Written by

Eric

Share this article

.svg)

Subscribe to updates

As a loan officer, I've had to make this tough phone call more times than I can count: telling a buyer their dream condo just got rejected for a conventional loan. The buyer's credit is flawless, but the building itself didn't pass the test. Welcome to the world of the non-warrantable condo.

It's a massive headache for buyers and lenders alike, usually because of strict Fannie Mae and Freddie Mac rules. But getting that "no" isn't a dead end. Let's break down exactly what this label means, why it happens, and how we can actually get your mortgage across the finish line.

Key Takeaways

- A non-warrantable condo simply doesn't meet the strict mortgage standards required by Fannie Mae or Freddie Mac.

- The label usually stems from HOA issues, like ongoing lawsuits, low reserve funds, or too much commercial space.

- You can't use a standard conventional loan. Instead, you'll need alternative routes like portfolio loans or non-QM mortgages.

- Expect to put down a much larger down payment and pay higher interest rates to offset the lender's risk.

Meaning: What is a Non-Warrantable Condo?

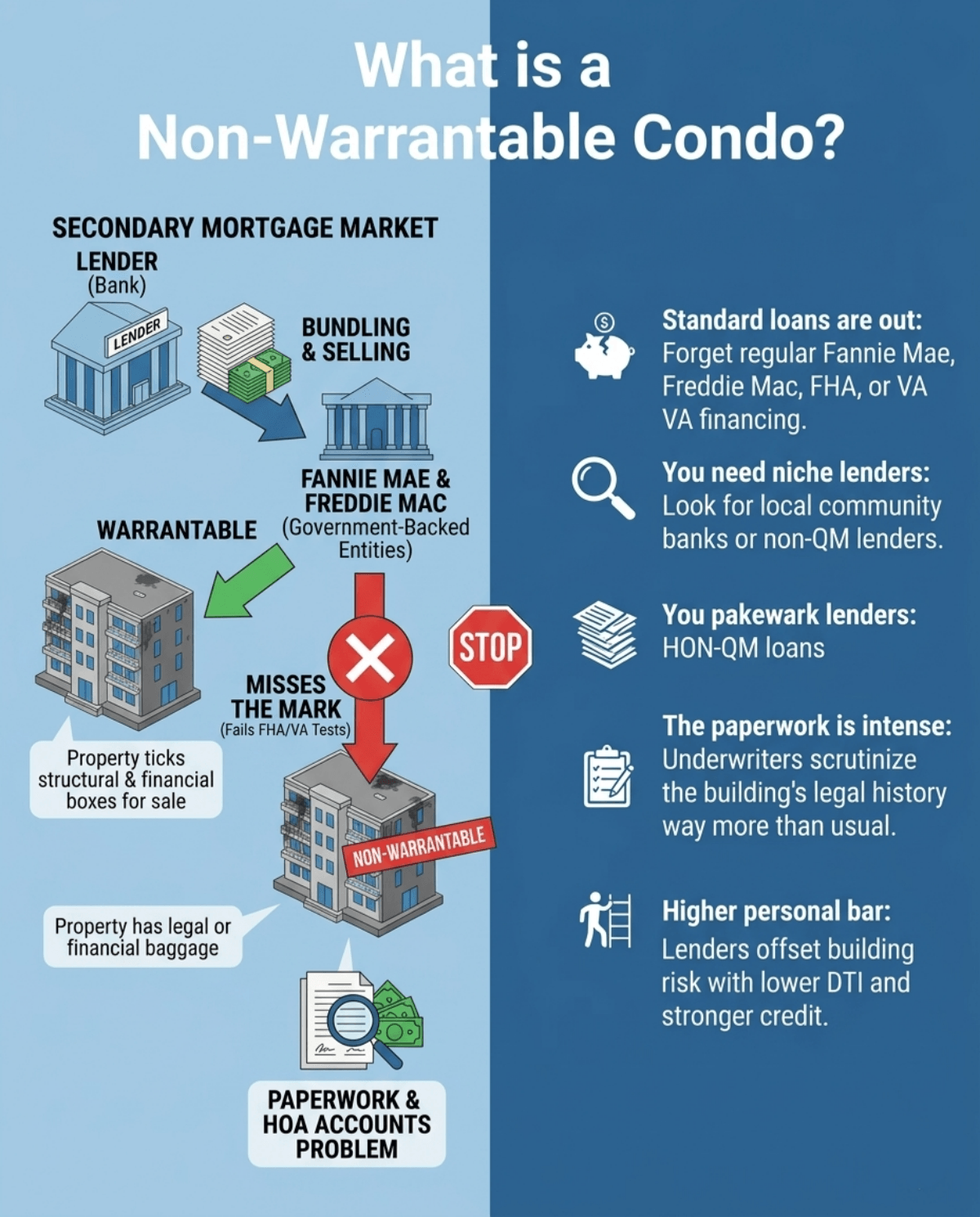

Think about how the secondary mortgage market works. When I write a conventional mortgage, my bank rarely keeps it. We bundle it up and sell it to government-backed giants like Fannie Mae or Freddie Mac. To make that sale, the condo project has to be "warrantable," meaning it ticks all their boxes for structural and financial safety.

So, what happens when a building misses the mark? Or fails similar FHA and VA tests? It gets tagged as a non-warrantable condo. This label simply means the property carries legal or financial baggage that big institutions won't touch. Honestly, it rarely means the roof is caving in. Usually, it points straight to a problem with the Homeowners Association (HOA)'s paperwork or bank accounts.

Here is what you actually need to know about these properties:

- Standard loans are out: Forget regular Fannie Mae, Freddie Mac, FHA, or VA financing.

- You need niche lenders: You'll be looking for local community banks or non-QM lenders.

- The paperwork is intense: Underwriters will scrutinize the building's legal history way more than usual.

- Higher personal bar: Lenders offset the building's risk by expecting lower debt-to-income (DTI) ratios and stronger credit from you.

What are the Reasons a Condo is Considered Non-Warrantable?

I've pored over countless Condo Questionnaires, and I can tell you Fannie Mae's red lines are incredibly strict. If a development trips up on even one of these rules, the whole building gets disqualified.

Here are the most common dealbreakers I see:

- Too much single-entity ownership: One investor or corporation owns more than 20% of the units.

- Pending litigation: The HOA is currently battling a major lawsuit involving structural safety.

- Oversized commercial space: Ground-floor retail takes up more than 35% of the total square footage.

- Condotel vibes: The place runs like a hotel with nightly rentals or timeshare setups.

- Low HOA reserves: The association's reserves are less than 10% of its annual operating budget.

- Too many renters: Investors own the majority of units, leaving very few actual owner-occupants.

Pros and Cons of a Non-Warrantable Condo

Taking on a non-warrantable property isn't automatically a bad move. Your perspective changes entirely depending on whether you're trying to buy a primary residence or you're an investor hunting for yield. Here's the reality of what you're walking into.

Benefits:

- Way less competition: Most buyers walk away when their traditional loan falls through. That leaves the door wide open for you.

- Solid price discounts: Sellers get desperate. They know their buyer pool is tiny, which gives you massive negotiation power.

- An investor's playground: If you're paying cash, these properties are often steals. A high renter ratio might scare off Fannie Mae, but it tells an investor the rental market is already proven.

Drawbacks:

- Heavy down payments: Lenders will ask for 20% to 30% upfront just to cover their perceived risk.

- Pricier money: Alternative financing simply costs more in interest and fees.

- A nightmare to resell: Eventually, you'll want to sell. And you'll be stuck dealing with the exact same financing hurdles the current owner is facing.

- Hidden HOA bombs: If the building was blacklisted for bad budgeting, you might get hit with a crippling special assessment down the line.

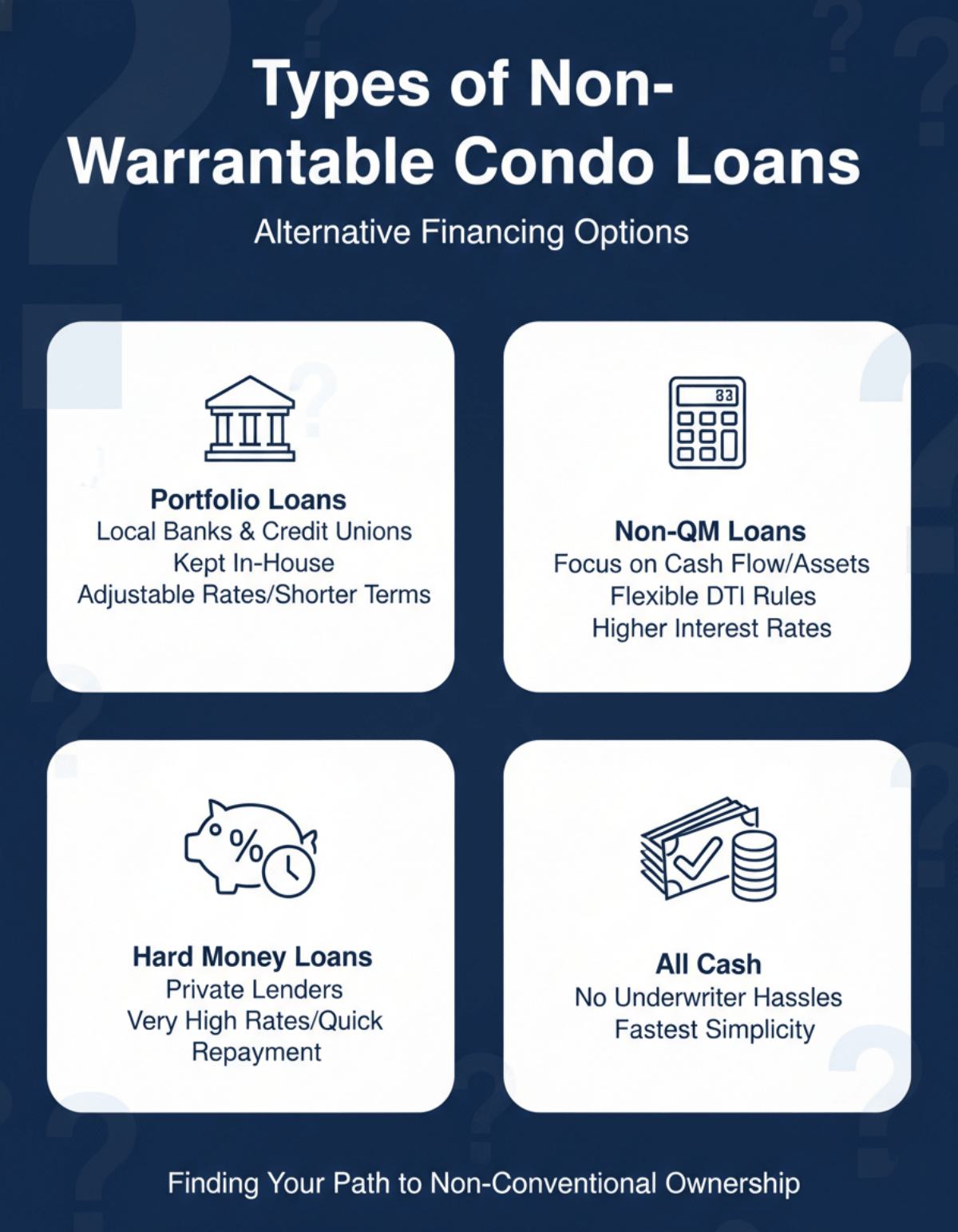

Types of Non-Warrantable Condo Loans

Hearing "no" from a conventional bank doesn't mean you're entirely locked out. Finding an experienced Mortgage Broker who knows their way around alternative financing is your best bet here.

If you want this condo, here are the loan types we typically look at:

- Portfolio Loans: Local credit unions or banks keep these mortgages on their own books instead of selling them off. The catch? You'll likely see adjustable rates or shorter terms.

- Non-QM Loans: These non-qualified mortgages care less about standard DTI rules and more about your raw cash flow or assets. Expect a bump in the interest rate.

- Hard Money Loans: A favorite for house flippers needing fast cash. The rates are steep, and you have to pay them back quickly.

- All Cash: The ultimate cheat code. Skipping the underwriter entirely makes the problem disappear.

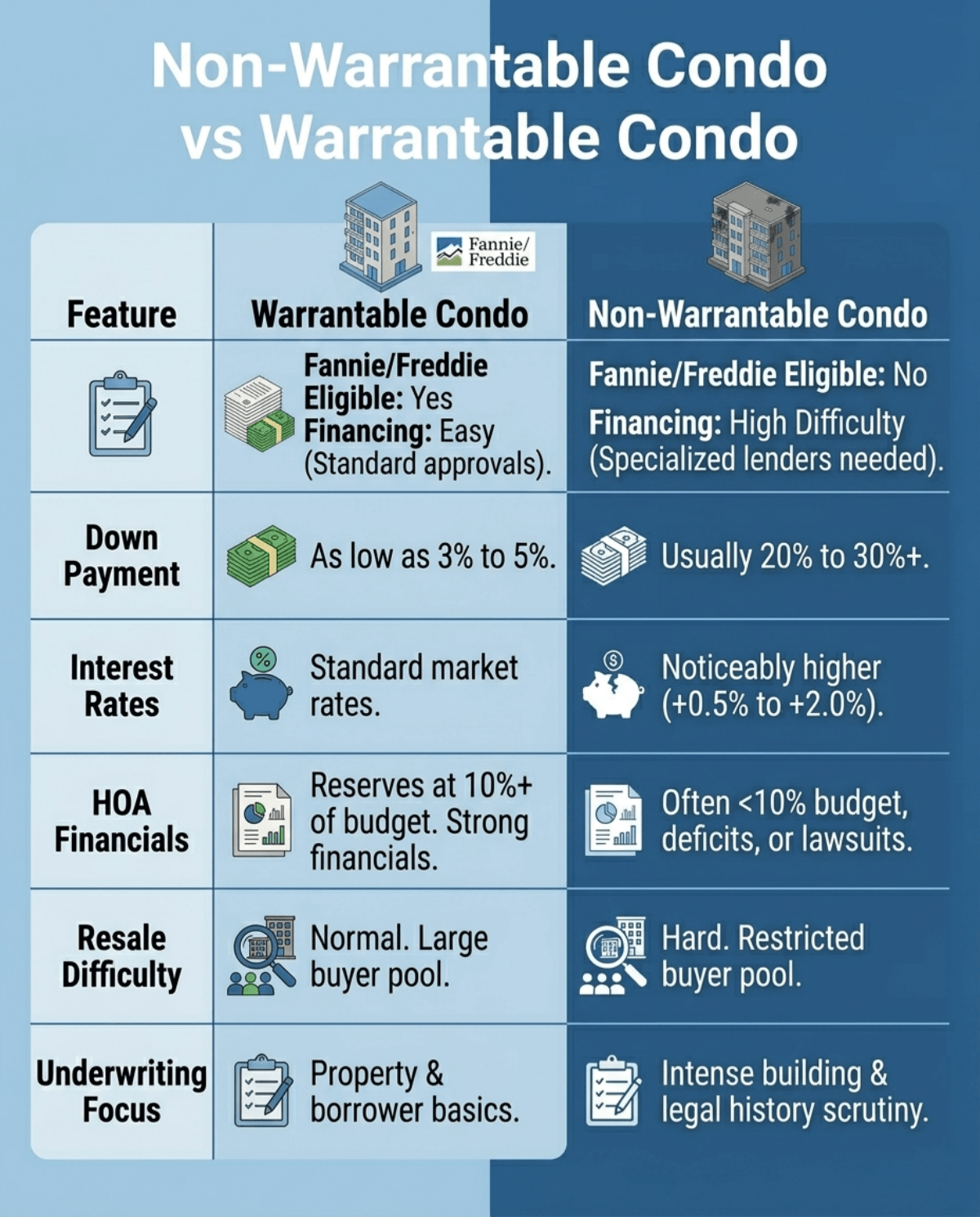

Non-Warrantable Condo vs Warrantable Condo

The easiest way to think about the difference between these two property types is looking at cash and headaches. Warrantable condos give you a smooth, boring, and predictable path to getting the keys. Non-warrantable properties, on the other hand, demand much more upfront capital and carry heavier borrowing costs. However, they can sometimes turn into incredible investments if you know how to navigate the extra friction.

Here is a quick snapshot of how they actually compare in the real world:

Paying attention to that massive gap in down payments and interest rates will quickly tell you if a slightly cheaper purchase price is actually worth the hassle.

FAQs About a Non-Warrantable Condo

Q1. Can a non-warrantable condo become warrantable?

Yes. This status isn't necessarily a permanent stain. If the HOA finally settles its pending lawsuits, boosts its reserve fund to meet Fannie Mae guidelines, or gets the investor ownership ratio back under control, the building can definitely earn back its warrantable title.

Q2. What are non-warrantable condo guidelines?

There isn't one universal rulebook for this. The term simply means the building failed the standard criteria set by Fannie Mae or Freddie Mac. From there, lenders offering portfolio or Non-QM loans will use their own private non-warrantable condo underwriting guidelines to figure out if they want the risk.

Also Read:

- What is Mortgage Eligibility Checker? Best Tool to Verify Guidelines

- Mortgage Guidelines: What Are They? How to Verify?

- How to Determine Mortgage Eligibility? Verify Guidelines in Seconds

- [Read First] What is a Non-Warrantable Condo Loan?

Q3. Do I need a larger down payment for a non-warrantable condo?

Yes. Since government-backed agencies refuse to guarantee these mortgages, your lender takes on all the risk. To make them comfortable lending you the money, you'll almost always need to bring at least 20% to 30% of the purchase price to the closing table.

Q4. Is it risky to buy a non-warrantable condo?

Yes, the risks are real. You are taking a gamble on the building's financial health. You could inherit a poorly managed HOA, get slapped with a massive special assessment to fix a leaking roof, or find yourself totally stuck when you try to sell later.

Also Read: Best Non-Warrantable Condo Lenders Near Me in 2026

Q5. Is it hard to sell a non-warrantable condo?

Yes. Whoever buys the place from you is going to face the exact same stressful financing hurdles you just went through. This shrinks your future buyer pool drastically, leaving you relying mostly on all-cash buyers or very experienced real estate investors.

Q6. Who determines if a condo is warrantable?

Your mortgage underwriter makes the final call. Early in the process, they shoot a Condo Questionnaire over to the HOA to dig into the building's bank accounts, legal standing, and renter ratios. They compare those answers directly against Fannie Mae guidelines.

Q7. Are interest rates higher for a non-warrantable condo?

Yes. Because your local bank or lender cannot easily sell these loans on the secondary market, they are stuck holding the liability. To justify that exposure, they charge a risk premium, typically sitting about 0.5% to 2% above standard market interest rates.

Conclusion: Should I buy a Non-Warrantable Condo?

So, is buying a non-warrantable condo a smart move? I always tell my clients it completely depends on your end game.

- If you have plenty of cash, want a long-term rental property, and negotiated a killer discount, then it might be a brilliant investment.

- But if you're a first-time buyer scraping together a down payment, or you plan to move in three years, I'd strongly suggest looking elsewhere. You just don't want to mess with the higher rates and resale traps.

Whatever you do, don't skip the due diligence. Hire an experienced real estate attorney to read every page of the HOA documents.

If you're stuck trying to figure out if you can even finance a place like this, don't guess. Reach out to a professional Loan Officer today so we can look at your specific financial situation together!

![[Ultimate Guide] How Do I Analyze Self-Employed Tax Returns?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a48809aea04f502e012dac9_analyze-self-employed-tax-returns-banner.png)