Written by

Eric

Share this article

.svg)

Subscribe to updates

As an active mortgage professional, I know firsthand how exhausting it can be to match homebuyers with the right California Down Payment Assistance (DPA) programs. Navigating fluctuating county income limits and varying guidelines takes hours of manual work.

To solve this, I rely on Zeitro Strata. This tool instantly finds eligible programs with reliable, verifiable source links, saving both loan officers and borrowers valuable time during the homebuying journey.

Key Takeaway

- Based on my years in the mortgage industry, here is the bottom line on California's DPA landscape:

- Diverse Options: Assistance exists at the state, county, and city levels.

- Not Just for First-Timers: Programs like GSFA Platinum accommodate repeat buyers.

- Deferred Payback: Most assistance is structured as silent seconds with 0% interest or shared equity.

- Preparation Matters: Mandatory homebuyer education is required across almost all programs.

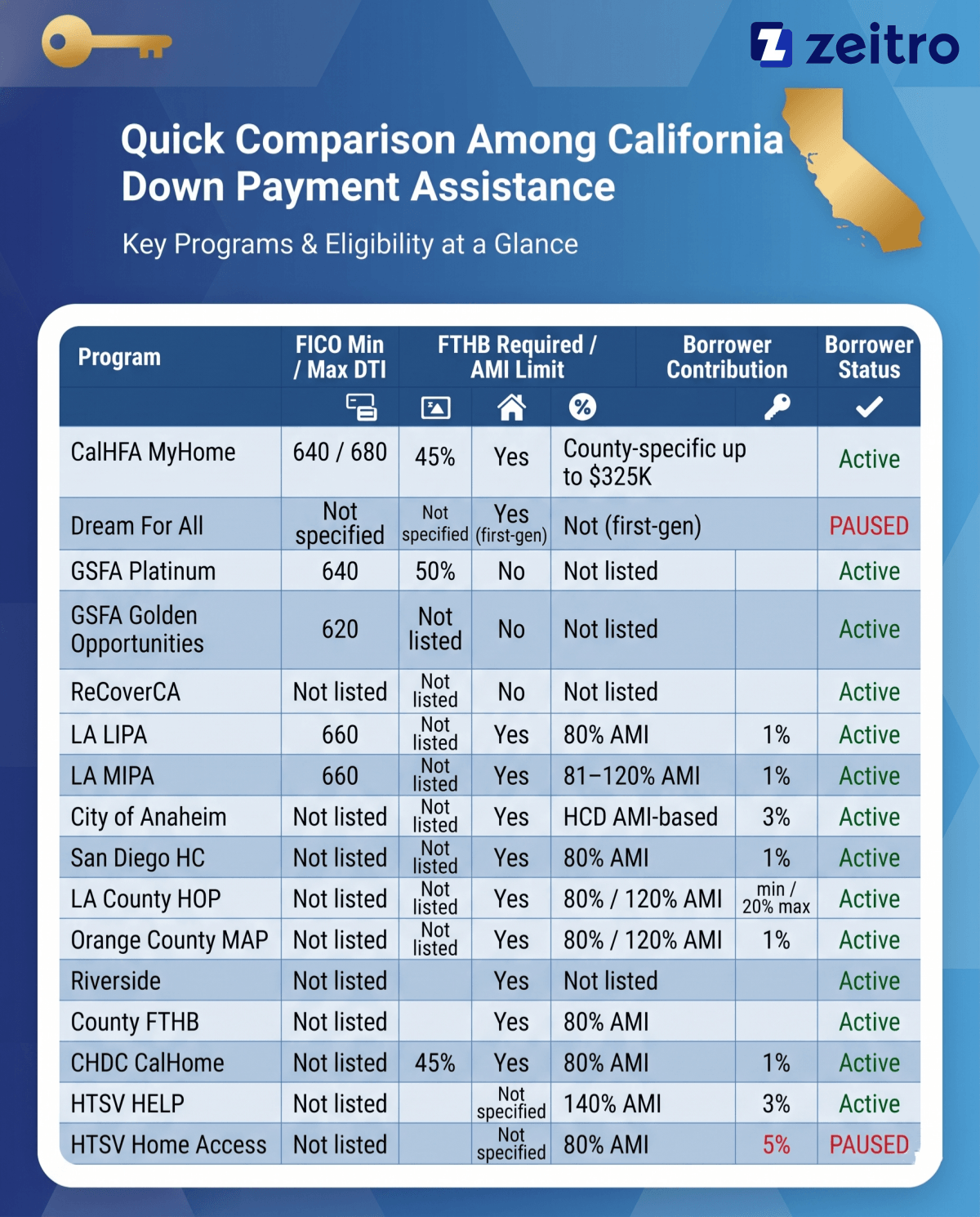

Quick Comparison Among California Down Payment Assistance

In my practice, I always start with a high-level eligibility check to avoid wasting a buyer's time on a program they cannot qualify for. The table below outlines the core metrics for California's primary DPA programs active in 2026.

*Disclaimer: Program terms, income limits, and funding pools change frequently. I highly recommend confirming details with an approved lender before entering contract.

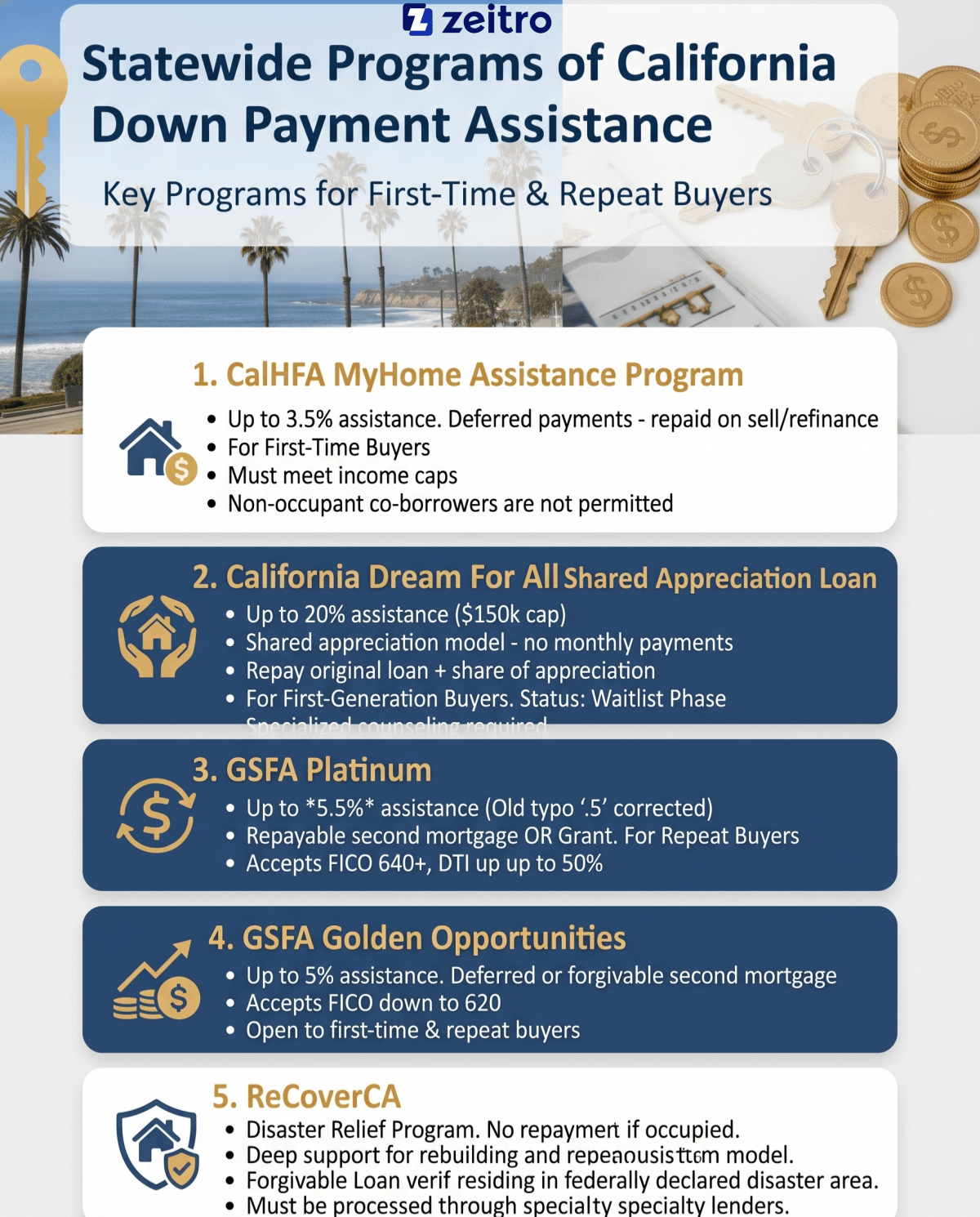

Statewide Programs of California Down Payment Assistance

Statewide programs form the foundation of most down payment strategies. Administered by state agencies like CalHFA and GSFA, these programs are widely accessible because they can be bundled directly with conventional or government first mortgages through hundreds of approved lenders across California.

#1. CalHFA MyHome Assistance Program

This is the most popular statewide program I recommend for first-time buyers. It acts as a silent second mortgage to help cover upfront costs.

Status: Active.

Assistance Amount: Up to 3.5% of the purchase price on FHA/VA/USDA loans, or 3% on conventional loans.

Repayment Terms: Payments are deferred. There are no monthly payments. The principal is repaid only when you sell, refinance, or pay off your primary mortgage.

Key Requirements: You must be a first-time homebuyer occupying the property as your primary residence. Your income must remain within CalHFA's county-specific caps, and you must complete an approved homebuyer education class. Non-occupant co-borrowers are not permitted.

#2. California Dream For All Shared Appreciation Loan

This is a shared appreciation loan designed to help first-generation buyers reduce upfront costs and increase purchasing power, rather than requiring a traditional large down payment.

Status: Vouchers IssuedWaitlist Phase. The registration portal closed in March 2026, and voucher status updates were released in late May 2026.

Assistance Amount: Up to 20% of the home's purchase price, capped at a maximum of $150,000.

Repayment Terms: This is a shared appreciation loan with no monthly payments. When you sell or transfer the home, you repay the original loan amount plus a share of the home's appreciation proportional to the assistance received (e.g., a 20% assistance share typically results in a 20% share of appreciation).

Key Requirements: At least one borrower must qualify as a first-generation homebuyer. All borrowers must be first-time buyers, meet county income caps, and complete specialized counseling.

#3. GSFA Platinum

If you are a repeat buyer who needs upfront cash, the Golden State Finance Authority (GSFA) Platinum program is one of the few avenues available.

Status: Active.

Assistance Amount: Provides up to 5.5% of the total loan amount to cover down payment or closing fees.

Repayment Terms: It is typically offered either as a repayable second mortgage or as a non-repayable grant, depending on the option selected.

Key Requirements: You do not need to be a first-time homebuyer to qualify. It accommodates credit scores as low as 640 and allows for a maximum debt-to-income (DTI) ratio of up to 50%.

#4. GSFA Golden Opportunities

This sister program to GSFA Platinum is my go-to for buyers who need flexible credit underwriting but still require substantial down payment support.

Status: Active.

Assistance Amount: Offers up to 5% of the first mortgage amount in assistance.

Repayment Terms: Typically structured as a deferred or forgivable second mortgage, depending on program terms and lender options.

Key Requirements: Open to both first-time and repeat buyers. The defining benefit is that it accepts FICO credit scores down to 620, making homeownership accessible to a broader credit profile.

#5. ReCoverCA

This program is designed to assist homeowners in specific federally declared disaster areas and is only available during designated funding periods.

Status: Active.

Assistance Amount: Offers deep financial support tailored to local rebuilding and acquisition costs.

Repayment Terms: This is structured as a forgivable loan. If you occupy the home as your primary residence for the required duration, the entire balance is forgiven, and no repayment is required.

Key Requirements: Borrowers must verify they resided in a federally declared disaster area (such as a wildfire or flood zone) during the disaster event. It must be processed through participating specialty lenders.

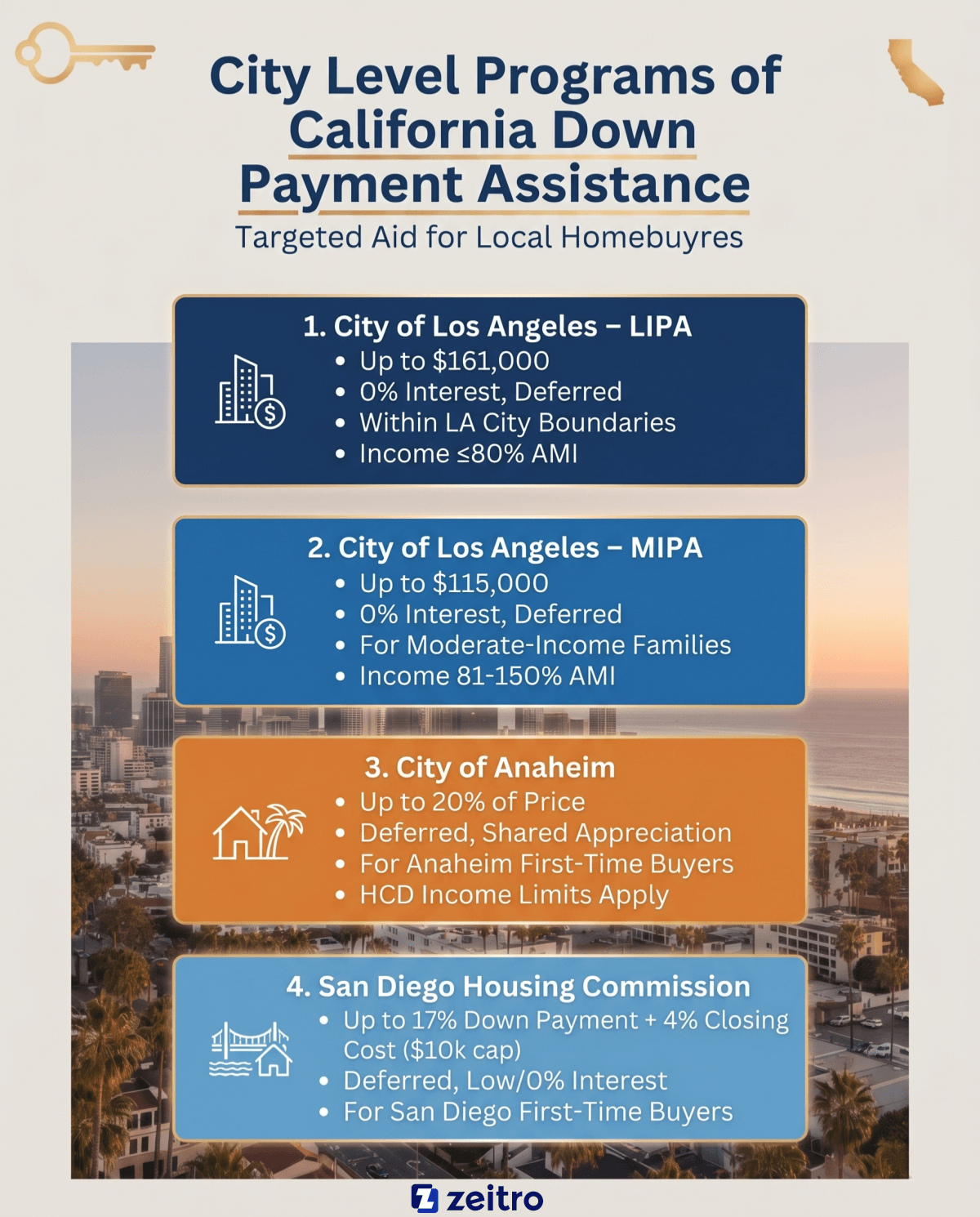

City Level Programs of California Down Payment Assistance

Many of my clients are surprised to learn that local municipalities offer their own highly generous DPA funds. Because city programs rely on local budgets, they operate on strict reservation cycles, but they often provide much larger assistance amounts than state programs.

#1. City of Los Angeles – LIPA

Run by the Los Angeles Housing Department (LAHD), LIPA is one of the most generous municipal programs in the country.

Status: Active. It runs on a strict reservation schedule with limited spots per round throughout 2026.

Assistance Amount: Up to $161,000 to cover down payment and closing costs.

Repayment Terms: This is a 0% interest, deferred loan with no monthly payments. It is typically structured as a deferred loan. Specific terms such as appreciation sharing or resale restrictions may vary by funding round and the full balance is due upon sale, title transfer, or at the end of 30 years.

Key Requirements: Your household income must be at or below 80% of the LA Area Median Income (AMI). Buyers must contribute at least 1% of the purchase price from their own funds, have a 660 minimum FICO score, and buy a home within Los Angeles city limits.

#2. City of Los Angeles – MIPA

MIPA is the middle-class counterpart to LIPA, helping families who earn moderate incomes but still struggle with Los Angeles home prices.

Status: Active, operating on periodic reservation dates in 2026.

Assistance Amount: Up to $115,000, depending on your exact moderate-income tier.

Repayment Terms: 0% interest, deferred loan with no monthly payments. Like LIPA, it includes shared equity and is repaid when you sell, refinance, or transfer the property.

Key Requirements: Income must be between 81% and 120% (or up to 150%) of the local AMI. Buyers must provide a 1% down payment from personal funds, maintain a 660 FICO score, and purchase within LA city boundaries.

#3. City of Anaheim

This program is designed specifically to help moderate-income families plant roots in Orange County.

Status: Active.

Assistance Amount: Provides a substantial second loan of up to 20% of the purchase price.

Repayment Terms: This is a deferred loan with no monthly payments. Repayment of the principal plus a proportionate share of the home's appreciation is required when you sell, transfer title, or refinance.

Key Requirements: Borrowers must invest at least 3% of their own funds into the transaction. You must be a first-time homebuyer, meet HCD income limits, and buy a home strictly within Anaheim city limits (unincorporated areas are excluded).

#4. San Diego Housing Commission

For buyers looking to purchase in the highly competitive San Diego market, SDHC offers a vital financial bridge.

Status: Active.

Assistance Amount: Up to 17% of the purchase price for down payment, plus an optional closing cost loan of up to 4% (capped at $10,000).

Repayment Terms: Typically structured as a deferred loan. Interest terms vary by program and may include 0% or low simple interest options. No monthly payments are made, and the accrued interest plus principal are repaid when you sell, refinance, or move out.

Key Requirements: Income must not exceed 80% of San Diego's AMI. You must be a first-time buyer contributing at least 1% of your own funds, and the property must sit within San Diego city limits with a purchase price under $883,025.

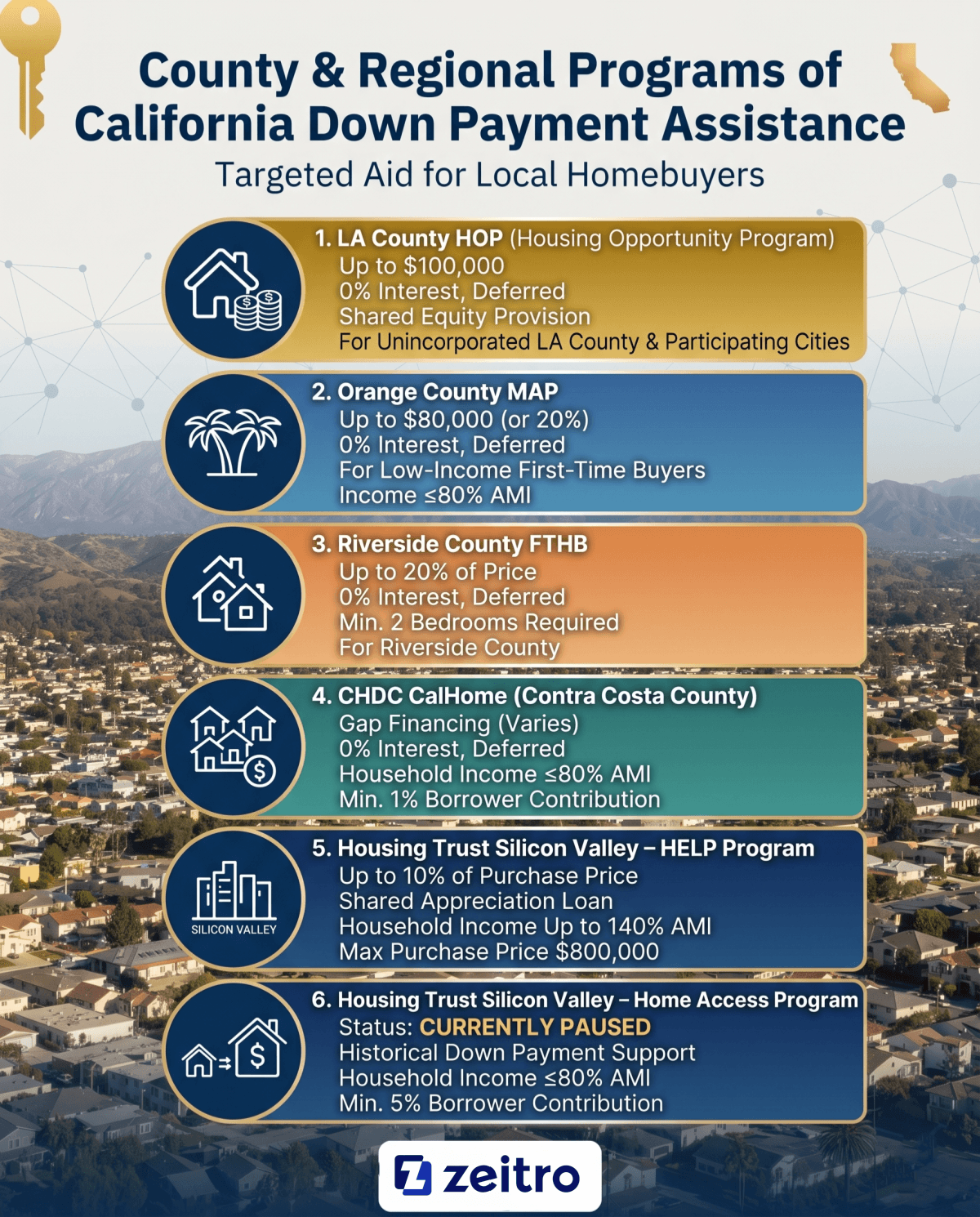

County & Regional Programs of California Down Payment Assistance

County and regional programs are excellent alternatives if your dream home lies outside city limits. These programs are designed to cover unincorporated county lands and participating smaller cities, offering robust funding options that frequently escape the mainstream spotlight.

#1. LA County HOP (Housing Opportunity Program)

LACDA administers these county-level programs, offering an exceptional resource for buyers looking in unincorporated LA County or its participating cities.

Status: Active on a first-come, first-served basis.

Assistance Amount: HOP80 offers up to $100,000 (max 20% of purchase price). HOP120 offers up to $85,000 (max 20% of purchase price).

Repayment Terms: Accrues 0% interest with fully deferred payments. It includes a shared equity provision, meaning the principal and a portion of home appreciation are repaid upon sale or transfer.

Key Requirements: Borrowers must be first-time buyers investing at least 1% of their own funds. Household income limits are capped at 80% AMI for HOP80 and 120% AMI for HOP120.

#2. Orange County MAP

This county-specific program helps low-income buyers manage the notoriously high cost of living in Orange County.

Status: Active.

Assistance Amount: Up to $80,000 or 20% of the home's purchase price, whichever is lower.

Repayment Terms: Typically structured as a 0% interest deferred loan, repaid upon sale, refinance, or transfer of the property. No monthly payments are required. The balance is paid off when you sell or refinance.

Key Requirements: Applicants must be first-time homebuyers earning under 80% of Orange County's AMI. The home must be located in unincorporated Orange County or one of its 14 participating cities, and you must take a mandatory homebuyer education course.

#3. Riverside County FTHB

This program uses federal HOME and state PLHA funding to support homeownership across Riverside County.

Status: Active.

Assistance Amount: Provides up to 20% of the purchase price to assist with down payment and closing costs.

Repayment Terms: A 0% interest, fully deferred loan with no monthly payments. It is paid back only when you sell, refinance, or move out of the property.

Key Requirements: Households must earn 80% AMI or less. A critical and often overlooked rule is that the home must have a minimum of 2 bedrooms. The property purchase price cannot exceed local limits, and it must be your primary residence.

#4. CHDC CalHome (Contra Costa County)

This program is designed to keep housing affordable in the East Bay, specifically targeting families buying in Contra Costa County.

Status: Active.

Assistance Amount: Provides gap financing up to the program's current funding limits (varies by cycle).

Repayment Terms: Deferred second loan with no monthly payments, allowing buyers to keep their monthly mortgage costs highly manageable.

Key Requirements: Household income must be at or below 80% of Contra Costa's median income. Buyers must be first-time homebuyers, contribute at least 1% of their own funds, and maintain a maximum debt-to-income (DTI) ratio of 45%.

#5. Housing Trust Silicon Valley (HTSV) – HELP Program

Managed by the Housing Trust Silicon Valley, HELP is a fantastic regional program targeting middle-income earners in the ultra-expensive Bay Area.

Status: Active.

Assistance Amount: Up to 10% of the home's purchase price to apply toward your down payment.

Repayment Terms: Structured as a shared appreciation loan with no monthly payments. Repayment is deferred until you sell, transfer, or pay off the first mortgage.

Key Requirements: Income limits are highly generous, allowing households earning up to 140% AMI to qualify. The maximum purchase price is capped at $800,000, buyers must contribute at least 3% of their own funds, and the property must be in Santa Clara County, Menlo Park, or East Palo Alto.

#6. HTSV Home Access Program

This specialized program was designed by HTSV to target low-income buyers in Alameda and Contra Costa Counties.

Status: CURRENTLY PAUSED (applications are temporarily closed while the program awaits new funding allocations).

Assistance Amount: Historically provided substantial down payment support to bridge the gap in expensive Bay Area markets.

Repayment Terms: Standard deferred payment structure with no monthly installments.

Key Requirements: Targeted households earning 80% AMI or less. Borrowers were required to provide a larger personal contribution of at least 5% of the purchase price from their own funds.

How to Apply for California Down Payment Assistance Programs?

Applying for DPA requires a strategic, step-by-step approach to ensure you do not miss out on limited funding:

- Identify Your Programs: Before anything else, I recommend running your scenario through Zeitro Strata. By inputting your target county and income, you instantly filter active programs you actually qualify for, avoiding paused options.

- Complete Homebuyer Education: Nearly all state and local programs require completion of an approved homebuyer education course (duration may vary by program).

- Get Pre-Approved with an Approved Lender: Because DPA funds are distributed through private institutions, you must work with a CalHFA or GSFA participating lender. They will package your DPA alongside your primary mortgage.

FAQs About Down Payment Assistance in California

Q1. Is California giving up to $150,000 to help first-time homebuyers?

Yes, but it is not "free money". This refers to the California Dream For All Shared Appreciation Loan, which provides up to 20% (capped at $150,000) for down payments. However, because it is a shared appreciation loan, you must repay the original amount plus 15% to 20% of your home's accrued equity when you sell or refinance. The program also utilizes a randomized lottery system and requires at least one borrower to be a first-generation homebuyer.

Q2. How do you qualify for down payment assistance in California?

While every program has unique guidelines, the core qualification rules typically revolve around:

- Buyer Status: Most programs require you to be a first-time homebuyer (no homeownership in the last three years).

- Income Limits: Your household income must stay below the county-specific caps.

- Credit Score: You generally need a FICO score between 620 and 680, depending on the program.

- Education: You must complete an approved homebuyer training course.

Q3. What is the biggest negative when using down payment assistance?

In my experience helping clients navigate these programs, the primary drawbacks include:

- Slightly Higher Rates: First mortgages paired with DPA programs may carry slightly higher interest rates depending on lender pricing and program structure.

- Balloon Payoff Risk: Since payments are deferred, you must pay off the entire secondary balance when you sell or refinance.

- Subordination Hurdles: If interest rates drop and you want to refinance your primary mortgage, getting a DPA agency to approve a subordination agreement can be a slow, complex process.

Q4. Who qualifies for down payment assistance in California?

DPA programs are designed to assist low-to-moderate-income buyers who plan to live in the home as their primary residence. However, eligibility has expanded:

- First-Generation Buyers: Qualify for specialized programs like Dream For All.

- Repeat Buyers: Can qualify through GSFA programs.

- Specific Professions: Many local programs feature dedicated allocations or relaxed limits for school employees, first responders, healthcare workers, and veterans.

Final Word

Navigating California's down payment assistance landscape can feel like studying for a highly complex exam. However, with the right strategy, bridging the down payment gap is entirely achievable. Before you start calling lenders, I highly recommend running your scenario through Zeitro Strata. It simplifies the research phase by aligning your profile with active programs in seconds, saving you hours of tedious document digging.

*Disclaimer: This guide is for informational purposes only. Programs, interest rates, and guidelines shift constantly. Always consult with a licensed, approved loan officer to verify current rules and your personal qualification status.

People Also Read

- Ability-to-Repay (ATR) Rule Explained: What to Know

- Mortgage Income Verification Guide for Loan Officers

- How to Verify Income for Mortgage: Detailed Guide for Loan Pros

- Max LTV: Check Maximum Loan-to-Value Ratios By Loan Types

- Best Mortgage CRM for Brokers, Lenders, MLOs