash in your walls means missing out on real wealth growth.

- Trapped Cash (Reduced Liquidity): You can't easily buy groceries with home equity if a sudden emergency hits.

- Prepayment Penalties: These are uncommon today, limited by law to the first three years on qualified loans with strict caps.

- Tax Hits: Depending on your filings, you might lose your mortgage interest tax deduction.

[8 Tips] How to Pay Off a Mortgage Early?

If the numbers make sense for your life, you need a realistic game plan—not just good intentions. Over my years of advising buyers, I've found these eight strategies actually work.

- Make Extra Principal-Only Payments: Extra amounts beyond your regular payment are typically applied to principal, but specify 'principal-only' to ensure it. I've seen clients make this mistake way too often.

- Switch to Biweekly Payments: Pay half your normal amount every two weeks. Because the calendar has 52 weeks, you sneak in a whole extra month's payment each year without really feeling the pinch.

- Refinance to a Shorter Term: Trading a 30-year mortgage for a 15-year one forces your hand. Yes, the monthly bill goes up, but a lower rate combined with a much shorter timeline saves a fortune.

- Request a Mortgage Recast: Got a bonus or inheritance? Drop a lump sum on your loan and ask the bank to "recast" it. They'll recalculate a lower monthly payment based on the new balance, usually for a tiny fee.

- Throw Windfalls at the Debt: Stop treating tax refunds or work bonuses like lottery winnings. Send them straight to your lender.

- Round Up Your Payments: If you owe $1,830, just round it up to $2,000. It's a tiny budget tweak that quietly chips away at your timeline.

- Try "House Hacking": Rent out a basement, spare room, or garage. Funnel every dime of that rental income directly toward the house debt.

- Downsize Your Space: Sell your oversized place, take the built-up equity, and buy a smaller home in cash. Instant zero-mortgage lifestyle.

![[8 Tips] How to Pay Off a Mortgage Early?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a0574f718464102613dd21c_paying-off-mortgage-early-tips.png)

Also Try:

- Zeitro Mortgage Affordability Calculator Free and Online

- Zeitro Mortgage Payment Calculator with Interest & Taxes

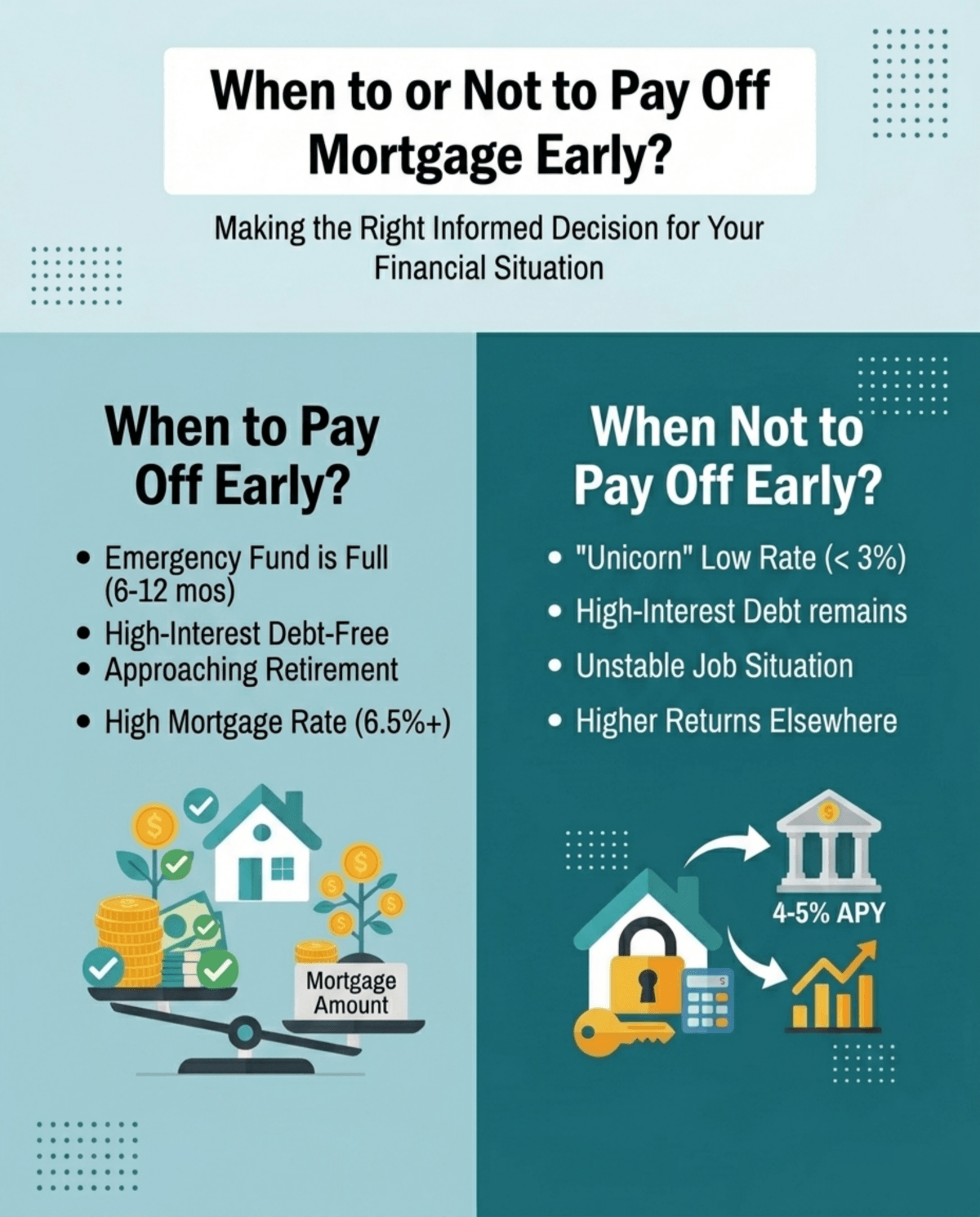

When to Pay Off Mortgage Early?

Not everyone is in the right season of life to aggressively pay down their housing debt. However, you should strongly consider wiping out your mortgage if you meet these specific criteria:

- Your Emergency Fund is Full: You already have six to twelve months of living expenses sitting safely in a highly liquid savings account.

- You Are Consumer Debt-Free: You have completely eliminated all high-interest liabilities, such as credit card balances, auto loans, and personal loans.

- You Are Nearing Retirement: Transitioning to a fixed income is much less stressful when you don't have a hefty housing payment looming over you every month.

- Your Interest Rate is High: If your rate is 6.5% or higher (common for recent purchases), paying it off guarantees a strong return.

When Not to Pay Off Mortgage Early?

Sometimes, keeping a mortgage is the smartest wealth-building decision you can make. Do not accelerate your payoff schedule under these circumstances:

- You Have a "Unicorn" Low Rate: If you secured a sub-3% fixed rate during the pandemic, don't touch it. When high-yield savings accounts pay 4% to 5%, you are literally earning more in interest than your mortgage costs. This is basic financial arbitrage.

- You Still Have High-Interest Debt: Never pay extra on a 5% home loan while carrying a 24% APR credit card balance. Always tackle the most expensive debt first.

- Your Job is Unstable: If your industry is experiencing layoffs, hoarding cash is far more important than building illiquid home equity. In a crisis, cash is king.

What to Consider Before Paying Off Mortgage Early?

Ready to pull the trigger? Hold on a second. Before you start draining your checking account, run through this quick checklist to protect yourself.

- Check for sneaky penalties: Dig up your closing documents or call your servicer to verify they won't slap you with a prepayment penalty fee.

- Confirm the payment logistics: Don't assume your bank knows what to do with extra cash. Call them to confirm the exact process, whether it's clicking a specific button online or writing a memo, so every cent goes directly to the principal.

- Consult your CPA: Ask your tax advisor how losing the Mortgage Interest Deduction will impact your April tax bill, especially if you usually itemize.

FAQs About Paying Off Mortgage Early

Q1. What is the 2% rule for mortgage payoff?

This general rule of thumb suggests you should only aggressively pay off your house if your mortgage rate is at least 2% higher than what you could safely earn investing. Others use it to mean adding an extra 2% to your monthly payments to slowly crush the principal.

Q2. How to cut 10 years off a 30 year mortgage?

You can chop a decade off your timeline by bumping up your monthly principal payments by roughly 30%. A simpler route? Combine a biweekly payment schedule with one large lump-sum extra payment at the end of each year. Consistency is key here.

Q3. How can I pay off my 20 year mortgage in 5 years?

Honestly, this takes extreme discipline. You'll need to throw a massive chunk of your take-home pay at the loan every single month. Most folks who pull this off either downsize their lifestyle drastically or use huge windfalls like an inheritance or a business sale.

Q4. Is it better to have money in savings or pay off a mortgage?

It boils down to simple math. Compare your savings account's after-tax Annual Percentage Yield (APY) against your loan's interest rate. If your high-yield savings pays 5% but your mortgage costs 3%, keep the money in the bank. You're coming out ahead.

Q5. What are tax implications of paying off mortgage early?

The biggest hit is losing your Mortgage Interest Deduction. However, because the standard deduction is so high these days, most homeowners don't even itemize anymore. For a lot of families, paying off the house actually changes absolutely nothing on their tax returns.

Final Word: Is It a Good Idea to Pay Off Mortgage Early?

At the end of the day, deciding to clear your mortgage is a classic tug-of-war between spreadsheet math and human emotion. The math might scream at you to invest your extra cash, especially if you have a rock-bottom rate.

But honestly? You can't put a price on the psychological freedom of walking into your living room and knowing you own it 100%. Before making your final move, play around with an online mortgage payoff calculator, or grab a coffee with a financial planner to see what makes sense for your 2026 goals.

People Also Read

- Are Mortgage Rates Expected to Go Down in 2026? Expert Forecasts

- Gross vs. Net Income for a Mortgage: What Lenders Use & Why

- 1099 Form Explained: What Is It? What Is Used for?

- 1099 Form vs W2: What's the Difference? Details Here

- What is a WVOE Form: Meaning, Purpose & Use

- Make Extra Payments on Mortgage: Is It Worth It?