Written by

Eric

Share this article

.svg)

Subscribe to updates

Last checked and updated on Auguest, 2026.

The mortgage market in 2026 doesn't forgive slow follow-up. If you're still tracking your pipeline with sticky notes, trusting "gut feel" on guidelines, or living inside a spreadsheet named Leads_Final_V2, you're leaving deals on the table.

I've spent years in loan origination, and the real pain was never just finding leads. It's the speed of conversion and the headache of structuring complex files. We're not just salespeople, we're technicians. A CRM in 2026 has to be more than a digital rolodex that fires off generic birthday emails. It needs to double as your relationship engine and your underwriting assistant.

If all you want is automated email blasts, almost any generic tool will do the job. But if you need real gains in origination speed, especially instant answers on tricky guidelines without digging through 500-page PDFs or waiting on an Account Executive to call back, Zeitro is the one I keep coming back to. It closes the gap between lead management and loan processing better than anything else I've tested this year.

Still, the right CRM depends entirely on where your business actually gets stuck. Here's my breakdown of the strongest options on the market right now.

7 Top CRM Options for Mortgage Brokers

I've demoed, tested, and lived inside most of these platforms over the past few years. The category has moved away from clunky "all-in-one" giants toward sharper, purpose-built tools, some leaning on AI, some leaning on marketing muscle.

Below is my honest read on the leading mortgage CRM software, from AI-driven origination assistants to enterprise marketing suites and the legacy platforms tied to specific loan origination systems.

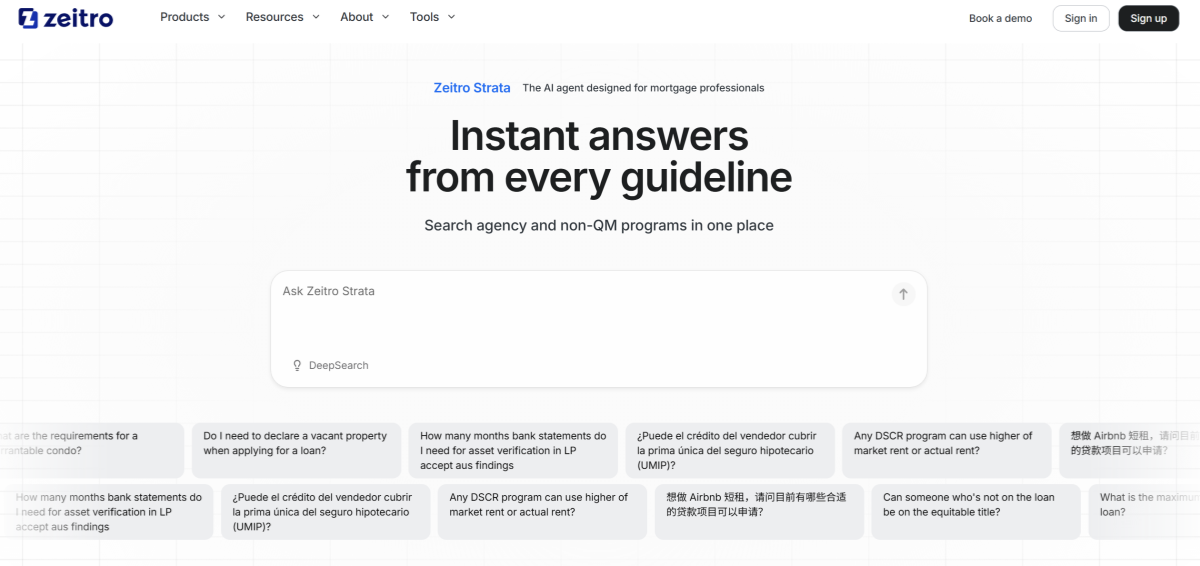

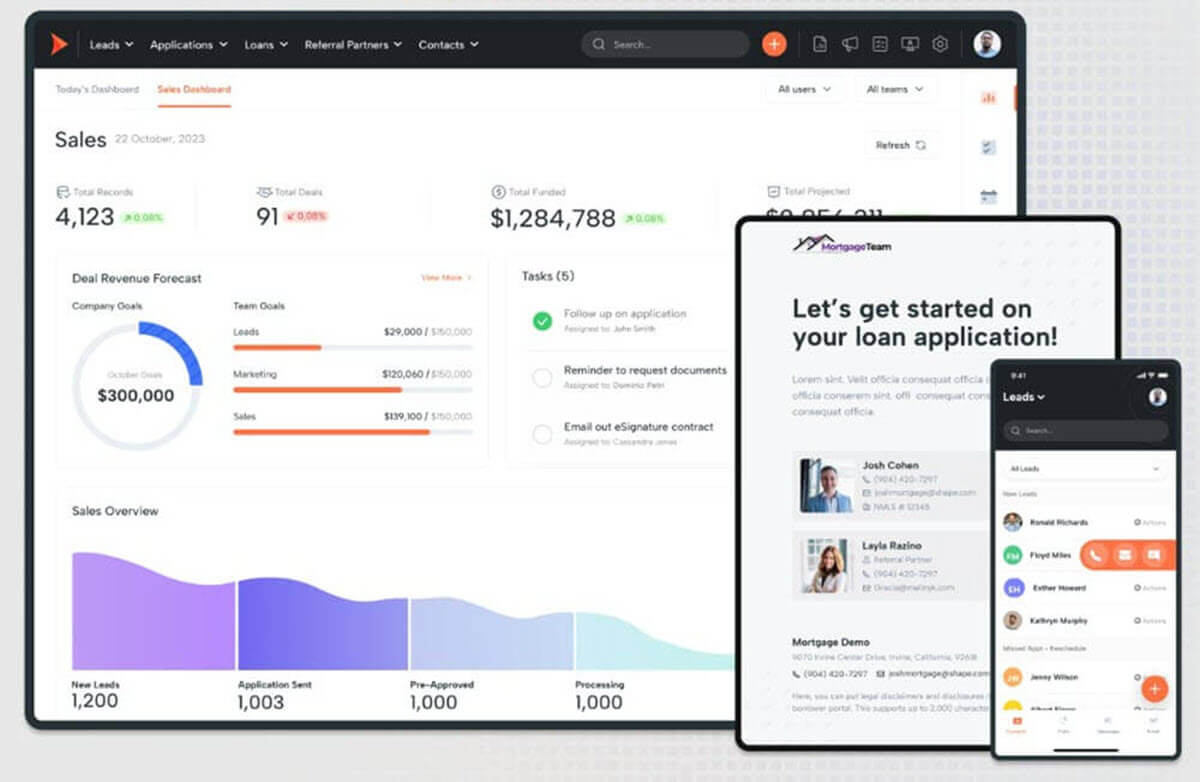

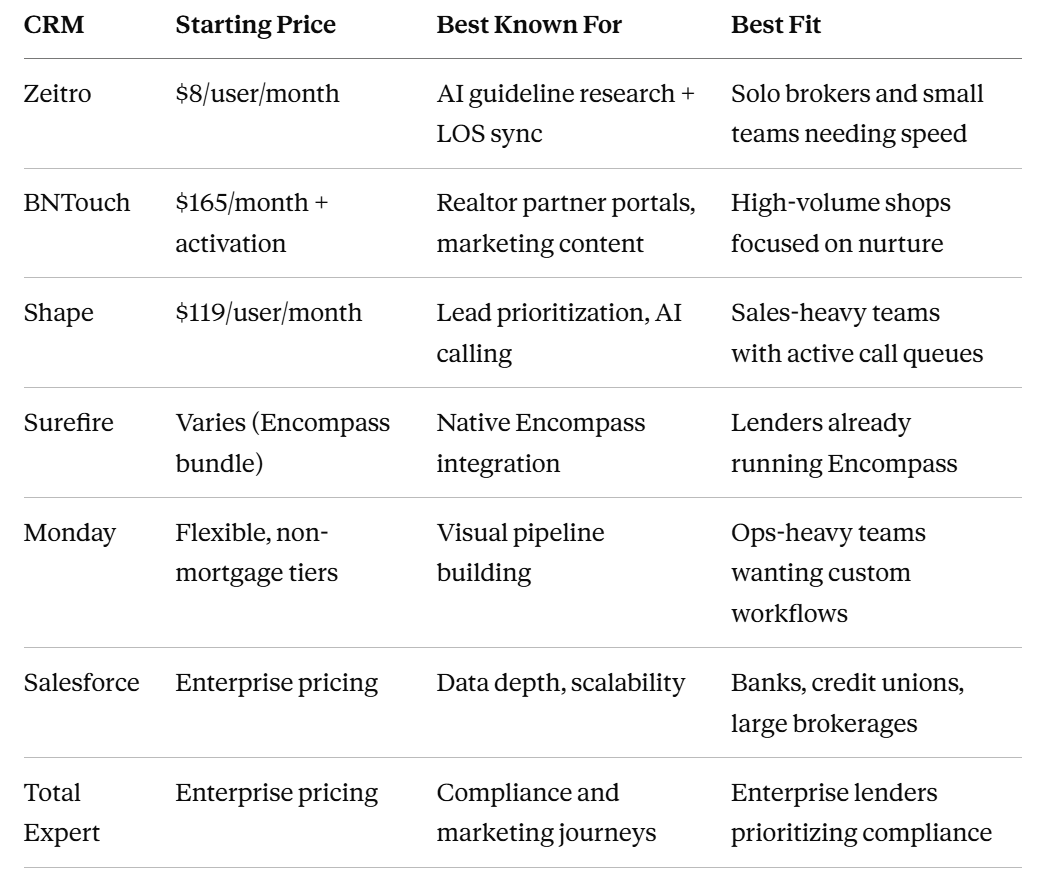

#1 Zeitro: Cost-effective, AI-Powered, and LOS-Integrated

Zeitro doesn't behave like a traditional CRM. While most platforms obsess over drip campaigns, Zeitro built itself around solving the industry's biggest time drain: research. It positions itself less as a marketing tool and more as a next-generation loan origination assistant.

The standout here is Zeitro Strata AI (the guideline assistant formerly known as Scenario AI, rebranded and upgraded in 2026). Every broker knows the drill: a self-employed borrower with a messy income history, or a property type that doesn't fit neatly into any box. Normally that means flipping through matrices or waiting for a callback. Strata AI cuts that out entirely.

Its DeepSearch function cross-checks guidelines from more than 100 investors and covers upwards of 1,000 underwriting guidelines, including agency programs plus Non-QM names like AAA Lending, AD Mortgage, CMG Financial, Freedom Mortgage, and HomeXpress. You type a scenario in plain English, and within seconds you get a sourced, citation-backed answer you can actually verify. It genuinely feels like having a senior underwriter parked next to your desk around the clock.

Beyond the AI layer, Zeitro runs Bluerate, a marketplace built for lead generation. Unlike aggregators that resell the same lead to five different brokers, Bluerate lets borrowers find you directly through your profile and your live rates, so the connection actually starts warm instead of cold.

Pros:

- AI Efficiency: Cuts guideline research time from roughly 30 minutes down to seconds, and many users report saving 7+ hours per loan file on manual lookup work alone.

- Genuinely Low Cost: Runs on a freemium model. The free Explorer tier gives you free queries a day to test it out, and the Individual paid plan starts at just $8 a month.

- Deep LOS Integration: Syncs cleanly with your loan origination system and exports 1003 data in FNM 3.4 format, which cuts down on manual re-entry errors.

- Personal Site: A verified profile on the Bluerate marketplace helps you attract organic borrowers already searching for your specific loan programs.

Cons:

- Brand Recognition: It's newer than legacy names like Salesforce or Total Expert, though its footprint is growing fast, and independent software reviewers have started listing Zeitro alongside established players like Shape and BNTouch in their 2026 mortgage CRM roundups.

- Marketing Depth: Its real strength is origination efficiency and inbound "pull" marketing through Bluerate, not heavy outbound email blasting.

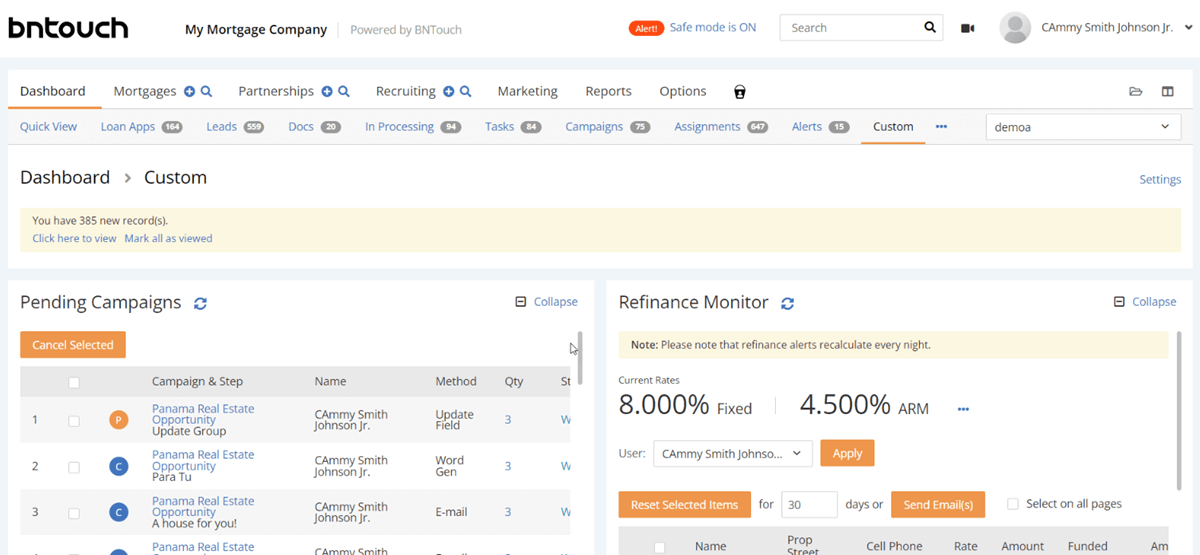

#2 BNTouch: Comprehensive, Scalable, and Strong on Lead Nurture

If your primary goal is pure marketing automation and nurturing realtor relationships, BNTouch remains a heavyweight champion. It is a purpose-built "Mortgage Marketing Ecosystem."

What I appreciate about BNTouch is its Partner Portal. Realtors are needy. They want updates constantly. BNTouch creates a dedicated space where your referral partners can log in and see the status of their leads without calling you. Additionally, their pre-built content library (videos, newsletters) is vast. If you run a high-volume shop where "Leads in, Emails out" is the mantra, BNTouch provides the infrastructure to handle that scale.

Pros:

- Full Marketing Suite: Pre-made content, video marketing, and voice/SMS automation baked right in.

- Partner Portals: A genuinely useful way to keep referral partners in the loop without extra phone calls.

- Solid Mobile App: One of the more functional apps for LOs working from the field.

Cons:

- Dated Interface: The UI feels busier and less modern than newer competitors.

- Learning Curve: So many features are packed in that smaller teams often feel overwhelmed setting it up.

- Pricing: The Individual plan runs $165 a month plus a $125 one-time activation fee, which adds up fast for a solo broker.

#3 Shape: Mortgage-Specific and Increasingly AI-Driven

Shape has evolved fast. What used to be a straightforward mortgage CRM now ships with its own AI layer, including AI-powered lead scoring and calling agents, alongside the lead prioritization tools it built its reputation on.

The core feature that keeps brokers loyal is its prioritization engine. Anyone who's stared at fifty leads and frozen up knows the problem: who do you call first? Shape tracks engagement signals, so if a cold lead suddenly opens three emails and revisits your site, it jumps to the top of your call queue. Combine that with a built-in dialer and a document portal, and you rarely have to leave the platform.

Pros:

- Smart Lead Sorting: Automatically ranks prospects so you're always calling the hottest lead first.

- Modern Interface: Clean, intuitive, and easy for new hires to pick up quickly.

- Built-In Dialer: Calling and texting happen right inside the browser, no extra tab-switching.

Cons:

- Cost Creep: Base pricing sits around $119 per user monthly on an annual plan (closer to $149 month-to-month), and add-ons push that higher quickly.

- Support Variability: Some user reviews mention inconsistent response times from technical support, so it's worth reading the contract closely before signing.

#4 Surefire (ICE Mortgage Technology): Best for Encompass-Native Teams

Surefire deserves a spot on this list simply because so many brokers using Encompass end up evaluating it by default. Originally built by Top of Mind, it passed through Black Knight before landing with ICE Mortgage Technology, and ICE has spent the last couple of years steadily migrating legacy Encompass CRM customers over to it.

The appeal is obvious if you're already inside the Encompass ecosystem: borrower data, loan milestones, and marketing automation sync without any manual export-import work. That said, the platform has had a rocky patch, including a widely reported system error in 2024 that sent an unusually large batch of unsolicited messages to borrowers. Worth knowing going in, and worth asking your rep about directly.

Pros:

- Native Encompass Sync: Practically zero setup friction if your LOS is already Encompass.

- Mature Content Library: Years of refined, mortgage-specific marketing templates.

Cons:

- Ownership Turbulence: Three ownership changes in under four years can mean shifting priorities and support quality.

- Less Ideal Outside Encompass: Brokers on other LOS platforms typically find better-fit alternatives elsewhere.

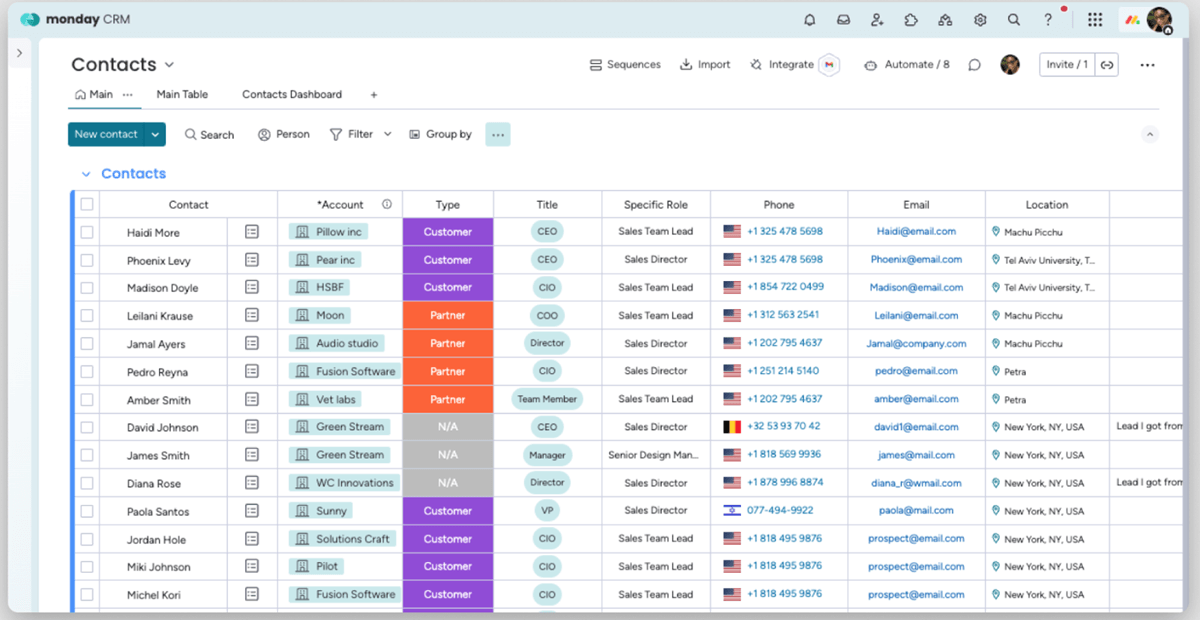

#5 Monday: Flexible and Great for Visual, Team-Based Workflows

Monday isn't built as a mortgage CRM out of the box. It's a work operating system, and for teams tired of rigid mortgage-specific software, that flexibility is refreshing.

I'd recommend it for operations-heavy teams that think in boards and columns. You can build a pipeline that moves a file from application to clear-to-close exactly the way your team visualizes it, and set a column to flag red automatically if an appraisal has been pending more than five days. It's excellent for keeping a team of processors and LOs on the same page.

Pros:

- Visual Pipelines: Best-in-class Kanban and timeline views for tracking loan status.

- Simple Automation: Easy "if this, then that" rules, like auto-emailing a borrower once status flips to Approved.

- Team Collaboration: Strong built-in chat and file sharing on individual tasks.

Cons:

- Not Mortgage-Native: No built-in 1003 fields or guideline data; you're building the CRM logic yourself from scratch.

- Integration Work: Connecting to Encompass or Calyx usually means adding Zapier or a custom API layer.

#6 Salesforce: Deeply Customizable, Built for Scale

Salesforce is the 800-pound gorilla. Specifically, their Financial Services Cloud is a powerhouse. This is the choice for banks, credit unions, or massive brokerages with 50+ LOs and a dedicated IT department.

The power of Salesforce is data. It can track absolutely everything. If you want a dashboard that correlates "Lead Source" with "LTV" and "Average Days to Close" across five different branches, Salesforce does it best. It is infinitely customizable, meaning it can be exactly the mortgage CRM you dream of, if you have the budget to build it.

Pros:

- Scalability: You genuinely won't outgrow it.

- Ecosystem Reach: Connects with nearly every LOS, marketing tool, and email client on the market.

- Reporting Depth: Unmatched analytics and custom dashboards.

Cons:

- Overkill for Small Teams: A shop of one to ten people will likely find it too complex and too costly.

- Hidden Costs: License fees are only the starting point; implementation and admin overhead run into the thousands.

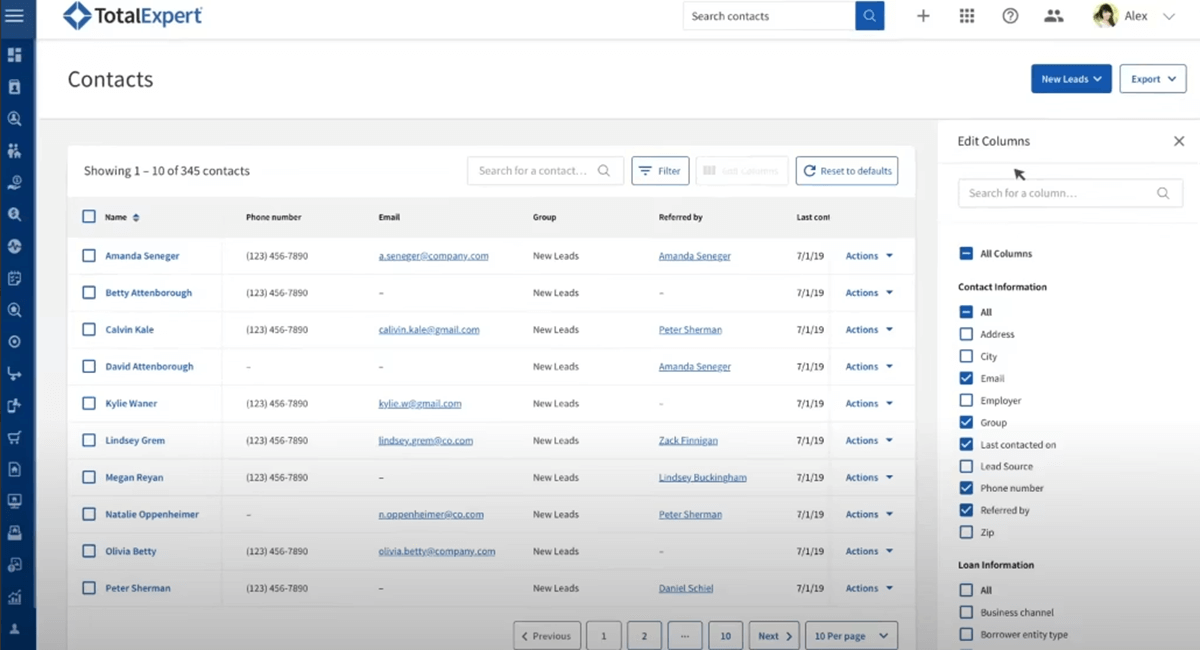

#7 Total Expert: Marketing-First, Compliance-Focused

Total Expert leans hard into customer experience and compliance, which explains why it's popular with lenders who lose sleep over marketing violations.

Its Journey Creator tool is genuinely impressive. You can map out a multi-channel campaign that feels personal, so once a loan closes, it can automatically trigger a five-year "check-in" sequence covering birthdays, refinance alerts, and equity updates, all pre-cleared by your compliance team. It also locks branding down so individual LOs can't go off-script with homemade flyers.

Pros:

- Compliance Guardrails: Among the strongest tools for keeping marketing assets on the right side of regulations.

- Journey Creator: A powerful visual builder for automated, multi-touch campaigns.

- Polished Content: Marketing assets look professionally designed rather than templated.

Cons:

- Enterprise-Skewed: Built for larger lending operations, not solo brokers.

- Heavy Setup: Implementation is a real project, not something you plug in overnight.

A Quick Side-by-Side for Top CRM for Mortgage Brokers

What to Weigh Before You Commit

Before you pull out the credit card, slow down. Too many brokers buy a Ferrari (Salesforce) when a reliable pickup truck (Zeitro) would've done the job. Run through these four questions first.

- Origination support or marketing engine? If your pipeline's already full but you're buried in paperwork and guideline checks, a marketing-first CRM won't fix that. Zeitro's Strata AI is built specifically to cut manual guideline work down to nearly nothing. If leads are your bottleneck instead, lean toward a marketing-heavy tool.

- Does it actually speak mortgage? Generic platforms like Monday have no idea what LTV or DTI means without months of custom setup. Zeitro and Shape both understand mortgage workflows natively, and Zeitro specifically supports direct digital 1003 exports in FNM 3.4 format.

- What's the real ROI? Zeitro starts at $8 a month per user, which is a rounding error if it saves even one hour of guideline research. Enterprise platforms often carry hidden implementation costs that never show up on the pricing page, so always confirm whether a "free trial" is fully functional or a stripped-down demo.

- How do you actually work? If you're meeting realtors in coffee shops all day, a strong mobile app matters more than anything else. If you're a processor at a desk, desktop integration with your loan origination software probably matters more. Pick the tool that matches how you physically get work done.

If You're Outgrowing an Older CRM

A lot of brokers searching for a new mortgage CRM right now aren't starting from zero, they're leaving a platform that's changed hands one too many times. Whiteboard CRM is a good example: since 2022 it's moved from an independent company to Aidium, then rebranded again under new ownership, most recently landing with Lendware in late 2025. That kind of churn tends to mean shifting roadmaps and inconsistent support, even when the underlying product is fine.

If that sounds familiar, it's worth prioritizing a CRM with a clear, stable roadmap and transparent pricing over one riding out its third rebrand in three years. That's exactly the gap Zeitro is built to fill for brokers who want dependable AI-driven tools without corporate musical chairs.

FAQ About Best Mortgage Broker CRM

What's the CRM mortgage companies switch to once they outgrow spreadsheets?

Most brokers move to a mortgage-native platform that combines lead tracking with guideline or pricing tools. Zeitro is a common landing spot because it adds AI-driven guideline research on top of standard CRM basics, without the enterprise price tag.

Is Shape the go-to software, or is there a more complete LOS plus CRM combo?

Shape is strong for lead prioritization and calling, but it isn't a full loan origination system. Brokers wanting both origination support and CRM functionality in one place often pair Zeitro's guideline and pricing tools with their existing LOS instead.

What are solid Total Expert alternatives for compliant, multi-channel campaigns?

BNTouch and Shape both offer compliant marketing automation at a lower price point than Total Expert, though neither matches its enterprise-grade approval workflows. For smaller teams, BNTouch's content library is usually the closer fit.

What should a solo mortgage broker look for in a CRM in 2026?

Low cost, fast setup, and mortgage-specific features like 1003 support and guideline lookup matter more than deep customization at this stage. Zeitro's $8-a-month plan and Strata AI research tool were built with exactly this use case in mind.

Conclusion: What Is the Best CRM for Mortgage Brokers?

There's no single perfect answer here, but there is a right pick for your specific bottleneck.

- Best for Loan Efficiency and AI: If you want to close faster and structure complex files instantly, Zeitro is the clear winner. Strata AI handles Non-QM and agency guideline questions in seconds, and Bluerate adds a genuine lead-generation layer on top.

- Best for All-in-One Marketing: If you need a full marketing suite to keep leads flowing to your team, BNTouch takes it.

- Best for Active Sales Teams: If you've got LOs on the phones all day, Shape's prioritization tools are hard to beat.

- Best for Encompass Shops: If your LOS is already Encompass, Surefire offers the smoothest sync.

- Best for Visual Customization: If you want to build your own process from scratch, Monday gives you the canvas.

- Best for Enterprise: If you're a bank or large lender prioritizing data and compliance, Salesforce or Total Expert remain the standards.

My honest advice: start with Zeitro. The barrier to entry is close to zero, and the time you save on guideline research alone tends to pay for itself within the first week. Figure out whether your real bottleneck is getting leads or processing them, then choose accordingly.

People Also Read

- [Tips] Where to Buy Mortgage Leads? Warm Leads for LOs

- Best CRM for Loan Officers 2026: Which One Suits You Most?

- 8 Best Non-QM Mortgage Lenders in 2026: Which to Choose?

- Full Guide: What is a non-QM Loan? Everything to Learn