Written by

Eric

Share this article

.svg)

Subscribe to updates

As an experienced loan officer, I have guided hundreds of families through the borrowing process. Whether you are a borrower trying to secure a home loan or a financial professional assessing risk, having the correct income verification documents is essential for a smooth transaction. This comprehensive guide covers what you need to prepare to prove your earning stability and keep your application moving forward.

Key Takeaway

- W-2 Employees: W-2 employees typically need recent pay stubs and W-2 forms. In some cases, such as recent job changes, lenders may also request an employment verification letter.

- Self-Employed Borrowers: Require federal tax returns, 1099s, and a current profit-and-loss statement.

- Alternative Income: Use complete bank flow records, award letters, or legal decrees to verify payouts.

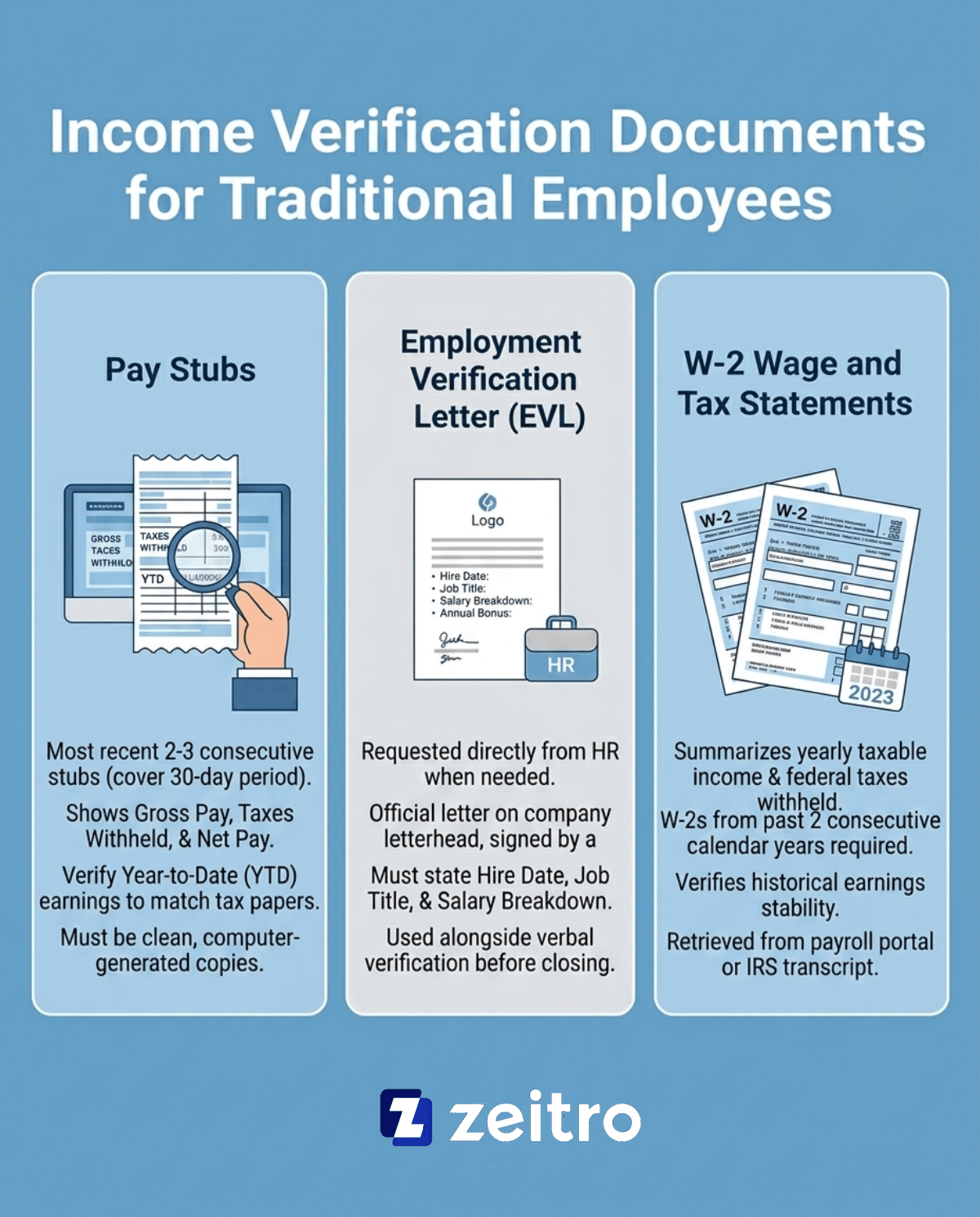

Income Verification Documents for Traditional Employees

If you earn a standard salary or hourly wage, your path to verification is usually straightforward. Lenders prefer traditional employment income because it is highly structured, predictable, and easy to document.

Also Read:

- How to Calculate Employment Income for a Mortgage?

- Ultimate Guide: How to Calculate Monthly Mortgage Payment?

- How to Calculate Mortgage Interest: Manually & Automatically

- How Should I Calculate Income If the Borrower Owns an LLC?

- [Ultimate Guide] How Do I Analyze Self-Employed Tax Returns?

Pay Stubs

When I review a traditional loan application, the very first thing I look for is your pay stubs. These documents show your current gross earnings, taxes withheld, and net take-home pay. Normally, lenders require your two or three most recent consecutive stubs to cover a full 30-day period.

Make sure your pay stubs include "Year-to-Date" (YTD) earnings. Underwriters rely on the YTD figure to verify that your income is steady and matches what is on your tax papers. Hand-written or incomplete stubs are a red flag, so always request clean, computer-generated copies from your payroll portal.

Employment Verification Letter (EVL)

Sometimes, standard pay stubs do not tell the whole story, especially if you recently started a job or changed positions. In these cases, we request an Employment Verification Letter directly from your company's Human Resources department. This official letter must be on company letterhead and signed by an authorized manager.

It should state your hire date, current job title, and salary breakdown, including whether bonuses or commissions are expected to continue. Underwriters typically perform a final verbal verification of employment shortly before closing, often within a few days of the settlement date, so keep your HR contact info up to date.

W-2 Wage and Tax Statements

For salaried workers, W-2 forms are a key reference for verifying historical earnings, typically used alongside pay stubs and employment verification. Your employer generates this form annually, summarizing your yearly taxable income and federal tax withholdings. I usually ask clients for W-2s from the past two consecutive calendar years.

We use them to verify that your income is stable year-over-year. Underwriters check that your name, Social Security Number, and the employer's tax ID match your loan application exactly. If you misplace your copy, you can retrieve it directly from your payroll provider or request an official transcript from the IRS website.

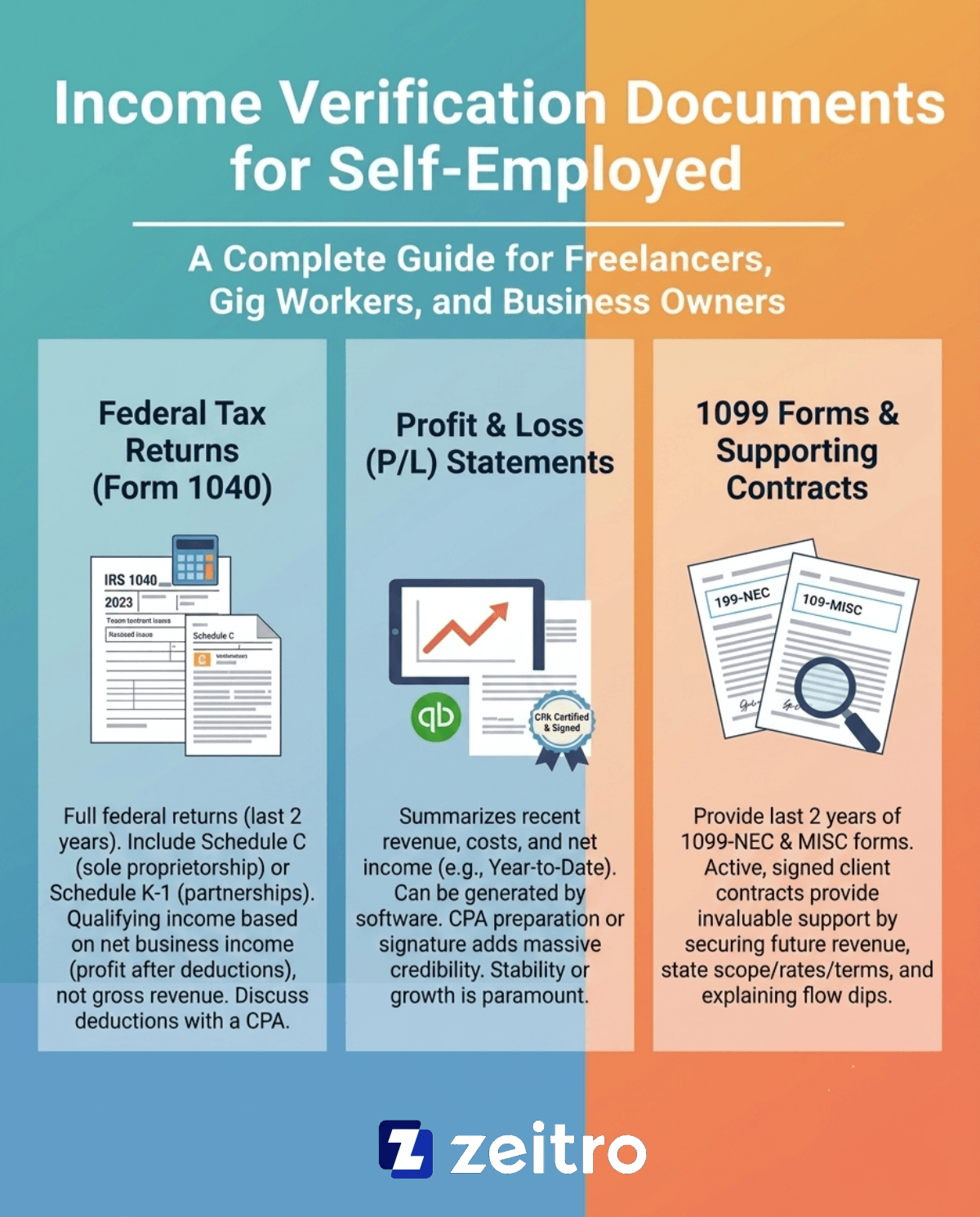

Income Verification Documents for Self-Employed

Proving your earnings as a self-employed individual can feel challenging, but it does not have to be. We look for a complete picture of your business solvency and cash flow stability.

Also Read:

- How to Calculate Self-Employed Income for a Mortgage?

- Gross vs. Net Income for a Mortgage: What Lenders Use & Why

- How to Verify Income for Mortgage: Detailed Guide for Loan Pros

Federal Tax Returns (Form 1040)

If you run your own business, IRS Form 1040 is the foundation of your income verification. Underwriters require your full federal tax returns from the last two years, including Schedule C for sole proprietorships or Schedule K-1 for partnerships.

It is vital to understand that lenders calculate your qualifying income based on your net business income (your profit after deductions), not your gross revenue. If you write off substantial business expenses to lower your taxes, it will also reduce your borrowable income. I always recommend discussing these deductions with your CPA before applying for a major loan.

Profit and Loss (P&L) Statements

Tax returns show us what happened in the past, but a Profit and Loss (P&L) statement shows us how your business is doing right now. This document summarizes your revenues, costs, and net income over a specific recent timeframe, usually the current year-to-date.

You can generate a P&L from accounting software like QuickBooks. However, having a Certified Public Accountant (CPA) prepare or sign off on your P&L adds massive credibility. Lenders want to see that your profits are steady or growing, not declining, to ensure you can easily manage future loan payments.

1099 Forms

If you work as an independent contractor or gig worker, you will receive 1099-NEC or 1099-MISC forms instead of a W-2. These tax forms prove non-employee compensation paid by your clients. I always ask clients to supply their most recent two years of 1099 forms to verify their income stream history.

Underwriters primarily use 1099 forms to verify income sources and amounts, while also considering the stability and concentration of those income streams. If all your income comes from one client, that represents a risk if the contract ends. We match these forms against your Schedule C to confirm that your declared earnings match IRS records.

Also Read:

- 1099 Form vs W2: What's the Difference? Details Here

- Ultimate Guide: How to Get a 1099 Form Online?

Business or Client Contracts

For newer freelancers or businesses with fluctuating monthly revenue, active client contracts are invaluable supporting documents. These signed agreements show that you have secured future revenue. Your contracts should clearly state the project scope, duration, payment rates, and terms of cancellation.

While a contract on its own rarely satisfies a lender's requirements without tax returns, it provides powerful proof of income continuity. I often use client contracts to explain seasonal dips in cash flow, showing underwriters that a borrower has a steady queue of incoming work.

Income Verification Documents for Alternative & Government Income

Not all qualifying income comes from an employer or a business. If you receive government assistance, investment payouts, or pension benefits, you can still secure a loan with the right paperwork.

Also Read:

- Reverse Home Mortgage Explained: Meaning, Requirements, Example

- 8 Highest-Rated Reverse Mortgage Companies for You

- Reverse Mortgage Eligibility: Check Requirements and Criteria Here

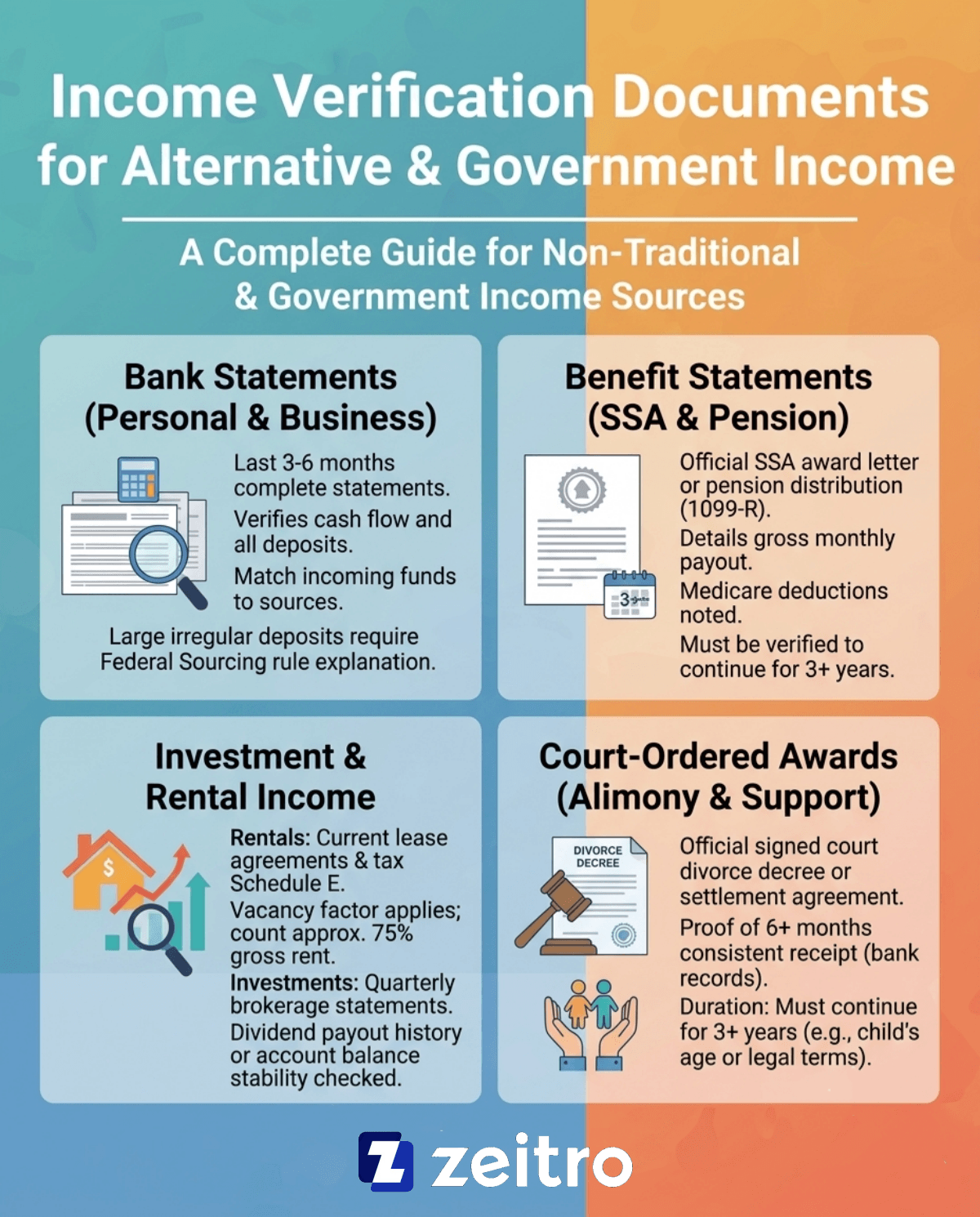

Bank Statements (Personal & Business)

Bank statements are an important tool for verifying cash flow, especially in bank statement loans or non-QM loan programs. Underwriters typically examine your last three to six months of complete, unaltered statements. We check every page to match incoming deposits with your stated income sources, like check deposits or wire transfers.

Be prepared to explain any large, irregular deposits that do not match your normal earnings. Unexplained funds can cause delays, as federal regulations require us to source all money used in a loan transaction to prevent money laundering.

Benefit Statements (Social Security & Pension)

If you are retired or disabled, your income is highly predictable, which underwriters love. To verify this, we need your official Social Security Administration (SSA) benefit award letter or your pension distribution statements (often reported on Form 1099-R).

These documents outline your gross monthly payout and any deductions for Medicare. In my experience, lenders generally require verification that these benefits are expected to continue for at least three years. Fortunately, government benefit letters are considered extremely reliable, making this one of the easiest verification processes to navigate.

Investment or Rental Income Statements

If you earn money from a stock portfolio, retirement accounts, or rental properties, we can use these assets to qualify you. For rentals, we will need your current, signed lease agreements and your tax return's Schedule E.

Be aware that Many lenders apply a vacancy factor, often around 25%, and may count approximately 75% of gross rental income, subject to additional expense adjustments and underwriting guidelines. For stocks and investments, provide your quarterly brokerage statements. We look for a history of consistent dividend payouts or check the overall account balance to ensure long-term stability.

Alimony, Child Support, or Court-Ordered Awards

Court-ordered payments, such as alimony or child support, are fully acceptable income sources. To use them, you must supply the official, signed court divorce decree or settlement agreement.

We also require proof that you have received these payments consistently for the past six months, which you can show using bank deposit records. Just like government benefits, we must verify that the payments will continue for at least three years, usually based on the age of your children or the specific legal terms in your decree.

FAQs About Income Verification Documents

Q1: What is the most widely accepted proof of income?

For most lenders and landlords, recent pay stubs combined with W-2 forms from the past two years are the gold standard. These documents are highly verified, standardized, and easily checked against tax records. For self-employed individuals, a filed federal tax return is the most trusted equivalent.

Q2: How can I prove income if I am paid in cash or do gig work?

If you receive cash or gig payments, you must keep pristine records. Use detailed bank statements to show regular cash deposits, save your 1099 forms, and keep an ongoing log of invoices. Underwriters will match your bank deposits with your annual tax return Schedule C to verify your earnings.

Q3: What must be included in an official employment verification letter?

An official letter must be written on company letterhead and signed by HR or a manager. It must include your full name, job title, exact hire date, salary, and pay frequency. It should also state whether your position is permanent and if overtime or bonuses are regularly paid.

Q4: How far back do lenders look for income verification?

Most conventional lenders look back exactly two years to establish your income stability. This is standard under Fannie Mae underwriting rules. They will average your self-employed net profits over a 24-month period, or verify that your W-2 employment has been continuous during that same timeframe without major unexplained gaps.

Q5: How do I request an official tax transcript from the IRS?

The fastest way is online. Go to IRS.gov, select "Get Your Tax Record," and log in using an ID.me account to download your transcript instantly. Alternatively, if you are applying for a mortgage, you will sign IRS Form 4506-C, which authorizes your lender to retrieve it directly.

Conclusion

In my years as a loan officer, I have seen many borrow applications stall simply because of missing or outdated financial papers. Gathering your income verification documents early is the single best step you can take to ensure a stress-free approval.

Whether you are a W-2 worker printing out your pay stubs or a business owner preparing a CPA-signed profit and loss statement, accuracy is everything. Before you submit your application, do a quick double-check: make sure your names, social security numbers, and addresses match across all documents. Being organized not only speeds up the process but also builds massive trust with your underwriter.