Written by

Eric

Share this article

.svg)

Subscribe to updates

Last week, I ran a desktop underwriting approval for a client with a 610 credit score. The system gave us a green light, but the funding lender suddenly rejected the file because of their internal rules. This is the frustrating reality of mortgage lender overlays. As a loan officer, I see these hidden guidelines derail deals constantly. Let's look at what these overlays are and how we can navigate them.

Key Takeaways

- Stricter Rules: Overlays are extra requirements that lenders add on top of standard agency guidelines.

- Common Hurdles: They usually target credit scores, debt-to-income (DTI) ratios, and employment verification.

- Smart Solutions: Comparing wholesale lenders or using automated assistant tools helps you bypass these roadblocks and close loans faster.

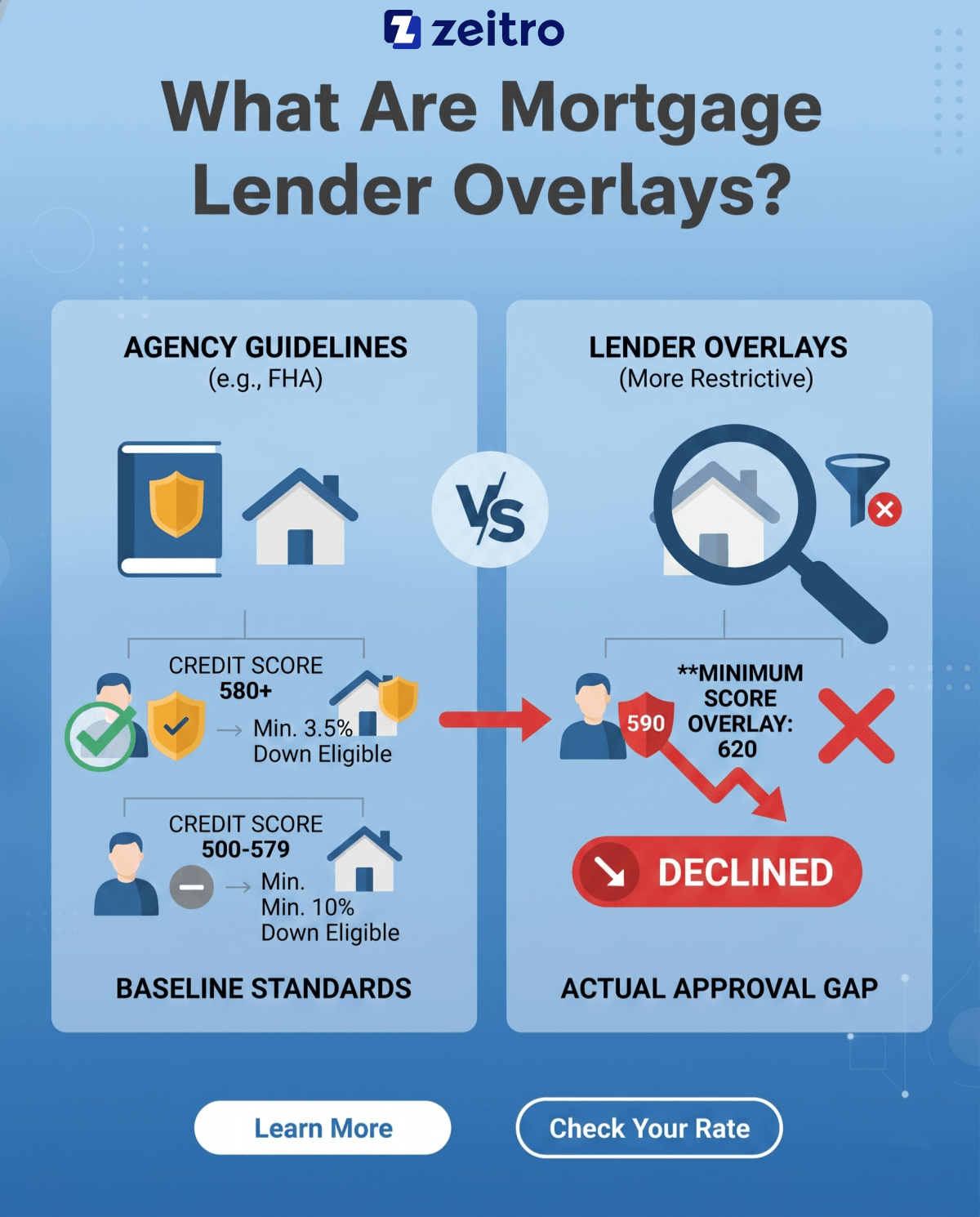

What Are Mortgage Lender Overlays?

To understand overlays, we have to look at how mortgage guidelines work. Standard rules are set by agencies like Fannie Mae or the Federal Housing Administration. These are the baseline standards a borrower must meet, though final approval may also depend on automated findings and lender-specific policies. However, lenders rarely stop there. They establish their own overlay rules that are usually more restrictive than agency guidelines.

For example, FHA guidelines generally allow a 3.5% down payment with a credit score of 580 or higher, while borrowers with scores from 500 to 579 may still qualify with 10% down. Yet, many wholesale lenders I work with enforce a minimum score overlay of 620. If my client has a 590 score, they may be eligible under FHA rules, but they would be declined by a lender that enforces a 620 minimum score overlay. It creates a massive gap between federal eligibility and actual approval.

Why Do Lenders Impose Overlays on Mortgages?

Mortgage lenders are not trying to make our lives difficult. They are simply managing their financial risk. When a lender originates a loan, they often sell it on the secondary mortgage market to investors. If a borrower defaults shortly after closing, the investor can force the lender to buy back the bad loan. This buyback risk can significantly hurt a lender's liquidity.

To protect themselves, individual institutions build extra safety margins. They look at risk layering, combining multiple marginal factors like high DTI and low credit, and use overlays to filter out files that fall outside their specific risk tolerance, even if a government program technically allows them.

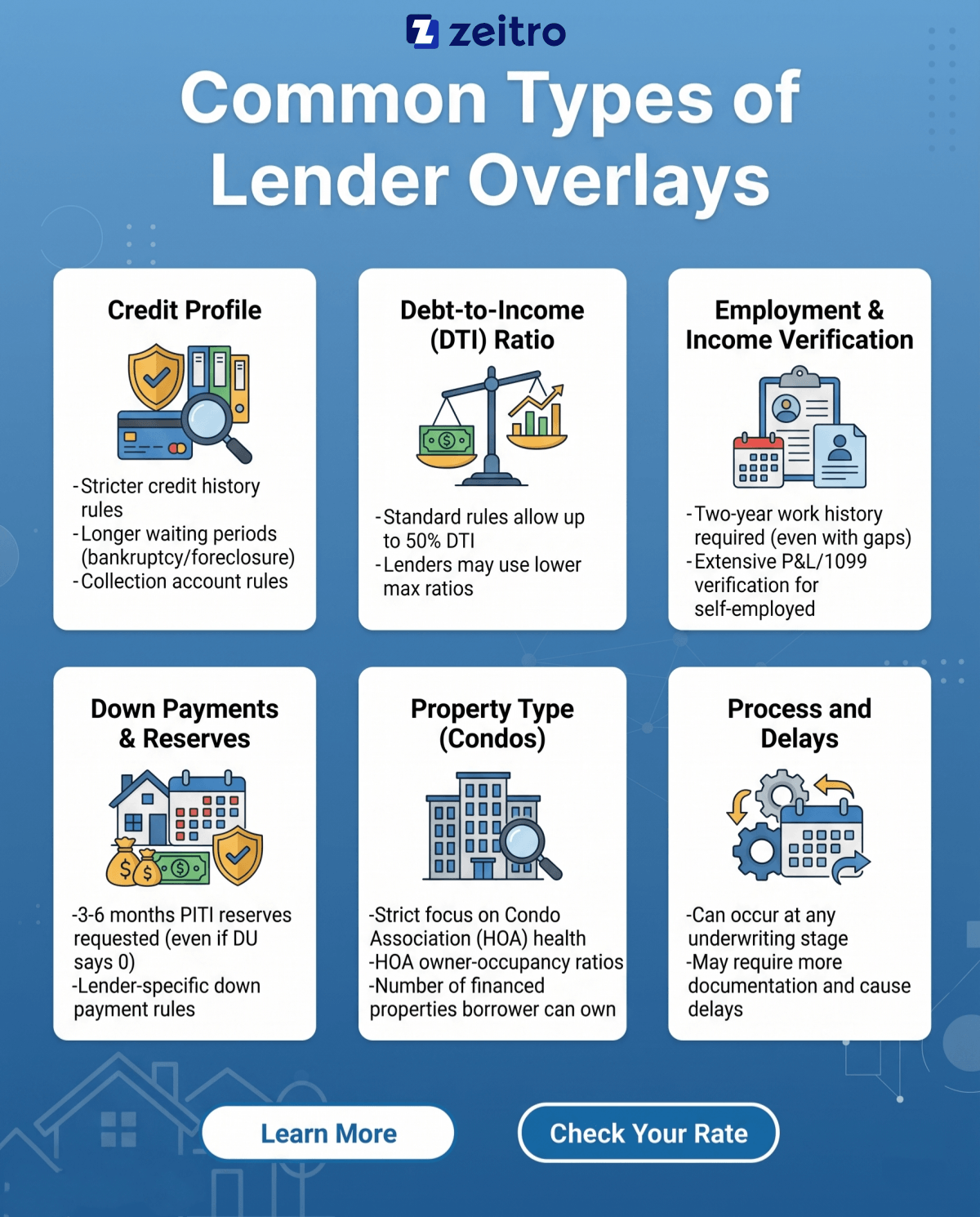

Common Types of Lender Overlays

Navigating these restrictions requires knowing where they usually hide. Overlays can show up at any point during underwriting, but they typically target a few core areas:

- Credit Profile: Beyond minimum scores, lenders often create overlays around credit history. They might require longer waiting periods after a bankruptcy or foreclosure than standard agency rules dictate, or they may require borrowers to pay certain collection accounts or meet stricter handling rules before closing.

- Debt-to-Income (DTI) Ratio: Fannie Mae's Desktop Underwriter can allow DTIs up to 50% for some case files, depending on the loan profile and automated findings.

- Employment & Income Verification: Lenders often require a two-year work history, though not every file needs uninterrupted employment with no gaps, even if agency guidelines allow for shorter periods. For self-employed clients, they might demand extensive profit and loss (P&L) statements and 1099 histories that go beyond standard requirements.

- Property Type: Condos are a prime target. Many lenders impose strict overlays regarding HOA financial health, owner-occupancy ratios, or the number of financed properties a borrower can own.

- Down Payments & Cash Reserves: Even if an automated approval requires zero reserves, a lender might demand three to six months of principal, interest, taxes, and insurance (PITI) as a buffer.

Can You Avoid Lender Overlays?

Yes, we can absolutely avoid overlays by working with mortgage brokers who have access to multiple wholesale lenders. Because different lenders have different risk tolerances, an overlay that stops a loan at one bank might not exist at another. The challenge isn't finding a lender. It is finding the right one quickly before your borrower gets discouraged by a denial. That is where modern technology makes a difference.

Zeitro Strata: How to Instantly Check and Verify Lender Overlays

In my daily work, manually reading through 500-page PDF guideline sheets from dozens of investors used to take hours. To solve this, I started looking into tools like Zeitro Strata AI. It functions as an AI-powered mortgage guideline assistant that lets loan officers run deep searches across more than 100 investors.

Instead of guessing if a lender has a credit score or DTI overlay, you can ask direct or broad questions and receive parsed, accurate answers in seconds. This utility is especially helpful for complex Non-QM loans like bank statement or DSCR programs, where guidelines change rapidly.

- Comprehensive Guidelines: It pulls data from leading lenders like AAA Lending, AD Mortgage, CMG Financial, and Greenbox, covering over 1,000 guidelines (including Asset Utilization, ITIN, Jumbo, and FHA).

- Citation-Backed Accuracy: The assistant provides direct source citations for every answer. This minimizes AI hallucinations and allows us to verify the exact page in the guideline to stay confident.

- Custom Tags and Filters: You can apply specific filters like DSCR or loan type to narrow your search to the exact programs your client needs.

- Advanced Income & DPA Matching: Beyond overlays, you can upload documents to automate income calculations, check Area Median Income (AMI) limits, and search for local Down Payment Assistance (DPA) programs.

FAQs About Mortgage Lender Overlays

Q1. What is the difference between agency guidelines and lender overlays?

Agency guidelines are the baseline requirements set by organizations like Fannie Mae or the FHA to establish loan eligibility. Lender overlays are stricter, optional guidelines added by individual lending institutions to protect themselves from borrower default.

Q2. Do overlays apply to Non-QM (Non-Qualified Mortgage) loans?

Yes. Non-QM investors design their own programs and guidelines. If a retail lender or broker-dealer adds a more restrictive requirement on top of an investor's standard program, that represents a Non-QM lender overlay.

Q3. Can a lender waive an overlay for a strong borrower?

It is rare. Overlays are usually built directly into the lender's underwriting software and credit policy. Instead of trying to get a waiver, it is usually much faster to move the file to a lender without that overlay.

Q4. Why do different lenders have different overlays for the same FHA loan?

Lenders have different risk tolerances, capital reserves, and business models. A large bank might use strict overlays to target only pristine borrowers, while a wholesale lender might accept higher risk to win more business.

Q5. How often do lenders update their overlays?

Lenders update overlays frequently, especially during volatile market conditions. Because these rules shift quickly based on secondary market demands, relying on printed guidelines or static PDFs often leads to outdated information.

Conclusion

Lender overlays can easily turn a promising loan application into a sudden denial, costing you time and client trust. However, once you understand how to navigate them, you can turn these obstacles into an advantage. Instead of spending hours reading through outdated PDF files, using a dedicated assistant can help you clear underwriting hurdles before they even arise.

Tools like Zeitro Strata AI streamline this process by verifying guidelines across multiple wholesale lenders in seconds. They offer ten free queries daily, making it easy to test how it fits into your workflow. By adopting these methods, you can work more efficiently and help more of your clients buy their homes.

Loan Officers Also Try

- Zeitro Mortgage Pricing Tool for Loan Pros

- Zeitro Mortgage Employment Income Calculator for Loan Pros

- Zeitro DSCR & Rental Income Calculator for Mortgage

- Zeitro Down Payment Assistance Search Tool