Written by

Eric

Share this article

.svg)

Subscribe to updates

When I first transitioned into mortgage processing, the avalanche of industry acronyms, federal regulations, and complex tax return calculations completely overwhelmed me. I remember scouring Reddit threads where absolute newbies shared my exact anxiety. Shadowing senior staff who effortlessly handled credit lines was helpful, but watching someone else work rarely translates into muscle memory.

To truly bridge the gap between theoretical knowledge and real-world loan files, you need structured training. A systematic approach will help you overcome the steep learning curve and rapidly sharpen your professional skills so you can confidently clear conditions.

Key Takeaways

- Master the Core Fundamentals: Your daily grind requires expertise in auditing URLA 1003s, crunching income data, and satisfying TRID compliance.

- Choose the Right Educational Path: Pathways range from budget-friendly YouTube crash courses to prestigious, paid certifications from the MBA or NAMP.

- Embrace Mortgage Tech: Modern processors rely heavily on AI tools like Zeitro to automate guideline searches and streamline workflows, saving countless hours on file stacking.

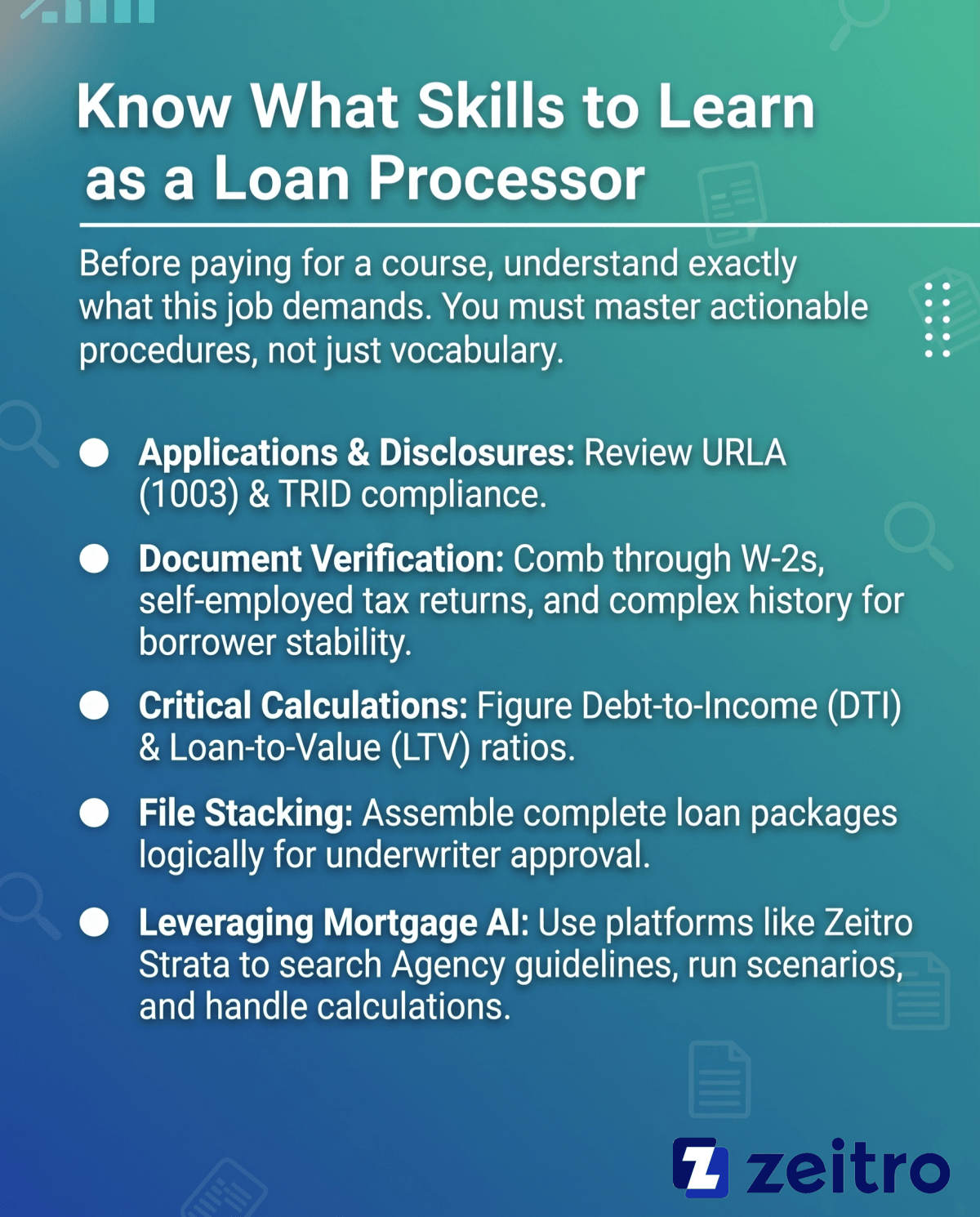

Know What Skills to Learn as a Loan Processor

Before paying for a course, understand exactly what this job demands. You must master actionable procedures, not just vocabulary.

- Applications & Disclosures: You will meticulously review the initial URLA (1003) and guarantee strict alignment with federal mandates like TRID.

- Document Verification: Expect to comb through W-2s, self-employed tax returns, and complex employment histories to prove borrower stability.

- Critical Calculations: You need sharp math skills to accurately figure Debt-to-Income (DTI) and Loan-to-Value (LTV) ratios.

- File Stacking: Assemble the complete loan package logically so the underwriter can approve it without kicking it back.

- Leveraging Mortgage AI: I highly recommend using platforms like Zeitro Strata. It instantly searches all Agency guidelines (Fannie Mae, FHA, VA), runs loan scenarios, and handles income calculations, keeping newbies from drowning in massive PDF manuals.

Also Read:

- [Guide] How to Calculate DTI Ratio for Mortgage?

- Ultimate Guide: How to Calculate LTV Ratio for Mortgage?

- How to Calculate Self-Employed Income for a Mortgage?

- How to Calculate Employment Income for a Mortgage?

- Gross vs. Net Income for a Mortgage: What Lenders Use & Why

Also Try Tools:

- Zeitro Mortgage Employment Income Calculator for Loan Pros

- Zeitro Mortgage Affordability Calculator Free and Online

- Zeitro Mortgage Payment Calculator with Interest & Taxes

Recommended Mortgage Loan Processor Training

The market offers a massive variety of educational resources. Which route you take ultimately depends on your current budget, existing industry experience, and whether you need an employer-recognized certificate to land your very first job. Let's break down the top options.

YouTube (Free)

If you are an absolute beginner with zero budget, this should be your very first stop. When I initially dipped my toes into the industry, YouTube was my saving grace for deciphering the endless sea of mortgage lingo. I suggest typing highly specific phrases into the search bar, such as "how to complete a 1003" or "mortgage processing 101." Many veteran originators and brokers post incredible, screen-share walkthroughs of their daily pipeline management.

However, you must stay vigilant regarding upload dates. Mortgage regulations, agency guidelines, and standardized forms evolve constantly. A video published back in 2019 might feature outdated TRID disclosure timelines or obsolete versions of the URLA. Always filter your search results for content posted within the last twelve to eighteen months to guarantee you are studying the most current lending environment.

Mortgage Bankers Association (MBA)

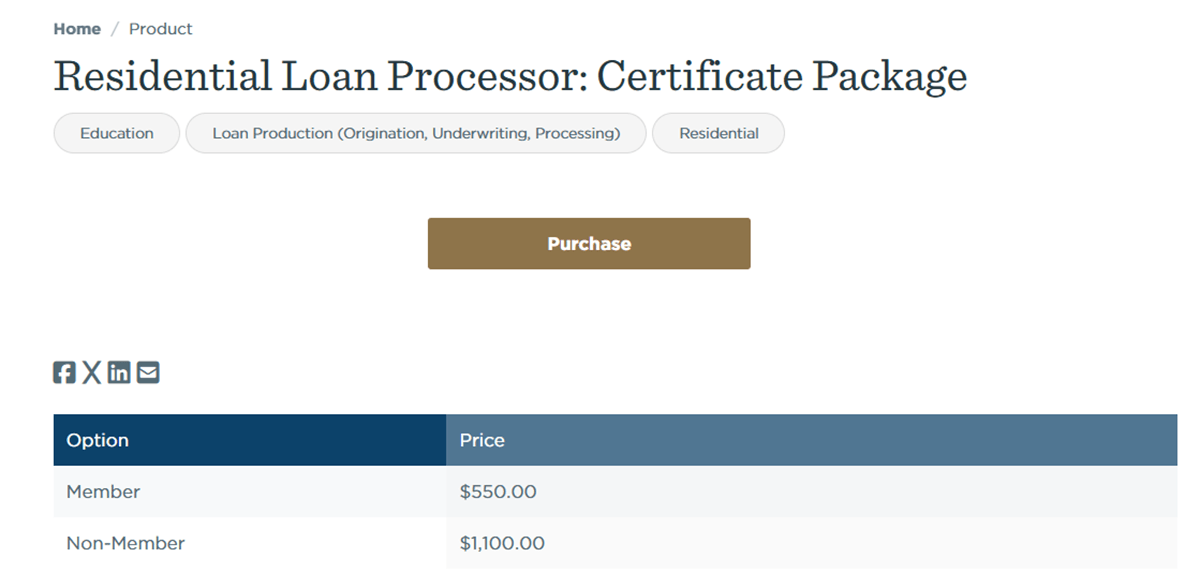

When you are ready to invest in a gold-standard credential, the MBA's "Residential Loan Processor Certificate Package" is widely recognized in the industry, particularly among larger lenders and banking institutions. Pricing is typically around $550 for MBA members and about $1,100 for non-members, though this may change over time.

The program generally includes multiple self-paced modules totaling around 30 hours of study. You will dive deep into foundational origination procedures, property appraisal evaluations, fraud detection techniques, and heavy regulatory compliance. I particularly like how this curriculum bridges the gap between basic data entry and actual risk mitigation. If you are aiming for a corporate role at a major retail lender or traditional bank where formal educational backing dictates your starting salary, securing this specific certificate will give you a massive competitive advantage.

National Association of Mortgage Processors® (NAMP®)

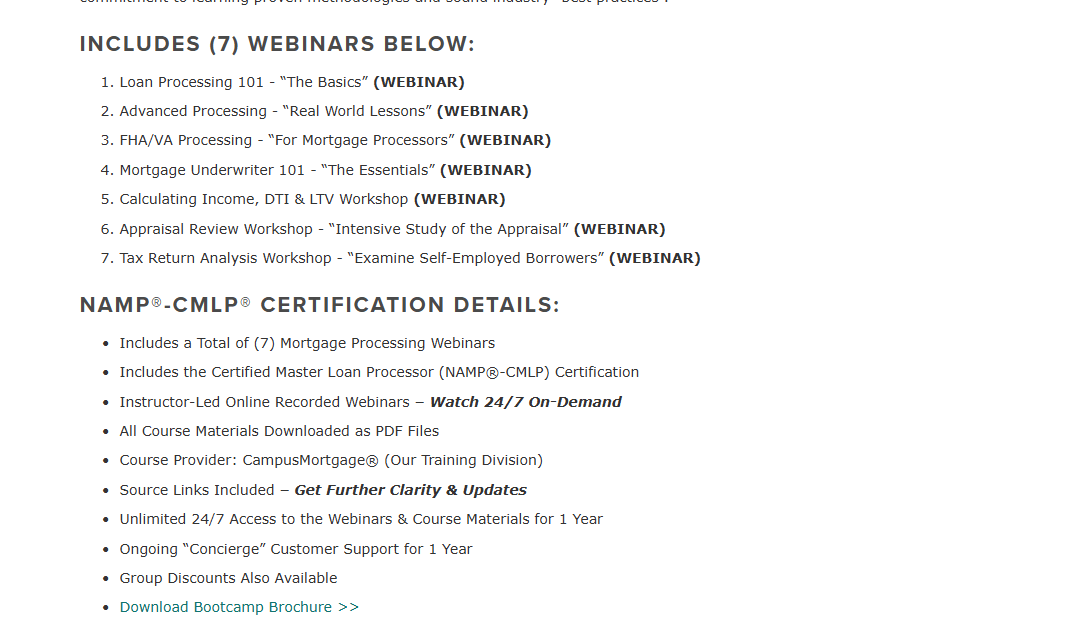

For those who want training hyper-focused solely on the processing niche, NAMP is a well-recognized organization within the mortgage processing niche. Their flagship offering, "The Official NAMP® Processor Boot Camp™," typically runs about $995.

What makes NAMP stand out is their intensely practical, 100% online curriculum. You are not just reading dry compliance text. You learn actionable strategies for FHA/VA file handling and complex tax return analysis. Completing their programs can help you work toward earning the NAMP-CMLP designation, which may require additional experience or qualifications.

I always recommend this specific pathway to anyone looking to make processing a long-term, lucrative career rather than just a stepping stone to underwriting. It proves to prospective wholesale lenders and brokerages that you possess serious, specialized expertise in moving complex borrower files straight to the closing table.

ICE Mortgage Technology (formerly Ellie Mae)

Since Encompass is one of the most widely used loan origination systems in the lending market, learning its specific ecosystem is incredibly strategic. ICE Mortgage Technology offers a phenomenal, quick-hit course typically priced around $63 in 45 minutes.

Usually takeing under an hour to complete, this self-study module won't make you an expert overnight, but it flawlessly illustrates how the processing role physically functions within their proprietary software. The curriculum heavily emphasizes utilizing the Uniform Residential Loan Application (URLA) directly within the LOS. If you recently landed a job at a company running on Encompass, or you know your target employers utilize it, taking this specific training is a no-brainer. It allows you to skip the clumsy software-fumbling phase and immediately start navigating digital files, ordering third-party services, and communicating with underwriters efficiently.

Bank Training Center

If you plan to work inside a traditional depository bank rather than an independent broker shop, the Bank Training Center (partnered with CampusMortgage) is your best bet. Their foundational module, "Loan Processing 101 - The Basics," costs $395, while their comprehensive Boot Camp sits at $995.

I appreciate this platform because it heavily targets the strict banker environment. Beyond teaching you standard DTI and LTV calculations, their curriculum dives deep into the rigid compliance standards unique to banking institutions, such as TRID, HMDA, BSA/AML, and UDAAP regulations. The instructors focus on fixing bad habits and teaching proper file structuring from day one. If your career goal involves handling portfolios for a credit union or a large retail banking entity, this training directly aligns with the rigorous internal audit standards you will face daily.

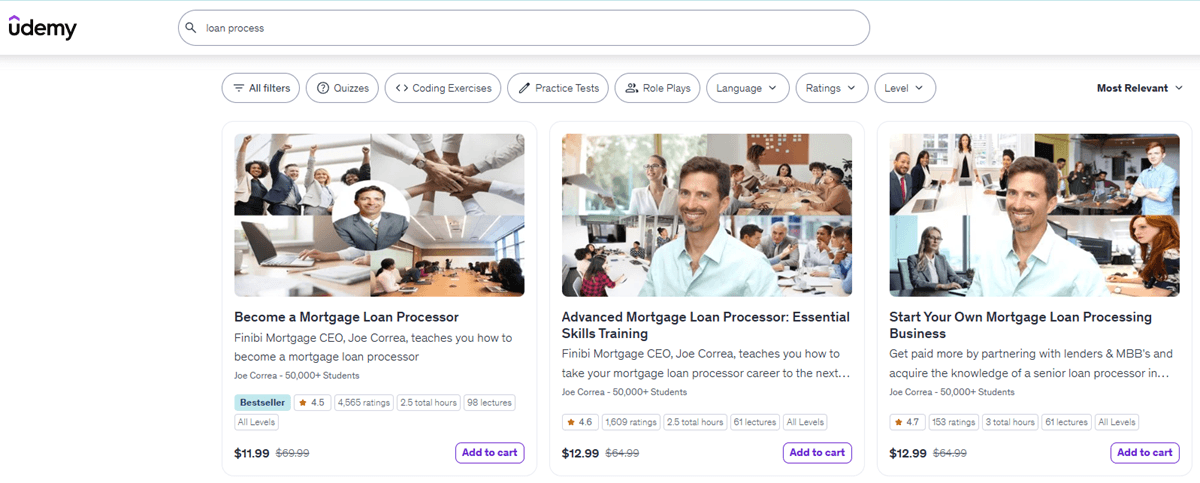

Udemy

When you want structured video learning without spending a fortune, Udemy serves as a fantastic, budget-friendly alternative. Depending on their frequent seasonal sales, you can typically grab comprehensive courses covering mortgage terminology or basic underwriting tasks for anywhere between $15 and $150.

Because anyone can upload a course, the quality varies wildly. You might find a hidden gem taught by a 20-year industry veteran, or a poorly recorded slideshow that barely scratches the surface. Before hitting the purchase button, I highly advise aggressively scrutinizing the student reviews. More importantly, check the "Last updated" date stamped on the course page. If the material hasn't been refreshed since 2025, walk away. The lending landscape shifts too rapidly to risk memorizing outdated loan limits, automated underwriting system (AUS) rules, or legacy disclosure timelines.

Considerations Before Starting Mortgage Loan Processor Training

Before committing to a specific program, weigh these crucial factors so you don't waste time or money:

- Your Budget: Determine if you should exploit free introductory content first or if you are financially ready to drop $1,000+ on a prestigious industry designation.

- Target Career Path: Are you aiming for a retail bank, a wholesale lender, or working as a 1099 independent contractor? Depository banks require vastly different compliance knowledge compared to nimble brokerages.

- Company Tech Stack: Find out what software your future employer uses. If they are locked into Encompass, prioritize ICE's official platform training over generic alternatives.

- Licensing Requirements: Depending on your state and employment type, you might need an active NMLS license. W-2 employees at direct lenders usually don't need one, while independent contract processors typically do.

FAQs About Mortgage Loan Processor Training

Q1. Do I need a license to be a mortgage loan processor?

Generally, if you work as a W-2 employee directly for a bank or direct lender, you do not need an individual license. However, requirements vary by state. In some cases, independent contract processors may need an NMLS license, especially if they perform loan originator activities

Q2. How long does it take to complete loan processor training?

It entirely depends on the platform's depth. Short software introductions, like those from ICE, take roughly 45 minutes. Conversely, comprehensive certification tracks from the MBA or NAMP demand around 30 hours of rigorous study, which might take several weeks to fully absorb.

Q3. Are paid mortgage loan processor courses worth it?

Yes, absolutely—especially if you leverage MBA or NAMP credentials to negotiate a higher starting salary or secure a promotion. However, if you are a total novice who cannot yet define basic industry acronyms, stick to free resources until you are certain this career fits you.

Q4. What is the best loan origination software (LOS) to learn?

Encompass, developed by ICE Mortgage Technology, remains the undisputed industry heavyweight and is used by many large lenders and financial institutions. Understanding its interface gives you a massive hiring advantage. Other prominent systems worth exploring include Calyx Point and Arive, which are incredibly popular among independent mortgage brokers.

Q5. Is loan processing hard for a beginner?

The initial learning curve is notoriously steep due to the aggressive compliance rules, complex tax return math, and endless acronyms. Yet, by completing structured training and utilizing modern AI tools to interpret guidelines, many people can become comfortable in the role within a few months, though mastery often takes significantly longer depending on deal complexity.

Conclusion

Stepping into the mortgage industry doesn't require emptying your wallet on day one. I always advise newcomers to hold off on spending cash immediately. Start by searching YouTube for walkthroughs on completing the 1003 and basic lingo tutorials. Once you feel confident you actually enjoy the workflow, invest in authoritative credentials from NAMP or the MBA to boost your resume.

Most importantly, succeeding in 2026 means embracing technology. Knowing how to calculate income manually is great, but leveraging AI platforms like Zeitro Strata to cross-reference agency guidelines instantly will separate you from the pack. Master the fundamentals, lean heavily on modern tech tools, and you will quickly transform from a nervous newbie into a top-tier loan processor.

People Also Read

- Max DTI for Mortgage: Requirements By Loan Types

- Max LTV: Check Maximum Loan-to-Value Ratios By Loan Types

- Mortgage Income Requirements: Learn Before You Apply

- Guide: How to Calculate Gross Income for a Mortgage?

- Explained: What is a Bank Statement? Everything to Know

- [Guide] Loan Origination Explained: Meaning, Process, Cost