Written by

Eric

Share this article

.svg)

Subscribe to updates

Choosing the right mortgage type can feel like navigating a stressful maze of financial jargon. Trust me, I've been there. If you pick the wrong one, you might overpay by thousands or face terrifying payment spikes later. That is why clearly comparing a fixed vs adjustable rate mortgage (ARM) is so critical.

In this guide, I will break down their full differences to help you make an informed financial decision. After reading, I highly recommend getting a free consultation with local loan officers for personalized advice.

Key Takeaways

- Fixed-Rate Mortgages offer rock-solid stability. Your principal and interest payments never change, making long-term budgeting incredibly predictable.

- Adjustable-Rate Mortgages (ARMs) provide cheaper upfront costs during an introductory period, but carry serious payment shock risks when market rates adjust later.

- How to Choose depends entirely on your timeline and risk tolerance. If you plan to move within a few years, an ARM might save cash. For long-term stays, lock in a fixed rate.

What is a Fixed Rate Mortgage?

I like to explain a fixed-rate mortgage as the ultimate "set it and forget it" financial tool. Simply put, your interest rate and your monthly principal and interest payments remain fixed for the life of the loan, although total monthly housing costs may still change due to taxes and insurance, whether you choose a 15-year or a 30-year term.

Even if the housing market crashes or national interest rates soar to historic highs, your monthly bill stays exactly the same. When I was deciding on my own financing, the peace of mind this brought was unmatched. It offers unparalleled stability for homeowners who want zero surprises.

Pros:

- Clear, predictable budgeting: You always know exactly what you owe every month.

- Protection from inflation: Your rate is locked, shielding you from future interest rate hikes.

- Easy to understand: There are no complex formulas or hidden adjustment clauses.

- Perfect for long-term living: Ideal if you plan to stay in your home for decades.

Cons:

- Higher initial rates: They generally start with higher interest than an ARM.

- Refinancing costs: If market rates drop, you will incur closing costs when refinancing, though these can sometimes be rolled into the loan or offset by accepting a slightly higher rate.

- Stricter qualification: A higher initial rate might slightly lower the total loan amount you get approved for, assuming the same income level.

What is an Adjustable Rate Mortgage (ARM)?

An adjustable-rate mortgage (ARM) uses a two-part loan structure. It begins with an "introductory period" featuring a fixed, significantly lower interest rate. You'll usually see this advertised as a 5/1 or 7/1 ARM. The first number represents how many years the rate stays fixed, while the second indicates how often the rate adjusts afterward.

After the initial phase ends, you enter the "adjustment period," where your interest rate floats based on a broader market index. While responsible lenders apply rate caps to prevent your interest from rising infinitely, an ARM still exposes you to noticeable interest rate risk over time.

Pros:

- Significantly lower starting rates: Early payments are much cheaper, easing initial financial pressure.

- Great for short-term plans: If you plan to sell or move before the adjustment period kicks in, it's highly cost-effective.

- Automatic drops: If the market dips during your adjustment phase, your rate may decrease during adjustment periods if the underlying index falls, subject to rate floors and adjustment terms.

- Higher buying power: The lower initial payment might help you qualify for a slightly more expensive home.

Cons:

- Payment shock: Your monthly payments could skyrocket once the fixed period ends.

- Highly unpredictable: Long-term budgeting is less predictable, though rate caps allow borrowers to estimate worst-case scenarios.

- Complex terms: Understanding the index margin and rate caps can be confusing.

- Market risk: Even with rate caps, you are betting against future market trends.

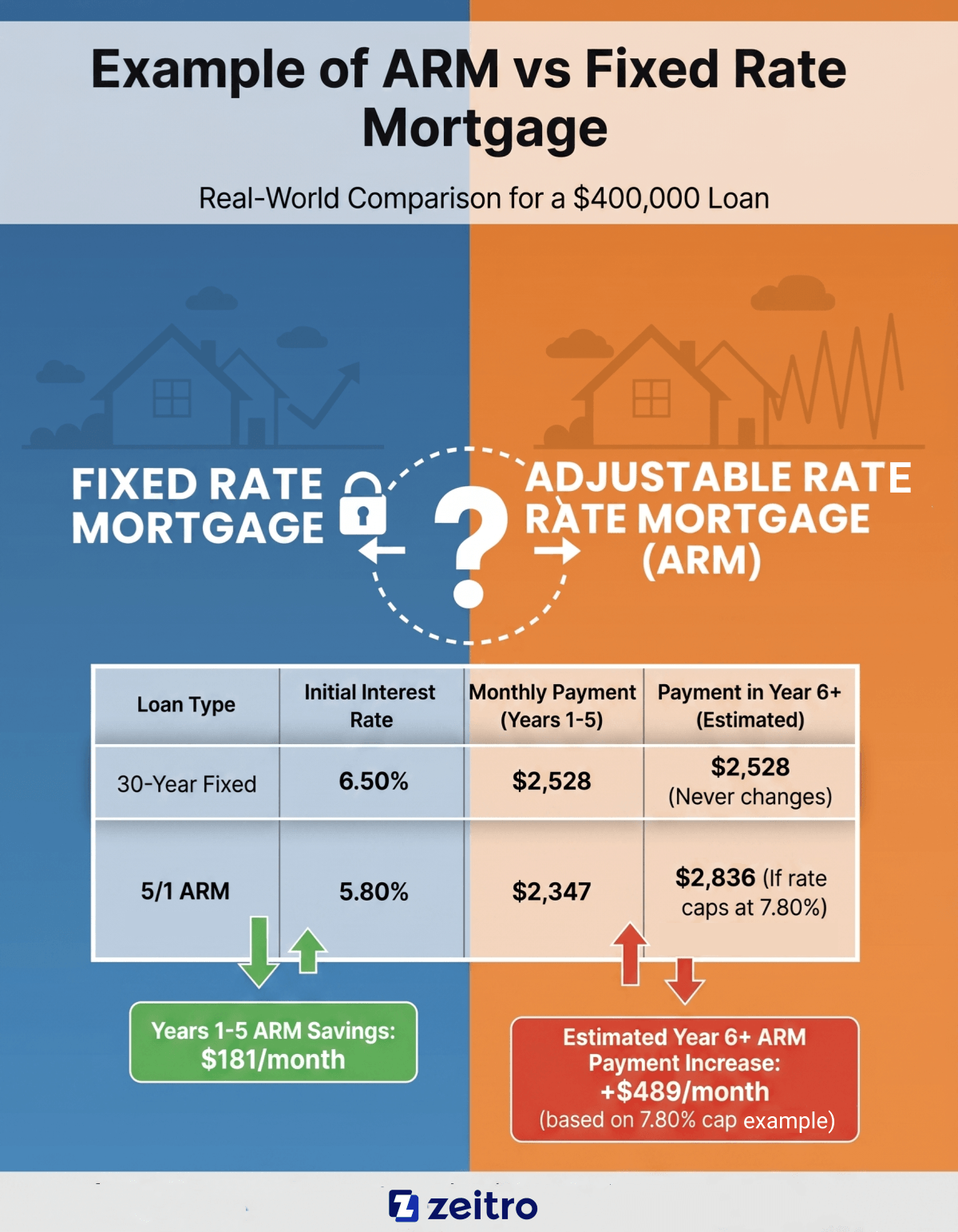

Example of ARM vs Fixed Rate Mortgage

To see how this plays out in the real world, let's look at the math. Imagine you are borrowing a $400,000 loan with a 30-year term. For illustration, assume a 30-year fixed rate around 6.5% and a 5/1 ARM at 5.8%, though actual rates vary daily by market conditions and borrower profile. For the first five years, the ARM saves you roughly $181 per month.

That's over $10,800 kept in your pocket! However, look what happens in Year 6. If the market index rises and your ARM adjusts up to 7.80% ((a typical ARM may include caps such as 2% per adjustment and a lifetime cap, though exact structures vary by loan)), your monthly payment could increase significantly (e.g., by several hundred dollars), depending on the new rate, remaining balance, and loan terms.

Disclaimer: For illustrative purposes only. Actual mortgage rates fluctuate with daily market conditions and your personal credit score. Always consult a professional before making a decision.

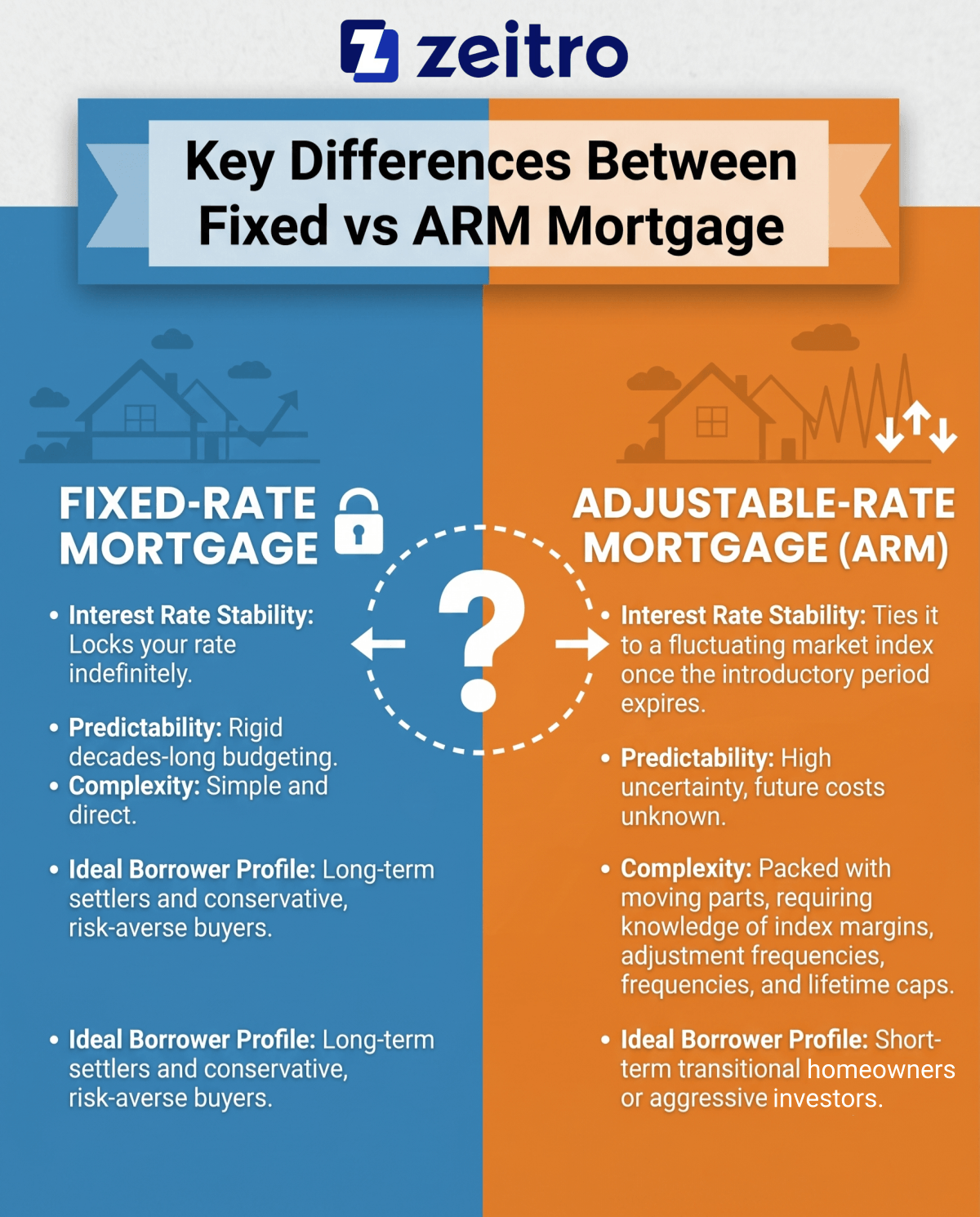

Key Differences Between Fixed vs ARM Mortgage

When deciding between these two paths, it helps to step back and look at the broader dimensions. I've found that the essence of the difference comes down to one question: How much future uncertainty are you willing to tolerate in exchange for cheaper costs today? You aren't just choosing a rate. You are choosing a risk profile. Here is a breakdown of the deepest contrasting factors.

- Interest Rate Stability: A fixed loan locks your rate indefinitely. An ARM ties it to a fluctuating market index once the introductory period expires.

- Long-Term Cost Predictability: Fixed mortgages are absolutely predictable, allowing for rigid decades-long budgeting. ARMs carry high uncertainty, as your future costs are unknown.

- Complexity: Fixed-rate contracts are simple and direct. ARMs are packed with moving parts, requiring you to understand specific terms like index margins, adjustment frequencies, and lifetime rate caps.

- Ideal Borrower Profile: A fixed option attracts long-term settlers and conservative, risk-averse buyers. An ARM favors short-term transitional homeowners or aggressive investors.

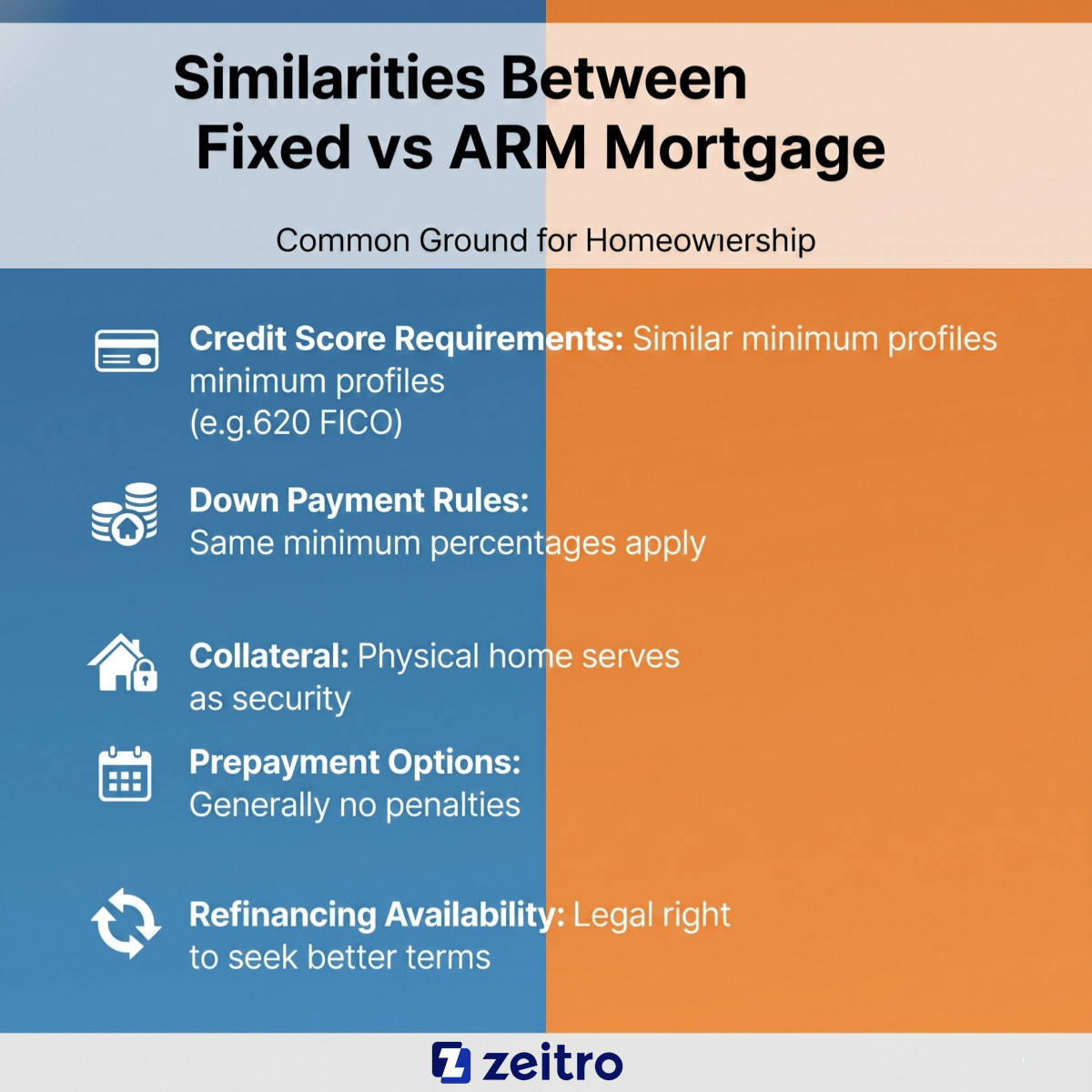

Similarities Between Fixed vs ARM Mortgage

Despite their opposing approaches to interest, we shouldn't overlook their common ground. After all, both are fundamental tools designed to help you achieve homeownership. To give you the full differences, I also need to point out where they overlap. By recognizing these shared traits, you'll see that the basic barriers to entry remain largely the same.

- Credit score requirements: Lenders demand similar minimum credit profiles (usually around 620 for conventional loans) regardless of the structure.

- Down payment rules: Both allow you to secure a property with the same minimum down payment percentages.

- Collateral: In both scenarios, the physical home serves as the collateral for the bank.

- Prepayment options: Most modern mortgages do not include prepayment penalties, though some specialized or non-qualified loans may still have them.

- Refinancing availability: You have the legal right to refinance either loan type down the road to secure better terms.

Fixed vs ARM Mortgage: Which to Choose?

There is no universal "winner" here. When friends ask me which one is objectively better, I always tell them it's not about the loan—it's about their life. You need to translate these financial concepts into an actionable roadmap that fits your specific housing goals. To make your decision easier, consider your lifestyle timeline and risk tolerance. Here is a practical framework to guide your choice.

Choose a Fixed-Rate Mortgage if...

- You plan to live in this specific house for 10 years or more.

- You are risk-averse and want to sleep peacefully knowing your bills will never spike.

- Current market interest rates are at historic or comfortable lows, and you want to lock them in permanently.

Choose an Adjustable-Rate Mortgage if...

- You confidently plan to move, sell, or refinance within 5 to 7 years.

- You anticipate a significant increase in your future income to absorb potential payment shocks.

- You want to redirect early cash flow savings into higher-yielding investments.

FAQs About ARM vs Fixed Rate Mortgage

Q1. What is the main downside of an adjustable-rate mortgage?

The biggest downside is "payment shock." When the initial fixed period ends, your interest rate adjusts to current market levels. If rates have spiked, your monthly mortgage payment will suddenly soar, potentially straining your monthly budget beyond what you can comfortably afford.

Q2. Can you refinance a fixed-rate mortgage?

Yes, absolutely. If widespread market interest rates drop below your current locked rate, you can refinance your loan to lower your monthly payments. Just remember to calculate the closing costs to ensure the long-term savings outweigh the upfront refinancing fees.

Q3. How often does an ARM rate change after the fixed period?

Typically, the rate changes once a year. For example, with a popular 5/1 ARM, the "5" means the rate is fixed for the first five years, and the "1" indicates that it will adjust annually for the remainder of the loan term.

Q4. Are ARM rates always lower than fixed rates initially?

Generally, yes. Banks take on less long-term interest rate risk with an ARM, so they pass those savings to you upfront. This discounted introductory rate is precisely what makes an ARM so attractive for the first few years.

Q5. Is it hard to switch from an ARM to a Fixed-rate mortgage?

No, it is relatively straightforward. You simply need to go through a standard refinance process. In fact, many borrowers deliberately secure an ARM for the short-term savings and refinance into a fixed-rate loan right before their adjustment period kicks in.

Conclusion

Ultimately, purchasing a home is one of the most substantial financial decisions you will ever make. A fixed-rate mortgage grants you the ultimate gift of long-term predictability, while an ARM offers fantastic short-term cash flow advantages. Your choice boils down to your personal timeline and how well you handle risk. Because everyone's credit score, income, and local housing market dynamics are entirely unique, reading articles online is only the first step.

I strongly recommend getting a free consultation with nearby professional loan officers. Let them run your exact numbers so you can confidently secure the mortgage strategy that best fits your life.

People Also Read

- When Does PMI Go Away? How to Get PMI Removed?

- [Tutorial] How to Estimate What Mortgage You Can Afford?

- Ultimate Guide: How to Calculate Monthly Mortgage Payment?

- How to Calculate Mortgage Interest: Manually & Automatically

- At What Income Level Do You Lose Mortgage Interest Deduction?

Also Try Tools:

- Zeitro Mortgage Payment Calculator with Interest & Taxes

- Zeitro Mortgage Affordability Calculator Free and Online

![[Solved] Can I Use K-1 Income to Qualify a Borrower?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a44cb55129383ad19f46080_can-i-use-k-1-income-to-qualify-a-borrower-banner.png)