Written by

Bochen W.

Share this article

.svg)

Subscribe to updates

Walk into any modern lending office and you’ll see it: loan origination isn’t what it used to be. Years ago, stacks of paper and endless phone calls ruled the day. Now, the real heavy lifting is digital, invisible, and—if you pick the right tools—almost effortless. For lenders, brokers, and credit unions, the real question is no longer “Should I go digital?” but “Which loan origination system vendor truly fits my needs?”

Before diving into system demos, map out your business’s top priorities. Consider your lending product mix, expected integration with other platforms (such as CRM or accounting software), regulatory compliance needs, automation level, and your team's ability to adapt to new technology. A smart selection process starts with a clear understanding of what you want—and what you can live without.

Let’s take a thoughtful stroll through today’s LOS vendor landscape, with a critical eye for both time-tested players and the new AI-driven contenders changing the rules.

List of Loan Origination System Vendors: Market Landscape & Trends

What Are Loan Origination Systems and Why Do They Matter?

Every lender has their own rhythm, but the best LOS platforms share a purpose: streamline the journey from first borrower inquiry to funded loan. These systems cut manual work, improve compliance, boost accuracy, and keep sensitive information secure. The right LOS can turn weeks of back-and-forth into a few swift clicks, freeing up teams to focus on building relationships—not wrestling with paperwork.

When evaluating LOS solutions, don’t just focus on the features list. Make sure the platform offers robust data security, user management, integration with your core banking systems, and the flexibility to support evolving business needs. Ask about the process for workflow customization and whether the system can scale as your business grows. Pay special attention to how each platform handles compliance, as regulations are only getting more complex.

We’re not just talking about simple software for filling out forms. Today’s LOS is a full-fledged digital command center, managing data, automating communication, integrating with banking systems, and keeping regulators satisfied. The world of LOS has grown up fast, and so have the expectations.

Top LOS Vendors: Comparing the Big Names

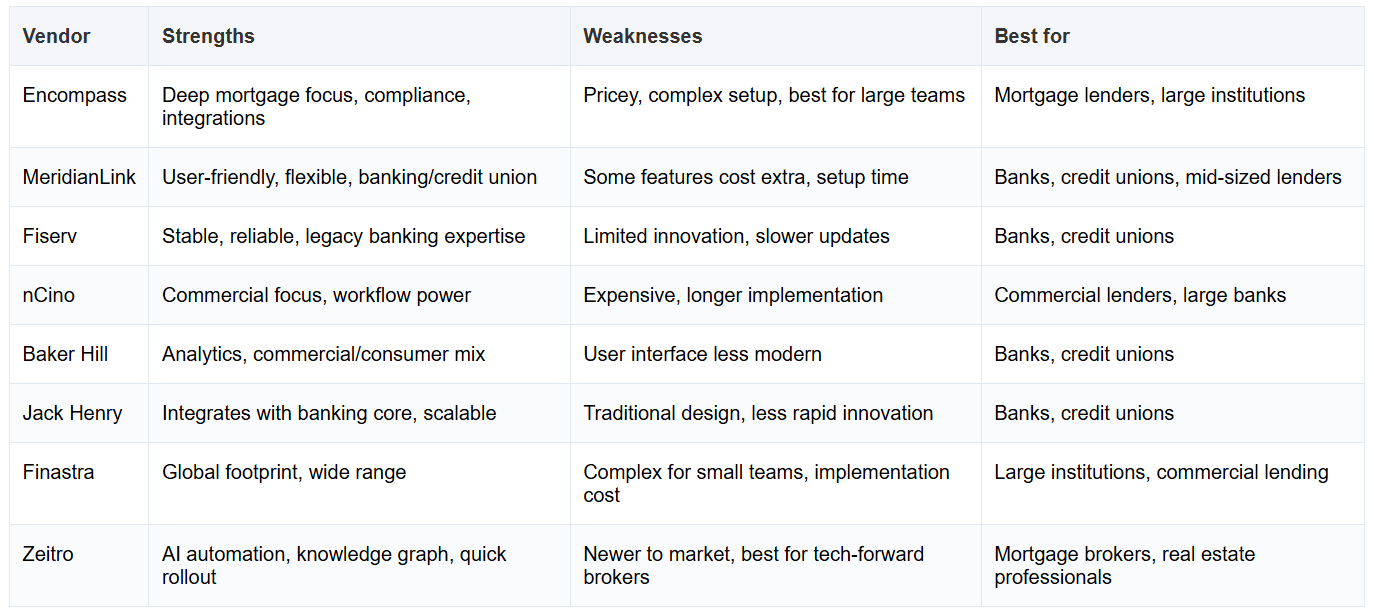

If you were to gather the most trusted names around the table, you’d likely spot Encompass (by ICE Mortgage Technology), MeridianLink, Fiserv, nCino, Baker Hill, Jack Henry, and Finastra. Each has its champions and its niches. Encompass, for instance, is practically a household name among mortgage professionals; Fiserv and MeridianLink are pillars in both banking and credit unions.

LOS Vendors at a Glance – Strengths & Weaknesses

How to Choose the Right LOS for Your Business

Start by listing must-have features, then compare how each vendor delivers on those. Key factors include: depth of automation, user experience, data security, reporting and analytics, ease of integration, and support quality. Don’t forget to ask about data migration options, API capabilities, and how easy it is to configure the system for your unique lending process. Cost isn’t just about license fees—factor in training, customizations, and long-term support.

Then there are the disruptors: Zeitro, for example, has built its reputation on an AI-driven, end-to-end platform. Unlike the giants, Zeitro was designed from day one to automate the entire loan process, using a knowledge graph database and smart modules for compliance, document management, and pricing. It’s a strikingly modern approach for mortgage brokers and real estate professionals in a field long dominated by legacy systems.

Trends Shaping the LOS Industry

It’s clear that automation, digital workflows, and AI aren’t just buzzwords—they’re becoming requirements. More lenders are expecting cloud-native platforms, real-time document processing, smart underwriting, and compliance modules that keep up with shifting regulations.

If your business is planning for future growth, favor platforms that regularly roll out updates and offer cloud deployment. Take time to compare how LOS vendors handle digital transformation—some, like Zeitro, have prioritized low-code configuration and real-time compliance tracking to help brokers and agents keep up with regulatory changes without the usual headaches.

Where once you had to choose between stability and innovation, vendors like Zeitro are now proving that it’s possible to have both: an LOS that’s fast, reliable, and surprisingly intelligent. They’re not alone, but they represent a broader industry shift towards user-friendly, all-in-one solutions that can adapt as fast as the market moves.

Loan Origination System Examples: Real-World Scenarios

The Classics: Encompass, MeridianLink, Fiserv

Take a look at any established lender, and you’ll likely see a classic LOS in action. Encompass is synonymous with mortgage origination, trusted for its compliance tools and integrations. MeridianLink and Fiserv are favorites in retail banking, handling both consumer and small business loans. Each system shines in a slightly different way, depending on whether your shop leans more toward high-volume retail lending or specialized commercial deals.

But every system has its quirks. Some lenders report that Encompass requires more onboarding time for new staff. Others find that MeridianLink’s advanced integrations take longer to set up. Before you select a platform, reach out to peers at similar-sized organizations for honest feedback—and ask vendors to demonstrate the full loan process, from application to closing.

The Innovators: Zeitro and AI-Driven Platforms

Over the past few years, I’ve watched Zeitro emerge from a Silicon Valley startup to a platform that truly makes a mark for mortgage professionals and brokers. The company’s knowledge graph engine, automated workflow, and “GuidelineGPT” compliance module aren’t just flashy marketing. I’ve seen how their five-minute borrower application, high completion rates, and automatic document validation have sped up approvals—sometimes dramatically. Zeitro isn’t here to be just another tool in the box; it’s aiming to be the operating system for mortgage professionals who want everything under one digital roof.

Streamlining Lending, Step by Step

Whether you’re using a classic system or a next-gen platform, the goal remains: cut out bottlenecks, boost accuracy, and give borrowers a seamless experience. Today’s best LOS platforms automate everything from eligibility checks to document uploads, making the lender’s job easier and the customer’s journey smoother.

When piloting a new LOS, build a checklist of real-world tasks (from application to post-closing) and evaluate each platform on speed, error rate, reporting, and borrower communication. This hands-on testing uncovers usability issues that can’t be seen in a demo. Many lenders are surprised by how much time they save—or lose—when switching platforms.

Loan Origination Software for Banks: What Matters Most

The Non-Negotiables

Banks don’t have time for half-measures. What matters most is security, compliance, seamless core integration, and the ability to handle large loan portfolios. Automation isn’t just a nice-to-have—it’s table stakes. When systems like Fiserv and Baker Hill offer deep banking integrations, they make it easier for teams to move quickly while still ticking all the regulatory boxes.

If your bank is considering a switch, ask for detailed integration documentation and confirm that all compliance features are up to date with local and federal regulations. Some banks have found unexpected costs in custom integration or delayed rollouts—ask about typical implementation timelines and what resources you’ll need on your end.

Standout Vendors

Of course, Encompass and Fiserv have earned their reputations. For banks, deep integrations, batch processing, and compliance support are essential, and these platforms deliver on those fronts. While new AI-powered LOS platforms are emerging, many—including Zeitro—are focused on serving mortgage brokers and real estate professionals rather than banking institutions. Be sure to choose a platform aligned with your organization’s core needs and regulatory requirements.

Boosting Efficiency, Supporting Growth

It’s not just about handling more loans. The right LOS can help banks enter new markets, launch new products, and grow their customer base—all while keeping operations lean. The difference between a good year and a great year often comes down to choosing a platform that grows with you.

Don’t underestimate the learning curve. For banks with teams used to legacy systems, staff buy-in is just as important as features. Request hands-on training and ongoing support, and always budget for unexpected bumps in the transition.

Commercial Loan Origination Software: Complexity and Control

What Makes Commercial Lending Unique

Commercial lending is a different beast: bigger deals, more moving parts, and a tighter focus on risk. Any LOS built for this space needs to handle complex approvals, multi-step workflows, and rigorous documentation. Risk management isn’t an afterthought—it’s the core of the business.

Key Players and Smart Solutions

nCino and Finastra are household names here. But in my own experience, platforms designed for mortgage professionals and brokers, such as Zeitro, are taking automation and document processing to new levels, especially for residential and investment property lending. Zeitro’s ability to configure workflows for multiple loan products—backed by real-time compliance and automated document checks—makes it well-suited for brokers and real estate agents who need to move fast and handle diverse loan scenarios. The flexibility to support DSCR, hard money, and private loans all on one platform is rare and valuable.

When shopping for a commercial LOS, ask vendors for client references who’ve implemented custom workflows. Pay close attention to how the system manages approval hierarchies, risk ratings, and document versioning. Don’t be afraid to request a sandbox environment to test these features in practice—commercial lending rarely fits a template.

Consumer Loan Origination Systems: High Volume, Seamless Experience

What Sets Consumer LOS Apart

Speed and simplicity are the order of the day. Borrowers expect quick approvals, easy digital self-service, and mobile-first experiences. That means high-volume processing, instant eligibility checks, and transparent communications at every step.

Vendors Leading the Pack

Jack Henry and MeridianLink have long been known for scalable, user-friendly platforms. But Zeitro’s approach—supporting a wide range of loan types (including Non-QM, FHA, USDA, and more), automating document intake, and integrating customer portals—raises the bar for what consumer lenders, especially mortgage brokers and real estate professionals, can offer.

For high-volume shops, make sure your chosen LOS can withstand peak activity and doesn’t slow down during busy cycles. Check that the platform supports strong data privacy and gives you visibility into borrower progress. Some lenders recommend running side-by-side trials to measure how quickly each system can move applicants from inquiry to funded loan.

Loan Origination Systems for Credit Unions: Flexibility & Member Experience

Credit Union Priorities

Credit unions live and die by member service. Their LOS must be customizable, easy to use, and able to integrate with the broader cooperative banking ecosystem. Batch processing and flexible workflows make all the difference.

Comparing Solutions

Traditional options from Fiserv, Jack Henry, and MeridianLink remain reliable choices. For mortgage brokers and real estate professionals who need high configurability and automation, platforms like Zeitro have emerged as strong options—but again, they are not tailored for credit union-specific compliance or operational needs.

Ask for a demonstration of how easy it is to update rates, disclosures, and member notifications in each system. For many credit unions, having self-service options for both staff and members is a must. Dig into what’s included “out of the box” and what requires vendor customization.

Encompass: The Mortgage LOS Standard

Encompass and Its Place in the Industry

Ask ten mortgage professionals about LOS vendors, and at least half will start with Encompass. It’s the gold standard for compliance, integrations, and mortgage-specific workflows. Few platforms can match its depth in pure mortgage origination.

But depth comes with complexity. New users should be prepared for a learning curve, and smaller lenders may find Encompass more robust than necessary. Check if you need all modules, or if a lighter configuration is more practical. Some mortgage brokers find that newer systems, like Zeitro, offer a more modern user experience with lower upfront setup.

The AI Revolution: What’s Next?

As we see the industry shift, newer platforms—Zeitro among them—are pushing boundaries with artificial intelligence, real-time analytics, and knowledge-driven automation. It’s not about replacing Encompass, but about expanding the definition of what a mortgage LOS can be.

LOS Workflows and Comparisons: From Application to Approval

The Core LOS Workflow

Every journey begins with an application, winds through document collection, and (hopefully) finishes at the closing table. Along the way: eligibility checks, underwriting, compliance validation, and constant back-and-forth with borrowers. The most advanced systems now automate each step, saving hours—and sometimes days—of manual labor.

How Today’s AI-Driven LOS Platforms Compare

When you line up the old guard with newcomers like Zeitro, differences start to appear. Traditional systems still shine in reliability and depth. AI-powered solutions are taking the lead in automation, efficiency, and user experience. Zeitro’s statistics—like a 250% increase in pipeline capacity, seven hours saved per file, and dramatically faster borrower onboarding—aren’t just numbers; they reflect a new reality for teams that embrace change.

No matter what system you choose, always test your workflow before going live. Build a checklist of each step and make sure the platform can handle exceptions, manual overrides, and last-minute changes. Efficiency isn’t just about automation; it’s about having the flexibility to support your unique lending process.

Frequently Asked Questions about LOS Vendors

- What is a loan origination system vendor?

A company or platform providing digital tools to manage the end-to-end process of loan origination for lenders, banks, credit unions, and brokers. - How do I choose the right LOS for my business?

Think about the types of loans you process, your institution’s size, required integrations, automation needs, and your team’s learning curve. Pilot programs and user feedback are worth their weight in gold. - How does automation improve loan origination?

Automation eliminates repetitive work, reduces errors, speeds up the approval process, and lets teams focus on higher-value tasks like client relationships. - Where does AI fit into all this?

Artificial intelligence powers smarter decisioning, real-time compliance, document verification, and even market analytics. It’s not about replacing people; it’s about helping them do more, better. For example, some brokers use Zeitro’s AI modules to automate guideline checks and document validation, freeing staff to focus on customer experience. - LOS vs. LMS—what’s the difference?

LOS (Loan Origination System) covers everything from application to funding. LMS (Loan Management System) handles servicing after the loan is booked. - Are there any hidden costs or common pitfalls with LOS platforms?

Be sure to ask about migration fees, support charges, integration costs, and contract terms. Try to negotiate for a pilot phase to test the real-world fit before making a full commitment.