Written by

Eric

Share this article

.svg)

Subscribe to updates

As a mortgage professional, I know the drill. A borrower wants to buy a home, but their tax returns don't tell the whole story of their actual purchasing power. Enter the WVOE. But here's the problem: figuring out exactly which lender accepts what under their specific WVOE guidelines means wasting hours reading PDF matrices. If you're tired of that manual grind, you're not alone.

Later in this guide, I'll show you how I use Zeitro Scenario AI to verify eligibility across different lenders in seconds just by chatting with it. But first, let's break down the fundamentals.

What Does WVOE Mean in a Mortgage?

WVOE stands for Written Verification of Employment. In the industry, we usually just call it Fannie Mae Form 1005. As an underwriter or loan officer, I use this document to confirm a borrower's hire date, current title, detailed breakdown of compensation (base, bonus, overtime), and the likelihood of their continued employment.

For first mortgages, the lender must send Form 1005 directly to the employer, and the completed form must be returned directly to the lender without passing through the borrower. For second mortgages, the borrower may hand-carry the form to the employer, but the employer must mail it back directly to the lender. It's strictly designed this way to prevent fraud and give lenders a clear, verified picture of a borrower's stable income.

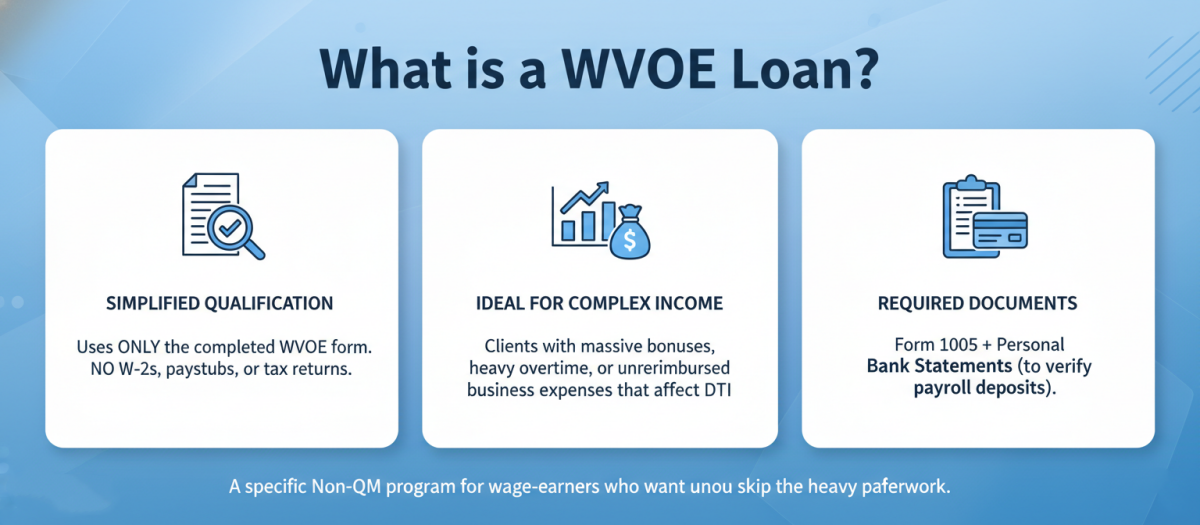

What is a WVOE Loan?

While a WVOE is just a piece of paper used in standard conventional loans, a "WVOE Loan" (or WVOE-Only Loan) is an entirely different beast. It's a specific Non-QM program tailored for traditionally employed wage-earners who want to skip the heavy paperwork.

With this product, you qualify the borrower using only the completed WVOE form. That means zero W-2s, no paystubs, and absolutely no tax returns. I find this program incredibly useful for clients who receive massive bonuses, heavy overtime, or have significant unreimbursed business expenses that ruin their debt-to-income (DTI) ratios on traditional tax filings. Lenders usually just require the Form 1005 paired with a couple of personal bank statements to prove the payroll deposits are real.

What are WVOE Mortgage Guidelines?

Guidelines exist because investors need to mitigate the risk of lending without traditional tax documents. While Fannie Mae has its standard rules, the real complexity lies in the Non-QM space. I've worked with dozens of lenders, and they all have their own unique "overlays" or extra restrictions for WVOE loans.

For instance, underwriters will rigorously vet the employer. The company must be an independently verifiable, legitimate entity. If your borrower works for a family business or holds any ownership shares in the company, they are instantly disqualified. Lenders also look at the consistency of income. If the WVOE shows a sudden, unexplained massive jump in commission right before closing, that's going to trigger conditions. Knowing these granular guidelines upfront is crucial so you don't waste time structuring a deal that will die in underwriting.

Key Requirements of a WVOE Loan

Every wholesale lender has slightly different matrices, but from my experience, the core requirements for a WVOE-only program usually follow a strict pattern to prevent fraud. Here is what you generally need to look out for:

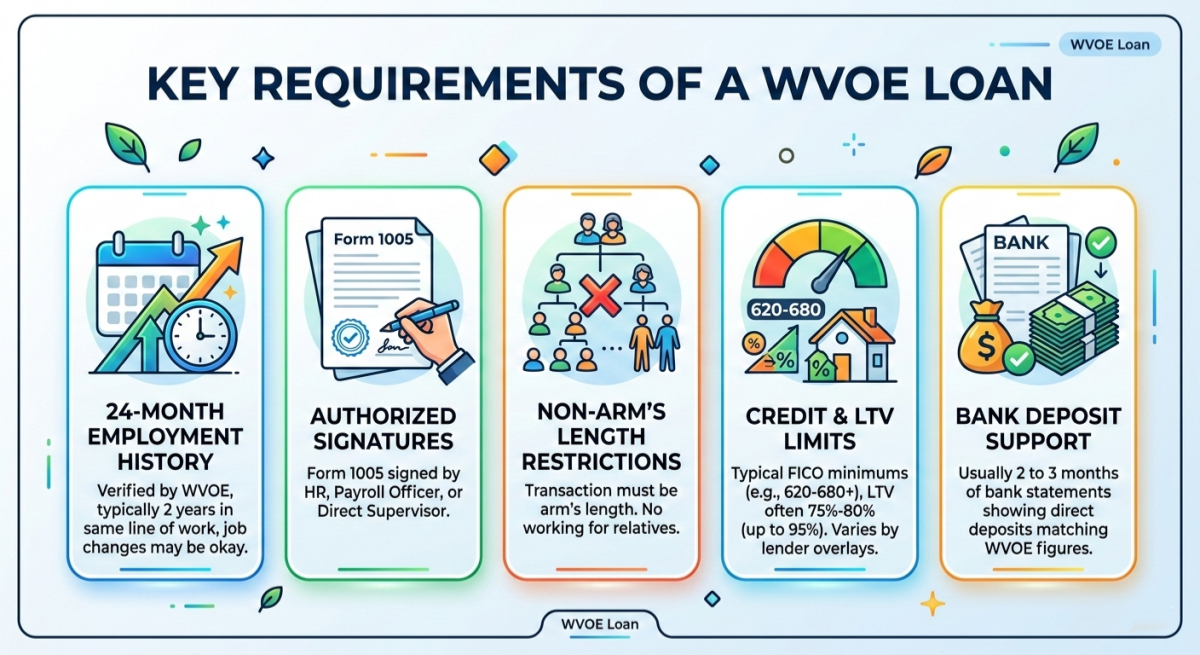

- Two-Year History: The borrower typically needs at least 24 months of employment history in the same line of work with the current employer, as verified by the WVOE. Changes in employer within the same field may be acceptable depending on the lender's overlays.

- Authorized Signatures: Form 1005 must be signed by an official HR representative, a payroll officer, or a direct supervisor.

- Non-Arm's Length Restrictions: The transaction must be arm's length. Working for a relative is a hard "no".

- Credit & LTV Limits: FICO minimums for WVOE loans typically start at 620-680 depending on the lender and program, with LTV ratios often capped at 75%-80% for purchases (up to 95% in some cases with stronger profiles). These vary by specific Non-QM lender overlays.

- Deposit Support: Lenders usually want to see 2 to 3 months of bank statements showing direct deposits that match the WVOE figures.

Bonus Tip: How to Efficiently Verify WVOE Guidelines?

If you're a Loan Officer or Broker, you already know the biggest pain point of Non-QM loans: comparing guidelines. Digging through a 100-page PDF from AD Mortgage or AmWest just to see if your borrower's specific scenario fits is a massive time sink.

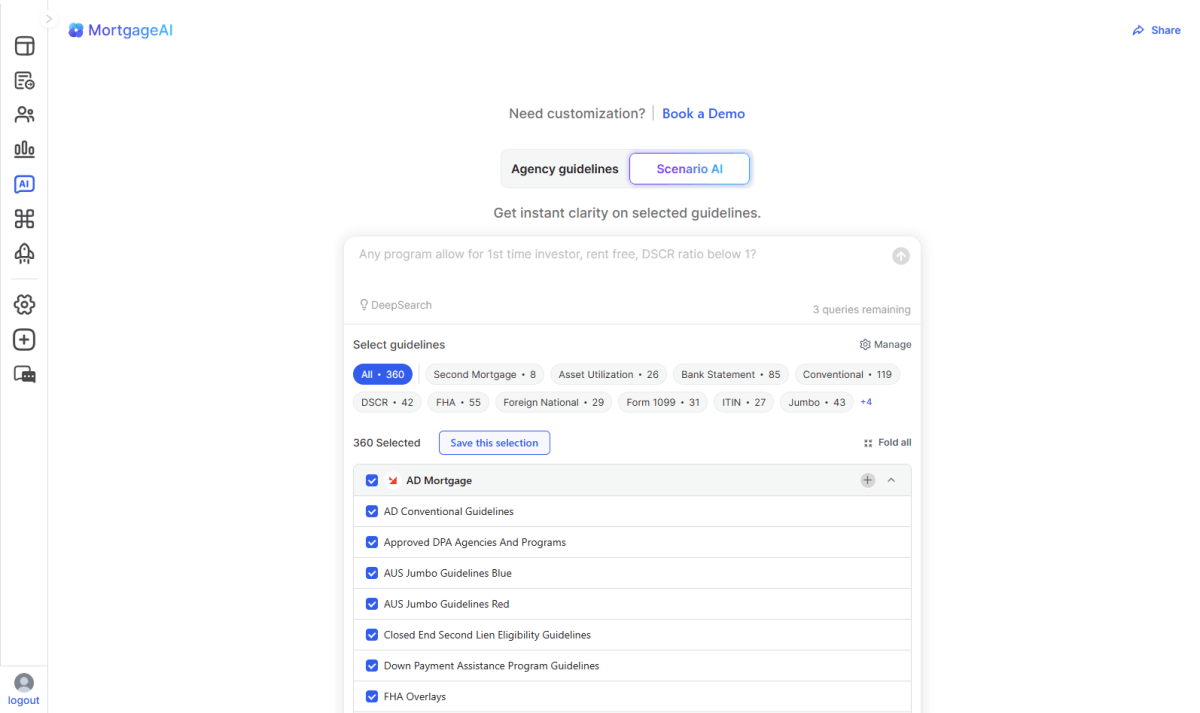

That's why I rely on Zeitro Scenario AI. It's an AI-powered mortgage guideline assistant built specifically for our industry, and it completely changes the way I do my loan research. Instead of hitting Ctrl+F through outdated matrices, you just type your scenario into the chat, and it instantly searches the actual guidelines.

Here's why it's a game-changer for my pipeline:

- Massive & Updated Coverage: It pulls from nearly 300 guidelines, including 35+ specific WVOE programs, from top lenders like Freedom Mortgage, HomeXpress, MK Lending, and AAA Lending.

- High Accuracy with Citations: It doesn't guess. It provides exact citations linking back to the source document, giving you hard proof for your underwriter.

- Lightning-Fast Answers: Ask anything from broad eligibility questions to niche product rules, and get an answer in seconds.

- Deep Explanation Function: If a lender's rule seems confusing, the "Explain" feature breaks it down further based on your selected documents.

- Cost-Effective & Multi-Language: It supports both English and Chinese queries, lets you share results via link, and starts at just $8/month (plus, you get 3 free queries a day).

FAQs About WVOE Guidelines

Q1. How do you obtain a WVOE?

The borrower signs an authorization upfront. The lender then sends Fannie Mae Form 1005 directly to the employer's HR or payroll department. The employer fills out the income and history details, signs it, and sends it straight back to the lender.

Q2. Do I have to fill out the employment eligibility verification?

No. Borrowers are strictly prohibited from filling out any part of the WVOE form aside from the initial signature authorizing the release of information. If a borrower handles, types, or edits the form, the lender will reject the loan.

Q3. What is the difference between VVOE and WVOE?

A VVOE (Verbal Verification of Employment) is a phone call by the lender obtained within 10 business days prior to the note date (closing) to confirm the borrower remains employed. It supplements earlier written verifications like WVOE, which is used during underwriting. A WVOE (Written Verification) is a detailed physical form used early in underwriting to calculate your full income history.

Q4. What are acceptable alternative documents for employment verification?

If a WVOE isn't possible, lenders usually default to traditional full-doc verification using W-2s, 30 days of paystubs, and recent tax returns. Alternatively, many lenders now pull automated verification data directly from third-party databases like The Work Number.

Q5. What are common red flags on an employment background check?

Underwriters actively look for discrepancies. Red flags include white-out marks on the form, round-number income estimates, the employer's address matching a residential home or PO Box, or the HR contact number linking back to the borrower's personal cell phone.

Conclusion

WVOE loans are an incredible tool in the Non-QM space, offering a lifeline to borrowers whose tax returns don't reflect their true purchasing power. However, navigating the strict overlays and shifting requirements of dozens of different wholesale lenders can easily burn hours of your day.

As mortgage professionals, our time is better spent building relationships and closing deals, not acting as human encyclopedias for PDF matrices. If you're ready to speed up your conditions and stop second-guessing your approvals, I highly recommend ditching the manual search. Try Zeitro Scenario AI for free today. It's the fastest way to get exact, citable guideline answers in seconds and keep your pipeline moving.

People Also Read

- 1099 Form Explained: What Is It? What Is Used for?

- 1099 Form vs W2: What's the Difference? Details Here

- Mortgage Guidelines: What Are They? How to Verify?

- Conventional Mortgage Guidelines: What and How to Check Quickly?

- Refinance Meaning: What Refinancing a Mortgage Really Means