Written by

Eric

Share this article

.svg)

Subscribe to updates

Buying a home is stressful enough without getting buried in confusing financial jargon. Two terms people constantly mix up are "mortgage lender" and "loan officer." They sound like the same thing, but confusing them will only complicate your financing.

When I work with buyers, I use a simple analogy: the lender is the institution providing the cash, while the loan officer is the actual human who walks you through the application.

Key Takeaways

- The Lender: The financial company (like a bank) that actually cuts the check for your mortgage.

- The Loan Officer: Your main point of contact who gathers your paperwork and guides you.

- The Difference: You borrow the money from the lender, but you work with the loan officer to secure it.

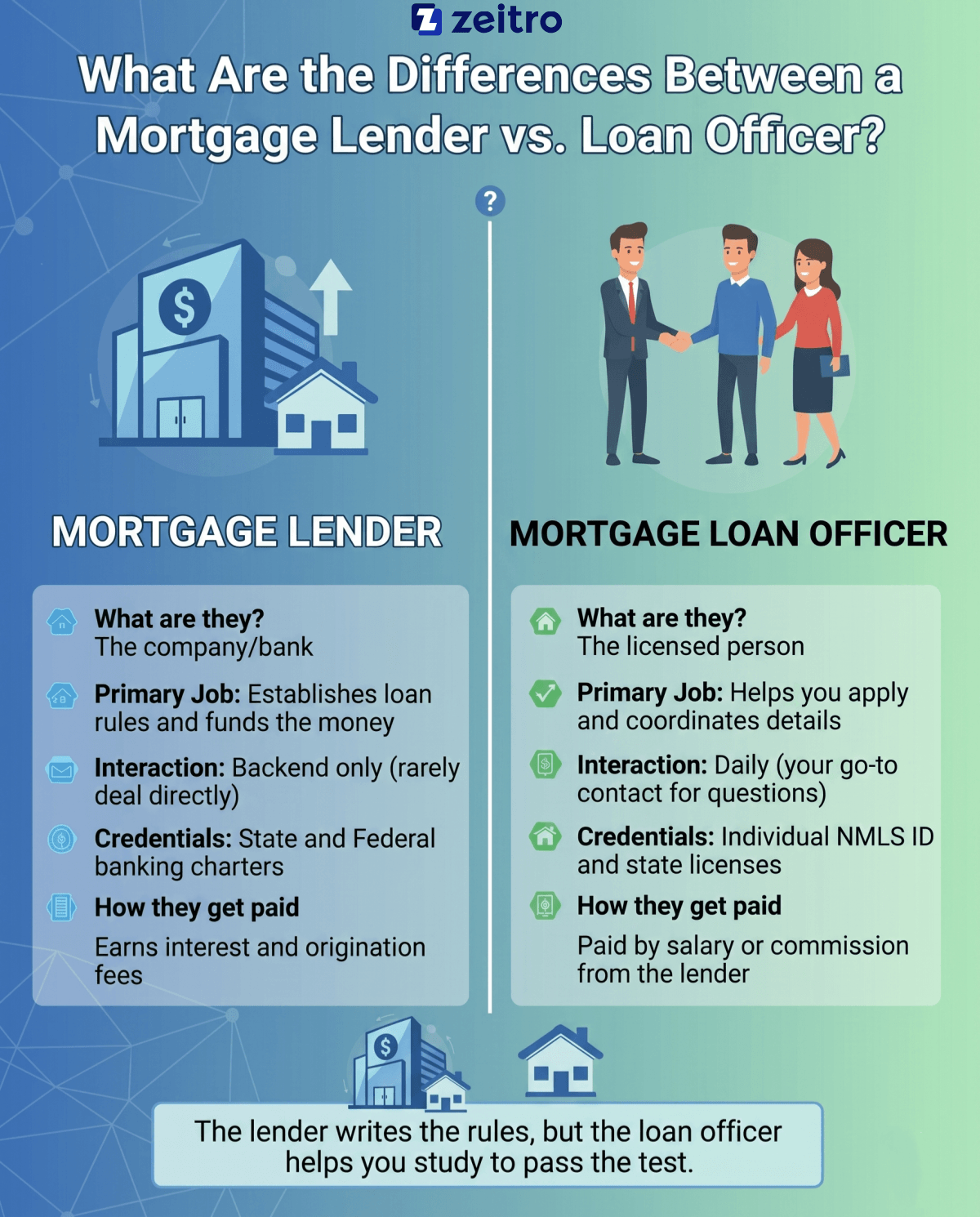

What Is a Mortgage Lender?

A mortgage lender is the financial engine behind your home purchase. You cannot buy a house without a serious source of capital, and that is exactly what the lender provides.

Here is what you need to know about them:

- Who they are: These are financial entities. They can be traditional retail banks (like Chase), local credit unions, or specialized online non-bank lenders.

- What they do: Lenders set the borrowing rules, evaluate your financial risk, dictate your interest rates, and ultimately provide the funds at closing, typically through a settlement or escrow process.

- Their scope: They operate on an institutional level. Once your loan is finalized, the lender (or a servicing company they hire) will collect your mortgage payments for the next 15 to 30 years.

When I help buyers compare options, I emphasize looking at the lender's specific guidelines. Different lenders specialize in different buyers, meaning one bank might reject you while another welcomes your business.

What Is a Mortgage Loan Officer?

A lender is a massive financial entity, meaning you typically do not interact directly with the institution itself, but rather through a representative, such as a loan officer. That is where a mortgage loan officer, often called an MLO, steps in. They are the actual person you talk to throughout the process.

Here is how their role works:

- Who they are: Licensed professionals who work either directly for a lender or as independent agents. They are your personal guide.

- What they do: They pull your credit, help you choose the right loan program (like FHA or conventional), collect your pay stubs, and package your application.

- Licensing: Legitimate loan officers must register through the Nationwide Multistate Licensing System (NMLS). You can search their unique NMLS ID online to check their licensing history.

A great loan officer makes or breaks your experience. They do not approve your loan themselves, but they build the case that convinces the lender to say yes.

What Are the Differences Between a Loan Officer vs. Lender?

To keep your home search moving smoothly, it helps to see how these two mortgage roles line up side by side. Here is a quick breakdown of their main differences:

I always tell my buyers: the lender writes the rules, but the loan officer helps you study to pass the test. Knowing the difference stops you from calling a giant bank's automated line when you should just text your loan officer.

How Do a Mortgage Lender and Loan Officer Work Together?

Think of the lender and the loan officer as a tag team working to get you into your new home. In most cases, they work together to complete a loan, although some lenders use more automated or centralized processes. Here is how they coordinate behind the scenes:

- The Start: You hand your financial paperwork to your loan officer.

- The Hand-off: The loan officer packages your file and submits it to the lender's internal underwriting team.

- The Review: The lender evaluates your file based on its own underwriting standards, as well as applicable investor and regulatory guidelines.

- The Troubleshooting: If the lender needs more proof of income, the loan officer contacts you to sort it out.

- The Finish: The lender approves the file and wires the money for closing.

FAQs About Mortgage Lenders vs. Loan Officers

Q1. Are lenders and loan officers the same?

No. A mortgage lender is the financial institution that actually provides the loan money. A loan officer is the licensed individual who acts as your personal contact and helps you complete the application.

Q2. What is another name for a loan officer?

A loan officer is frequently called a Mortgage Loan Originator (MLO). Depending on the bank, they might also go by Mortgage Consultant, Home Loan Specialist, or Mortgage Representative.

Q3. Does a loan officer work for only one lender?

It depends on their job setup. Retail loan officers work for a specific bank and can only offer that bank's loan products. However, loan officers working as independent mortgage brokers can work with multiple lenders to shop around for you.

Q4. How do loan officers get paid, and do I pay them directly?

Loan officers earn their money through commissions or base salaries paid by the lending institution. You should not pay a loan officer directly as an individual. Legitimate fees are paid to the lending institution or through the official closing process. Any legitimate fees are handled at closing.

Q5. Who should I contact first when buying a home?

Start by contacting a loan officer. They will look over your finances, guide you through your budget, and help you get a pre-approval letter, which is essential before you start touring houses.

Wrap Up

Buying a home is a massive financial step, but breaking down who does what makes the process a lot easier to handle. As you start shopping for a home loan, keep these basic roles in mind:

- The Lender is the corporate bank checking your credit, setting the rules, and funding the mortgage.

- The Loan Officer is your human guide, answering your questions and keeping the paperwork moving.

When you are ready to apply, focus on both sides of the coin. Look for a lender that offers great rates, but make sure you choose a loan officer who communicates well and keeps your stress levels low.

People Also Read

- What is Mortgage Underwriting? A Complete Guide & FAQs

- Mortgage Underwriter vs Loan Officer: Which Career Is Best?

- Loan Officer vs Real Estate Agent: Key Differences to Learn

- Loan Officer Requirements: Education, Licensing & Qualifications

- Is There a Loan Officer University for Newcomers?

- Realtor vs Loan Officer: What's the Difference?