Written by

Eric

Share this article

.svg)

Subscribe to updates

As a loan professional, I see it every day: homebuyers reviewing their mortgage statements and wincing at that extra Private Mortgage Insurance (PMI) fee. If you put less than 20% down, you know exactly what I mean. While PMI helped you secure your house sooner, it is ultimately a sunk cost that protects the lender, not you.

The good news? You aren't stuck with it forever. Depending on your loan type and how much your property has appreciated, there are clear, legal ways to drop this expense and keep more cash in your pocket. Let's explore your best options.

Key Takeaways

- You can actively request PMI cancellation once your property hits 80% equity.

- Under federal law, lenders must automatically terminate PMI when your loan-to-value (LTV) ratio drops to 78%.

- A clean, on-time payment history is strictly required before any insurance falls off.

- Alternative methods like home remodeling or refinancing can help you shed the premium years ahead of schedule.

Also Try: Zeitro Private Mortgage Insurance (PMI) Calculator

Does PMI Go Away at 20%?

No, it doesn't vanish automatically at 20%. Under the Homeowners Protection Act (HPA), reaching 20% equity (or an 80% LTV) is merely the trigger point where you earn the right to request cancellation.

If you do nothing, your servicer isn't legally obligated to drop the premium until your balance naturally pays down to 78% of the original purchase price.

To stop paying as soon as you cross that 80% threshold, you must take the initiative and submit a formal, written request to your lender.

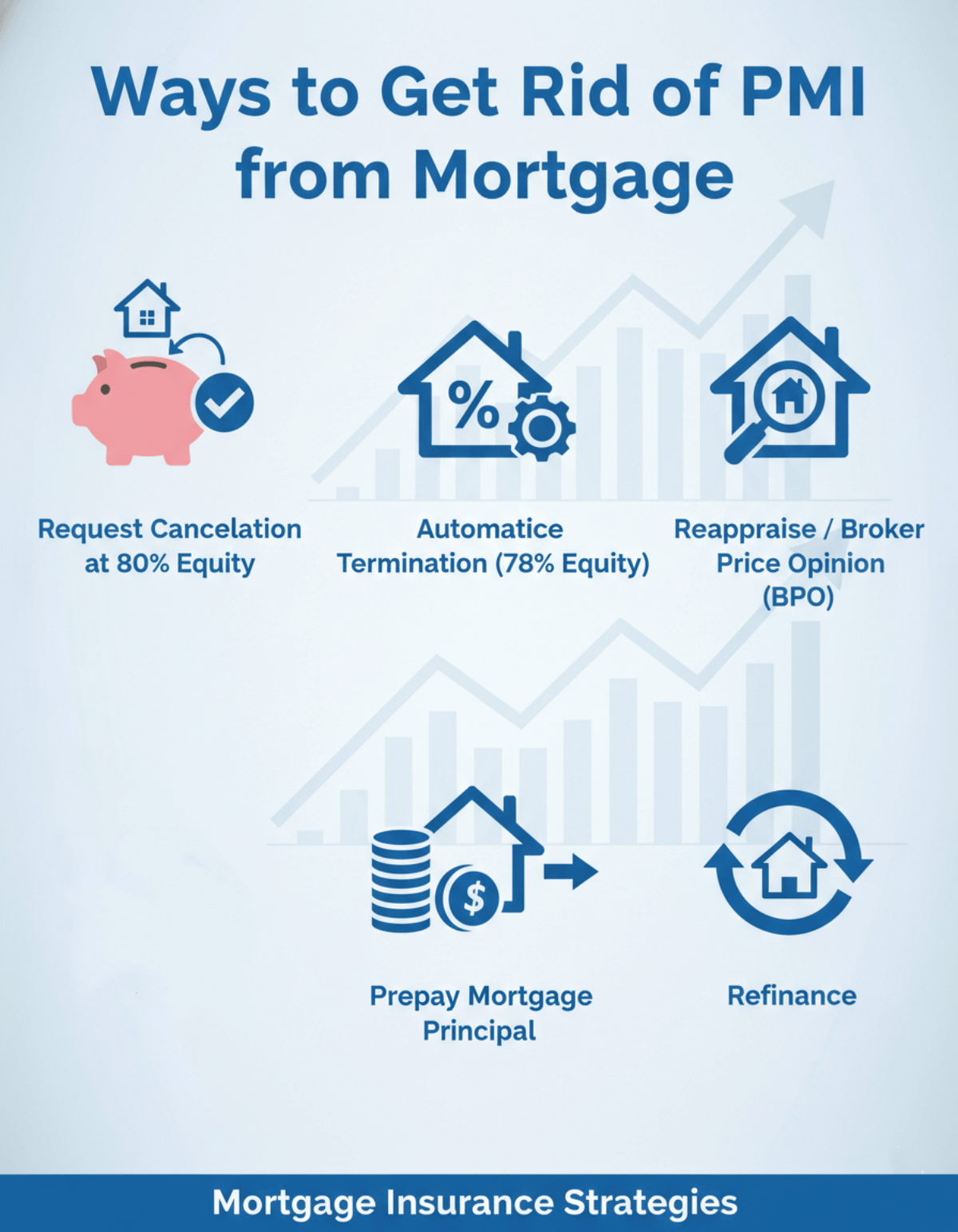

Ways to Get Rid of PMI from Mortgage

Fortunately, you have several legitimate paths to shake off this monthly burden. It all depends on your current financial situation and local housing market trends.

Request Cancellation at 80% Equity

Once your loan balance drops to 80% of your home's original purchase price (or the original appraised value, whichever was lower), you are in the driver's seat. Don't wait for your servicer to reach out. You need to write a formal letter requesting the removal of your private mortgage insurance.

Keep in mind that this 80% mark is calculated based strictly on your regular amortization schedule. The lender might require a basic certification to ensure the property hasn't declined in value and that no second mortgages or mechanics' liens are silently attached to your title.

Taking action at this exact moment saves you money before automatic termination kicks in months later.

Automatic Termination (78% Equity)

If writing letters isn't your style, you can simply rely on federal law. The Consumer Financial Protection Bureau (CFPB) enforces a rule stating that lenders must automatically cancel your PMI once your mortgage balance reaches 78% of the property's original value.

This happens naturally as you stick to your standard schedule. There is a catch, though: you must be completely current on your payments.

If you happen to be behind on your mortgage when the 78% milestone hits, the servicer will maintain the insurance coverage until you catch up and your account is back in good standing.

Reappraise/Broker Price Opinion (BPO)

What if your neighborhood has exploded in popularity, or you just completed a massive kitchen renovation? Your house is likely worth more now, meaning your Loan-to-Value ratio has naturally shrunk. In a hot market, you don't have to wait years to hit that magic equity number based on the old purchase price.

You can ask your lender to calculate your LTV using the current market value. Usually, this requires paying out of pocket for a professional appraisal or a Broker Price Opinion (BPO).

A crucial piece of advice from my experience: always contact your lender first. Hiring an outside expert without their blessing will just waste your money.

Prepay Mortgage Principal

For those who want to aggressively slash their debt, prepaying your mortgage principal is a fantastic strategy to remove PMI faster. By making extra principal payments each month or dropping a large lump sum, say, from a tax refund or a work bonus, you accelerate your timeline to hit that 80% LTV mark.

Even throwing an extra $100 toward the loan every billing cycle chops away at the balance significantly over time. Just make sure you specifically instruct your servicer to apply the extra funds directly to the "principal balance." Otherwise, they might hold the cash as a credit for future interest, defeating the purpose.

Refinance

When interest rates dip or your property value spikes, refinancing is a powerful move. By replacing your current mortgage with a brand new conventional loan, you bypass the old PMI completely, as long as your new loan sits at an 80% LTV or lower.

Refinancing also gives you a chance to secure a better interest rate or adjust your loan term. However, you need to run the numbers carefully. Refinancing comes with closing costs, which usually range from 2% to 5% of the loan amount. I always advise clients to calculate their break-even point: divide your total closing costs by your monthly savings.

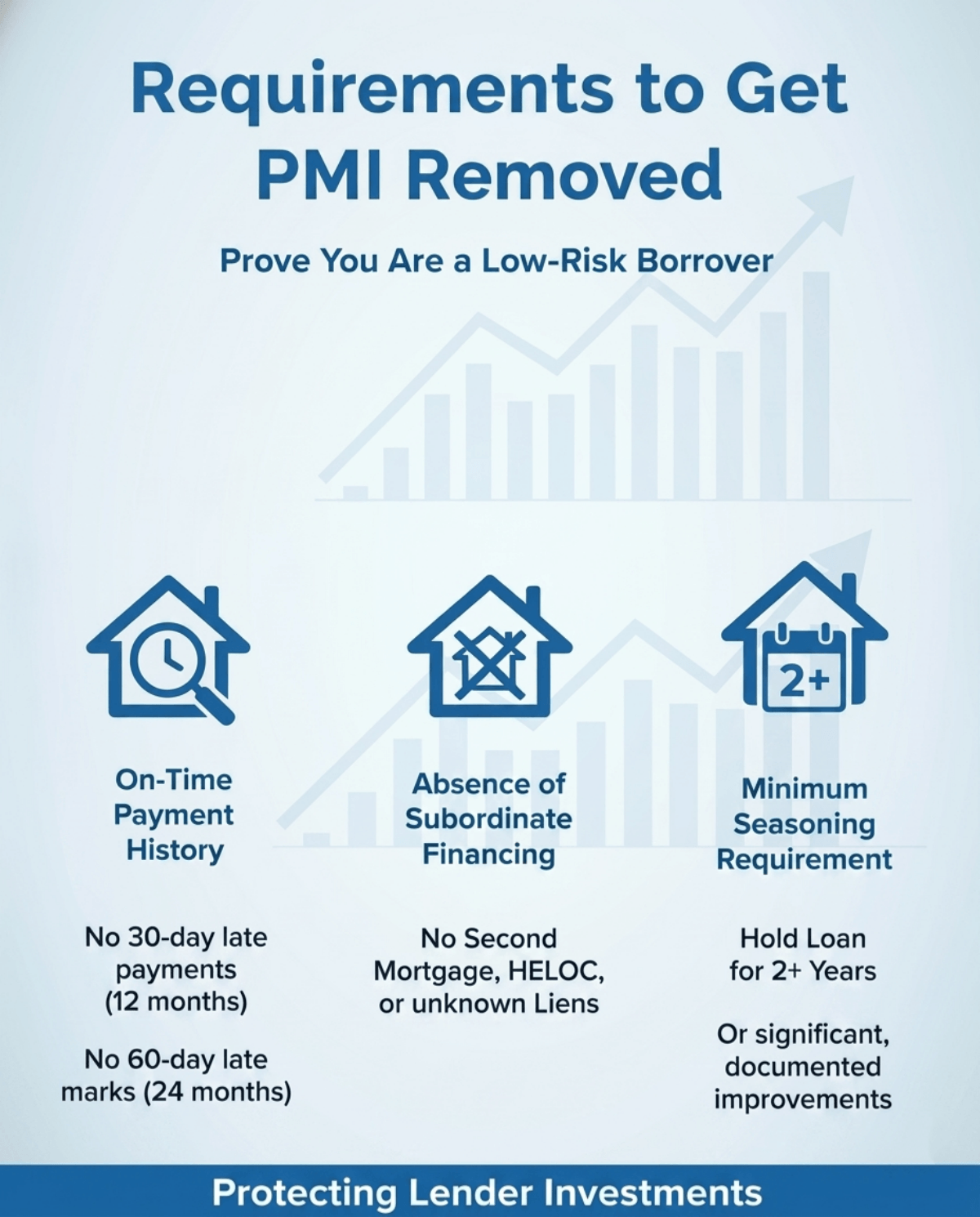

Requirements to Get PMI Removed

Before any servicer agrees to drop your mortgage insurance, you must prove you are a low-risk borrower. Meeting the equity threshold isn't enough. Lenders enforce strict rules to protect their investments. Here is what they look for:

- On-Time Payment History: Your track record must be spotless. Usually, this means zero payments that were 30 days late within the past 12 months, and no 60-day late marks in the last 24 months.

- Absence of Subordinate Financing: The bank wants to ensure no hidden debt is threatening their position. Having a second mortgage, a HELOC, or unknown liens can complicate or temporarily block your cancellation request.

- Minimum Seasoning Requirement: Lenders typically enforce a "seasoning period," meaning you must hold the loan for at least two years before requesting removal based on a new appraisal, unless you've made significant, documented structural improvements.

FAQs About Removing PMI from Mortgage

Q1. When does PMI go away on an FHA loan?

Technically, FHA loans don't have PMI. They use a Mortgage Insurance Premium (MIP).

If your original down payment was under 10%, your MIP usually stays for the life of the loan, though some older FHA loans may allow MIP cancellation once the loan‑to‑value ratio falls to 78% of the original value.

If you put down 10% or more, MIP expires after 11 years.

Q2. Does PMI go away after 20 percent automatically?

No, private mortgage insurance does not go away automatically when you reach 20% equity. At 20% (or 80% LTV), you only earn the legal right to submit a written request to your lender for cancellation.

If you don't actively ask your servicer to remove it, federal law dictates that the insurance will only drop off by itself when your loan‑to‑value (LTV) ratio reaches 78% of the original purchase price, assuming your payments are completely up to date.

Q3. Can home improvements help remove PMI faster?

Yes, substantial home improvements can accelerate your PMI removal. Adding a bedroom, finishing a basement, or completely remodeling a kitchen increases your property's overall market value, which in turn lowers your Loan-to-Value (LTV) ratio.

When you make these types of major structural upgrades, many lenders will waive the standard two-year waiting period (seasoning requirement). You can request a new appraisal to prove you've crossed the 20% equity threshold, but always clear the appraiser with your servicer beforehand.

Q4. Can you avoid PMI with 10% down?

Yes, you can avoid paying monthly PMI even if you only have a 10% down payment by exploring alternative financing structures.

One common method is Lender-Paid Mortgage Insurance (LPMI), where the bank covers the premium upfront in exchange for slightly raising your mortgage interest rate. Another strategy is an 80-10-10 "piggyback" loan, where you take out a primary mortgage for 80%, a second mortgage for 10%, and put 10% cash down. Furthermore, VA or USDA loans never require monthly PMI.

Q5. How much is PMI on a $300,000 loan?

On a $300,000 loan, you can expect PMI to cost between $1,500 and $4,500 per year, which translates to roughly $125 to $375 per month.

The exact price usually ranges from 0.5% to 1.5% of your total loan amount annually. Your personal premium depends heavily on your credit score, your down payment size, and your debt-to-income ratio. Borrowers with excellent credit usually secure rates on the lower end of that spectrum.

Conclusion: Is It Better to Pay PMI or Put 20% Down?

Deciding whether to save up a full 20% down payment or bite the bullet on PMI is a highly personal financial decision. Waiting years to save 20% carries a massive opportunity cost. You might miss out on a great home, and rising property prices could price you out of the market entirely.

Conversely, paying PMI is an unrecoverable monthly expense, but it allows you to start building equity and lock in a property immediately. I always recommend sitting down with a trusted loan officer to review your specific assets. Run the numbers, evaluate your local housing market, and choose the path that best supports your long-term wealth.

People Also Read

- Max LTV: Check Maximum Loan-to-Value Ratios By Loan Types

- Max DTI for Mortgage: Requirements By Loan Types

- Mortgage Debt-to-Income Ratio Explained: Definition& Max DTI

- [Guide] How to Calculate DTI Ratio for Mortgage?

- Mortgage Application Form 1003 (URLA): Everything You Need to Know

- How to Calculate PMI? Do the Math On Your Own