Written by

Eric

Share this article

.svg)

Subscribe to updates

I am thrilled to announce a significant milestone in our journey. As of March 2026, our flagship product, formerly known as Scenario AI and GuidelineGPT, has officially been rebranded as Zeitro Strata AI. This change isn't just about a new name. It reflects a massive leap in our technology.

By moving to an advanced agentic framework, we've built a tool that does more than just answer questions—it serves as the foundational decision layer for the modern mortgage enterprise. Whether you are a broker or a lender, I'd like to introduce you to the next generation of mortgage intelligence.

Introduction to Zeitro

At our core, Zeitro is an AI-native technology company that has been pushing the boundaries of the mortgage industry since 2018. We operate as an independent entity, meaning we aren't tied to any specific lender. This neutrality is something I am particularly proud of because it allows us to serve the entire mortgage ecosystem with total objectivity.

Our team is a unique blend of veteran mortgage experts and elite AI engineers from tech giants like Google and Apple. We've combined deep domain knowledge with enterprise-grade security, evidenced by our SOC 2 Type II certification. We understand that in this industry, accuracy and data protection aren't optional—they are the bedrock of trust. We built Zeitro to remove the manual grind from guideline research, giving professionals the instant, transparent answers they need to close loans faster.

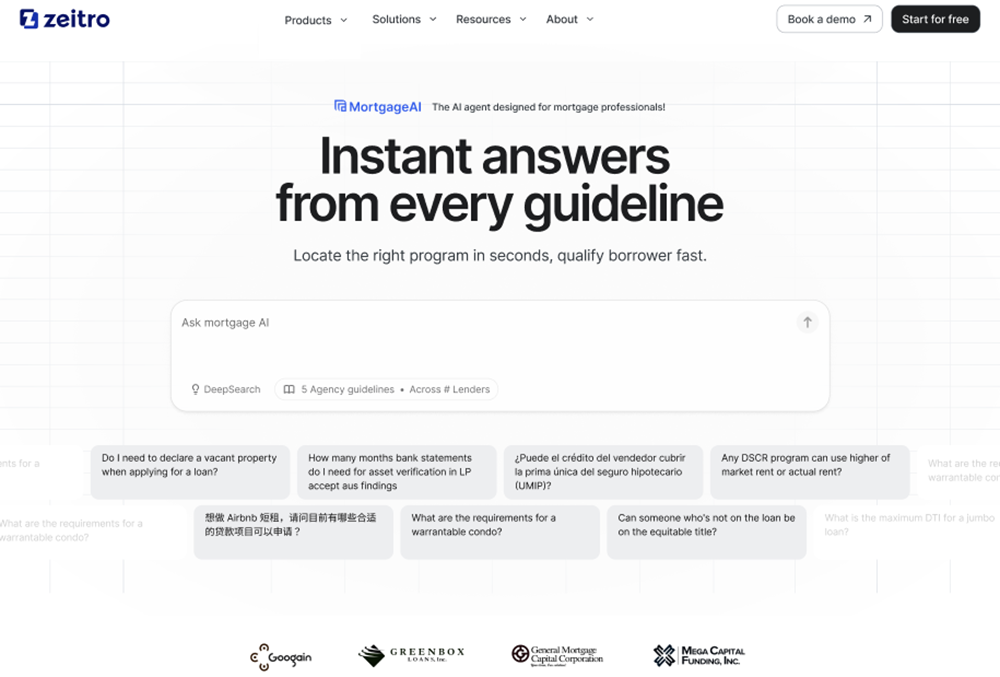

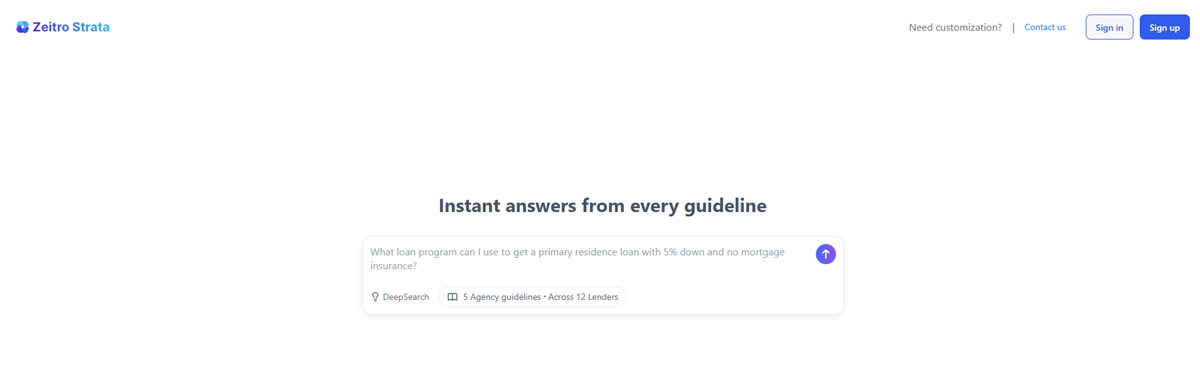

Learn: What Zeitro Strata AI Is?

So, what exactly is Zeitro Strata AI? Think of it as your most experienced underwriting assistant, available 24/7. It is an AI-powered mortgage guideline agent designed specifically for the U.S. market. It's the perfect fit for Loan Officers, Brokers, and Wholesalers who are tired of digging through 500-page PDF manuals.

In today's 2026 market, Non-QM loans, like DSCR and bank statement programs, have grown to represent nearly 15% of all originations. This complexity makes Zeitro Strata AI more essential than ever. It handles everything from simple "what is" questions to complex eligibility scenarios across both QM and Non-QM products. I've seen it help teams deliver pre-qualifications 2.5x faster while cutting manual guideline work entirely. It's not just a search bar. It's a decision-support engine that helps you say "yes" to more borrowers with total confidence.

Explore the Features of Zeitro Strata AI

When we designed the features for Zeitro Strata AI, our goal was to eliminate the "black box" feel of traditional AI. Here is what makes it a game-changer for your daily workflow:

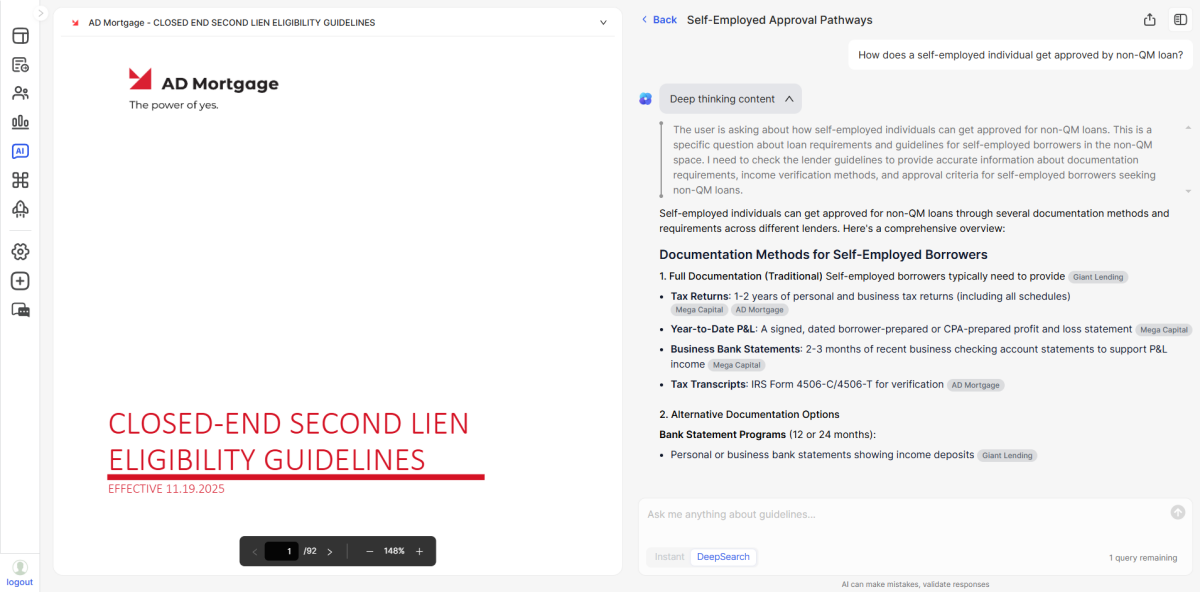

- DeepSearch Technology: It cross-checks guidelines from over 100 investors, like AAA Lending and Freedom Mortgage, in seconds, not minutes.

- Massive Guideline Library: We cover a variety of loan types, including specialized products like Asset Utilization, ITIN, and Foreign National loans.

- Full Source Transparency: Every answer comes with a Citation. You can click through to see exactly which page of the investor's manual the information came from.

- Explain Function: If a guideline is particularly dense, you can use the "Explain" feature to get a secondary breakdown of the requirements.

- Multi-language Support: I love that our users can input queries in English or Chinese and receive professional, accurate responses.

- Seamless Sharing: You can instantly share a specific answer via an email link to keep your borrowers and partners in the loop.

Tutorial: How to Use Zeitro Strata AI?

Getting started is incredibly simple. I've seen new users master the platform in under two minutes. Here is the typical four-step process:

- Select Your Scope: Start by using customizable tags. You can narrow your search to specific lenders or loan types like DSCR or Jumbo to ensure the results are relevant.

- Ask Your Question: Type in your scenario. You don't need to be a prompt expert. You can ask specific questions like "What is the max LTV for a 12-month bank statement loan with a 680 FICO?" or more vague situational queries.

- Review and Explain: Within seconds, Zeitro Strata AI will provide a precise answer. If you need more detail, click the "Explain" button for a deeper dive.

- Verify and Export: Check the citations to confirm the source. From there, you can share the findings or move the data into our Digital 1003 system to finalize the application.

FAQs About Zeitro Strata AI

Q1. How often are the mortgage guidelines updated?

We update our database continuously. Our system tracks over 100 investors to ensure you are looking at the most current requirements for 2026.

Q2. Can I use Zeitro Strata AI for free?

Yes! We offer an Explorer Plan which is completely free. It includes 3 Mortgage AI queries per day and access to our personal website and pricing engine tools.

Q3. Does the "Explain" feature cost extra queries?

Yes, the Explain feature functions as a new deep-search query based on your selected range to ensure the highest accuracy, so it does consume a query from your daily limit.

Q4. What makes the name "Strata" different from the old "Scenario AI"?

"Strata" signifies the "foundational layer." While the old tool was great for scenarios, Zeitro Strata AI is built on an agentic framework meant to be the core decision layer for your entire mortgage business.

Q5. Is my borrower's data safe when using the AI?

Absolutely. Security is our priority. We are SOC 2 Type II certified, which means we follow the highest industry standards for data protection and operational privacy.

Conclusion

The transition from Scenario AI to Zeitro Strata AI marks a new era for mortgage professionals. In a market where speed and accuracy define success, you can't afford to spend seven hours per loan file on manual research. I truly believe that by using Zeitro Strata AI, you aren't just adopting a new tool. You're gaining a competitive edge that allows you to close 30% more loans.

Whether you're dealing with a complex Non-QM investor or a standard FHA file, our agentic AI is here to provide the clarity you need in seconds. I invite you to try the Explorer Plan today for free. Experience firsthand how the foundational decision layer of Zeitro can transform your workflow and help you grow your business in this evolving 2026 housing market.

People Also Read

- Best Mortgage CRM for Brokers, Lenders, MLOs

- Best Loan Origination Software for LOs/Brokers

- Mortgage Guidelines: What Are They? How to Verify?

- What is Mortgage Eligibility Checker? Best Tool to Verify Guidelines

- Best Mortgage Underwriter Software: AI & Guideline Verification

- Why Have Mortgage Rates Risen When Oil Prices Increase?