Written by

Eric

Share this article

.svg)

Subscribe to updates

Applying for a mortgage is always exciting, but the pile of required paperwork can quickly become overwhelming. When I first bought a home as a freelancer, I was surprised when my lender asked for a stack of 1099 forms to verify my self-employment income.

Fortunately, finding these documents is easier than it looks. Here is my practical guide on how to safely find and download your 1099 forms online today.

Key Takeaways

- Instant Access: You can download 1099 forms from client billing portals. You can use an IRS Wage and Income Transcript to view reported income, although lenders may still require original documents or additional verification.

- Mortgage Proof: Lenders may request 1099 forms as supporting documents, but they primarily rely on tax returns, profit and loss statements, and bank records to verify income.

- Compliance: Even if a 1099 is missing, you must still legally report your earnings using bank records.

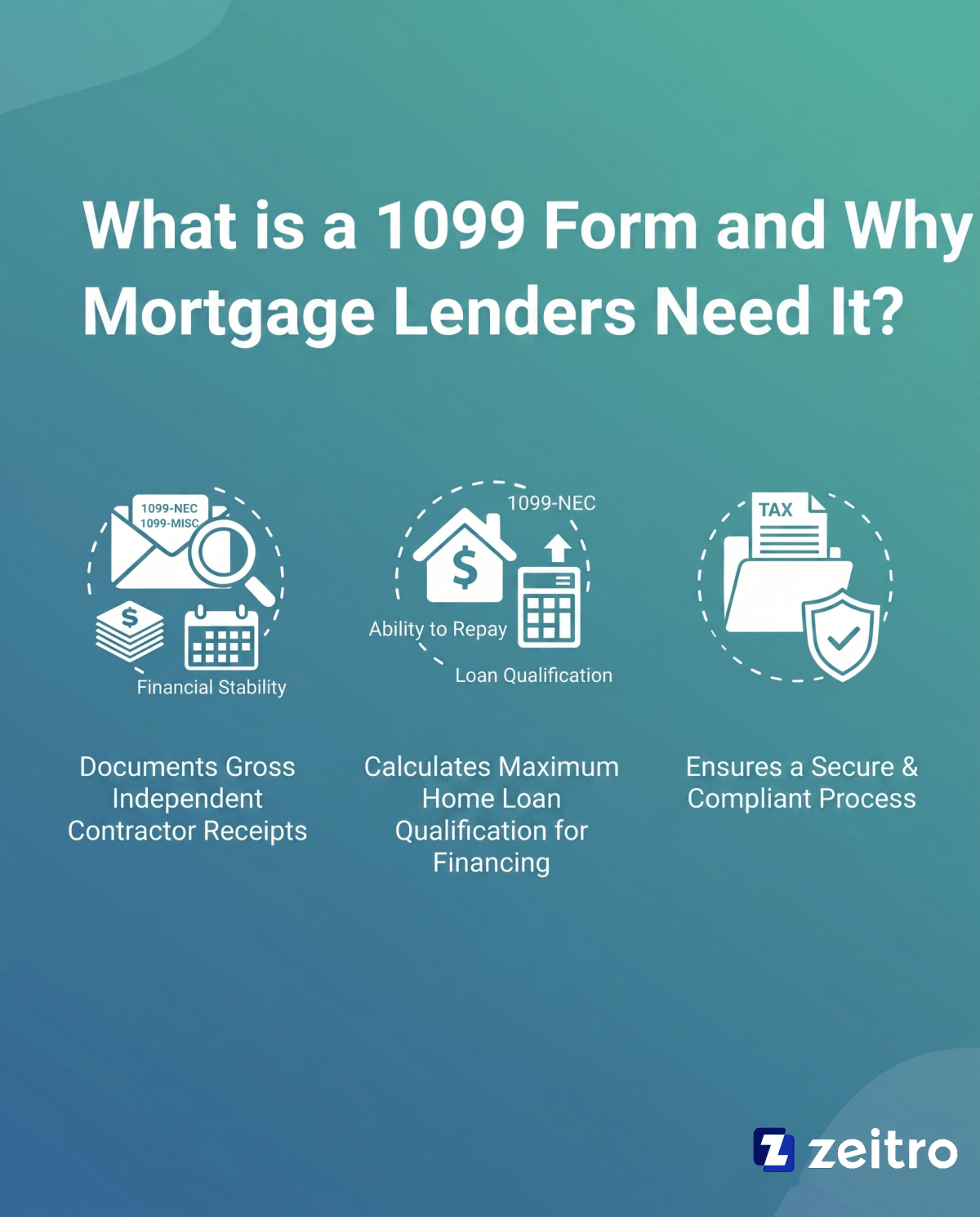

What is a 1099 Form and Why Do Mortgage Lenders Need It?

When I first applied for a home loan as an independent contractor, I quickly realized that traditional lenders look at the world differently. Instead of standard W-2 tax forms, self-employed professionals receive various IRS 1099 forms, like the 1099-NEC (Nonemployee Compensation) or 1099-MISC. Underwriters use these documents to analyze our financial stability over time.

Because we do not have a standard salary pay stub, these 1099 statements help document gross business receipts, but lenders typically rely on full tax returns and supporting financial records to assess income. They help lenders determine our "Ability to Repay" and calculate the maximum home loan we qualify for, ensuring the loan process remains secure and compliant.

Also Read:

- 1099 Form vs W2: What's the Difference? Details Here

- How to Determine Mortgage Eligibility? Verify Guidelines in Seconds

- Mortgage Income Requirements: Learn Before You Apply

- Guide: How to Calculate Gross Income for a Mortgage?

- How to Calculate Self-Employed Income for a Mortgage?

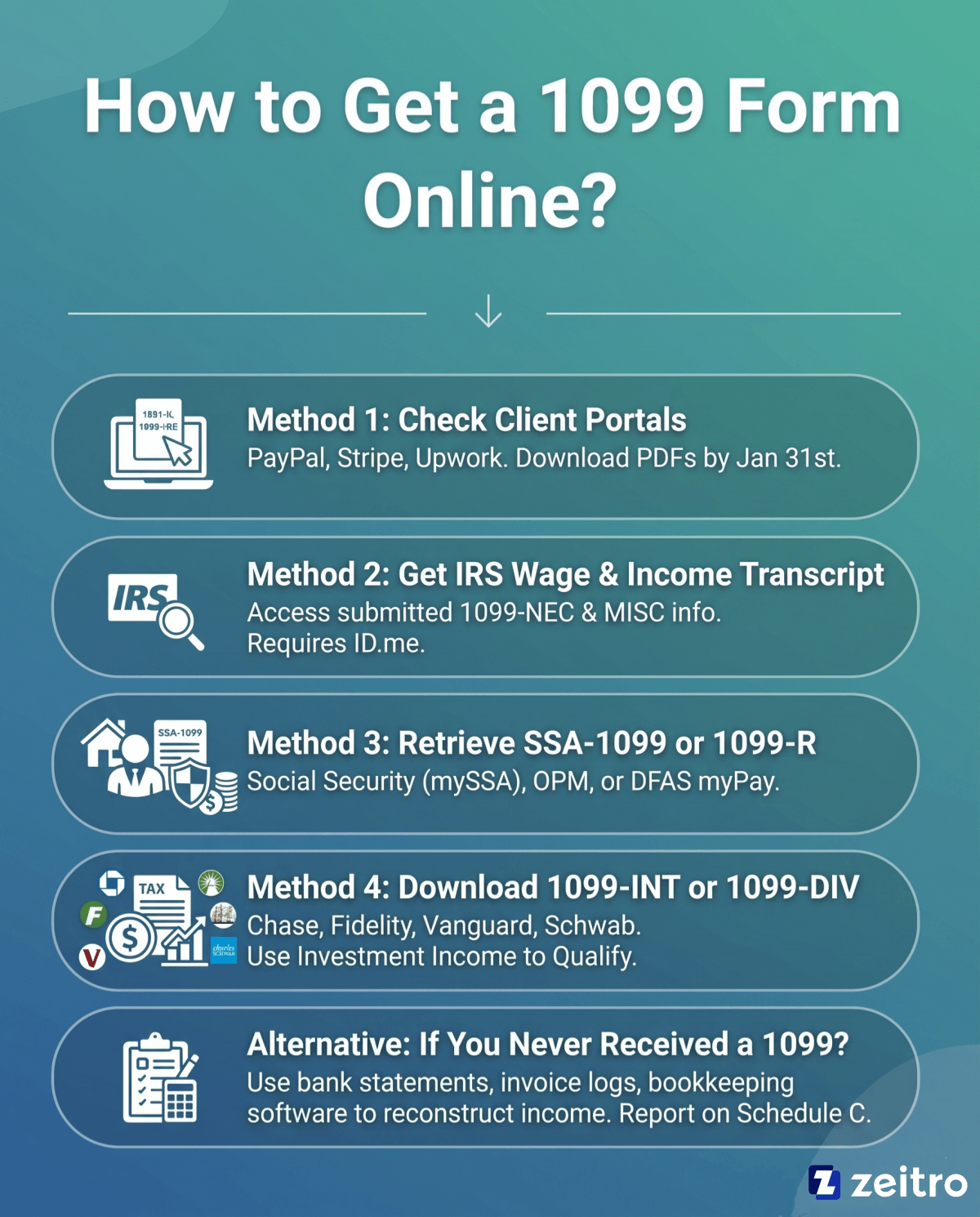

How to Get a 1099 Form Online?

Retrieving your documents online is straightforward once you know where to look. I recommend starting with the fastest methods first.

Method 1: Check Client or Payer Portals

If you work as an independent contractor or freelancer, your first stop should be the digital platforms where you receive payments. Some platforms, such as PayPal, Stripe, or Upwork, may issue forms like 1099-K or 1099-NEC depending on your activity and reporting thresholds, while payroll providers like Gusto or ADP generate forms only if the payer has set them up to do so.

I recommend logging into your accounts and navigating to the "Tax Documents," "Statements," or "Settings" tab. Because payers are legally required to distribute these forms by January 31st, they are usually available for PDF download around this time. If you do not see yours, check your email archives for a notification containing a secure download link. Taking a few minutes to check these portals is often the fastest way to gather your records without having to wait for physical mail to arrive.

Method 2: Get an IRS Wage and Income Transcript

When a former client goes out of business or becomes completely unresponsive, you can go straight to the source. The IRS maintains records of many tax documents submitted by third parties under your Social Security Number, though the data may be incomplete or subject to delays and updates. To access this, log into your IRS Individual Online Account using your secure ID.me credentials.

Once logged in, select the option to "Get Transcript" and choose "Wage and Income Transcript" for the relevant tax year. This document displays reported 1099-NEC and 1099-MISC information submitted to the IRS, although it may not always reflect the most current or complete records. One detail to keep in mind is that the IRS transcript database may not be fully updated for the current tax year until late spring, typically around May or June.

Method 3: Retrieve SSA-1099 or 1099-R Online

For borrowers using retirement or pension income to qualify for a mortgage, lenders typically require documentation such as SSA-1099 or 1099-R, along with verification that the income is stable and likely to continue.

If you receive Social Security benefits, you will need Form SSA-1099. You can download an electronic copy easily by logging into your personal "my Social Security" account on the official Social Security Administration website.

On the other hand, if you are a federal civil service retiree or military veteran receiving retirement pay, you will need Form 1099-R. These can be retrieved by logging into the Office of Personnel Management (OPM) services portal or the Defense Finance and Accounting Service (DFAS) myPay system.

Having these official federal logins active beforehand helps prevent unexpected delays when your loan underwriter requests proof of steady retirement income.

Method 4: Download 1099-INT or 1099-DIV

If a portion of your qualifying mortgage income comes from investments, savings accounts, or stock dividends, your lender may request your 1099-INT or 1099-DIV forms if you plan to use investment income to help qualify for the loan.

You do not have to wait for your financial institutions to mail these papers. Instead, log into your online banking or investment brokerage portals, such as Chase, Fidelity, Vanguard, or Charles Schwab. Navigate to their "Tax Center," "Statements," or "Documents" tab. Financial institutions typically make these PDFs available for secure download by late January or mid-February.

I always make it a habit to download these directly to a secure folder. Having clean, original PDF copies ready to upload helps speed up the mortgage pre-approval process and keeps your application moving forward smoothly.

Alternative: What to Do If You Never Received a 1099?

There are times when a client simply fails to issue a 1099, even after you have reached out to them multiple times. When this happens, you should not delay your tax filing or your mortgage application. Instead, gather your own financial records to calculate your total earnings.

I rely heavily on my bookkeeping software, invoice logs, and monthly bank statements to reconstruct my exact income for the year. When filing your taxes, you must still report this nonemployee compensation on your Schedule C (Form 1040).

Lenders will still evaluate this income based primarily on your tax returns and IRS transcripts, and may use bank statements as supporting documentation rather than relying on a missing 1099 form, keeping your home purchase on track.

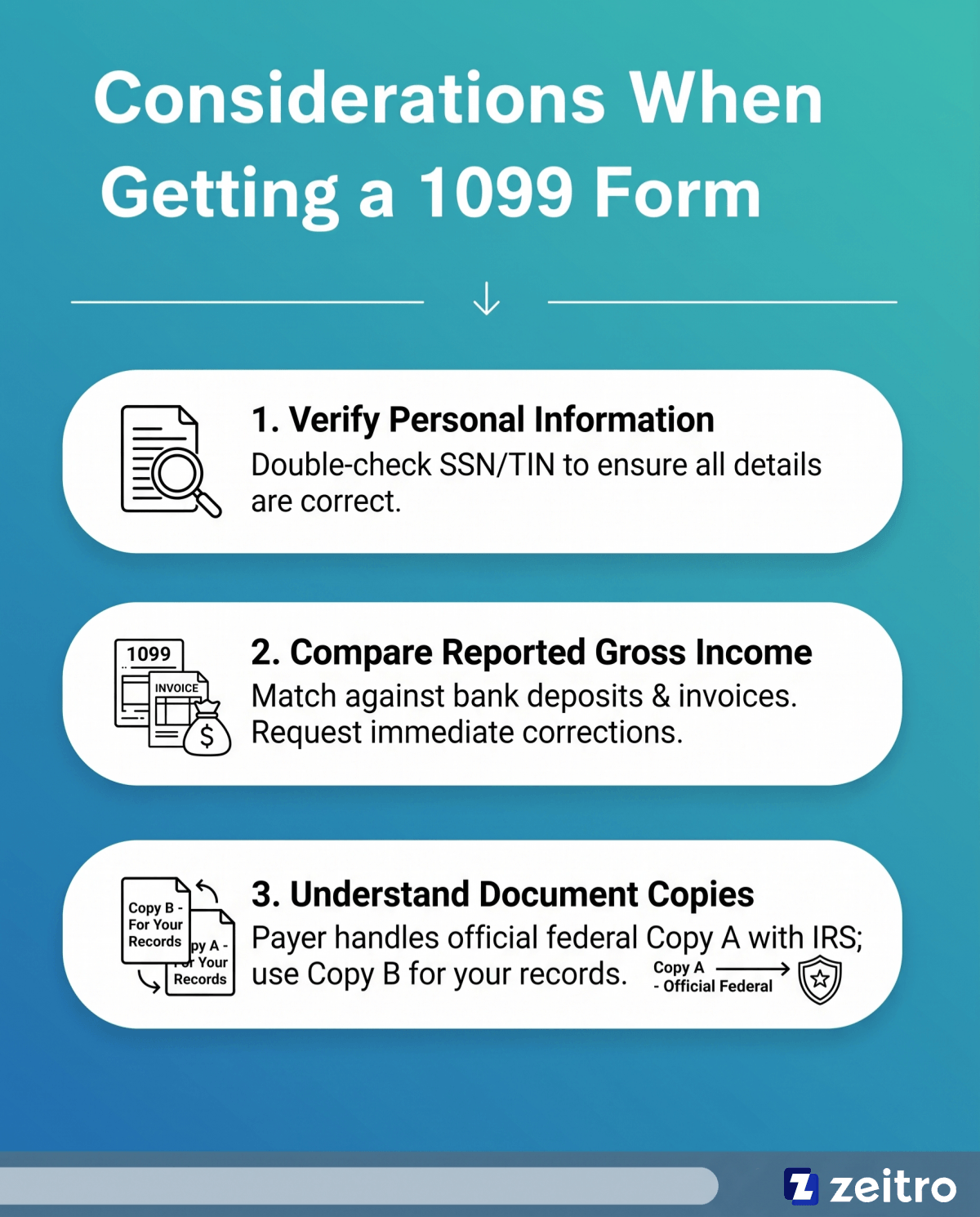

Considerations When Getting a 1099 Form

Before submitting these forms to a mortgage loan officer, I always double-check the details.

- First, verify that your Social Security Number (SSN) or Taxpayer Identification Number (TIN) is entirely correct. A single typo can delay your tax filing or cause a lender to pause your application.

- Second, compare the reported gross income on the 1099 against your own bank deposits and invoices. If you spot a discrepancy, contact the payer immediately to request a corrected form. Giving a lender documents that mismatch your official tax transcripts can raise red flags during underwriting.

- Lastly, remember that while you can download Copy B for your records, the official federal Copy A is handled directly between the payer and the IRS.

FAQs About Getting a 1099 Form

Q1. What happens if I don't receive a 1099?

If a client fails to send a form, contact them directly to request it. If they remain unresponsive, calculate your earnings using your bank records and report the income anyway.

Q2. Can I file my taxes without a 1099?

Yes, you can. The IRS expects you to report all earned self-employment income, even if a client never issues a 1099. Use your invoices and bank statements to determine the total.

Q3. What is a "1099-Only Mortgage" and do I need tax returns?

A 1099-only mortgage is a Non-QM loan allowing self-employed borrowers to qualify using only their 1099 forms and bank statements. This often means tax returns may not be required, but lenders will still review alternative documentation such as bank statements or income verification reports.

Q4. How many years of 1099 history do traditional lenders require?

Traditional lenders typically require a steady two-year history of 1099 income. However, some conventional programs might accept a one-year history if you have worked in the exact same industry for several years.

Q5. Why does my mortgage lender require an IRS transcript if I already provided my 1099s?

Lenders use Form 4506-C to request your transcripts directly from the IRS. This helps them verify that the 1099 forms you provided match what was officially reported, protecting against potential fraud.

Conclusion

Navigating the home-buying process as a self-employed professional can feel challenging, but gathering your tax documents does not have to be. Obtaining your 1099 forms online is a straightforward process, whether you access client portals or retrieve transcripts directly from the IRS website. I found that preparing these documents early saved me from last-minute stress during underwriting.

Since mortgage programs and IRS guidelines can shift, I highly recommend consulting with a certified tax professional or a licensed mortgage advisor to discuss your specific financial situation. With the right preparation, you can confidently take the next steps toward securing your home loan.

People Also Read

- Income Needed for Mortgage: Methods, Examples & Requirements

- Must-Read Tips for Paying Off Mortgage Early

- [Solved] What Percentage of Income Should Go to Mortgage?

- Guide: Loan Origination Points Explained in Mortgage