Written by

Eric

Share this article

.svg)

Subscribe to updates

As a loan officer, my heart used to sink when a borrower said they owned an LLC. Calculating income for these clients can feel like hitting a moving target. The trick is knowing how the IRS taxes the entity. To skip this manual headache, you can upload tax documents directly to Zeitro's Income Calculator and automate the entire process.

Key Takeaways

- Tax Classification is Key: How the LLC is taxed by the IRS dictates which schedules and forms we must analyze.

- The 25% Boundary: The 25% ownership threshold generally determines whether the borrower is treated as self-employed for mortgage income analysis under Fannie Mae and Freddie Mac guidelines, but documentation requirements can vary by scenario.

- Paper Adjustments: Non-cash expenses like depreciation and depletion are added back to the net profit.

- Liquidity Rules: To use K-1 ordinary income, you must verify the business has the liquidity to distribute those earnings.

- Automation Saves Time: Utilizing tools like Zeitro automates calculations in line with Fannie Mae and Freddie Mac guidelines.

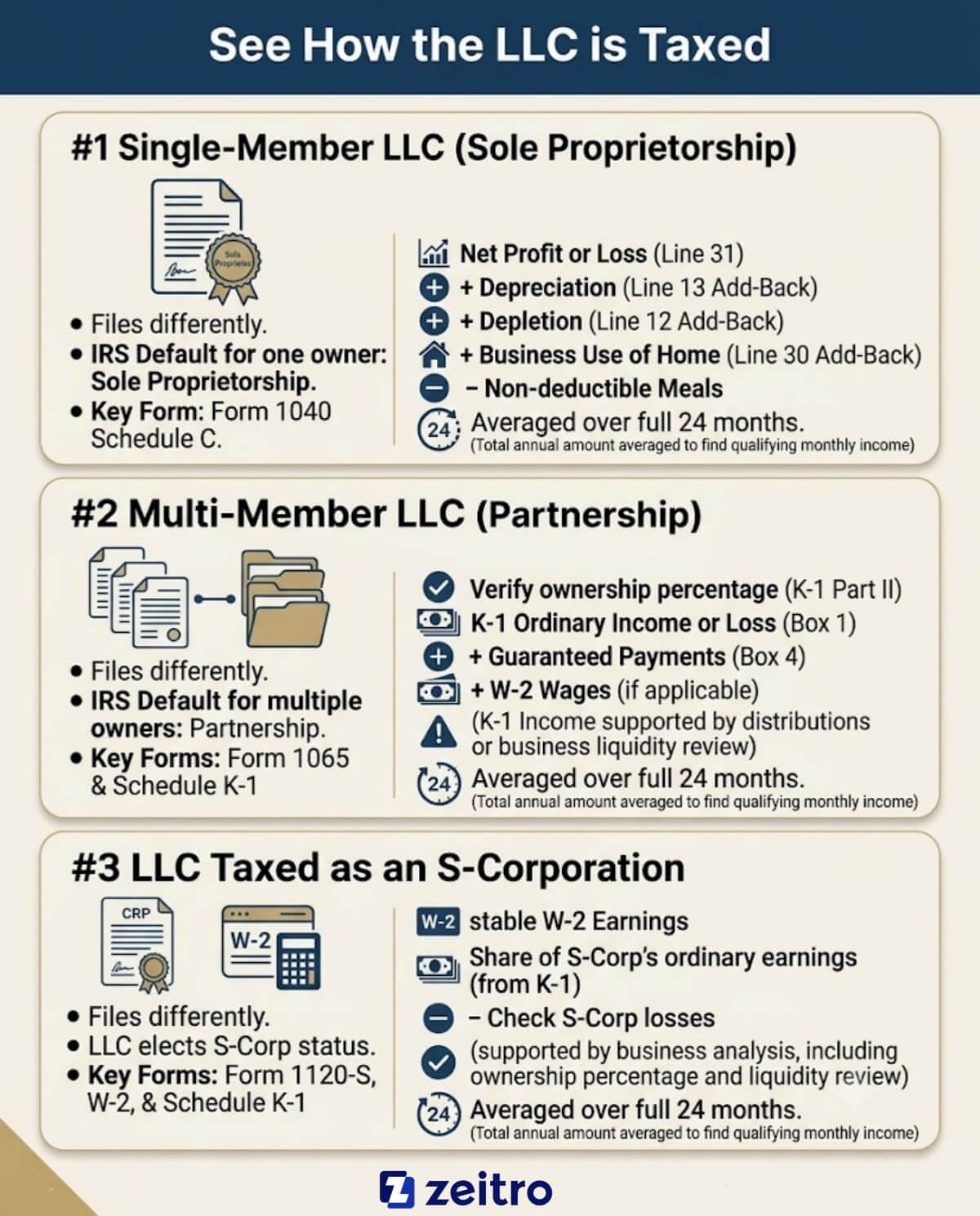

See How the LLC is Taxed

When I first started underwriting, I assumed an LLC was just an LLC. I quickly learned that the IRS does not see it that way. An LLC is a legal structure, but for tax purposes, it can wear many different hats. Before you pull out your calculator, you must identify how the business files its taxes. This choice determines our entire path forward.

#1. Single-Member LLC (Sole Proprietorship)

If your borrower is the sole owner and has not elected corporate status, they are taxed as a sole proprietorship. For this setup, we look directly at Schedule C on their personal Form 1040.

I start calculations at the bottom of Schedule C with the Net Profit or Loss listed on Line 31. Because tax returns focus on minimizing tax liability rather than showing borrowing power, we get to adjust this number. We add back non-cash paper write-offs like depreciation from Line 13 and depletion from Line 12. If they claim a business use of home on Line 30, we typically add that back too, while subtracting any non-deductible meals and entertainment.

The standard calculation is: Net Profit + Depreciation + Depletion + Business Use of Home - Non-deductible Meals = Qualifying Income.

#2. Multi-Member LLC (Partnership)

When an LLC has multiple owners, the IRS defaults to taxing it as a partnership. This means we must examine IRS Form 1065 and the borrower's individual Schedule K-1.

First, we verify the ownership percentage in Part II of the K-1. We look at Box 1 for ordinary income or loss and Box 4 for any guaranteed payments. In my experience, the biggest rookie mistake is blindly using the Box 1 ordinary income. Under Fannie Mae Form 1084 and Freddie Mac Form 91 rules, K-1 income may be used when the lender verifies that the income was actually distributed or that the business has adequate liquidity to support the withdrawal of earnings.

The standard calculation is: K-1 Ordinary Income (if supported by distributions/liquidity) + Guaranteed Payments + W-2 Wages (if applicable) = Qualifying Income.

#3. LLC Taxed as an S-Corporation

Sometimes an LLC elects to be taxed as an S-Corporation. In this scenario, the business files IRS Form 1120-S, and the borrower receives both a W-2 salary and a Schedule K-1.

We must review both documents. First, we pull their stable W-2 earnings. Next, we look at the K-1 to see their share of the S-Corp's ordinary earnings. As with partnerships, S-corp income must be supported by the tax returns and relevant business analysis, including ownership percentage and any required liquidity review. If the S-corp shows a loss, the lender must analyze how that loss affects total qualifying income under the applicable guidelines.

The final calculation is: W-2 Earnings + Borrower's Share of Corporate Earnings - S-Corp Losses = Qualifying Income.

What Lenders Require for an LLC Borrower?

Borrowers with less than 25% ownership are subject to K-1 income guidelines, which are different from full self-employment analysis requirements.

Typically, we must collect:

- Two years of individual federal tax returns (Form 1040)

- Two years of business tax returns (Form 1065 or 1120-S) with all K-1s

- Recent Year-to-Date Profit and Loss statement and Balance Sheet

- LLC Operating Agreement to verify ownership

If tax returns do not reflect the borrower's ability to qualify, some lenders may consider bank-statement loan programs, with documentation requirements that vary by product and lender.

Also Read:

- Income Verification Documents: A Complete Guide for Employees and Self-Employed

- Mortgage Income Verification Guide for Loan Officers in 2026

- How to Calculate Self-Employed Income for a Mortgage?

Bonus Tip: Calculate Income LLC Borrower's Instantly

Manual income calculation for self-employed borrowers is notoriously slow and prone to human error. That is why I recommend trying the Zeitro Mortgage Income Calculator.

This platform allows loan officers and underwriters to bypass complex math completely. You simply upload the borrower's tax documents, and the system extracts and processes the data instantly. Under the hood, the calculator is powered by Zeitro Strata, an advanced AI Guideline Assistant. It automatically cross-references and verifies your borrower's financial data against Fannie Mae and Freddie Mac guidelines. It is a secure, reliable, and incredibly simple tool that ensures your income calculations are compliant and audit-ready in seconds, giving you peace of mind and saving hours of manual underwriting.

FAQs About Calculating Income If the Borrower Owns an LLC

What if the borrower's LLC shows a net loss on tax returns?

If the borrower owns 25% or more of the LLC, a net loss will reduce their qualifying income. We must deduct this loss from their other income sources, averaged over a 12-to-24-month period, to ensure we accurately represent their overall financial standing.

Can I qualify an LLC borrower using only one year of tax returns?

Yes, but only if the automated underwriting system (like DU or LPA) explicitly permits a one-year documentation waiver. Typically, the business must have been active for at least five years, or the borrower must have a strong history in a similar role.

Do lenders add back depreciation for S-Corporations and Partnerships?

Yes. Just like Schedule C sole proprietorships, we can add back depreciation and amortization from Form 1065 or Form 1120-S. However, we can only add back the portion that corresponds directly to the borrower's percentage of ownership in the company.

How do we handle a borrower who owns less than 25% of an LLC?

We treat them as a standard employee. We do not require full corporate tax returns. We qualify them using their personal W-2 wages and any history of K-1 distributions, provided the income is stable and likely to continue for three years.

What can I do if a borrower's tax returns show too many write-offs to qualify?

I recommend looking into alternative mortgage programs, such as a Bank Statement Loan. These Non-QM programs allow us to do a borrower income analysis based on the average monthly deposits into their business bank accounts, completely bypassing their taxable net income.

Final Word

Calculating qualifying income for a borrower who owns an LLC does not have to be an exhausting chore. Once you understand how the business is taxed and which forms to analyze, the puzzle pieces fall into place. However, because guidelines are constantly shifting, relying on manual calculation is a recipe for compliance issues and delayed closings.

I have found that leveraging smart automation is the best way to scale your business. To protect your pipeline and secure accurate calculations instantly, I highly recommend using the Zeitro Mortgage Income Calculator. It keeps your files compliant and lets you focus on what you do best: closing loans.

People Also Read

- What Conditions Will Underwriting Ask for? Get to Know

- What Income Can Be Used for Qualification? Learn Now

- How to Calculate Overtime Income for a Mortgage?