Written by

Eric

Share this article

.svg)

Subscribe to updates

If there is one company that divides opinion more than any other, it's Better Mortgage. One user claimed they saved $4,000 in fees effortlessly, while another posted a horror story about being "ghosted" three days before closing.

In 2026, with interest rates still being the biggest hurdle for homebuyers, the promise of a "no-commission, digital-first" lender is incredibly tempting. But is the lower price tag worth the potential lack of human support? I've analyzed their latest terms, tested their famous "One Day Mortgage" claim, and dug into thousands of borrower reviews to give you the unvarnished truth. Here is my deep dive into whether Better Mortgage is a brilliant hack for saving money or a headache waiting to happen.

What Is Better Mortgage?

Better Mortgage (NMLS ID #330511) isn't your grandfather's bank. Better Mortgage launched its mortgage services in 2016, but the parent company Better.com was founded by Vishal Garg in 2014. It launched with a specific mission: to digitize the mortgage process and eliminate the "middleman."

Most traditional lenders employ Loan Officers who earn a commission, which is usually 1% to 2% of the loan amount on every deal they close. Better.com removed this layer entirely. Instead, they use non-commissioned support staff and a proprietary algorithm (affectionately dubbed "Tinman") to underwrite loans.

By 2026, they have solidified their position as a Direct Lender. This means they lend their own money rather than just brokering the deal to someone else. For you, this business model supposedly translates to lower rates and zero lender fees but as we'll see, a purely digital approach isn't for everyone.

Better Mortgage Pros and Cons: A Quick Snapshot

No lender is perfect. In my analysis, Better Mortgage is a tool, exceptional for some jobs, but terrible for others. Here is the high-level breakdown:

Pros

- Zero Lender Fees: They genuinely do not charge origination, application, or underwriting fees. This alone can save you $1,000-$2,000 compared to big banks, as traditional origination fees often range from 1% of the loan or $995–$1,500 flat.

- One Day Mortgage™: They can issue a Commitment Letter which carries more weight than a pre-approval, in 24 hours if you link your bank accounts digitally.

- Better Price Guarantee: If you find a competitor with a better price, they promise to match it (and historically have offered $100 credits if they match).

- Speed: Their automated system runs 24/7. You can get pre-approved at 2 AM on a Sunday.

Cons

- Inconsistent Human Support: You don't get a dedicated Loan Officer. You get a "team," meaning you might talk to a different person every time you call.

- Strict on "Weird" Income: If you are self-employed with complex tax write-offs, their algorithm often struggles to approve you.

- No USDA Loans: As of early 2026, they still do not offer USDA loans for rural properties.

- Rate Volatility: While often lower, their rates can change rapidly based on market algorithm shifts.

Loan Options & Services: What Does Better Offer?

Better isn't a niche lender anymore. They offer a full suite of products. However, their menu is tailored toward the "standard" borrower.

Purchase Loans (FHA, VA, Conventional)

I checked their current roster, and they cover the "Big Three":

- Conventional Loans: Standard fixed-rate (15 or 30 years) and adjustable-rate mortgages (ARMs).

- FHA Loans: Great for first-time buyers with lower credit scores (minimum 580 usually required).

- VA Loans: For veterans and active military. Better is known for offering competitive rates here, though they don't always have the specialized military expertise of a lender like Veterans United.

They generally do not support USDA loans or construction loans.

Refinance Options (Cash-Out & Rate-and-Term)

This is Better's bread and butter. Because refinancing is usually less time-sensitive than buying a home, their digital model shines here.

- Rate-and-Term: Purely to lower your interest rate or change the loan length.

- Cash-Out: If you have built up equity, you can refinance for a larger amount and take the difference in cash.

One Day Mortgage™: How It Works

This is their flagship feature for 2026. Most lenders take days to underwrite a file. Better claims to do it in 24 hours.

It's legit, but there is a catch. You must link your bank accounts (via Plaid) and upload your paystubs within 4 hours of locking your rate. If you do this, they provide a "Commitment Letter."

In a bidding war, a Commitment Letter beats a Pre-approval letter every time because it means an underwriter has already vetted your finances.

HELOC & Home Equity Lines

If you don't want to lose your low interest rate on your main mortgage, Better offers a HELOC (Home Equity Line of Credit).

They advertise funding in as fast as 7 days. I noticed they often waive appraisal fees for HELOCs by using automated valuation models (AVMs), which keeps closing costs very low.

Better Cover (Insurance) & Better Real Estate Services

They want to be your "One-Stop Shop."

- Better Cover: This is an insurance aggregator that lets you shop for homeowners insurance during the loan process.

- Better Real Estate: If you use one of their partner real estate agents, they often offer a discount on closing costs, which is historically around $2,000, but check current terms.

Better Mortgage Rates, Fees, and Closing Costs

This is the main reason you are reading this review. Are they actually cheaper?

The "Zero Lender Fee" Promise

Yes, it is real. Most banks charge a 1% "Origination Fee" or a flat "Admin Fee" of $995 to $1,500. Better charges 0 for this. On a $400,000 loan, that is an instant saving.

The "Hidden" Costs

However, "No Lender Fees" does not mean "No Closing Costs." You will still pay:

- Third-Party Fees: Appraisal, Credit Report, Title Insurance, and Government Recording Fees.

- Escrows: Property taxes and insurance pre-payments.

- Points: Watch out for this. Sometimes Better shows a very low interest rate, but if you look closely at the Loan Estimate, it might require you to pay "Discount Points" upfront to get that rate. Always check Section A of your Loan Estimate.

Special Features & Incentives

Beyond the standard loans, Better uses aggressive incentives to win business.

The Better Price Guarantee

I love this feature for negotiation. If you get a Loan Estimate from a competitor like Rocket or a local broker, that has a lower APR for the same loan terms, Better will match it. In the past, they have even credited customers $100 if they honor the match.

Even if you don't plan to use Better, get a quote from them to force your local lender to drop their price.

Better Real Estate Agent Match

They have a network of partner agents. If you buy a home with one of them, Better typically applies a discount to your closing costs. While the discount is nice, ensure the agent knows your local market. Don't hire a bad agent just to save $2,000 on a $500,000 purchase.

Better Mortgage Customer Reviews & Reputation

Marketing is one thing. User experience is another. I analyzed sentiment across major platforms for 2025-2026.

Positive Feedback (Trustpilot, Zillow, Credit Karma)

Ratings vary by platform: Trustpilot shows around 3.9/5 ("great"), but some recent aggregates dip to 2.3/5 ("poor"). BBB holds an A- rating.

Tech-savvy users love them. Reviews frequently mention "fastest process ever," "loved not talking on the phone," and "saved huge money on fees." The One Day Mortgage feature is heavily praised by people who needed to close quickly.

Common Complaints & Issues

The negative reviews are specific and concerning. The most common complaint is "Ghosting." Because there is no single commission-based loan officer, files sometimes get stuck in limbo if an issue arises.

Borrowers with slightly complicated income (freelancers, recent job changes) report that Better's underwriters ask for the same documents repeatedly or deny the loan at the last minute.

Better Mortgage BBB Rating & History

Better.com generally maintains a B to A- rating with the Better Business Bureau (BBB). They are accredited, which means they pay to be there, but they also respond to complaints.

You will see a spike in complaints from 2022-2023 regarding layoffs, but recent 2025-2026 feedback shows operations have stabilized.

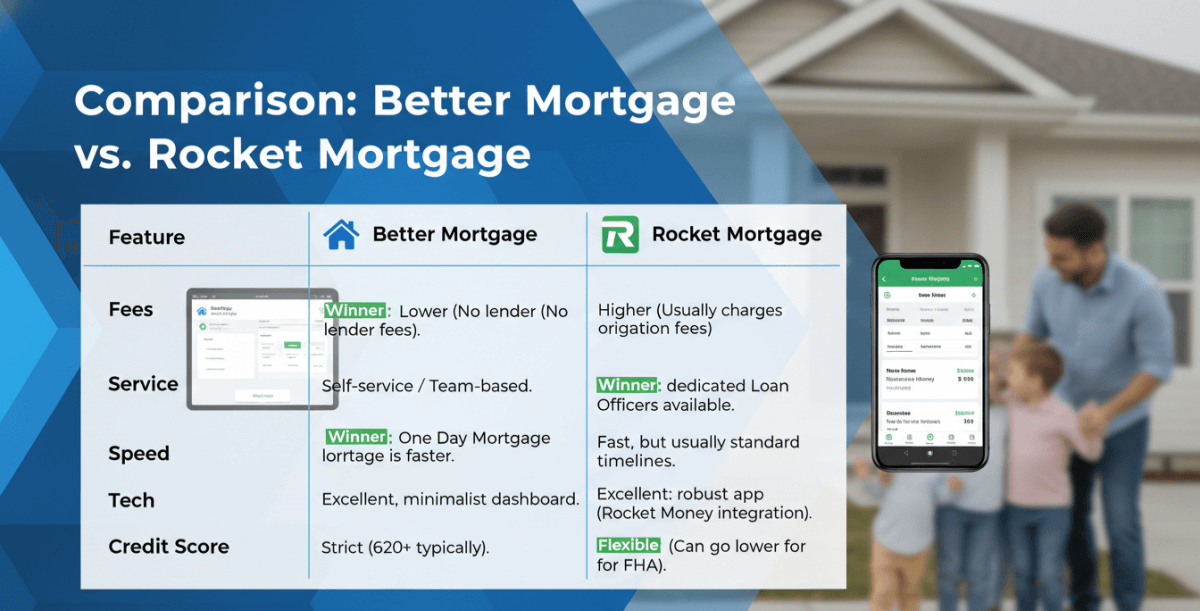

Comparison: Better Mortgage vs. Rocket Mortgage

These are the two giants of online lending. How do they compare?

- Choose Better if you are price-sensitive and have a simple financial profile.

- Choose Rocket if you are a first-time buyer who needs someone to answer the phone and walk you through every step.

Frequently Asked Questions (FAQs)

Is Better Mortgage legitimate and safe?

Yes. They are a fully licensed lender (NMLS #330511) regulated by federal and state laws. They have funded billions in loans and are a public company (Better Home & Finance).

Why are Better Mortgage rates lower than others?

It comes down to overhead. They don't have physical branches, and they don't pay loan officers commissions. They pass those operational savings on to you in the form of lower rates.

What credit score is required for Better Mortgage?

Minimum credit scores are 620 for conventional loans, 580 for FHA loans, and 620 for VA loans (higher than some competitors for VA).

Does Better Mortgage charge origination fees?

No. They famously charge $0 in origination fees, underwriting fees, or application fees.

Who owns Better.com?

Better is a publicly traded company. It was founded by Vishal Garg, who remains the CEO. SoftBank was famously a major early investor.

The Verdict: Should You Use Better Mortgage?

After reviewing the data for 2026, my verdict is that Better Mortgage is an excellent financial tool, but a mediocre service provider.

You should use Better Mortgage if:

- You are a W-2 employee with a steady paycheck and good credit (700+).

- You are comfortable uploading documents and managing tasks online without help.

- You want the absolutely lowest closing costs possible.

- You are doing a simple refinance.

You should avoid Better Mortgage if:

- You are self-employed with complex tax returns.

- You are buying a unique property (fixer-upper, rural land).

- You get stressed easily and need a human to reassure you throughout the process.

Even if you don't use them, apply with them. Get their official Loan Estimate. It costs you nothing, and you can show that paper to any other lender and say, "Can you beat this?" That piece of paper is your most powerful weapon in buying a home this year.

People Also Read

- Are Mortgage Rates Expected to Go Down in 2026? Expert Forecasts

- CrossCountry Mortgage Review: Rates, Services, Insights

- AmeriSave Mortgage Review: An Honest Look for Borrowers & LOs

- 8 Best Non-QM Mortgage Lenders: Which to Choose?

- Best DSCR Loan Lenders: Which to Choose from?