![[2026 Read First] What is a Non-Warrantable Condo Loan?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/69d5b904f98358aa9156684d_non-warrantable-condo-loan-banner.png)

Written by

Eric

Share this article

.svg)

Subscribe to updates

You finally spot the perfect condo, only to hear the lender reject it because the building is "non-warrantable." It's a massive letdown for any homebuyer trying to lock down a place. Traditional banks usually walk away from these units, leaving you wondering if you should just give up on the property entirely.

But a rejection from a conventional lender isn't the end of the road. You just need a different type of financing. Let's break down exactly what non-warrantable condo loans are, where to find them, and how you can actually get the keys to your new place.

Key Takeaway

- These loans are built for condos that don't fit the strict warrantability rules set by Fannie Mae or Freddie Mac (FHA spot approvals may apply in limited cases).

- Expect to bring a larger down payment, show a solid credit history, and have a bit more cash saved up compared to a standard mortgage.

- Your best financing bets usually include Portfolio loans, Non-QM products, and Bank Statement programs.

- Talking to a mortgage pro who actually specializes in these quirky properties is your best move to avoid getting denied later on.

What is a Non-Warrantable Condo Loan?

Simply put, a non-warrantable condo loan is a mortgage for a condo that Fannie Mae and Freddie Mac refuse to touch. Normal mortgages require the entire building to be "warrantable." That means the development has to pass strict tests, like having a high percentage of owner-occupants, limited commercial space, and a financially healthy HOA. If a building is packed with renters, acts like a hotel (a condotel), or is caught up in a lawsuit, it instantly gets slapped with the non-warrantable label.

Because regular lenders can't easily sell these loans on the secondary market, they have to keep them on their own books or use private money. Since the lender is taking on the risk themselves, you'll likely see slightly higher interest rates. To offset the property's risk, the underwriter is going to dig deep into your personal finances. They care way more about your ability to repay than whether the building meets some arbitrary government standard.

Also Read:

- Warrantable vs Non-Warrantable Condo: What's the Difference?

- [Explained] What is a Warrantable Condo for Homebuyers?

- 2026 Ultimate Guide: How to Buy a House for the First Time?

Requirements of a Non-Warrantable Condo Loan

Buying a condo outside the normal guidelines means you have to prove you're a safe bet. Lenders are taking a chance on the building, so they need you to look great on paper to balance things out. While every bank has its own playbook, here is what you generally need to bring to the table:

- A heavier down payment: Forget about 3% down. You'll usually need to put down 20% to 30% to get approved.

- Solid credit: Most lenders want to see a score of at least 680, but pushing that past 700 gets you much better terms.

- Plenty of reserves: Be ready to show you have enough cash left over to cover 3 to 6 months of mortgage payments.

- Low debt-to-income (DTI) ratio: Keeping your DTI under 43% shows you aren't biting off more than you can chew.

Also Read:

- Max DTI for Mortgage: Requirements By Loan Types

- [Guide] How to Calculate DTI Ratio for Mortgage?

- Non-Warrantable Condo Guidelines: Verify Eligibility in Seconds

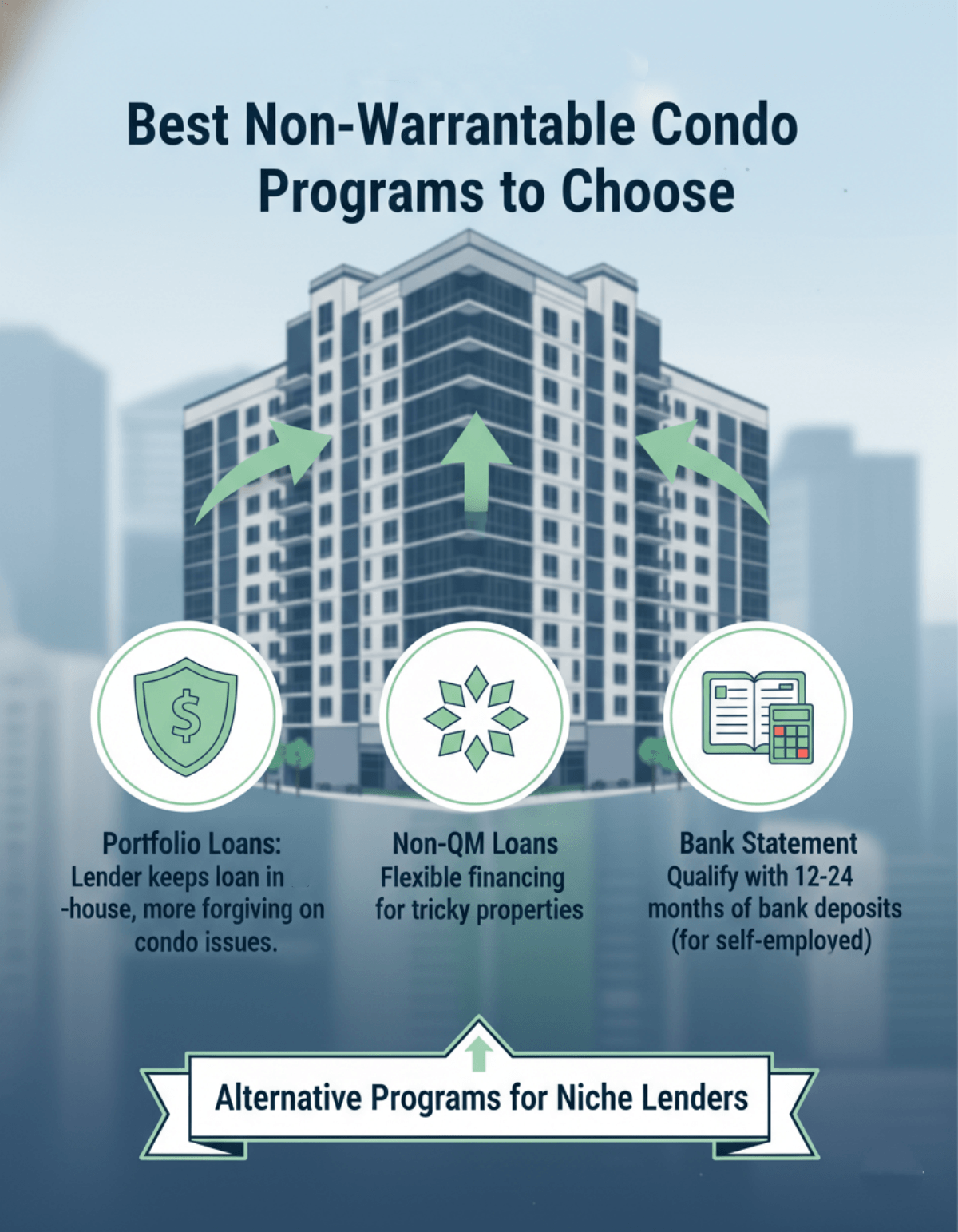

Best Non-Warrantable Condo Programs to Choose

Since a standard mortgage won't work here, you need to look at alternative programs. The good news is that plenty of niche lenders specialize in exactly this kind of real estate. They've built products specifically for buyers who want a non-warrantable unit but have the finances to handle it. If you're looking to buy in 2026, these are the main programs you should target:

- Portfolio Loans: Instead of selling your mortgage to Wall Street, the Non-Warrantable Condo lender keeps the loan in-house. Since it's their money, they make the rules and are way more forgiving about condo project issues.

- Non-QM Loans: Non-Qualified Mortgages are basically the wild card of real estate financing. They are incredibly flexible and perfect for tricky properties like condotels or buildings heavily dominated by investors.

- Bank Statement Programs: If you're self-employed, tax returns rarely tell the whole story. These programs let you qualify using 12 to 24 months of business or personal bank deposits instead, clearing a major hurdle for business owners.

How to Get a Non-Warrantable Condo Loan?

Getting a non-warrantable loan takes a bit more effort than a standard home purchase. Because the property falls into a weird category, you need to be prepared before you even start talking to sellers. Here is a realistic step-by-step approach to locking down the money:

- Get your finances in order: Gather your tax returns, bank statements, and proof of those cash reserves. A strong financial profile is your best leverage.

- Pull the condo documents early: Figure out why the building is non-warrantable. Grab the HOA budget, the master insurance policy, and the condo questionnaire so your lender knows what they are dealing with.

- Find a niche mortgage pro: Don't waste time at a big-box bank. Jump onto Bluerate to find and consult with a local loan officer for free. They know exactly which lenders actually fund these quirky properties and can guide you locally.

- Compare your options: Have your loan officer pull a few different scenarios so you can weigh the interest rates against the down payment requirements.

- Close the deal: Clear underwriting, sign the paperwork, and grab your keys.

What to Consider Before Applying for a Non-Warrantable Condo Loan?

Just because you can get a loan for a non-warrantable condo doesn't automatically mean you should buy it. These units can be fantastic investments or great places to live, but they come with strings attached. Before you hand over an earnest money deposit, make sure you've weighed these factors:

- Tougher resale value: When it's time to sell, your future buyer will likely face the same financing headaches you did. That smaller buyer pool can make the condo harder to unload.

- More expensive financing: Because lenders take on higher risk, you'll usually end up paying slightly higher interest rates and heftier closing costs.

- HOA drama: Sometimes a building is non-warrantable for a really bad reason, like a broke HOA or a massive pending lawsuit. Dig into the condo board's financials so you don't get hit with a surprise assessment later.

- Less competition: The silver lining? Since conventional buyers can't touch these units, you might snag the place at a noticeable discount.

FAQs About a Non-Warrantable Condo Loan

Q1. What is the best non-warrantable Condo Loan?

A Portfolio loan or a Non-QM mortgage usually takes the top spot. Since these don't follow Fannie Mae or Freddie Mac's rigid rulebook, lenders can actually use common sense to approve your application based on your personal financial strength.

Q2. What are non-warrantable condo guidelines?

The rules really depend on the lender. They'll definitely look at why the building failed the standard test, like checking the HOA budget or looking for lawsuits. But mostly, their guidelines focus heavily on making sure you have a low DTI, a great credit score, and plenty of cash reserves.

Q3. What is the minimum down payment for a non-warrantable condo?

You can sometimes find lenders willing to accept 10% or 15% down. However, the reality is that most programs will ask for at least 20% to 30% down to get you a decent interest rate and push the approval through smoothly.

Q4. What is the minimum credit score for a non-warrantable condo?

Aim for at least a 680 to give yourself a fighting chance. If your score is hovering around 640 or 660, you aren't completely out of luck, but you'll likely need to bring a much larger down payment to convince a Non-QM lender to take the deal.

Q5. What are the red flags when buying a condo?

Watch out for HOAs with empty reserve accounts, a ton of deferred maintenance on the building, or a high number of owners who are behind on their dues. Active lawsuits or upcoming special assessments are also massive warning signs you shouldn't ignore.

Final Word

Buying a non-warrantable condo might feel like an uphill battle, but it's far from impossible if you know where to look. Yes, you have to jump through a few extra hoops. You'll likely need a bigger down payment, a cleaner credit history, and maybe stomach a slightly higher interest rate. But in return, you get access to properties that conventional buyers simply can't touch.

Whether you end up using a Portfolio loan or a Non-QM product, the secret is teaming up with a mortgage professional who actually understands this space. Take a hard look at the building's HOA financials, get your own paperwork organized, and you'll be well on your way to securing the perfect condo in 2026, even if traditional banks won't give it a second glance.

People Also Read

- Bank Statement Mortgage Guidelines: What Is It? How to Verify?

- Non-QM Loan Guidelines: How to Check and Verify with AI Accuracy

- 8 Best Non-QM Mortgage Lenders: Which to Choose?