Written by

Eric

Share this article

.svg)

Subscribe to updates

I've seen it happen countless times: a buyer falls in love with a gorgeous downtown condo, only to have their mortgage denied at the last minute. Or maybe you're a new loan officer staring at a rejected file, wondering what went wrong. Buying a condo isn't just about the physical unit. You are buying into the financial health of the entire community.

That's where the concepts of warrantable vs non-warrantable condos come into play. Government-backed agencies like Fannie Mae (FNMA) and Freddie Mac (FHLMC) have strict rules about what they will finance. Let me walk you through how to spot the difference, avoid heartbreaks, and find the right loan for your situation.

Key Takeaways

- Warrantable condos meet strict Fannie Mae and Freddie Mac guidelines, qualifying for standard, low-interest conventional loans.

- Non-warrantable condos don't fit these traditional rules, requiring specialized financing like portfolio or Non-QM loans.

- The biggest differences lie in your wallet: non-warrantable properties typically demand larger down payments (often 20%+) and carry higher interest rates compared to warrantable ones.

What is a Warrantable Condo?

In simple terms, a warrantable condo is a property that fully complies with the lending guidelines set by major mortgage entities, specifically Fannie Mae, Freddie Mac, the FHA, or the VA. When a condominium project checks all their boxes, lenders can confidently approve your conventional mortgage, knowing they can later package and sell that loan on the secondary mortgage market.

For you as a homebuyer, buying a warrantable property is incredibly beneficial. It means the building is considered low-risk and financially sound. Because the lender's risk is minimized, you get access to the most attractive financing options available. You can enjoy lower interest rates, flexible terms, and you might even qualify with a down payment as low as 3% to 5%. Essentially, "warrantable" translates to a smoother, cheaper, and far less stressful borrowing experience.

What is a Non-Warrantable Condo?

By process of elimination, a non-warrantable condo is simply any project that fails to meet those strict government agency standards. But I need to clear up a massive misconception right now: "non-warrantable" does not necessarily mean it's a bad property.

Some of the most luxurious high-rises or unique buildings fall into this category. Common examples include condotels (condos operating like hotels), projects still under active construction, or communities currently facing significant legal disputes. Sometimes it's just a technicality in the homeowner's association (HOA) budget. It just means the property's risk profile doesn't fit neatly into a traditional lending box. Since Fannie Mae won't buy these loans, mainstream banks usually won't touch them. To buy one, you'll need cash or alternative financing routes, like Non-QM (Non-Qualified Mortgage) or portfolio loans held directly by specialized lenders.

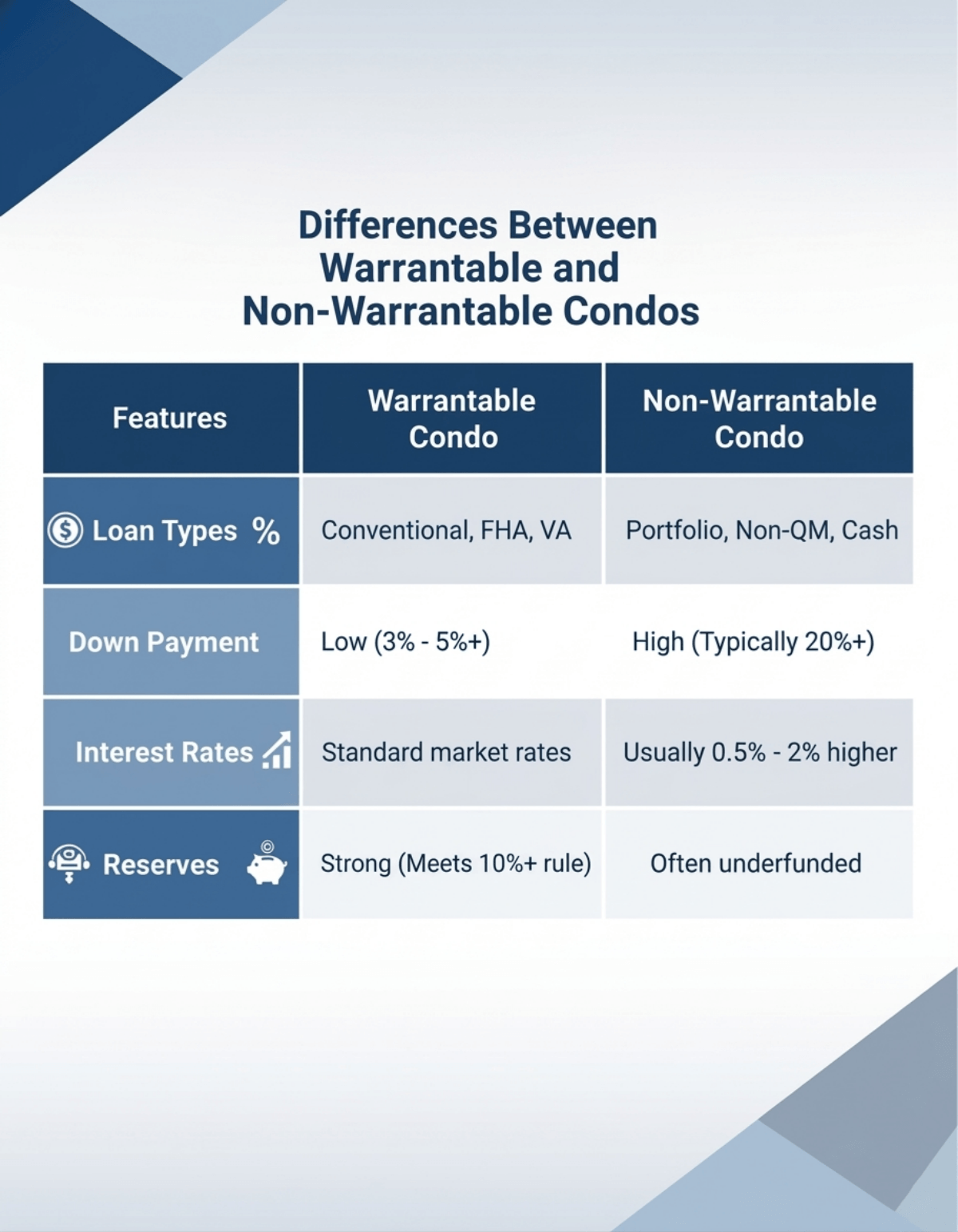

Differences Between Warrantable and Non-Warrantable Condos

The gap between these two property types comes down to financial metrics and how the community operates. Here is a quick breakdown of what lenders look at when classifying a project, which I'll explain in detail below.

Financing

The type of mortgage you can use completely shifts depending on the property's status. Warrantable properties make standard conventional, FHA, and VA financing available, following Fannie Mae and Freddie Mac guidelines. These are the highly regulated, standardized products most buyers use.

If the building is non-warrantable, traditional lenders will issue a hard denial. Instead, you must pivot to alternative lenders offering portfolio loans or Non-QM products. These are mortgages that the bank or private lender intends to keep on their own balance sheet rather than sell to Fannie Mae. Because they make their own rules, they can accept the unique risks of the property, though it usually requires working with a specialized mortgage broker to find them.

Down Payment

Your initial cash outlay looks very different between the two. If you are purchasing a warrantable primary residence, standard loan programs might let you walk away with as little as a 3% to 5% down payment. It's highly accessible for first-time buyers.

Conversely, non-warrantable condos almost always require a much heavier upfront investment. Because the lender is taking on a non-traditional asset, they want more skin in the game from you. While a few niche programs might allow 10% down, the vast majority of portfolio and Non-QM lenders will ask for at least 20% to 30% down. If it's a severe case, like a condotel, expect the down payment demands to climb even higher.

Rates

Interest rates follow risk. Since warrantable units meet stringent federal guidelines, they represent the lowest possible risk to the mortgage industry. Consequently, you are rewarded with standard, competitive market interest rates.

When financing a non-warrantable unit, prepare for a rate bump. Lenders are retaining this loan on their own books (portfolio lending) and accepting a higher risk of default or property devaluation. To offset that exposure, they usually charge interest rates anywhere from 0.5% to 2% higher than what you'd get on a conventional mortgage. Over a 30-year term, that extra percentage point adds up significantly, making your monthly payments noticeably steeper compared to a standard property.

Owner Occupancy

Lenders closely examine who actually lives in the building. A community heavily populated by actual homeowners is considered much more financially stable. For a condo to remain warrantable, agencies require that no more than 50% of the units are investor‑owned rentals, meaning at least 50% must be owner‑occupied or used as second homes. This rule applies regardless of whether you are buying a primary residence or an investment unit.

When a building turns into an investor paradise, say, 60% or 70% of the units are rented out to tenants, the project quickly becomes non-warrantable. Lenders fear that transient renters don't maintain the property as well as owners, and out-of-state investors might be quicker to walk away from HOA dues during an economic downturn.

Litigation

Lawsuits are a massive red flag in the mortgage world. If the HOA is actively involved in major litigation, especially cases regarding structural soundness, safety, habitability, or significant financial disputes, Fannie Mae will immediately classify the entire project as non-warrantable. They won't risk lending on a building that might face a multi-million-dollar judgment.

However, a savvy loan officer knows that not all lawsuits kill a deal. Minor slip-and-fall claims covered by the association's insurance, or small disputes over neighborhood rules, usually won't affect the warrantability. The key is reviewing the exact nature of the lawsuit. But if it's a massive construction defect claim against the developer, conventional financing is completely off the table.

Reserves

A condo's reserve account is essentially its savings account for rainy days, like a roof replacement. Under Fannie Mae's "10% Rule", an HOA must allocate at least 10% of its annual budgeted assessment income to a replacement reserve fund. Projects that fall below this threshold are not eligible for warrantable status.

In practice, many lenders and boards aim for significantly higher reserve contributions, often 15% or more, to strengthen long‑term financial stability without triggering Fannie Mae disqualification.

As someone who reviews these files daily, I'll add a crucial update: agencies are getting even stricter post-Surfside. Lenders now demand fully funded reserve studies, and recent Fannie Mae guideline adjustments are pushing that reserve requirement closer to 15%. If an HOA has been keeping dues artificially low by neglecting their savings, buyers will be punished by losing access to normal financing until the community raises its assessments.

Commercial Space

Mixed-use buildings are incredibly popular in urban areas, who doesn't love having a coffee shop right in their lobby? But there is a strict limit. Fannie Mae guidelines mandate that no more than 35% of the total square footage of the building can be dedicated to commercial space.

If commercial space, like retail stores, restaurants, or offices, exceeds 35% of the building's total square footage, the project is generally classified as non‑warrantable under Fannie Mae guidelines. Agencies enforce this rule because they want to finance residential homes, not commercial enterprises. A heavy commercial footprint changes the traffic, noise, and overall risk profile of the building, meaning buyers there will have to rely on portfolio lenders to get the deal done.

Single Entity Ownership

A healthy condo association relies on diversified ownership. If a single individual, investor group, or corporation owns too large a piece of the pie, they gain oversized voting power and pose a concentrated financial risk.

Under current Fannie Mae rules, for projects with 21 or more units, a single entity generally cannot own more than 20% of the total units, and Fannie treats exceeding this threshold as a reason to classify the project as non‑warrantable. If a wealthy investor buys up 30% of the building to use as long-term rentals, the entire complex becomes non-warrantable. Lenders know that if this one major investor goes bankrupt and stops paying their HOA dues, the entire community's budget could collapse, dragging everyone else's property values down with it.

Can a Non-Warrantable Condo Become Warrantable?

Yes, absolutely! A condo's classification isn't a permanent tattoo. It is dynamic and can change as the community evolves. A project that is unfinanceable today might be perfectly fine next year.

Here are the most common scenarios where a community regains its warrantable status:

- Litigation resolved: Once a major structural lawsuit is settled or dismissed, the red flag is removed.

- Reserves fixed: The HOA increases monthly dues to meet the mandatory 10% (or higher) reserve allocation.

- Construction finishes: A new development finally completes its last phase and turns control over to the homeowners.

- Ownership diversifies: A major investor sells off enough units to drop below the 20% single-entity threshold.

As a buyer or loan officer, your best tool is the Condo Questionnaire. You can ask the HOA to fill this out periodically to verify the community's most up-to-date financial and legal status before submitting an offer.

FAQs About Warrantable vs Non-Warrantable Condo

Q1. What does it mean when someone asks if a condo is warrantable?

They are asking if the property meets the specific lending guidelines set by Fannie Mae and Freddie Mac. If it does, the buyer can easily purchase the unit using a standard, low-interest conventional mortgage. If not, they will need alternative financing.

Q2. What makes a condo non-warrantable in FNMA?

Fannie Mae considers a condominium project non‑warrantable if it fails to meet any one of several key criteria. The most common reasons include inadequate reserve funds (allocating less than 10% of the annual budget), excessive commercial space (over 35% of the building's square footage), active structural litigation, a single entity owning more than 20% of the units, or the project operating like a hotel (condotel).

Q3. What is the minimum down payment for a non-warrantable condo?

While a few rare non‑QM programs might allow 10% down, for most borrowers you should generally expect a minimum down payment of 20%. Depending on the specific risk factor, like it being a condotel, some portfolio lenders will require 25% to 30% upfront to approve the loan.

Also Read: Non-Warrantable Condo Guidelines: Verify Eligibility in Seconds

Q4. How to buy a non-warrantable condo?

You cannot use a standard bank loan. Instead, you need to find a mortgage broker who specializes in portfolio loans or Non-Qualified Mortgages (Non-QM). These private lenders look past Fannie Mae rules. Alternatively, you can bypass financing altogether and pay entirely in cash.

Also Read: Best Non-Warrantable Condo Lenders Near Me in 2026

Q5. Is a non-warrantable condo a bad investment?

Not necessarily. Because they are harder to finance, you face less buyer competition and can often negotiate a lower purchase price. If the HOA fixes the issues (like settling a lawsuit) and the building becomes warrantable later, your property value could see a significant jump.

Conclusion

Ultimately, the difference between a warrantable and non-warrantable condo boils down to financing ease and cost, rather than the physical quality of the home itself. A non-warrantable status simply means the community's financial layout or legal situation doesn't align with standard federal guidelines, pushing you toward higher rates and larger down payments.

Before you fall in love with a property and write an earnest money check, protect yourself. I highly recommend having your loan officer request and review the HOA's Condo Questionnaire upfront. Catching a red flag early saves everyone time and heartbreak. If you do encounter a non-warrantable situation, don't panic—just be prepared to pivot to a specialized mortgage broker who knows exactly how to navigate portfolio and Non-QM loans.

People Also Read

- Non-QM Loan Guidelines: How to Check and Verify with AI Accuracy

- Max LTV: Check Maximum Loan-to-Value Ratios By Loan Types

- Max DTI for Mortgage: Requirements By Loan Types

- AI Mortgage Underwriting Explained: Will You Be Replaced?

- Ultimate Guide: How to Calculate LTV Ratio for Mortgage?

- [Read First] What is a Non-Warrantable Condo Loan?

![[Ultimate Guide] How Do I Analyze Self-Employed Tax Returns?](https://cdn.prod.website-files.com/6731bc6e813a541b54c30b10/6a48809aea04f502e012dac9_analyze-self-employed-tax-returns-banner.png)