Written by

Eric

Share this article

.svg)

Subscribe to updates

When you apply for a mortgage, it is completely natural to wonder if your loan officer can persuade the underwriter to approve your loan, especially if your file has a few wrinkles. The short answer is yes, but not through backroom deals or pressure.

Based on my years in the industry, I can tell you that a loan officer influences an underwriter primarily through professional advocacy, clear documentation, and presenting a strong, compliant file.

Key Takeaways

- Advocacy, Not Pressure: Loan officers influence underwriters by presenting clear facts, not by forcing decisions.

- Legal Boundaries: Strict federal laws are designed to protect the underwriter's independent judgment and prevent improper influence.

- The Power of Paperwork: A well-prepared loan file with strong compensating factors is a loan officer's best tool.

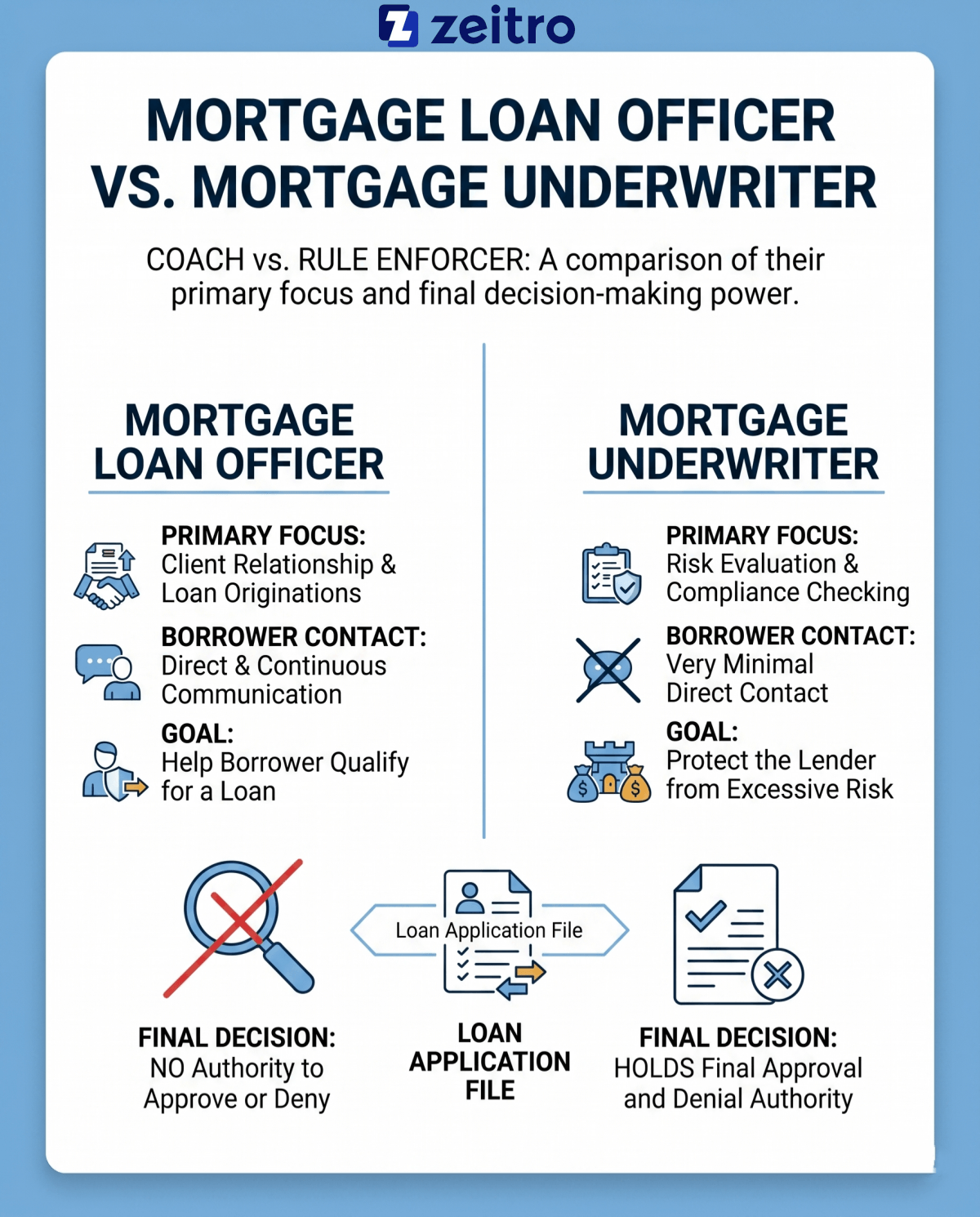

What is a Mortgage Loan Officer?

Think of me, your mortgage loan officer (MLO), as your personal guide and advocate throughout the home-buying journey. I am the client-facing professional who helps you navigate the complex world of home financing. My job is to understand your unique financial goals, find the right loan program for you, and help you package your application so it looks as strong as possible.

In my daily routine, I handle several key tasks:

- Prequalifying borrowers and assessing their financial readiness.

- Educating clients on different loan products, like conventional, FHA, or VA loans.

- Gathering initial documents, including tax returns, W-2s, and bank statements.

- Structuring and submitting the final loan application package to our processing and underwriting teams.

I want your loan to close just as much as you do, which is why I work hard to present your financial story in the best light.

What is a Mortgage Underwriter?

While I am your guide, the mortgage underwriter is the final gatekeeper. Operating behind the scenes, the underwriter's primary responsibility is risk assessment. They typically do not work directly with the borrower and instead communicate through the loan officer or processor. Instead, they scrutinize your financial profile against strict institutional and investor guidelines, such as those set by Fannie Mae, Freddie Mac, or the FHA.

The underwriter's daily responsibilities include:

- Verifying your employment, income, credit history, and asset reserves.

- Evaluating the home appraisal to ensure the property is worth the purchase price.

- Issuing "conditions" that must be met before final approval can be granted.

- Making an approval decision based on established guidelines, subject to final verification and investor requirements.

They ensure that we are making a safe, compliant loan that you can actually afford to pay back, protecting both you and the lending institution.

Mortgage Loan Officer vs. Mortgage Underwriter

To make the loan process easier to understand, it helps to look at how our roles differ. While we both want to see loans get approved safely, our daily focus and responsibilities are quite distinct.

I am here to coach you through the hurdles, while the underwriter is there to make sure every rule has been followed.

Also Read: Mortgage Underwriter vs Loan Officer: Which Career Is Best?

Can a Loan Officer Influence an Underwriter?

In the mortgage industry, "influence" is a highly regulated word. Under federal laws like the Dodd-Frank Wall Street Reform and Consumer Protection Act, underwriters must remain completely independent. I cannot pressure, threaten, or bribe an underwriter to approve a loan. If I tried, I would be violating compliance policies and risking my license.

However, I can absolutely influence the outcome of your loan through professional advocacy and solid evidence. If your file is complex, perhaps you are self-employed or had a brief gap in employment, I use several ethical strategies to build a winning case:

- Highlighting Compensating Factors: If your credit score is on the lower side, I might point out to the underwriter that you have a massive down payment or significant cash reserves.

- Drafting a Strong Letter of Explanation (LOX): I will help you draft a clear, factual letter explaining any financial anomalies, such as a one-time medical bill that temporarily hurt your credit.

- Guideline Interpretation: If an underwriter takes an overly conservative view of a specific rule, I can research the agency guidelines (like Fannie Mae's selling guide) and present a logical counter-argument.

Ultimately, my goal is to deliver a file so clean and well-documented that the underwriter has every reason to say "yes."

How Do Loan Officers and Underwriters Collaborate for Loan Approval?

Although we have different responsibilities, we are not enemies. We work as a team to get you into your home. A smooth home loan approval depends entirely on how well we communicate and collaborate behind the scenes.

Here is how we work together to secure your approval:

- Pre-Underwriting Clean-Up: I review your bank statements and tax transcripts beforehand to catch and fix issues before the underwriter even sees the file.

- Addressing Conditions Quickly: When the underwriter issues a conditional approval, I act fast to gather the exact paperwork they need, saving everyone time.

- Solving Complex Problems: If a unique situation arises, we discuss it directly to find a solution that fits the lender's risk tolerance and guidelines.

By keeping our communication professional and respect-driven, we can dramatically speed up your time-to-close.

Conclusion

Navigating the mortgage process can feel overwhelming, but you do not have to do it alone. While I cannot force an underwriter to sign off on your loan, my ability to present your financial story accurately is the single most powerful tool we have. Underwriters rely on facts and guidelines, and my job is to make sure your facts are undeniable.

When you work with a loan officer who understands how to build a strong case, you vastly improve your chances of hearing those three favorite words in real estate: "clear to close." If you are ready to start, let's get your paperwork organized today.

People Also Read

- Detailed Guide: How to Become a Loan Officer with No Experience?

- Mortgage Loan Officer Salary: How Much Do Loan Officers Make?

- Mortgage Underwriter Salary: How Much Does a Home Loan Underwriter Make?

- [NO Experience] How to Become a Mortgage Underwriter?

- AI Mortgage Underwriting Explained: Will You Be Replaced?