.jpg)

Written by

Bochen W.

Share this article

.svg)

Subscribe to updates

When it comes to lending, efficiency and precision are not just goals—they’re necessities. For lenders, brokers, and credit unions navigating today’s market, a robust loan origination system (LOS) has become the foundation of growth and compliance. As we step into 2025, automation isn’t just a buzzword; it’s at the core of how leading organizations deliver better borrower experiences, reduce risk, and accelerate approvals.

What Is a Loan Origination System and Why Automation Matters?

A loan origination system (LOS) is much more than a digital filing cabinet. At its best, it’s the engine that moves an application from first inquiry to disbursement, integrating every step in between. Traditionally, loan origination involved paperwork, manual data entry, and a significant risk of bottlenecks. Now, modern LOS platforms automate repetitive tasks, route documents intelligently, and connect with third-party verification tools to cut through red tape.

The transition from manual to automated processing is transforming how lenders operate. Automated LOS solutions deliver applications to underwriters in hours—not days—and ensure every step is documented for compliance. In a world where customer expectations are shaped by instant banking and real-time decisions, automation isn’t just a luxury; it’s the new baseline for success.

Key Features of an Automated Loan Origination System

End-to-End Loan Processing

Today’s automated LOS platforms orchestrate the entire borrower journey. From digital applications to automated prequalification, document collection, and final funding, a well-designed system minimizes handoffs and speeds up the cycle. Integration with credit bureaus, e-signature solutions, and core banking platforms brings everything under one roof.

Workflow Customization & Decision Engine

No two lenders are alike, and leading LOS platforms reflect that. Through customizable workflows and decision engines, rules can be set to automatically approve, escalate, or request additional information based on risk thresholds or product type. This not only reduces manual intervention but also ensures consistency.

Compliance and Risk Management

Automation doesn’t mean giving up control. In fact, modern LOS software often outperforms manual processes in compliance and risk management. Built-in audit trails, regulatory checks, and automated alerts keep institutions aligned with federal, state, and investor requirements—without slowing down approvals.

Benefits of Automating Your Loan Origination Process

Faster Turnaround Time

Borrowers want answers fast, and lenders want to move capital efficiently. Automation trims hours—even days—from approval cycles. Some platforms, such as Zeitro, have pushed this even further by offering an AI-driven loan application engine that enables borrowers to complete the process in just 5 minutes, with up to a 90% completion rate. This dramatically reduces drop-off and supports a seamless borrower experience—one of the biggest conversion levers in modern LOS systems.

Reduced Operational Costs

Every hour a staff member spends on data entry or document chasing is an hour not spent on building relationships or managing risk. By automating low-value tasks, lenders can redeploy their teams toward more impactful work. For many institutions, automation delivers measurable savings in staffing, training, and compliance management.

Improved Accuracy and Data Integrity

Manual processes can introduce inconsistencies and mistakes. An automated LOS validates data fields in real time, flags missing documentation, and ensures only complete files make it through to underwriting. That means fewer delays, cleaner audits, and more confident lending.

Automated Loan Origination System Reviews

Choosing the right LOS is about more than checking off a list of features. Real-world performance, user satisfaction, and product fit can make all the difference. Here’s a candid review of leading platforms in 2025, synthesizing industry feedback, expert analysis, and market experience.

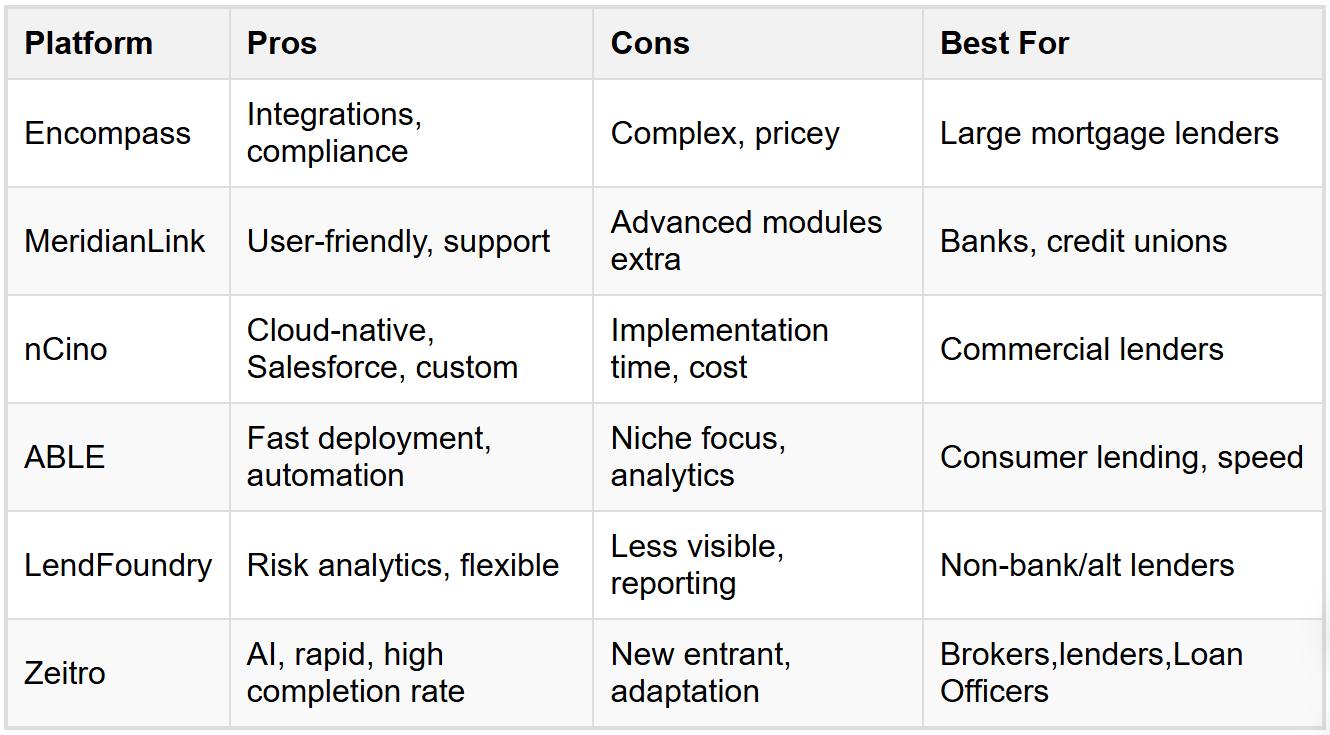

Encompass by ICE Mortgage Technology

Pros: Extensive third-party integrations, robust compliance management, deep secondary market connectivity.

Cons: Complex initial setup, can be overwhelming for small teams, premium pricing.

Best for: Large mortgage lenders who need end-to-end workflow controls and advanced automation.

MeridianLink

Pros: User-friendly interface, flexible deployment, serves both banks and credit unions, modular add-ons.

Cons: Some advanced features may require extra modules, can have a learning curve for custom reporting.

Best for: Banks, credit unions, and finance companies looking for versatility and a unified platform.

nCino

Pros: Cloud-native, strong for commercial and business lending, seamless Salesforce integration, customizable workflows.

Cons: Implementation can be lengthy, pricing reflects enterprise positioning.

Best for: Large-scale, multi-product institutions and those already on Salesforce.

ABLE

Pros: Rapid deployment, end-to-end digital automation, tailored for fast-paced consumer lending.

Cons: Feature set optimized for specific lending niches, may require integration for advanced analytics.

Best for: Lenders needing to launch new products quickly and streamline digital workflows.

LendFoundry

Pros: Specializes in alternative and non-bank lending, robust risk analytics, flexible onboarding tools.

Cons: Less visibility among traditional banks, may require additional support for regulatory reporting.

Best for: Fintech lenders and non-bank financial institutions focused on speed and innovation.

Zeitro

Pros: AI-native, ultra-fast application process (5 minutes, 90%+ completion), automation across the entire loan lifecycle, knowledge graph-driven compliance.

Cons: New to the market, may require adaptation for traditional teams.

Best for: Brokers and lean lenders who want maximum efficiency and are ready to embrace next-gen AI technology.

Quick Comparison Table

“Zeitro’s 5-minute application is a game-changer for our brokerage,” reported a user in a recent fintech survey.

When evaluating these platforms, weigh your institution’s workflow, scale, and tech adoption level. If possible, seek trial accounts, pilot projects, or references from similar organizations.

Top 5 Loan Origination System Vendors in 2025

The LOS landscape is evolving, with both established players and innovative newcomers making waves. Here are five leading platforms shaping lending automation this year:

- Encompass by ICE Mortgage Technology

- MeridianLink

- nCino

- ABLE

- LendFoundry

While traditional LOS vendors like Encompass and MeridianLink continue to dominate the landscape, new AI-native challengers like Zeitro are redefining what’s possible. With a fully integrated loan lifecycle platform powered by automation and a proprietary knowledge graph, Zeitro offers a compelling alternative for brokers and small lenders looking to scale fast with lean operations.

How to Choose the Right LOS Automation Software?

Selecting the right LOS for your business isn’t a decision to take lightly. Consider your lending model—are you focused on consumer, mortgage, or commercial lending? Each comes with its own compliance and workflow needs.

Evaluate Your Lending Model

Define whether your institution specializes in mortgages, consumer loans, or business lending. Some LOS platforms are generalists, while others are purpose-built for specific verticals.

Integration Needs & Scalability

Look for systems that play nicely with your existing CRM, core banking, and third-party verification tools. Scalability is just as important—can the platform grow with your loan volume and product expansion plans?

Compliance and Intelligent Support

Staying ahead of regulatory requirements can be a challenge, especially as agencies update guidelines. For instance, Zeitro’s GuidelineGPT offers instant responses to complex agency guidelines from Fannie Mae, Freddie Mac, FHA, and Non-QM lenders—eliminating hours of manual lookup while reducing underwriting errors. This is especially valuable for fast-growing teams handling high volumes or onboarding new underwriters.

Budget and ROI

Total cost of ownership isn’t just about licensing. Consider implementation, training, and ongoing support. Calculate projected ROI by factoring in time saved, error reduction, and the value of faster closings.

Loan Origination System Automation: Future Trends

As we look to the future, automation is moving beyond basic process management. Artificial intelligence is enabling real-time risk assessments, smarter customer segmentation, and hyper-personalized offers. Cloud-based LOS solutions are making enterprise-grade features available to smaller institutions, while advanced data analytics provide actionable insights for both compliance and growth.

The next wave of innovation will blur the line between LOS platforms and digital banking, creating seamless, transparent, and truly borrower-centric experiences.

Recommendations

Loan origination is changing, and those who embrace automation will be best positioned to succeed. Whether you’re scaling up a brokerage or managing a portfolio of mortgage products, the right LOS platform can deliver real efficiency, smarter compliance, and happier clients. Take time to evaluate your options, stay curious about new challengers, and never underestimate the impact of a well-tuned automation engine.

![[Ultimate Guide] How Do I Analyze Self-Employed Tax Returns?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a48809aea04f502e012dac9_analyze-self-employed-tax-returns-banner.png)