![[Guide] What is a Loan Officer License? How to Get It?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a2a4bea3297d243acdd60ca_loan-officer-license-banner.png)

Written by

Eric

Share this article

.svg)

Subscribe to updates

If you want a piece of the massive U.S. mortgage market, getting your loan officer license is your starting point. I remember looking at this process years ago and feeling completely swamped by the weird acronyms and legal talk. It does not have to be that complicated, though. I wrote this guide to cut through the jargon, show you exactly how the license works, and map out the real steps to get yours.

Key Takeaways

- Formal Name: You are technically getting a Mortgage Loan Originator (MLO) license.

- The Big Test: Requires 20 hours of classes and passing the SAFE exam (75% score).

- The Checks: You must pass credit and FBI criminal background checks.

- Sponsorship: Your license only becomes active once a licensed broker employs and sponsors you.

What is a Loan Officer License?

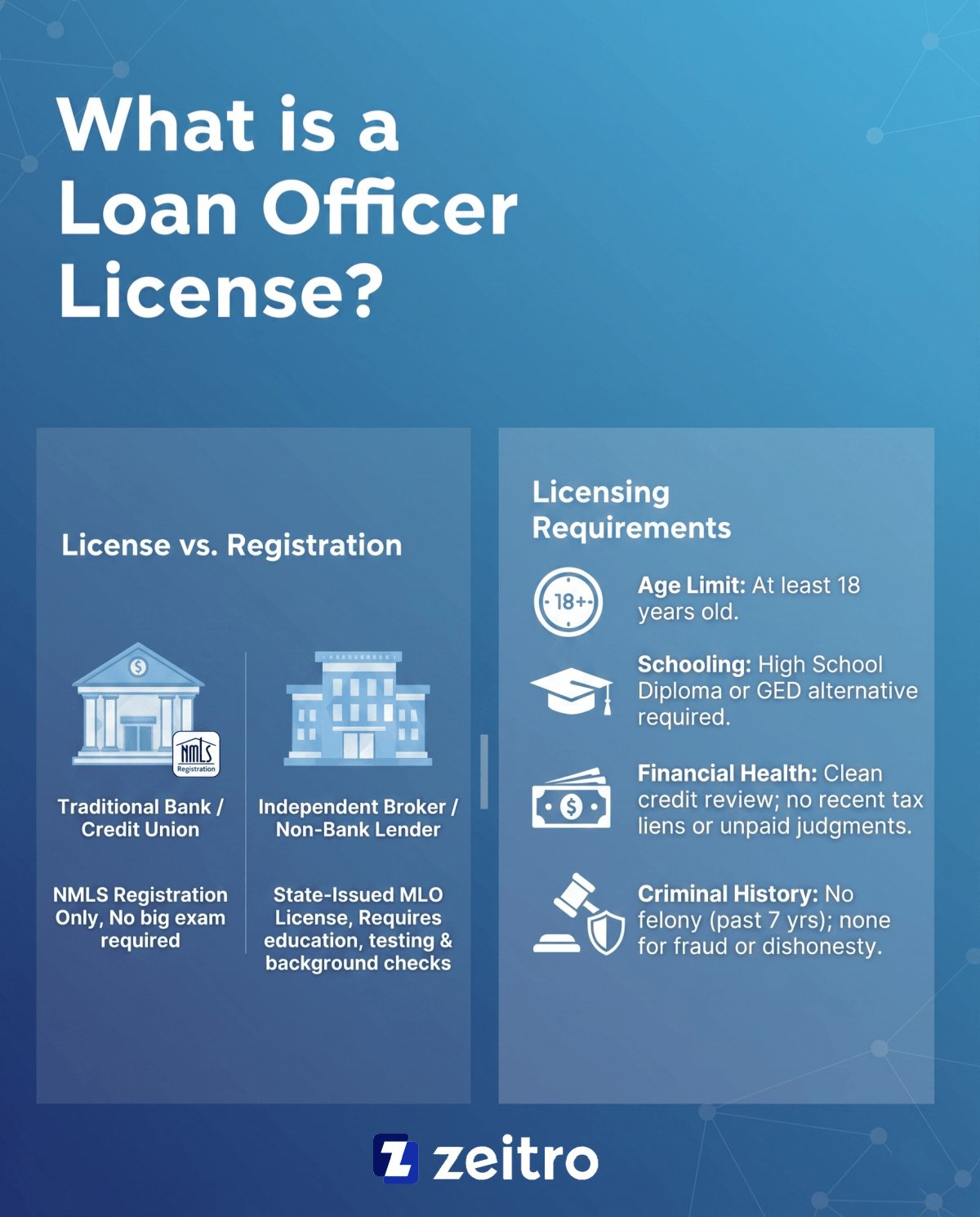

Think of a loan officer license as your legal permission slip to offer, negotiate, or assist consumers with residential mortgages. Officially, the industry calls this role a Mortgage Loan Originator (MLO).

Here is a detail I always warn beginners about: there is a huge difference between being "licensed" and "registered". If you get hired by a traditional depository bank or credit union, you only need to register with the NMLS. You do not have to take the big exam. But if you want to work for an independent mortgage broker or a non-bank lender, where the commissions are often much more lucrative, you absolutely must get a state-issued MLO license. That license indicates you have met the required education, testing, and background-check standards for the state.

Also Read:

- Best Mortgage Companies for New Loan Officers

- Guide: How to Get NMLS License? All the Details

- What are the Duties and Responsibilities of Loan Officers

- Best CRM for Loan Officers: Which One Suits You Most?

Loan Officer Licensing Requirements

Before you spend any money on prep courses, make sure you actually qualify to hold a license under the federal SAFE Act. Most states have similar baseline rules, but you should expect to meet these core standards:

- Age limit: You have to be at least 18 years old.

- Schooling: A high school diploma or GED equivalent is required.

- Financial health: The state reviews your credit report. They want to see financial responsibility, meaning no recent tax liens or unpaid judgments.

- Criminal history: No felony conviction within the past 7 years, and no felony at any time involving fraud, dishonesty, breach of trust, or money laundering.

[Step-by-Step Guide] How to Get a Loan Officer License?

Getting your license follows a strict sequence, but keeping track of the tasks makes it much easier to handle. Here is the process I recommend following:

- Set up your NMLS Account: Head over to the NMLS Resource Center and create an individual account. Once registered, the system gives you a permanent NMLS ID number. You will use this ID as your unique identifier in NMLS records and related mortgage business activities.

- Take the 20-Hour Course: You must buy and complete a pre-licensing education program approved by the NMLS. This program covers 3 hours of federal law, 3 hours of ethics, 2 hours of non-traditional mortgages, and 12 hours of general electives. Double-check your state's rules, because some states require additional state-specific education.

- Pass the SAFE National Test: This is the hardest part. You must register through your NMLS account and take the 120-question exam. You need a score of 75% or higher. The exam has 120 questions, but only 115 are scored. Honestly, about 46% of test-takers fail their first try. My advice? Do not try to wing it—buy a reputable test prep program and drill practice exams.

- Complete the Screening Process: Pay the fees in your NMLS portal to schedule a fingerprinting appointment for an FBI background check. You must also authorize an independent credit report check.

- Find a Sponsoring Broker: Most state-licensed MLOs cannot activate their license without an employing company or broker sponsorship. To activate your license, an employing mortgage company, broker, or other approved financial institution must establish the required relationship and sponsorship. Start talking to local offices while you study so you can land a job quickly.

- Apply and Pay: Once your sponsoring company has established the relationship in NMLS, submit your MU4 application and complete any state-specific requirements. Pay your state's licensing fees, and wait for the state regulator to review and issue your active license.

![[Step-by-Step Guide] How to Get a Loan Officer License?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a2a4c15494957cac842895f_loan-officer-license-steps.png)

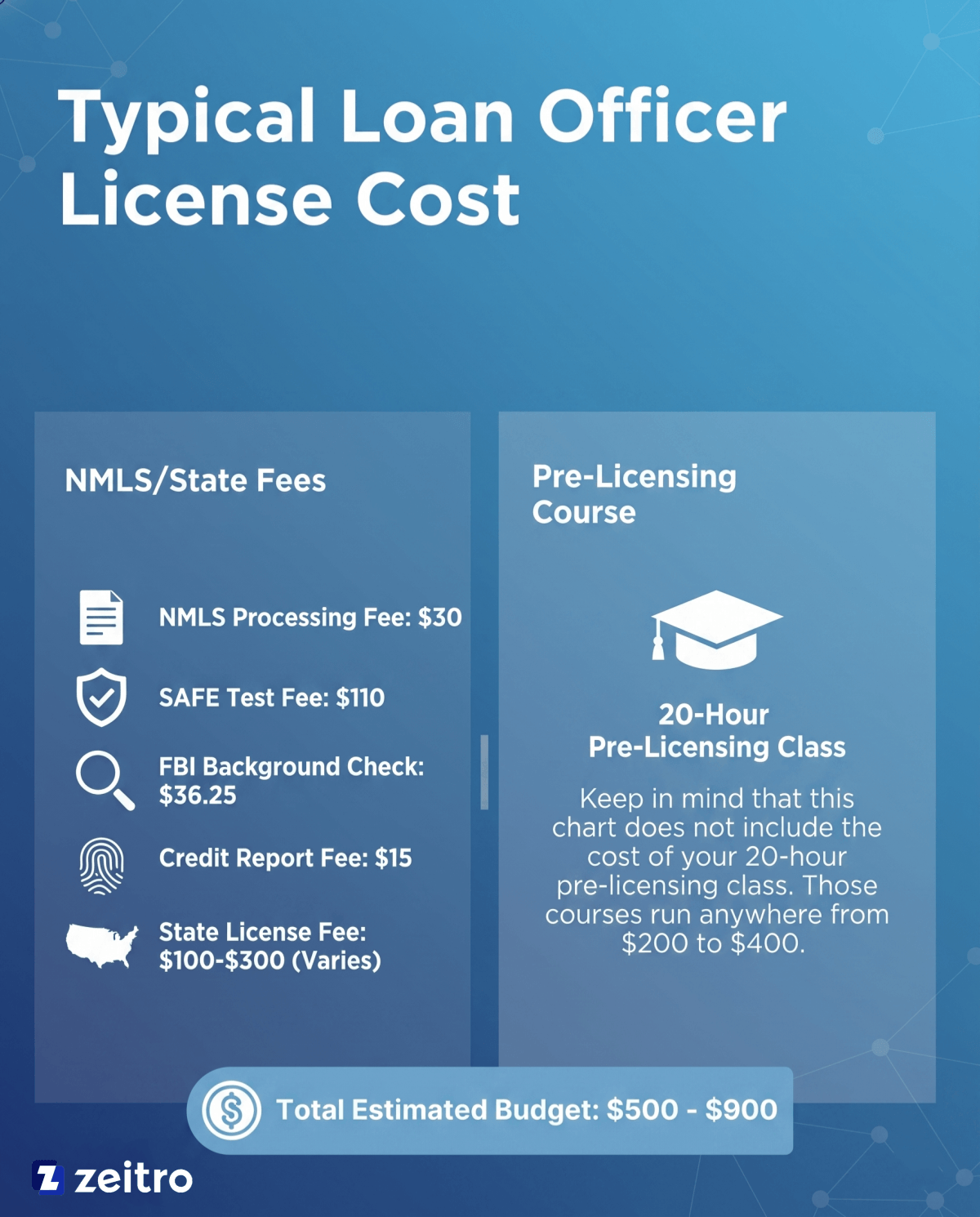

Typical Loan Officer License Cost

Starting a mortgage business is surprisingly cheap compared to other industries. To help you budget, here is what you will pay the NMLS and state agencies:

- NMLS Processing Fee: $30

- SAFE Test Fee: $110

- FBI Background Check: $36.25

- Credit Report Fee: $15

- State License Fee: varies by state, often around $100–$300.

Keep in mind that this chart does not include the cost of your 20-hour pre-licensing class. Those courses run anywhere from $200 to $400. In total, budget around $500 to $900 to get everything up and running.

FAQs About the Loan Officer License

Q1. How hard is it to get a loan officer license?

The actual paperwork is simple, but the SAFE exam is tough. With a first-time pass rate sitting around 55%, it is a notoriously difficult test. You will need to memorize strict federal rules, compliance dates, and math formulas. If you give yourself three to four weeks of focused study, though, you can definitely pass.

Also Read: How to Become a Loan Officer with No Experience?

Q2. How much commission do loan officers make on a $500,000 loan?

Most originators make 1% to 2% of the total loan size. On a $500,000 mortgage, the total fee is $5,000 to $10,000. Just keep in mind that you do not keep all of that. You have to split the commission with your sponsoring broker. If you are on a 50/50 split, you take home $2,500 to $5,000.

Q3. Is getting a mortgage loan officer license worth it?

Yes, if you are a self-starter who loves networking. MLOs enjoy flexible hours and unlimited earning potential without needing a college degree. The catch is that your income depends entirely on commissions, meaning a slow housing market with high interest rates can hurt your wallet. It takes grit, but the upside is huge.

Q4. What is the loan officer license test?

It is officially called the SAFE Mortgage Loan Originator Test. You have 190 minutes to finish 120 multiple-choice questions. Only 115 questions count toward your score. The other 5 are ungraded trial questions. The exam tests you on federal laws (like RESPA and TILA), general mortgage concepts, ethics, and uniform state rules.

Q5. What is the average loan officer salary?

According to the Bureau of Labor Statistics, the median annual pay for loan officers was $74,180 in May 2024. Income can vary widely depending on commissions, market conditions, and performance. Some entry-level spots offer a small base salary of $40,000, but because your real money comes from commission bonuses, there is no limit. Many experienced, hard-working originators consistently pull in well over six figures.

Also Read: Mortgage Loan Officer Salary: How Much Do Loan Officers Make?

Conclusion

Breaking into the mortgage business takes some real effort, but the path is incredibly rewarding if you stick with it. Once you finish your hours, push through the exam, and clear your background checks, you will have a highly valuable credential in your hands.

My biggest piece of advice is to focus heavily on finding a local broker who is willing to train you, rather than just chasing the highest commission split right away. Go ahead and set up your NMLS account today, find your state's specific education requirements, and take that first step toward a new career.

People Also Read

- Best Mortgage Loan Officer Training: Which to Pick?

- Best Mortgage Underwriter Training Online: Improve Your Expertise

- Best Mortgage Loan Processor Training for Beginners

- 11 Best Loan Officer Schools for Newbies: Online & Local

- Loan Officer vs Real Estate Agent: Key Differences to Learn

- Mortgage Lender vs Loan Officer: What's the Difference?

- Loan Officer Requirements: Education, Licensing & Qualifications

- Is There a Loan Officer University for Newcomers?