Written by

Eric

Share this article

.svg)

Subscribe to updates

When I bought my first home, looking at the 30-year amortization schedule made my stomach drop. The total interest was staggering. I immediately wondered: Is there a better way? What if I pay biweekly instead of monthly? Is it actually worth it?

If you are facing a massive 30-year loan and want to keep your cash flow manageable while saving a fortune in interest, you are in the right place. Let me walk you through exactly how this strategy works, its hidden traps, and whether it's the right move for you.

Key Takeaways

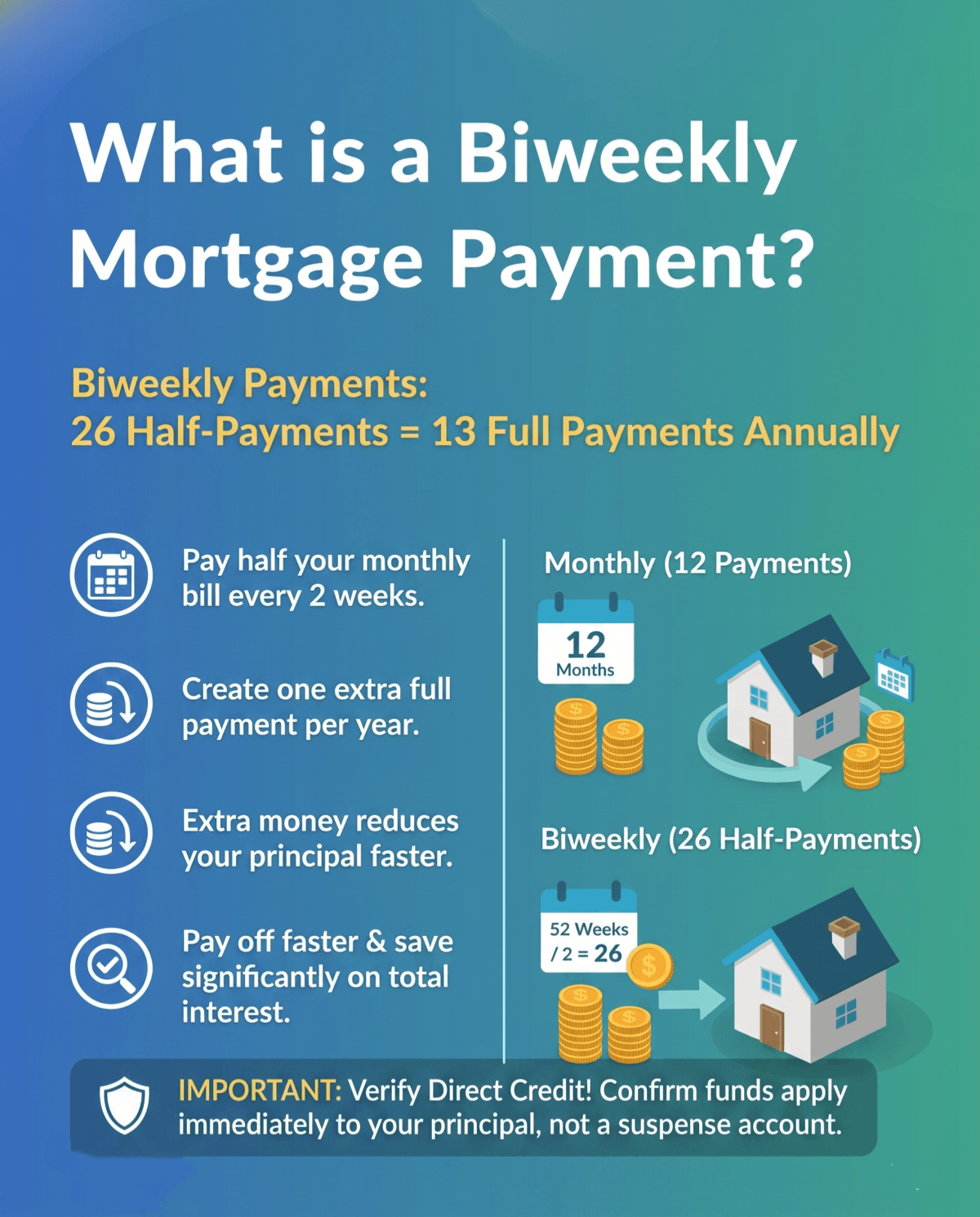

- The core math: In a typical full year, you make 26 half-payments, which equals 13 full monthly payments.

- The biggest benefit: You can shave five to six years off a typical 30-year loan and save tens of thousands in interest.

- The major warning: Never pay a third-party company to set this up. Always watch out for hidden setup fees from lenders.

What is a Biweekly Mortgage Payment?

A biweekly mortgage payment simply means cutting your standard monthly bill in half and paying that smaller amount every two weeks. When I first heard this, I confused it with a bimonthly schedule. They are entirely different! Bimonthly (or semi-monthly) means paying twice a month, usually on the 1st and 15th, resulting in 24 half-payments (12 full months). Biweekly, however, follows the 52 weeks in a calendar year. You end up making 26 half-payments, which equals 13 full payments annually.

Can you choose this option right away? Sometimes. A few lenders let you select a biweekly schedule during your initial loan application. However, most standard mortgages are written as monthly contracts. If you want to switch later, you usually have to request a modification through your loan servicer.

How Do Biweekly Mortgage Payments Work?

The magic of this strategy lies in how the calendar forces an extra payment and how that money is applied. Here is exactly where your cash goes:

- The 13th Payment: Because there are 52 weeks in a year, paying every two weeks yields 26 half-payments. That creates one extra full payment per year.

- Principal reduction: This extra money goes toward reducing your principal faster, which in turn lowers the total interest you pay over time.

- The snowball effect: Since your principal drops faster, the compound interest calculated on your remaining balance shrinks drastically.

You must be careful, though. I discovered that some banks don't process the half-payment immediately. Instead, they park your money in a suspense account until the second half arrives to make a full monthly payment. Always verify that your bank credits the funds directly to your principal right away.

Pros and Cons of Biweekly Mortgage Payments

Like any financial strategy, this approach has two sides. Here is what I learned when weighing my options.

Benefits:

- Build equity faster: You own your home outright much quicker.

- Massive interest savings: You keep tens of thousands of dollars in your pocket instead of giving it to the bank.

- Budget alignment: If you receive biweekly paychecks, syncing your mortgage bill with your payday makes cash flow management incredibly smooth.

Drawbacks:

- Loss of flexibility: Depending on your lender, you may be expected to continue the biweekly schedule, although many programs can be modified or canceled if needed.

- Hidden fees: This is my biggest pet peeve. Some third-party management companies and even shady lenders charge "enrollment fees" or "per-transfer fees." If you pay $300 just to set it up, you are needlessly eating into your own interest savings.

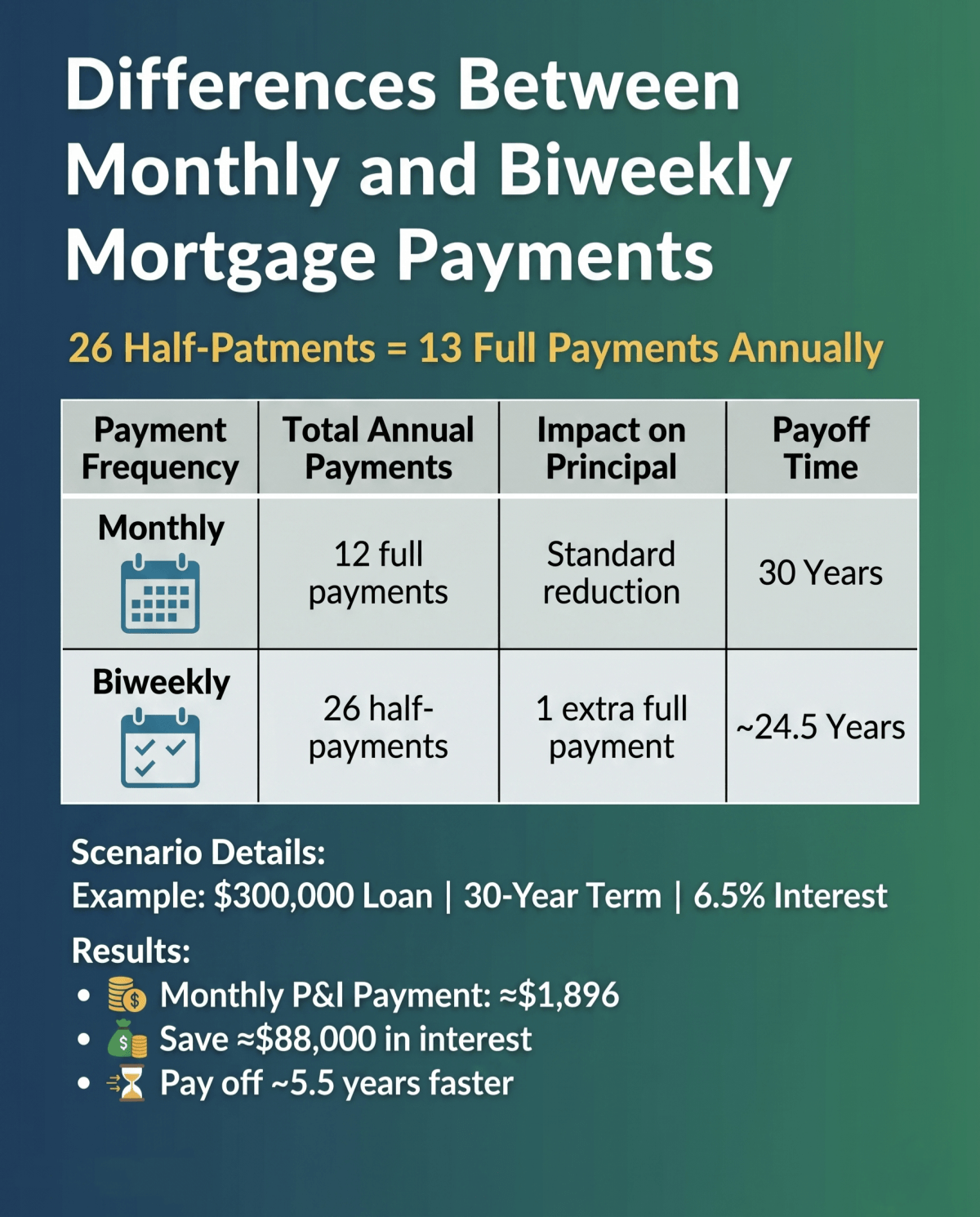

Differences Between Monthly and Biweekly Mortgage Payments

To show you the real impact, let's compare the two methods. I ran the numbers for a standard $300,000 mortgage on a 30-year term with a 6.5% interest rate.

In this scenario, a standard monthly payment is about $1,896. Over 30 years, you would pay around $382,600 in interest alone. By switching to biweekly, you make the equivalent of 13 payments a year. This small tweak saves you roughly $88,000 in interest and shaves more than five years off your loan!

Every loan is slightly different due to taxes and escrow. I highly recommend using a free online mortgage calculator to plug in your exact rate and balance. It is the best way to see your personal math.

Also Read:

- Must-Read Tips for Paying Off Mortgage Early

- Ultimate Guide: How to Calculate Monthly Mortgage Payment?

- How to Calculate Mortgage Interest: Manually & Automatically

- [Solved] How Much Interest Will I Pay on My Mortgage?

Key Considerations: Which to Choose?

Deciding between the two isn't just a math problem. It's a lifestyle choice. Before you change your payment plan, ask yourself these crucial questions:

- What is your pay schedule? If you get paid on the 1st and 15th, a biweekly mortgage might mess up your checking account balance.

- Is your cash flow tight? Committing to an accelerated schedule leaves less room for error during tough months.

- Are there fees? Does your servicer offer this for free? If not, run away.

- What is your opportunity cost? If your mortgage rate is only 3% from a few years ago, you might be better off investing that extra cash in an index fund earning 8%, rather than paying down cheap debt.

Alternatives to Biweekly Mortgage Payments

If a formal biweekly contract feels too restrictive or expensive, you have brilliant DIY alternatives. I personally use these to get the exact same benefits without the rigid rules.

- DIY Extra Yearly Payment: Just stick to your monthly schedule, but manually send one extra lump-sum payment directed at the principal at the end of the year.

- The 1/12 Rule: Take your normal monthly principal and interest payment, divide it by 12, and add that fraction to your bill each month. It mathematically equals a 13th payment by year's end.

- Refinancing: If you want a guaranteed faster payoff and rates have dropped, you could refinance into a 15-year mortgage.

With the DIY methods, you retain total control. If your car breaks down in October, you can simply skip the extra payment without facing penalties.

FAQs About Biweekly Mortgage Payments

Q1. How much faster will I pay off my mortgage with biweekly payments?

Usually, you can shave four to six years off a standard 30-year loan. The exact timeline depends heavily on your interest rate. Loans with higher interest rates actually see a more dramatic reduction in payoff time because the extra principal payment eliminates more compounding interest.

Q2. Does a biweekly mortgage save you money?

Yes, absolutely. While your individual payment amounts don't get cheaper, your lifetime cost drops significantly. Because the extra annual payment reduces your principal balance faster, you are charged less interest over the life of the loan, saving you tens of thousands of dollars.

Q3. Can I switch to biweekly payments at any time?

Most lenders allow you to transition at any point during your term. However, you must contact your loan servicer directly to set it up. Also, check your contract to ensure you won't trigger any early prepayment penalties, though these are rare on modern conventional loans.

Q4. Do I need a third-party company to set up biweekly payments?

Absolutely not. Please do not fall for this trap. Many third-party services charge hundreds of dollars in setup and transaction fees to do something you can do for free. You can easily arrange this directly with your bank or automate a DIY strategy yourself.

Q5. Does making biweekly payments build credit faster?

No, it won't significantly speed up your credit-building process. Credit bureaus care primarily about your on-time payment history and your credit utilization ratio, not the frequency of your mortgage drafts. Paying monthly or biweekly yields the same positive mark on your credit report.

Conclusion: Is Making Biweekly Mortgage Payments a Good Idea?

To answer the ultimate question: Yes, it is an incredibly effective strategy, but only under the right circumstances. If your employer pays you every two weeks, your cash flow is stable, and your bank offers free automated biweekly deductions, it is a fantastic, "pain-free" way to save a fortune.

However, if your lender charges a fee or your income fluctuates, I highly recommend skipping the formal setup. Instead, use the DIY 1/12 rule. You will secure the exact same massive interest savings while keeping the financial flexibility you need to sleep peacefully at night.

People Also Read

- Ultimate Guide: How to Buy a House for the First Time?

- [Tutorial] How to Estimate What Mortgage You Can Afford?

- Guide: How to Calculate Gross Income for a Mortgage?

- Mortgage Interest Deduction: Details, Limits & FAQs

![[Solved] Can I Use K-1 Income to Qualify a Borrower?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a44cb55129383ad19f46080_can-i-use-k-1-income-to-qualify-a-borrower-banner.png)