Written by

Eric

Share this article

.svg)

Subscribe to updates

As a loan officer or mortgage underwriter, I know that few tasks trigger a headache faster than opening a complex income file. Whether I am analyzing a straightforward W-2 salary or wading through a self-employed borrower's corporate tax returns, calculating qualifying income is the ultimate high-stakes puzzle. One minor miscalculation can cause an automated underwriting system (AUS) rejection or, worse, a post-closing repurchase demand.

Over the years, I've learned that the biggest trap is treating all income sources the same. Salaried earners offer predictability, while self-employed borrowers require us to dissect business cash flow, depreciation add-backs, and stability trends. In this guide, I will share the exact verification steps, rules, and strategies I use to clear income conditions quickly and keep loans on track.

Key Takeaways

- Income Type Dictates the Blueprint: Salaried W-2 files focus on consistency and YTD calculations, whereas self-employed applications demand a deeper look into net business cash flows and tax return schedules.

- Alternative Paths Save Deals: When standard tax returns do not tell the whole story, non-QM options like Bank Statement or DSCR loans keep the pipeline moving.

- Timing Is Critical: Employment must be verified at application, cross-checked with the IRS, and reconfirmed right before funding.

Why Is Income Verification Crucial for Mortgages?

In my years in this industry, I've seen that verifying income is about far more than just checking a box for the file. It is the foundation of a sustainable loan.

- CFPB Compliance: The Ability-to-Repay (ATR) rule legally obligates lenders to make a reasonable, good-faith determination that a borrower can repay their mortgage.

- Protecting Secondary Market Liquidity: To sell loans to Fannie Mae or Freddie Mac, our calculations must align with agency selling guides.

- Mitigating Default Risk: Rigorous validation protects the lender from buyback requests and prevents borrowers from taking on unsustainable monthly payments.

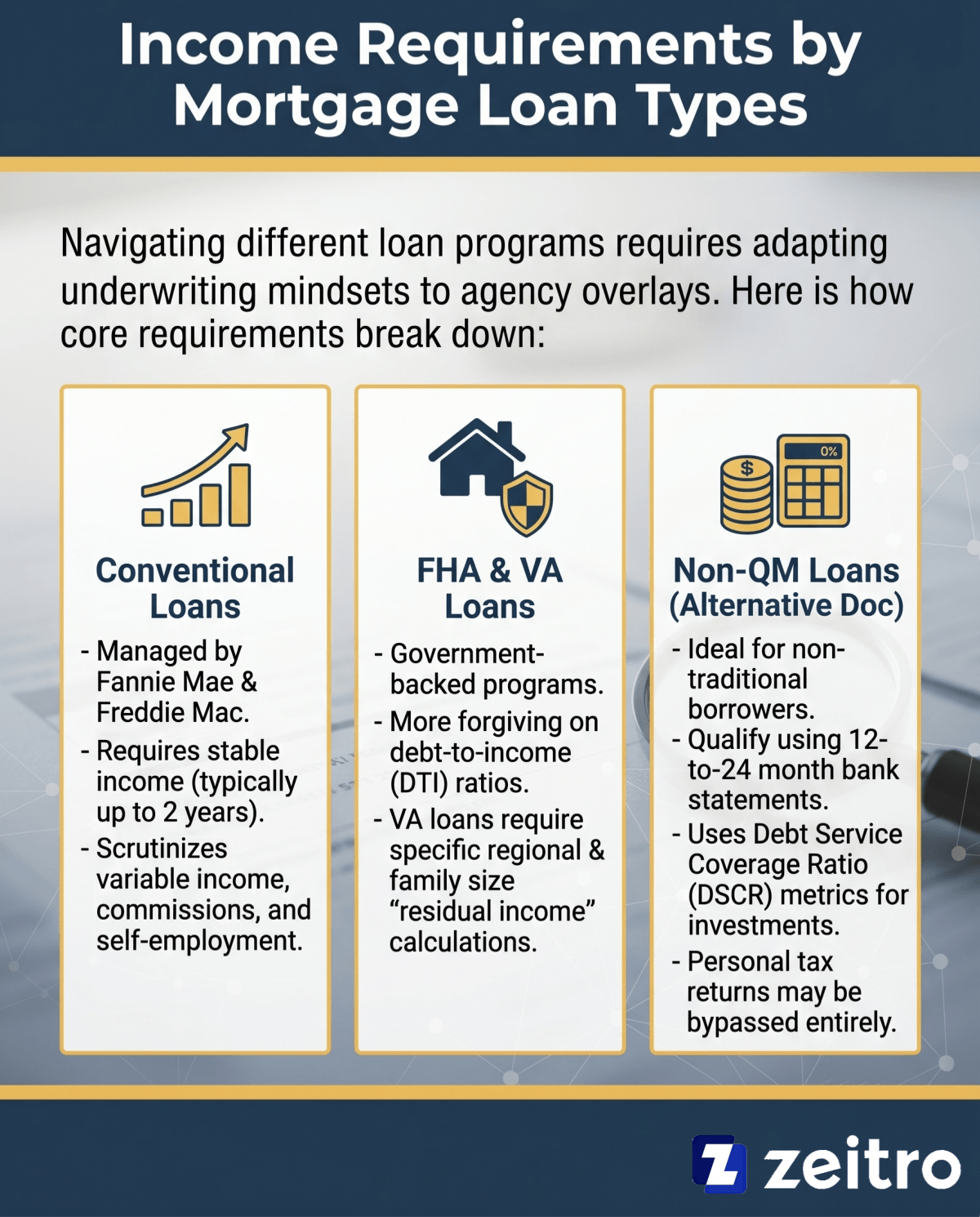

Income Requirements by Mortgage Loan Types

Navigating different loan programs requires us to shift our underwriting mindset based on specific agency overlays. Here is how I break down the core income requirements across different mortgage types:

- Conventional Loans: Governed by Fannie Mae and Freddie Mac, these generally require a stable income history, typically covering up to two years, though exceptions may apply depending on the borrower's profile. They strictly scrutinize variable income like bonuses, commissions, and self-employment.

- FHA & VA Loans: These government-backed programs are slightly more forgiving on debt-to-income (DTI) ratios. However, VA loans add an extra layer of protection by requiring a specific "residual income" calculation based on region and family size.

- Non-QM Loans (Alternative Doc): For borrowers who do not fit the traditional mold, Non-QM programs are lifesavers. They allow us to qualify self-employed clients using 12-to-24-month bank statements or utilize Debt Service Coverage Ratio (DSCR) metrics for investment properties, bypassing personal tax returns entirely.

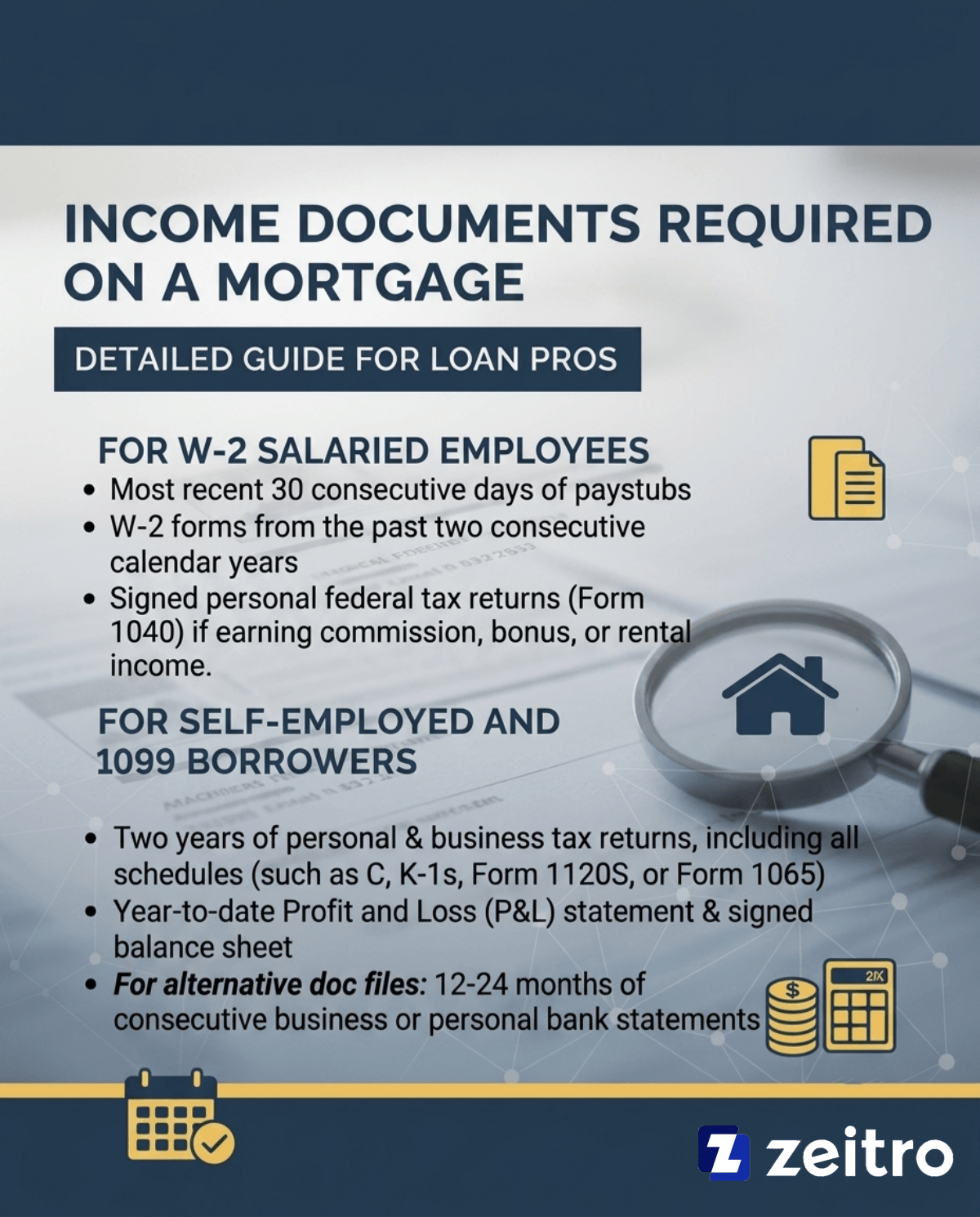

Income Documents Required on a Mortgage

To avoid last-minute delays, I make sure my processing team requests the exact document package upfront. This package depends heavily on how the borrower earns their living.

- Income Verification Documents: A Complete Guide for Employees and Self-Employed

- Borrower Income Analysis: Ultimate Guide for Loan Officers

- What Income Can Be Used for Qualification? Learn Now

For W-2 Salaried Employees:

- Most recent 30 consecutive days of paystubs .

- W-2 forms from the past two consecutive calendar years .

- Signed personal federal tax returns (Form 1040) if they earn commission, bonus, or rental income .

For Self-Employed and 1099 Borrowers:

- Two years of personal and business tax returns, including all schedules, such as Schedule C, K-1s, Form 1120S, or Form 1065.

- A year-to-date Profit and Loss (P&L) statement and a signed balance sheet.

- For alternative doc files: 12 to 24 months of consecutive business or personal bank statements.

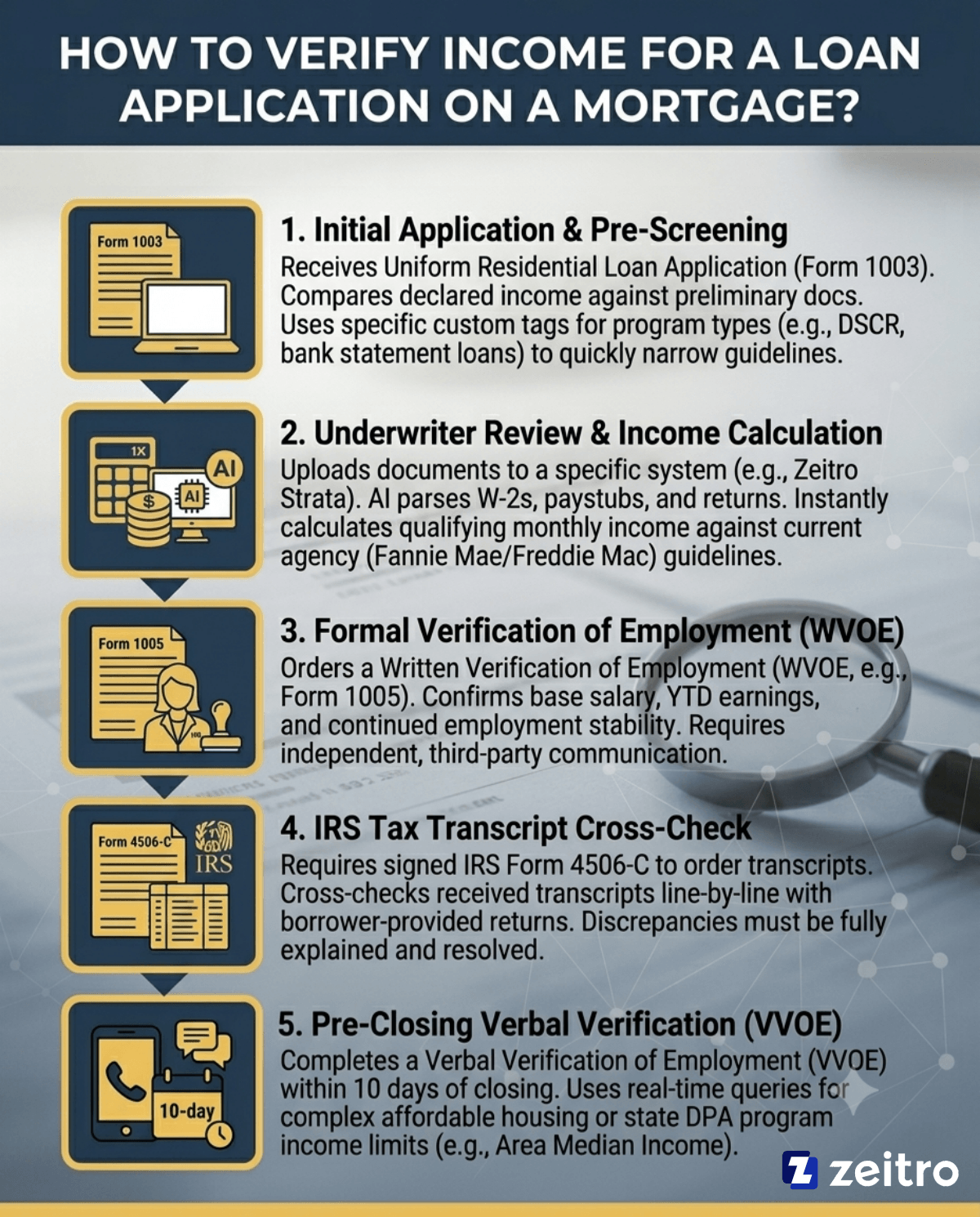

How to Verify Income for a Loan Application on a Mortgage?

Calculated income determines the maximum loan amount a borrower qualifies for, meaning underwriters must follow a rigid, audit-proof sequence. A single oversight on a paystub or tax schedule can trigger a post-closing audit flag. Over my career, I've refined this into five distinct, repeatable steps that keep our files clean, compliant, and ready for a smooth closing.

Step 1: Initial Application & Document Pre-Screening

The process starts when we receive the Uniform Residential Loan Application (Form 1003). I immediately compare the borrower's declared income against their preliminary documents. During this initial triage, I use Zeitro Strata to quickly check multiple investor guidelines.

By using its custom tags for program types like DSCR or bank statement loans, I can narrow down the exact guidelines for the applicant's scenario in seconds instead of digging through individual lender PDF manuals. This keeps us from moving down the wrong loan path early on.

Also Read:

- What Are FHA Mortgage Guidelines? How to Verify FHA & Overlays Quickly?

- Conventional Mortgage Guidelines: What and How to Check Quickly?

- VA Mortgage Guidelines: What Are They and How to Check Them Quickly?

- DSCR Mortgage Guidelines Explained: What and How to Verify?

- Bank Statement Mortgage Guidelines: What Is It? How to Verify?

Step 2: Underwriter Review & Income Calculation

Next, we calculate the qualifying gross monthly income. For salaried earners, this is straightforward, but variable income and self-employment taxes require meticulous averaging. Instead of manually keying numbers into spreadsheets and risking typos, I upload the income documents directly to Zeitro Strata.

Its AI-powered engine automatically parses the W-2s, paystubs, or tax returns to calculate the qualifying monthly income instantly. It even references current Fannie Mae and Freddie Mac guidelines to ensure the calculations are compliant, turning a 30-minute chore into a few seconds of work.

Also Read:

- How to Calculate Self-Employed Income for a Mortgage?

- How to Calculate Employment Income for a Mortgage?

- How to Calculate Mortgage Interest: Manually & Automatically

Step 3: Formal Verification of Employment (WVOE)

We must verify that the borrower's job is stable. I may order a Written Verification of Employment (WVOE), often using forms such as Fannie Mae Form 1005 or other third-party verification services. This document is sent directly to the employer's HR department to confirm base salary, year-to-date earnings, and the likelihood of continued employment. The verification must be obtained through independent, third-party communication to ensure reliability and prevent fraud.

Step 4: IRS Tax Transcript Cross-Check (Form 4506-C)

To prevent mortgage fraud, we require borrowers to sign IRS Form 4506-C. This authorizes us to request tax transcripts directly from the IRS. Once received, I match the IRS transcripts line-by-line with the tax returns the borrower provided in Step 1. Any discrepancies in reported adjusted gross income or write-offs must be fully explained and resolved before we can issue a clear-to-close.

Step 5: Pre-Closing Verbal Verification of Employment (VVOE)

Shortly before closing (typically within 10 days, depending on agency or investor guidelines), we must complete a Verbal Verification of Employment (VVOE). When dealing with complex affordable housing programs or state down payment assistance programs, I also use Zeitro Strata's chat interface. I can query regional Area Median Income (AMI) limits or specific program guidelines in real time to make sure our borrower remains fully eligible right up to the closing table.

How Does Debt-to-Income (DTI) Ratio Matter?

Income verification exists primarily to establish an accurate Debt-to-Income (DTI) ratio. In my experience, even a tiny oversight, like forgetting to deduct a business loss from a self-employed borrower's personal income, can push the back-end DTI past the commonly referenced 45%–50% range for conventional loans, though higher ratios may be approved depending on automated underwriting results.

If the qualifying income is calculated incorrectly, the DTI is wrong, which invalidates the automated underwriting approval and can stall the entire transaction right before closing.

FAQs About Verifying Income

Q1. What causes a delay in income verification?

Delays usually stem from missing tax schedules, unreadable paystub uploads, or slow employer responses to WVOE requests. For self-employed borrowers, failing to provide an updated, signed Profit & Loss statement is the number-one reason files get stuck in processing.

Q2. How do lenders verify employment?

We use direct verification methods. This includes sending Form 1005 to HR, using electronic databases like The Work Number, or conducting a verbal phone verification with the employer's verified business number within 10 days of the note date.

Q3. What are the alternative options to verify income?

If a client has complex taxes with heavy write-offs, we turn to Non-QM options. These include 12-to-24-month bank statement loans, 1099-only programs, asset depletion loans, or DSCR loans for investment properties where personal income isn't verified.

Q4. How do underwriters handle declining income for self-employed borrowers?

If a self-employed borrower's tax returns show a drop in net income from year one to year two, we typically avoid averaging the two years and may be required to use the lower or more recent income, depending on the degree and explanation of the decline. Per agency guidelines, we must use the lower, more recent year's income. If the decline is significant, the loan may be declined unless we obtain a strong letter of explanation and proof of business stabilization.

Q5. Can rental income from a departing primary residence be used to qualify?

Yes, but you must document it carefully. Under current Fannie Mae guidelines, you typically need a fully executed lease agreement and proof of a security deposit or first month's rent check. Lenders generally apply a 25% vacancy factor, allowing you to use 75% of the gross rental income to offset the primary housing liability.

Conclusion

Mortgage income verification is a balancing act between speed and strict compliance. In my day-to-day workflow, I've realized that relying purely on manual lookups and old-fashioned spreadsheets is no longer sustainable. That is why having the right technology in your corner is a game-changer. For loan officers and underwriters looking to simplify this process, Zeitro Strata is a highly effective AI-powered assistant.

It indexes over 1,000 guidelines from 100+ top investors, covering Conventional, FHA, VA, and Non-QM programs like DSCR and bank statements. Strata delivers accurate, citation-backed answers in seconds, significantly reducing the risk of AI hallucinations. With features like automatic income calculation and a free daily tier of 10 queries, it is a practical tool that helps mortgage professionals save time, reduce processing errors, and close more loans with confidence.

Also Try Tools

- Zeitro Mortgage Employment Income Calculator for Loan Pros

- Zeitro Mortgage Affordability Calculator Free and Online

- Zeitro Mortgage Payment Calculator with Interest & Taxes